Aluminum Rollover Cost: Beyond the Prompt-Date Spread

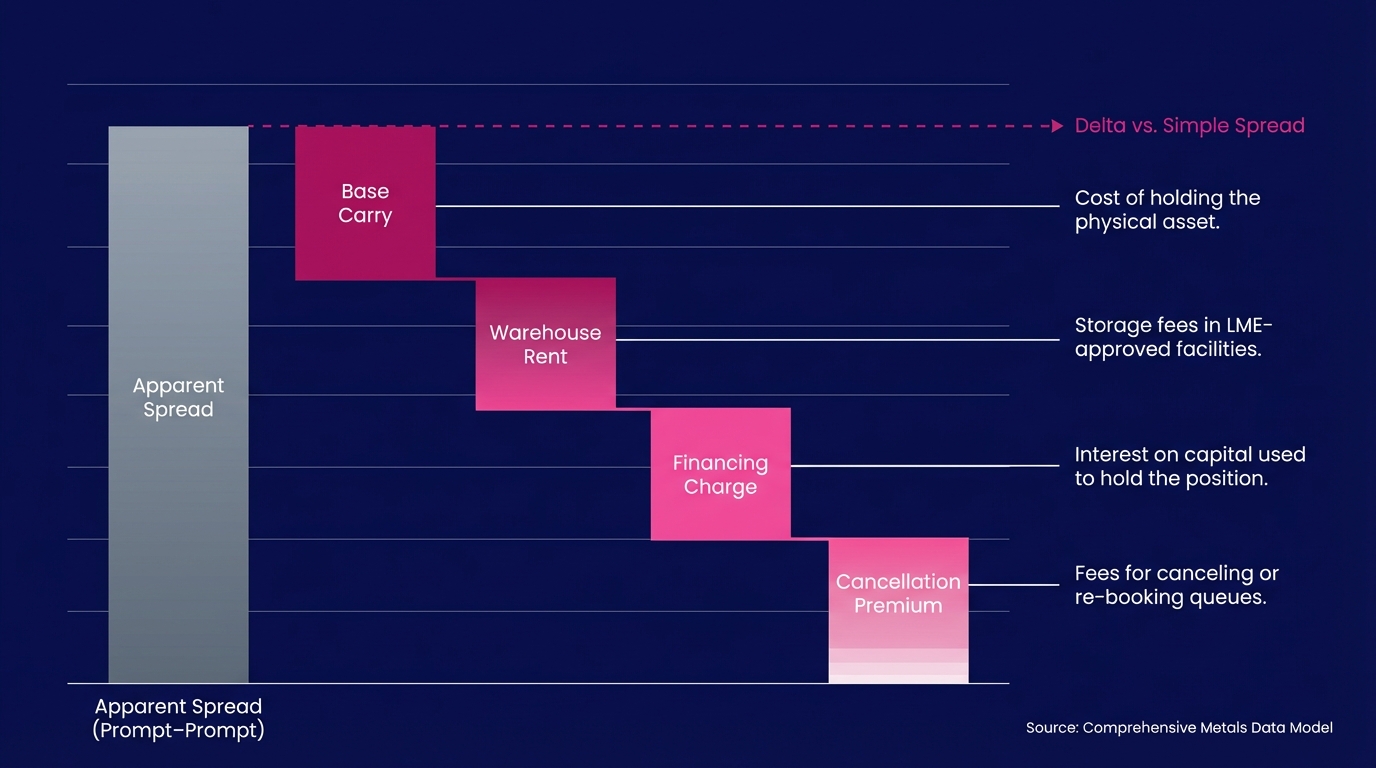

The most consequential gap in aluminum rollover accounting is also the most common. Most desks record rollover cost as the spread between the outgoing and incoming prompt dates. That figure is real. It is also incomplete. The full aluminum rollover cost integrates four discrete components: the prompt-date spread, warehouse rent, financing charges, and cancellation premiums. Each is governed by its own market mechanism and requires its own data source.

LME stock reports show aluminum holdings at LME-approved warehouses averaged over 500,000 metric tonnes across 2023. This establishes warehouse rent as a structurally significant cost variable on any physical-linked position, rather than a rounding error. When the prompt spread trades at near-flat contango or backwardation, the cost components outside the spread can dominate total rollover cost. A data model that does not capture all four will price the transaction incorrectly.

This post decomposes aluminum rollover cost line by line, the way it should appear in a trade settlement memo.

What the Prompt-Date Spread Misses in Aluminum Rollover Cost

The prompt-date spread is the difference in LME aluminum price between two specific delivery dates, typically the outgoing near-leg and the incoming far-leg of a rollover transaction. When the market is in contango, the far-leg price exceeds the near-leg price and the spread is positive. In backwardation, the spread is negative.

