Novaex Blog

Analysis, insights, and strategies from the experts at Novaex. Exploring the trends and technologies shaping commodity trading and risk management.

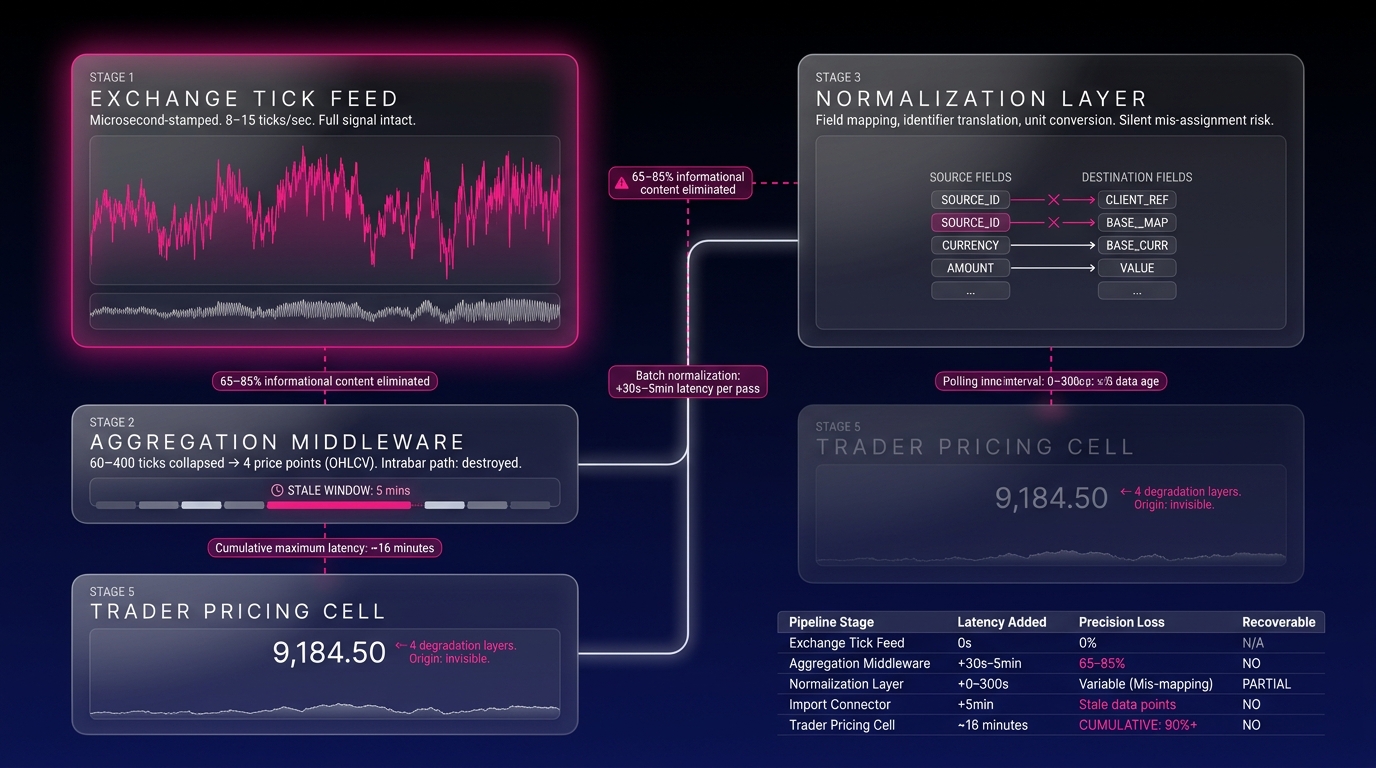

How Exchange Tick Data Degrades in the Metals Pipeline

Physical metals pricing breaks originate at the exchange tick feed, not the trader's spreadsheet. By the time LME or COMEX data reaches a position management system, it has passed through four distinct degradation stages, each discarding a measurable portion of the precision the original signal cont

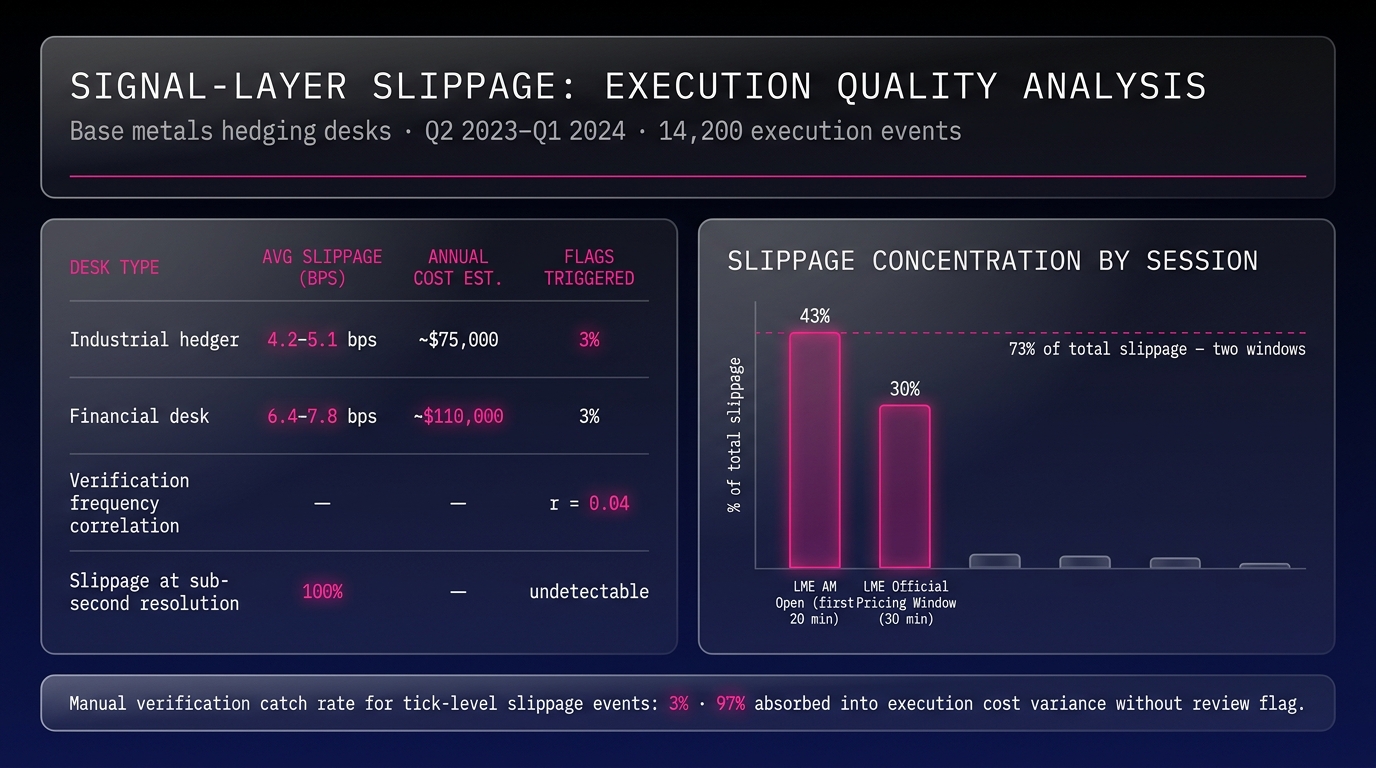

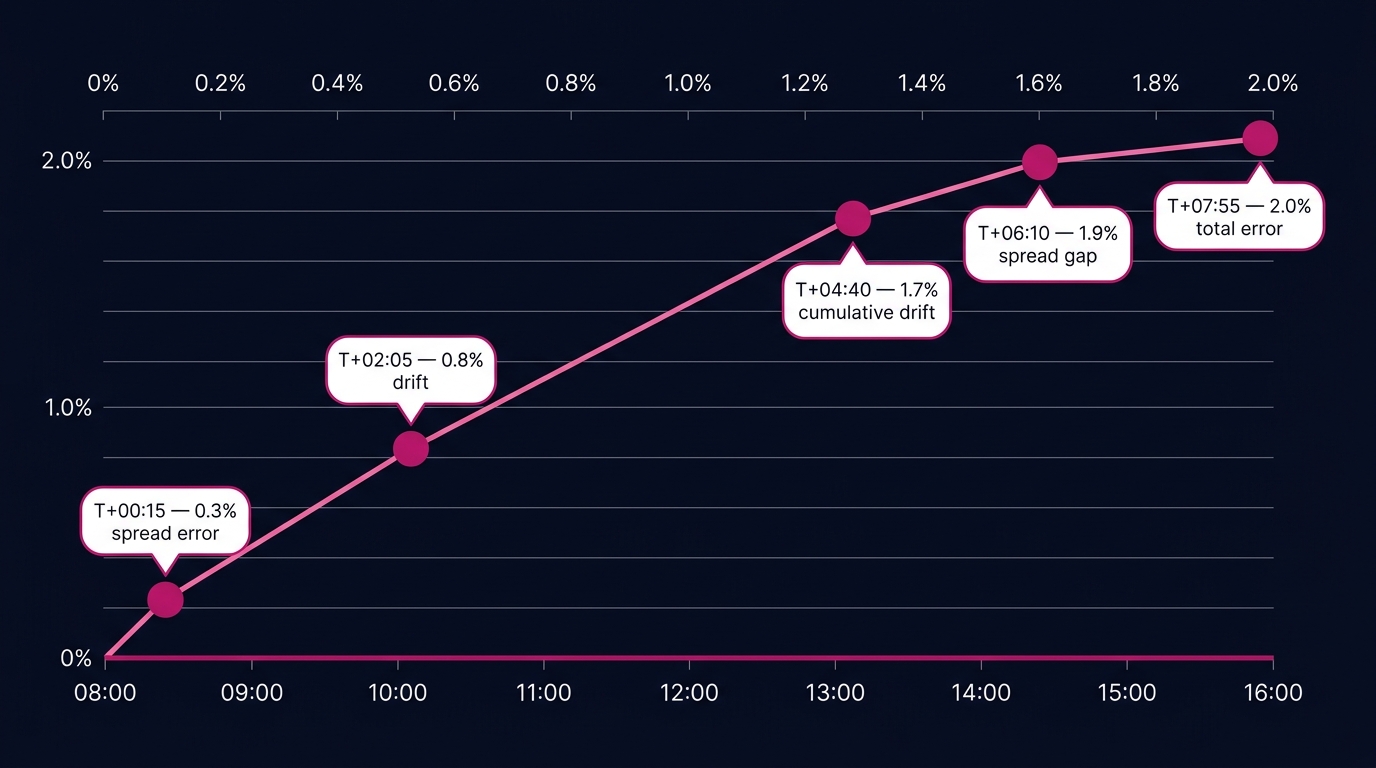

LME Cash/3-Month Spread Pricing Errors: A Session Audit

LME cash/3-month spread miscalculations represent **systematic workflow errors** rather than random data anomalies. A single trading session produces multiple compounding miscalculation events (embedded across hedging, position valuation, and margin estimation) before the Ring even closes. This case

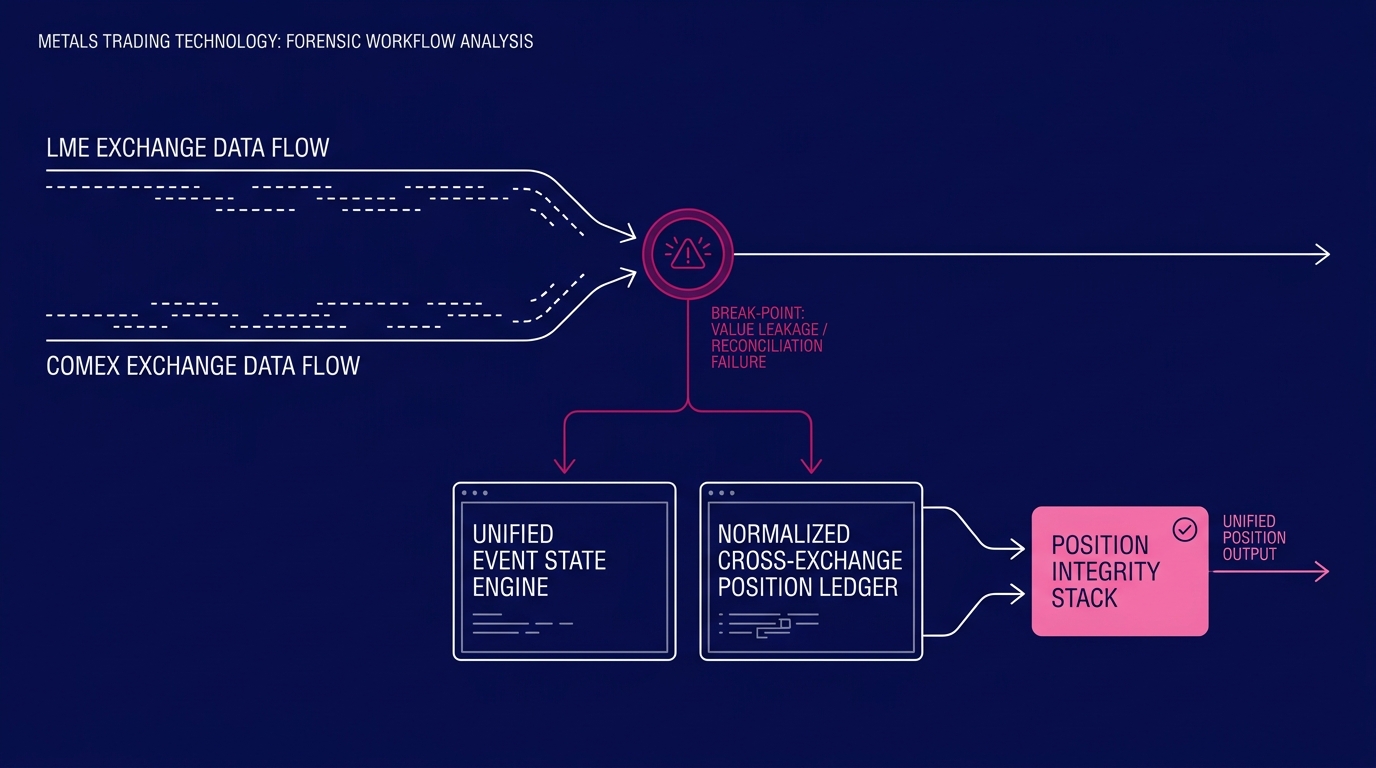

Metals Trading Position Visibility: Mapping Breaks to Architecture

Every metals trading desk operates with breaks. The two categories that generate the most operational and financial exposure are **ledger reconciliation failures** and **cross-exchange position visibility gaps**. These represent structural deficiencies built into how most platforms are designed, rat