Traders commonly read this number as the cost of rolling a forward position. That reading is partially correct and structurally incomplete.

Why Does the Prompt-Date Spread Understate True Rollover Cost?

The prompt-date spread captures only the time-value differential priced into the futures curve at a single moment. It does not account for physical storage obligations attached to warranted metal, the capital cost of funding the position over the roll tenor, or the market-set cost of cancelling a warehouse warrant.

The LME's published pricing methodology designates the cash-to-three-months spread (cash/3M) as the benchmark reference for aluminum carry. However, the fully-loaded rollover cost can diverge from cash/3M by 15, 30% depending on prevailing warehouse queue lengths and the counterparty-specific financing benchmark in effect at the time of the transaction.

A desk that records only the spread is booking a partial transaction cost and deferring the remainder as an unrecognized liability. On a 1,000-metric-tonne position, that unrecognized remainder routinely reaches five figures per roll event, as the assembled cost table in a later section of this post will quantify.

LME aluminum forward curve methodology

LME Warehouse Rent: A Fixed-Rate Cost with Variable Impact

Warehouse rent is the daily storage fee charged by LME-approved warehouse operators for metal held under LME warrant. The LME publishes maximum permissible rates annually, but actual rates are negotiated between warrant holders and warehouse operators within that ceiling and vary by location.

As of the LME's 2023 tariff schedule, the maximum permissible warehouse rent for aluminum is approximately $0.41 per metric tonne per day at most major locations. On a standard 25-metric-tonne LME lot, that rate translates to $10.25 per lot per day. It accrues continuously while the warrant remains live.

How Do LME Warehouse Rents Affect Rollover Pricing?

LME warehouse rent affects rollover cost by accumulating over the full calendar duration between the outgoing prompt date and the incoming prompt date. The longer the roll tenor, the greater the warehouse rent component as a direct, non-negotiable cost to the holder of the warrant. At locations experiencing elevated queue conditions, the effective tenor can extend well beyond the standard three-month horizon.

Research by Metal Bulletin (now Fastmarkets) shows warehouse queues at certain LME locations reached 50-plus weeks during the 2012, 2014 aluminum stock buildup. This effectively multiplied the warehouse rent component by approximately 17 times relative to a standard quarterly roll. Even at normalized queue levels, rent on a 1,000-tonne position over a 90-day roll tenor exceeds $3,690 based on the current maximum tariff rate.

This figure does not appear in the prompt-date spread. It must be sourced separately from the LME warehouse tariff database, cross-referenced to the specific warrant location, and integrated into the rollover cost model as a discrete line item.

The location variable matters independently of the rate. Rent at a warehouse experiencing queue-driven delays may accrue for a longer period than rent at a warehouse with immediate load-out availability, even if both charge identical daily rates. A cost model that applies a generic tenor assumption without warrant-location data will systematically misprice warehouse rent on a portion of any multi-location portfolio.

LME warehouse tariff schedule and approved location list

Financing Charges: The Cost of Carry on Physical-Linked Positions

Financing charges represent the interest cost of funding the aluminum position over the roll period. In a metals-forward rollover, the financing charge compensates the counterparty for the time value of capital deployed to maintain the position from the outgoing prompt date to the incoming prompt date.

The standard calculation follows this structure:

Financing Charge = Notional Value × (Reference Rate + Credit Spread) × (Days / 360)

Notional value equals the LME aluminum settlement price multiplied by lot size in metric tonnes. The reference rate was historically USD LIBOR but transitioned to SOFR (Secured Overnight Financing Rate) following the cessation of panel-bank LIBOR in June 2023.

How Is the Financing Charge Calculated in a Metals Rollover?

For a 25-metric-tonne lot at an aluminum price of $2,300/mt and a SOFR-based all-in financing rate of 5.30%, the financing charge over a 90-day roll period equals approximately $801 per lot. Scaled to a 1,000-tonne position (40 lots), the financing charge reaches $32,040, an amount entirely absent from the raw prompt-date spread.

CME Group transition documentation for metals financing benchmarks notes the LIBOR-to-SOFR migration introduced basis risk for legacy positions referencing term SOFR versus overnight compounded SOFR. This adds a secondary precision requirement: the applicable rate variant must be identified at the transaction level rather than assumed to be uniform across the book.

A data model that pulls the prompt spread without capturing the reference rate variant, the current financing tenor, and the lot-level notional will miscalculate financing charges on every rollover processed. The error direction depends on whether the counterparty's actual funding cost sits above or below the rate implied by the contango; a question the spread alone cannot answer.