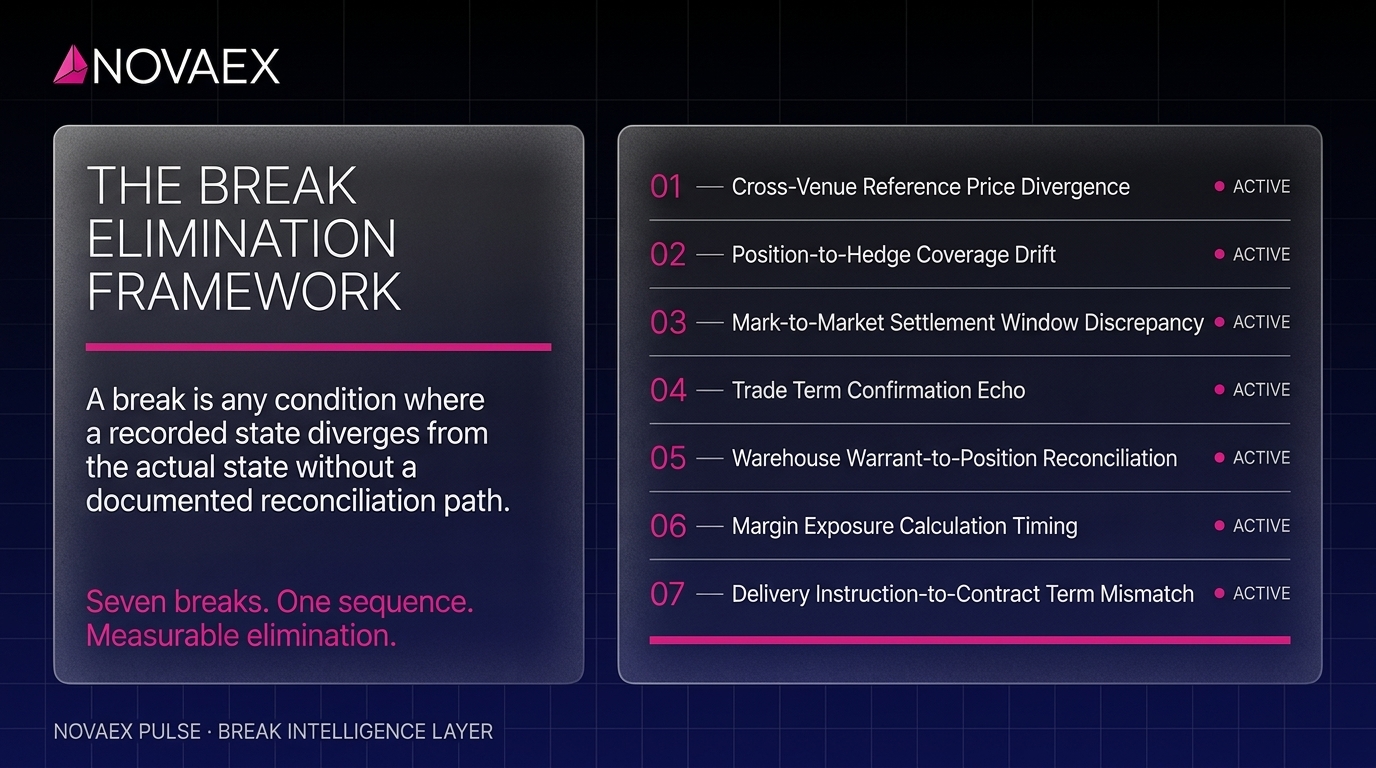

The Break Elimination Framework for Physical Metals Trading

Physical metals trading desks lose measurable margin to seven recurring operational breaks. These are predictable failures with specific mechanisms, documentable costs, and a defined elimination sequence. The **break elimination framework** names, sequences, and measures each break by margin impact,

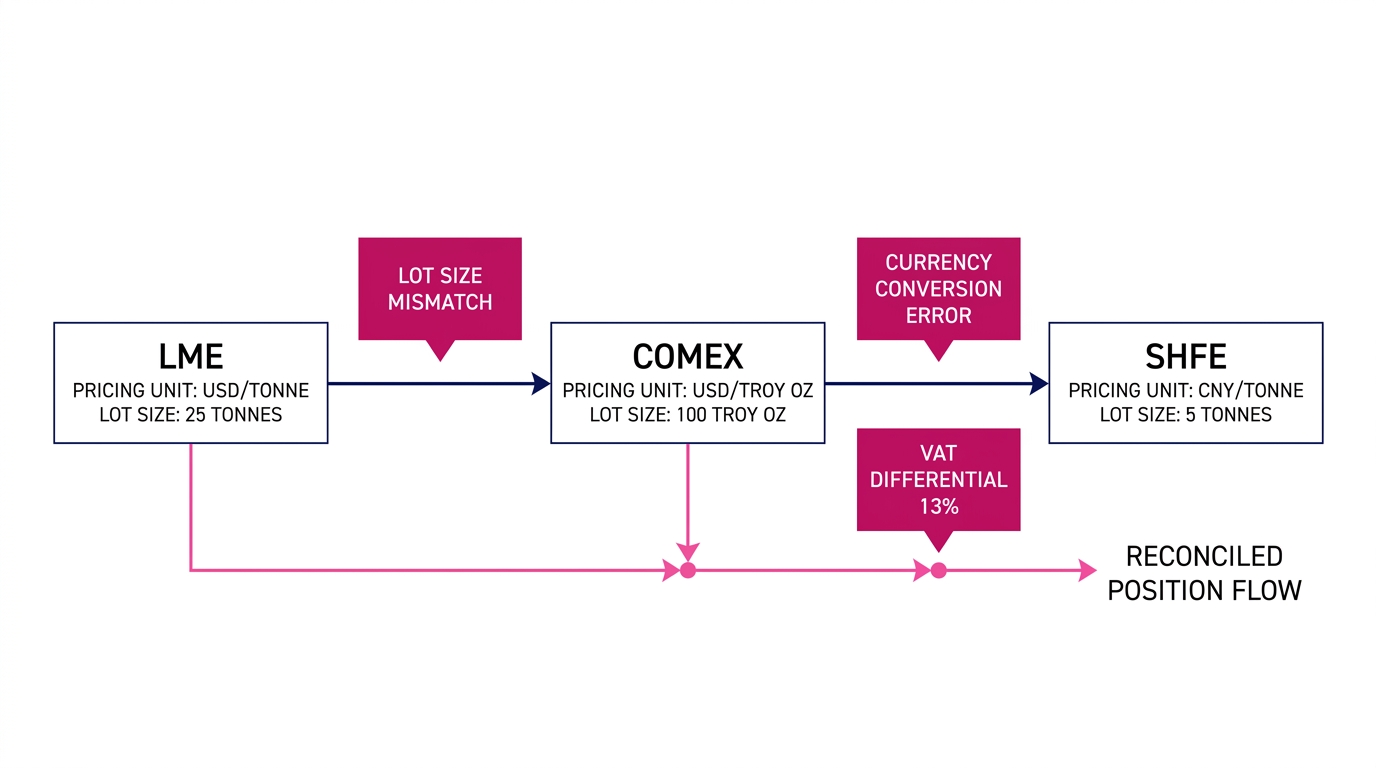

Cross-Exchange Basis Management for Metals Traders

Cross-exchange basis management in physical metals trading means tracking the price differential between correlated contracts on different exchanges (LME, COMEX, SHFE, MCX) while accounting for contract size mismatches, currency exposures, and delivery specification differences simultaneously. Get t

Metals CTRM Implementation Complexity Is a Vendor Choice

Front-office metals traders have absorbed this complexity as an accepted cost of doing business. The evidence examined here demonstrates that assumption is not technically justified.

Metals Trading Breaks: The Margin Loss You're Not Tracking

In physical metals trading, every P&L conversation starts with price. Discussions focus on whether copper closed above the hedge level or if aluminum rallied before the LME fix. Price exposure is visible, auditable, and discussed in every morning brief.

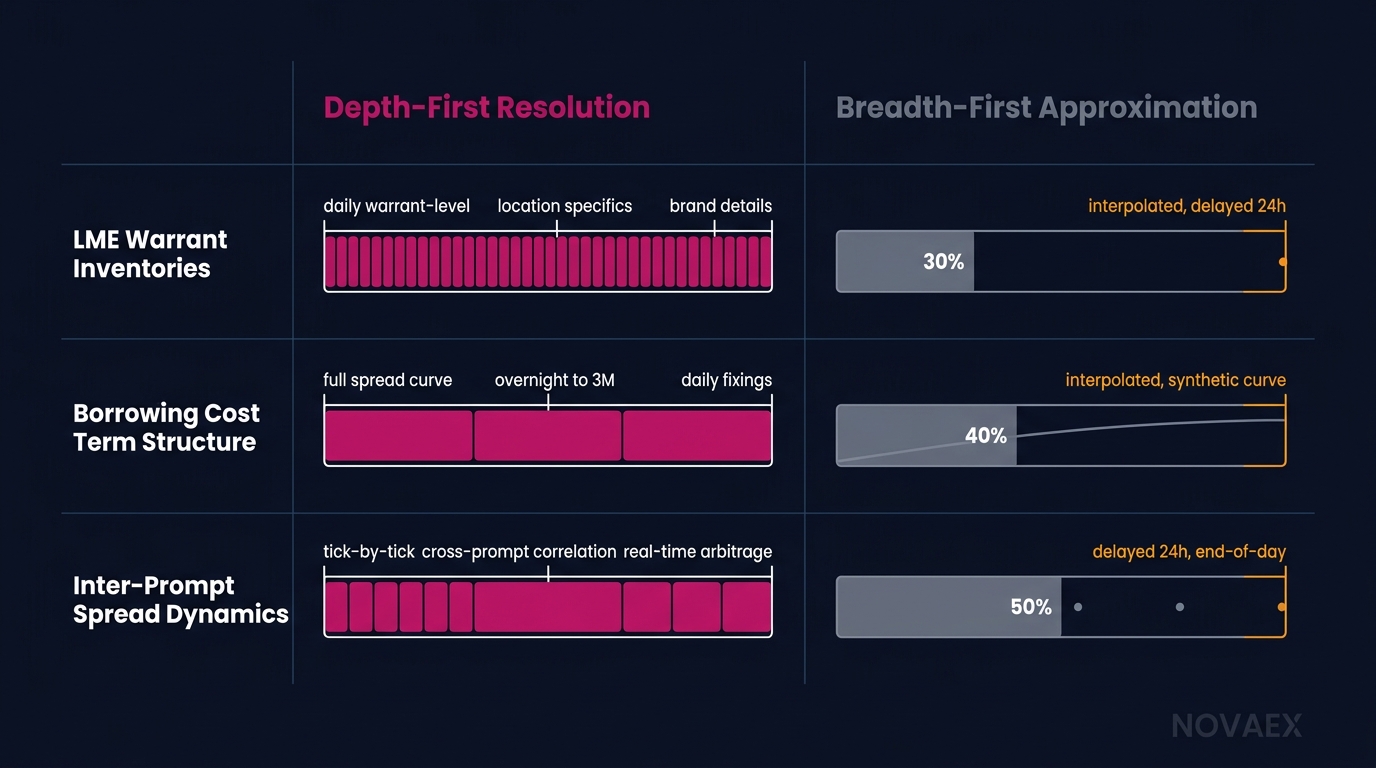

Depth-First Intelligence: LME Data Breadth Platforms Miss

Depth-first commodity intelligence means owning every layer of exchange-native data for a specific market before claiming competency in it. For base metals, that begins with three non-negotiable constructs: LME warrant inventories, borrowing cost term structures, and inter-prompt spread pricing. Bre