Does Contango Fully Compensate for Financing Cost?

Contango in the aluminum forward curve theoretically reflects the cost of carry, which includes financing. In practice, the contango priced into the prompt spread represents market consensus rather than any individual counterparty's funding cost. A desk with above-market funding costs will consistently experience a negative differential between contango received and financing charges paid.

This structural drag accumulates without clear attribution when financing is treated as netted within the spread rather than modeled as a discrete component. It becomes visible only when the P&L attribution review asks why roll economics underperform the curve. By that point, the variance has already settled.

SOFR transition impact on commodity financing benchmarks

Cancellation Premiums: The Variable Traders Most Often Omit

The warrant cancellation premium is the cost charged to cancel an LME aluminum warrant, converting warranted metal from exchange-registered inventory to off-warrant, load-out-ready metal. Cancellation is a prerequisite for physical delivery from an LME warehouse, and the premium is set exclusively by the warehouse operator.

Cancellation premiums are not fixed. They are quoted by individual warehouse operators and vary based on:

- Location premium or discount relative to LME official settlement price

- Queue position at the specific warehouse

- Metal specification, including alloy grade, shape, and LME-approved brand

- Prevailing physical market tightness in the relevant delivery region

What Is a Cancellation Premium in Metals Trading?

A cancellation premium is the above-LME-settlement fee charged to convert an LME warrant into a delivery instruction for physical aluminum load-out. Unlike the prompt-date spread, which reflects a futures-market price differential observable on-screen, the cancellation premium is an over-the-counter rate determined by warehouse operators and physical market conditions that may bear no direct relationship to the futures curve.

Fastmarkets pricing data shows aluminum cancellation premiums at Rotterdam have ranged from $10 to $55 per metric tonne in the post-pandemic period. That range represents a cost of $250 to $1,375 per standard 25-tonne LME lot. At 1,000 metric tonnes, the variance alone ($10 to $55/mt) is $45,000 per roll event.

A rollover model that excludes cancellation premiums fails to approximate the cost with an acceptable margin of error. Instead, it omits a variable with a four-figure per-lot range determined by market conditions entirely outside the futures curve. That constitutes a severe data gap rather than a simplifying assumption.

Cancellation premium data must be sourced from physical market pricing services; Fastmarkets, S&P Global Commodity Insights (Platts), or direct warehouse operator quotation; at the time of each rollover transaction. It cannot be inferred from any futures market input.

Fastmarkets aluminum physical premium methodology

S&P Global Commodity Insights aluminum warrant cancellation data

Assembling the Full Aluminum Rollover Cost

The fully-assembled aluminum rollover cost is the arithmetic sum of all four components, each sourced from its own data feed and calculated at the lot level before aggregation to the position level.

| Cost Component | Data Source | Example: 1,000 mt, 90-day roll |

|---|---|---|

| Prompt-date spread | LME prompt forward curve | Variable: e.g., $18/mt contango = $18,000 |

| Warehouse rent | LME tariff schedule, location-specific | $0.41/mt/day × 90 days = $36,900 |

| Financing charge | SOFR + spread × notional × (days/360) | ~$32,040 at 5.30% SOFR, $2,300/mt |

| Cancellation premium | Physical market service / warehouse operator | $10, $55/mt = $10,000, $55,000 |

| Total rollover cost | Integrated model | $96,940, $141,940 |

In this example, the prompt-date spread represents less than 19% of total rollover cost at the low end of the cancellation premium range. The remaining 81%-plus is invisible to any system that records only the spread.

What Is Included in an Aluminum Rollover Cost?

An aluminum rollover cost includes four components: the prompt-date spread between outgoing and incoming delivery dates, warehouse rent accrued on warranted metal over the roll tenor, the financing charge calculated on the notional position value at the applicable reference rate, and the warrant cancellation premium set by the warehouse operator for the specific location and metal specification. Each component requires a discrete data input and a separate calculation method; none can be derived from another.

Industry surveys by Accenture and Oliver Wyman indicate over 60% of mid-market metals trading desks track rollover costs at the spread level only, with supplemental components captured in spreadsheets or reconciled manually after settlement. This is the quantified gap between what trading operations believe they are measuring and what they are actually measuring in their position management systems.

The table above also illustrates why rollover cost variance is so difficult to attribute in post-settlement reviews when the cost model is underspecified. When the total is off, there is no component record that locates the error; only a residual that disappears into trading P&L.

commodity trading operations benchmarking studies

Why Only a Metals-First Data Model Can Close the Gap

Each of the four rollover cost components draws from a structurally different data source:

- Prompt-date spread → LME real-time forward curve, tick-level

- Warehouse rent → LME tariff database, location-keyed to warrant record

- Financing charges → SOFR or term SOFR feed, tenor-adjusted, position-level notional

- Cancellation premiums → Physical market pricing service or direct warehouse operator API

Can a Generic CTRM Platform Calculate True Rollover Cost?