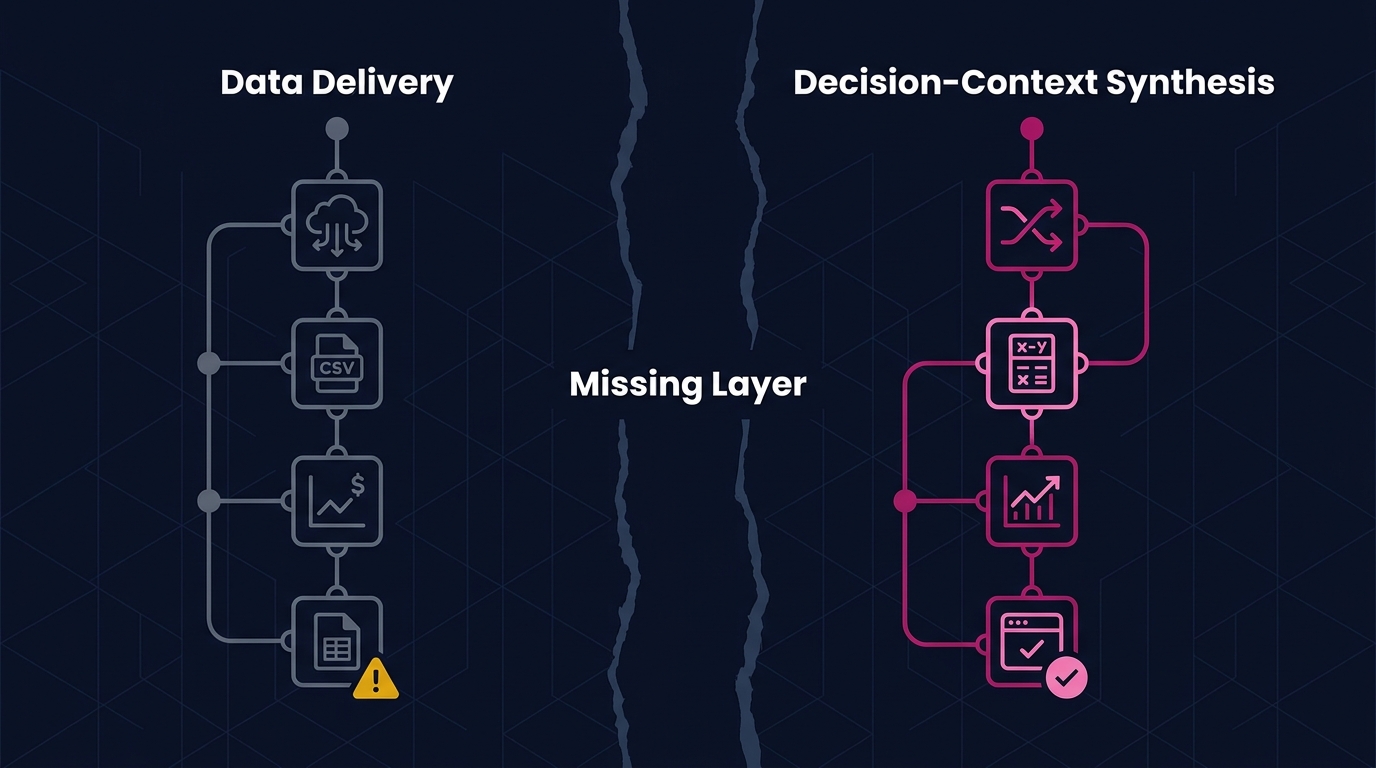

Commodity Data vs. Trading Intelligence: The Gap

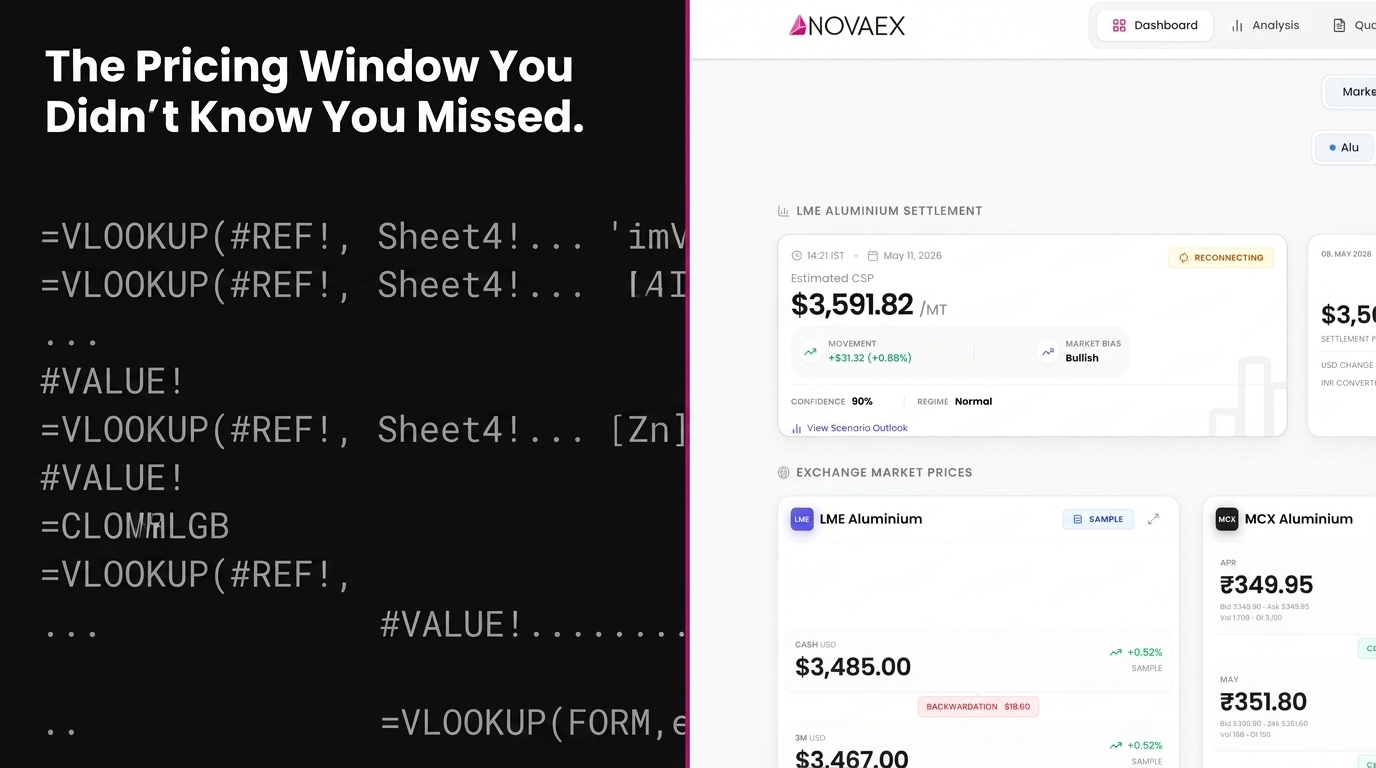

Your data vendor and your trading intelligence platform are not the same system. This is true even when trading infrastructure treats them as equivalent. A data vendor delivers prices, settlement values, and exchange feeds. A trading intelligence platform synthesizes that data into **decision-contex

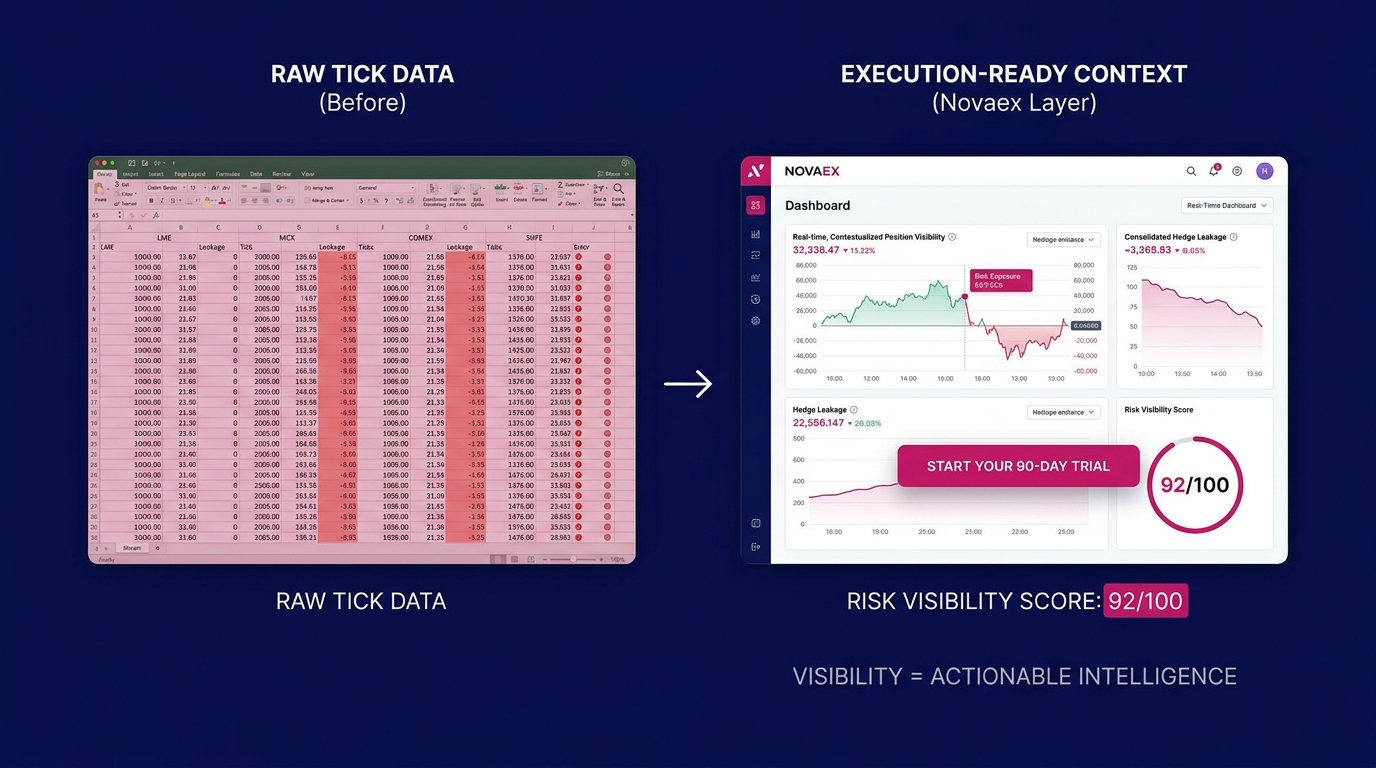

Metals Trading Position Visibility: Raw Tick to Ready Signal

Most platforms terminate the process at stage one, delivering data but failing to provide decision context.

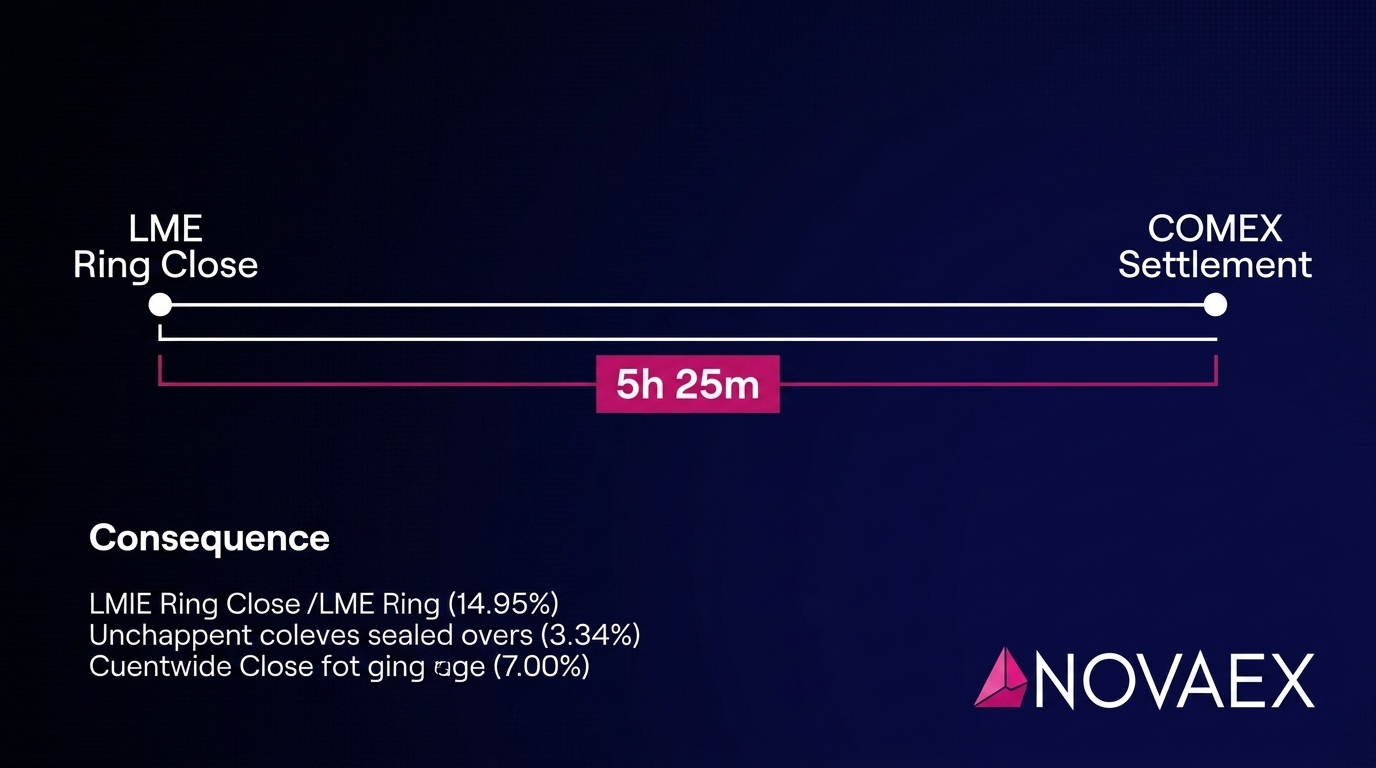

Your Hedge Ratio Calculation Has a Timestamp Problem

A hedge ratio built on LME and COMEX prices captured at different times is not a complete hedge ratio. It is an approximation with an embedded timing error. This error is one that is fully calculable from the session structure of both exchanges.

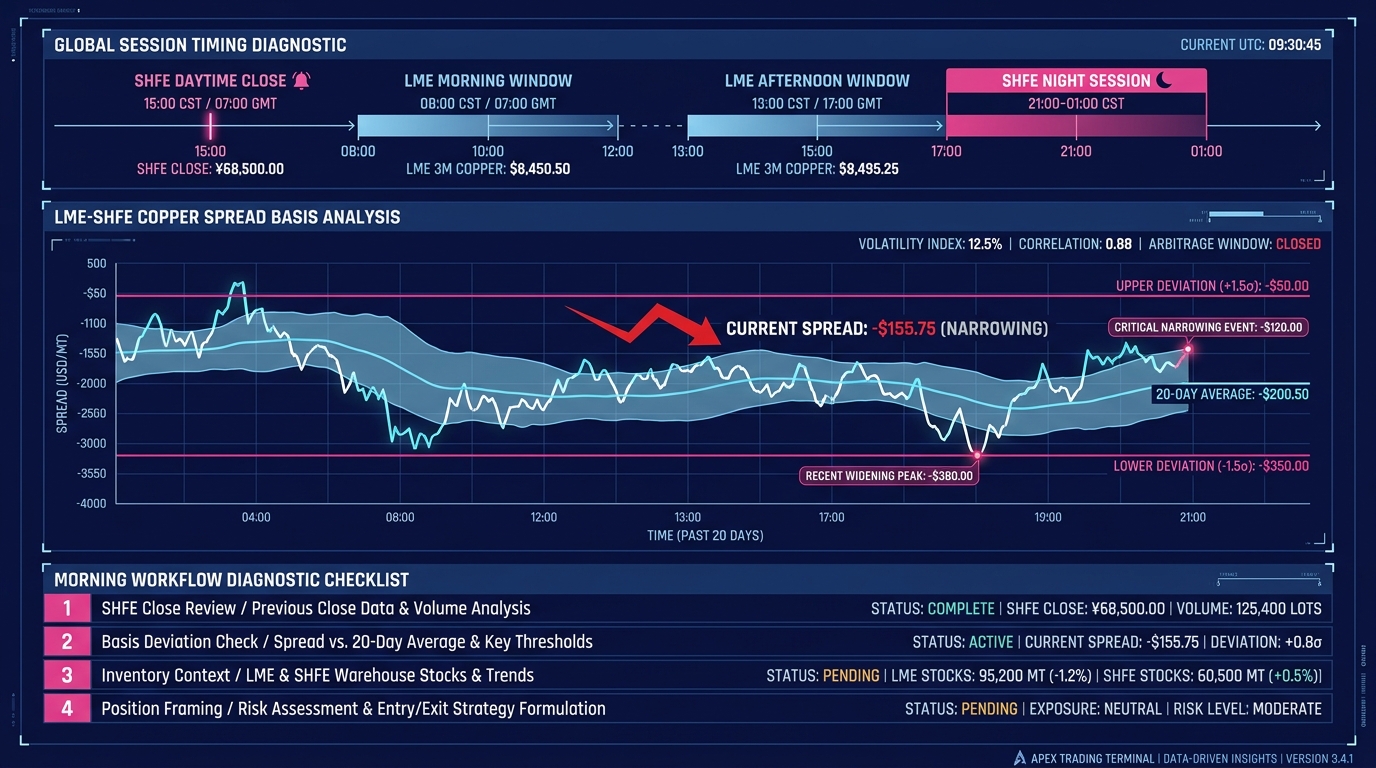

SHFE Pricing in Your Intraday Workflow: No Analyst Needed

SHFE pricing context belongs in every base metals trader's intraday decision cycle. The mechanism is direct: SHFE's daytime session closes at 15:00 Beijing time, 07:00 GMT in winter, before LME electronic trading reaches peak liquidity. That close delivers a confirmed Chinese price signal, a calcula