A generic CTRM platform can be configured to calculate rollover cost components, but configuration is not the same as native integration. Gartner's market analysis on CTRM software implementations shows custom configuration projects for metals-specific workflows average 14, 22 months and frequently require external data connectors that the platform vendor does not actively maintain through market structure changes such as the LIBOR-to-SOFR transition or LME tariff schedule updates.

The result is a system that approximates rollover cost when all four feeds happen to be current and validated. However, that approximation degrades with every data feed update the vendor's generalist architecture does not automatically propagate. Every LME tariff revision, every SOFR compounding methodology update, and every change in a warehouse operator's cancellation premium quotation cadence creates a manual reconciliation obligation that the platform cannot absorb on its own.

A metals-first data model treats LME warrant data, physical premiums, and post-LIBOR financing benchmarks as native data types, rather than external connectors bolted onto a multi-commodity core. The architecture difference determines whether rollover cost is calculated with precision or estimated with exposure.

LME warrant management system and data architecture

CTRM platform selection criteria for base metals desks

Building a Rollover Cost Framework That Holds Under Scrutiny

The operational standard for aluminum rollover cost calculation is achievable with the right data architecture. The five-step framework below defines what a properly constructed metals position management system should produce on every rollover event. It also defines what a manual or spreadsheet-based process must replicate to reach the same standard.

Step 1: Prompt-Spread Capture

Pull the bid, offer, and mid for the exact outgoing and incoming prompt dates from the LME forward curve at time of transaction. Record all three separately. Use the agreed trade rate, not an end-of-day fix, for settlement purposes.

Step 2: Warehouse Rent Accrual

Identify the warehouse location recorded on each warrant in the position. Apply the published daily tariff rate for that location. Calculate total accrual as: daily rate × calendar days in roll tenor × quantity in metric tonnes. Do not apply a single portfolio-average rate across locations.

Step 3: Financing Charge Calculation

Identify the reference rate in effect on the transaction date; SOFR, term SOFR, or another agreed benchmark as documented in the counterparty agreement. Apply the formula: Notional × Rate × (Days/360). Notional equals the settlement price on the trade date multiplied by the lot quantity in metric tonnes.

Step 4: Cancellation Premium Integration

Source the current cancellation premium from Fastmarkets, S&P Global Commodity Insights, or a direct warehouse operator quotation for the specific location, alloy grade, and shape. Apply as a per-metric-tonne charge to the full quantity subject to warrant cancellation.

Step 5: Total Rollover Cost Assembly and Attribution

Sum all four components. Record each as a separate cost line in the trade settlement memo and in the position management system. Post-settlement variance analysis between estimated and actual rollover cost must be attributable to a named component, rather than absorbed as an undifferentiated P&L adjustment.

ISDA guidance on commodity trade documentation establishes that component-level cost disaggregation is the accepted standard for trade settlement audit trails in physical and financial commodity transactions. A settlement memo that records only total rollover cost fails to meet that standard and cannot support a component-level dispute resolution process.

ISDA commodity trade documentation standards

aluminum rollover cost settlement memo template

Conclusion: Rollover Cost Is a Four-Variable Problem

The prompt-date spread is the most visible component of aluminum rollover cost, though it rarely represents the largest cost factor and never stands alone. Warehouse rent, financing charges, and cancellation premiums each carry material dollar values on any position of size; and together they routinely exceed the spread itself on standard 90-day roll tenors.

Each component requires a discrete data source, a precise calculation method, and a system architecture capable of integrating all four inputs in real time and at the warrant level. A platform that cannot do this delivers only a fraction of the total rollover cost.

Three immediate steps for any desk reviewing its rollover cost methodology:

- Audit the current calculation. Determine whether your system captures all four components or records the prompt spread as a proxy for total cost. Identify which components, if any, are tracked in disconnected spreadsheets or reconciled manually post-settlement.

- Map your data sources. Confirm live access to the LME tariff database keyed to warrant locations, a SOFR-based financing benchmark feed at the applicable compounding convention, and a physical premium service for cancellation premiums by location and grade.

- Establish component-level variance tracking. If your post-settlement reconciliation cannot attribute rollover cost variance to a specific component, your cost model is underspecified. So is your visibility into where roll economics are leaking.

Novaex aluminum position management and rollover cost workflow