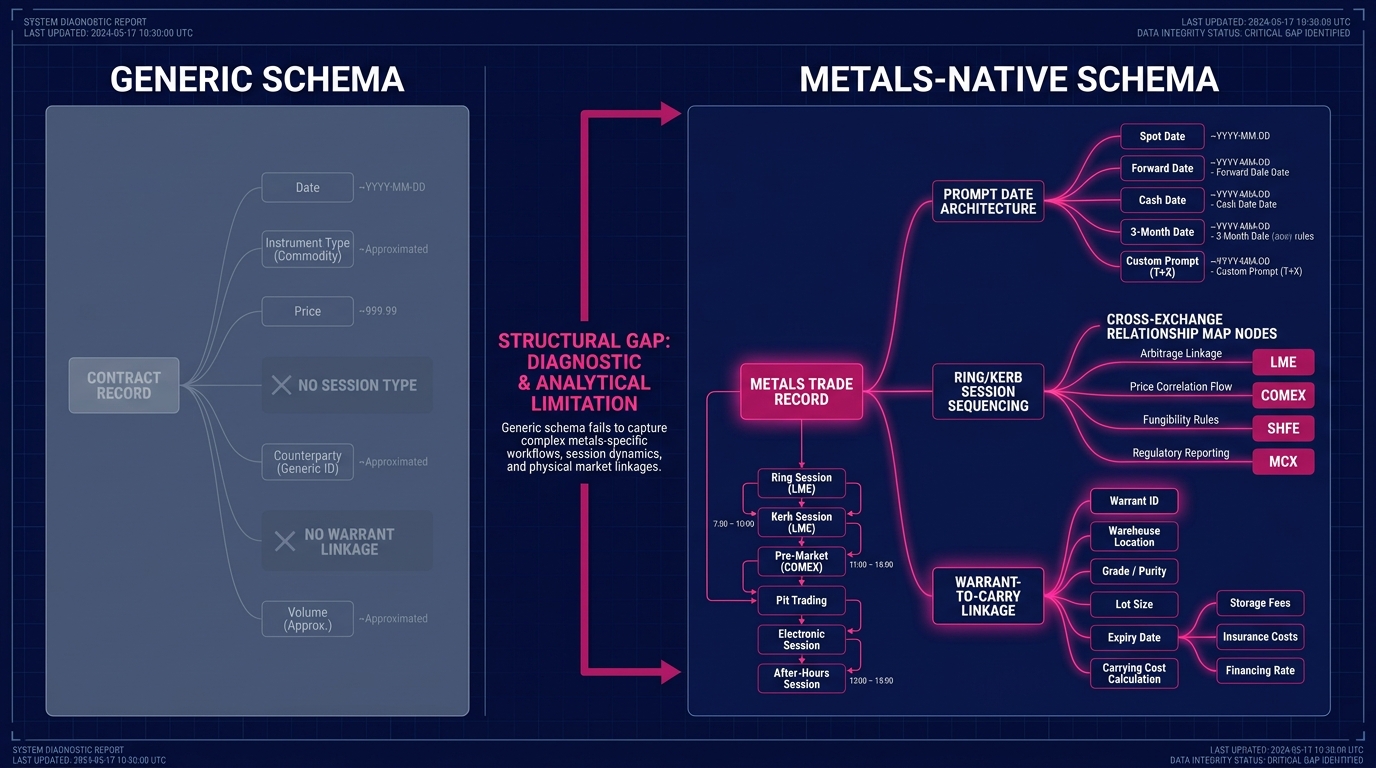

Why Base Metals Data Quality Starts at Architecture

The front-office trader running LME copper positions against COMEX exposure has a specific problem: data arriving in their platform may be technically present and yet structurally inadequate. Prices exist, timestamps are populated, volumes are accurate, yet still the spread relationship misfires or

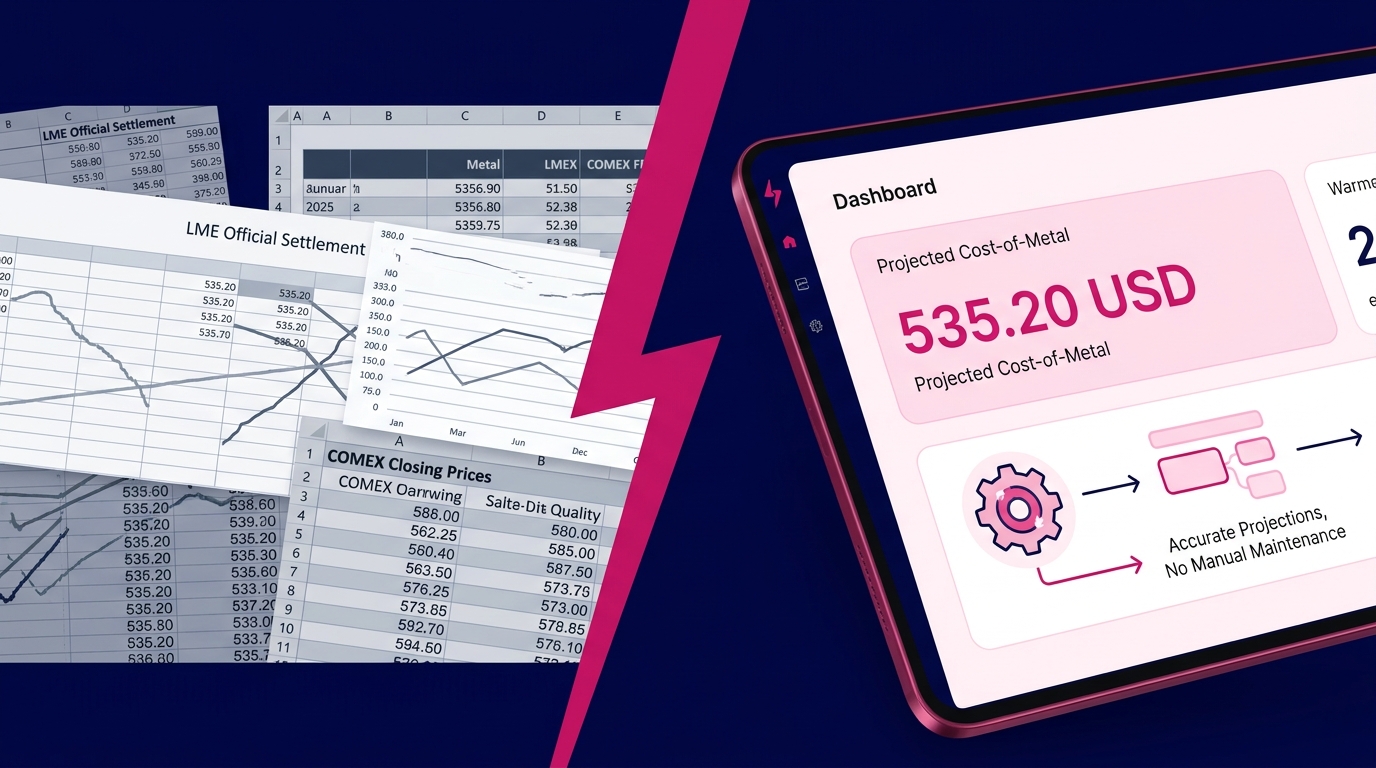

Daily Price Sheet: 9 Metals Trading Workflows Replaced

A metals trading **daily price sheet workflow** consists of nine discrete manual tasks, from exchange settlement price collection to team distribution, each with a defined input, trigger, and output. This document maps each task to its exact platform replacement function. Each replacement maps to a

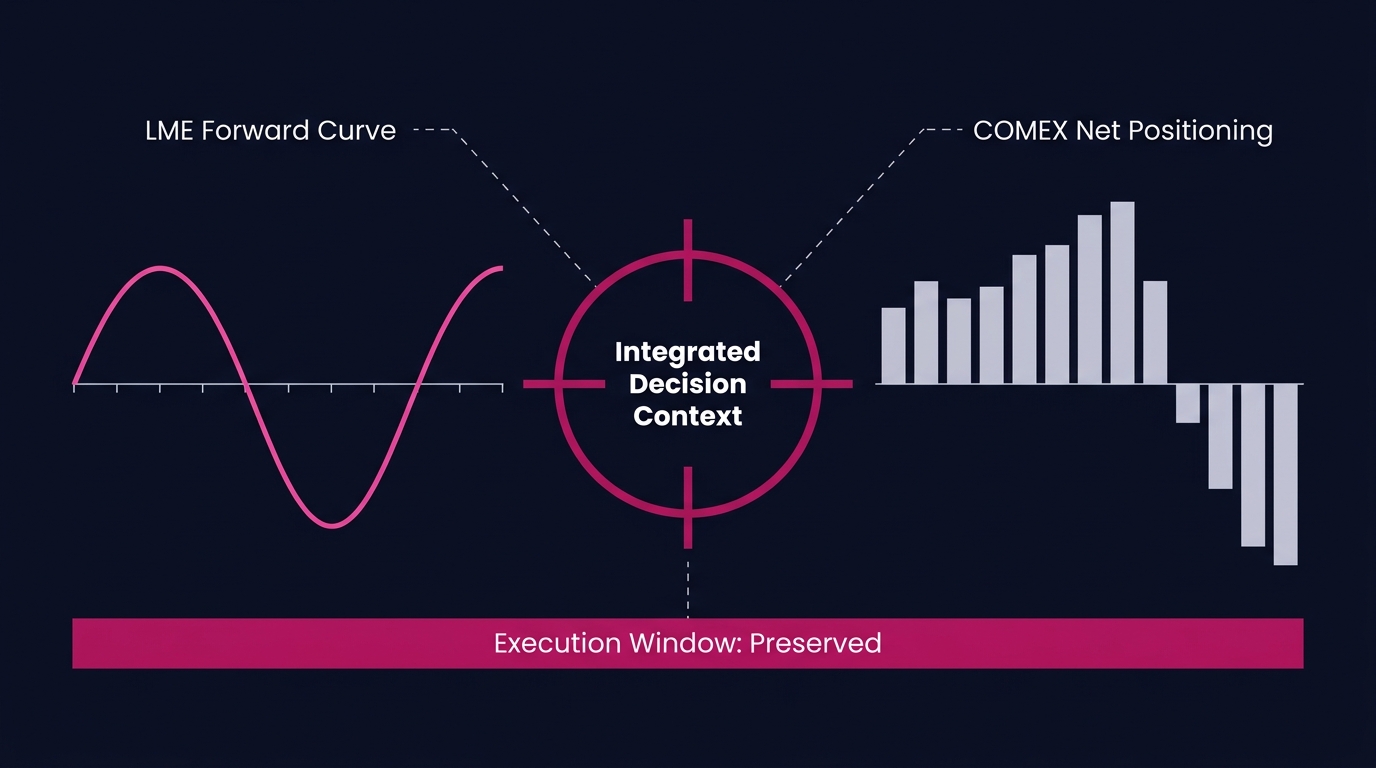

COMEX-LME Integration for Copper Hedging Decisions

Every copper hedging decision is a timing problem nested inside a confidence problem. Traders must determine exactly how precisely a signal can be verified before committing to a hedge at a specific prompt date.

Defensible Execution Documentation Starts at Trade Time

Post-hoc reconstruction of trade rationale is the single most common reason execution documentation fails under scrutiny. **Defensible execution documentation** is achieved by capturing decision rationale, market context, and authorization logic at the exact moment of trade. When real-time capture i

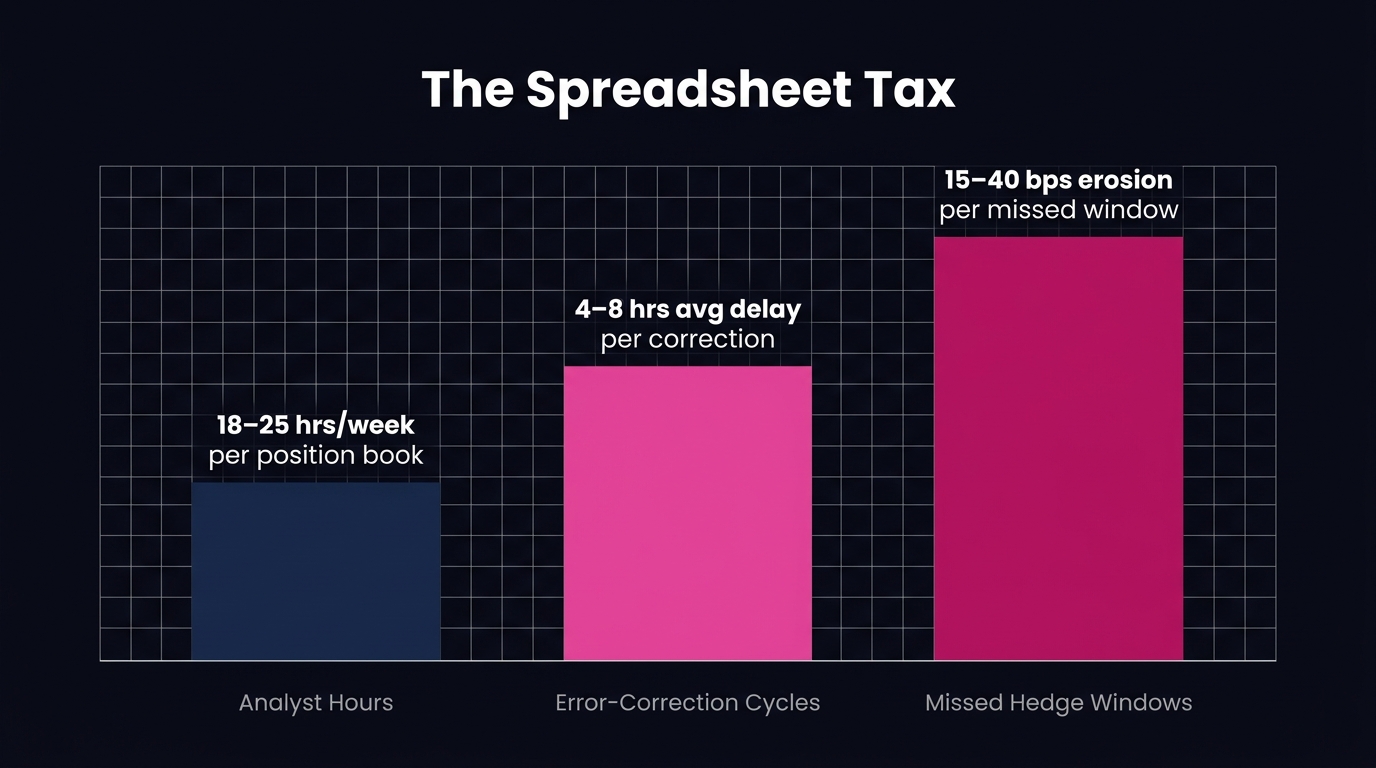

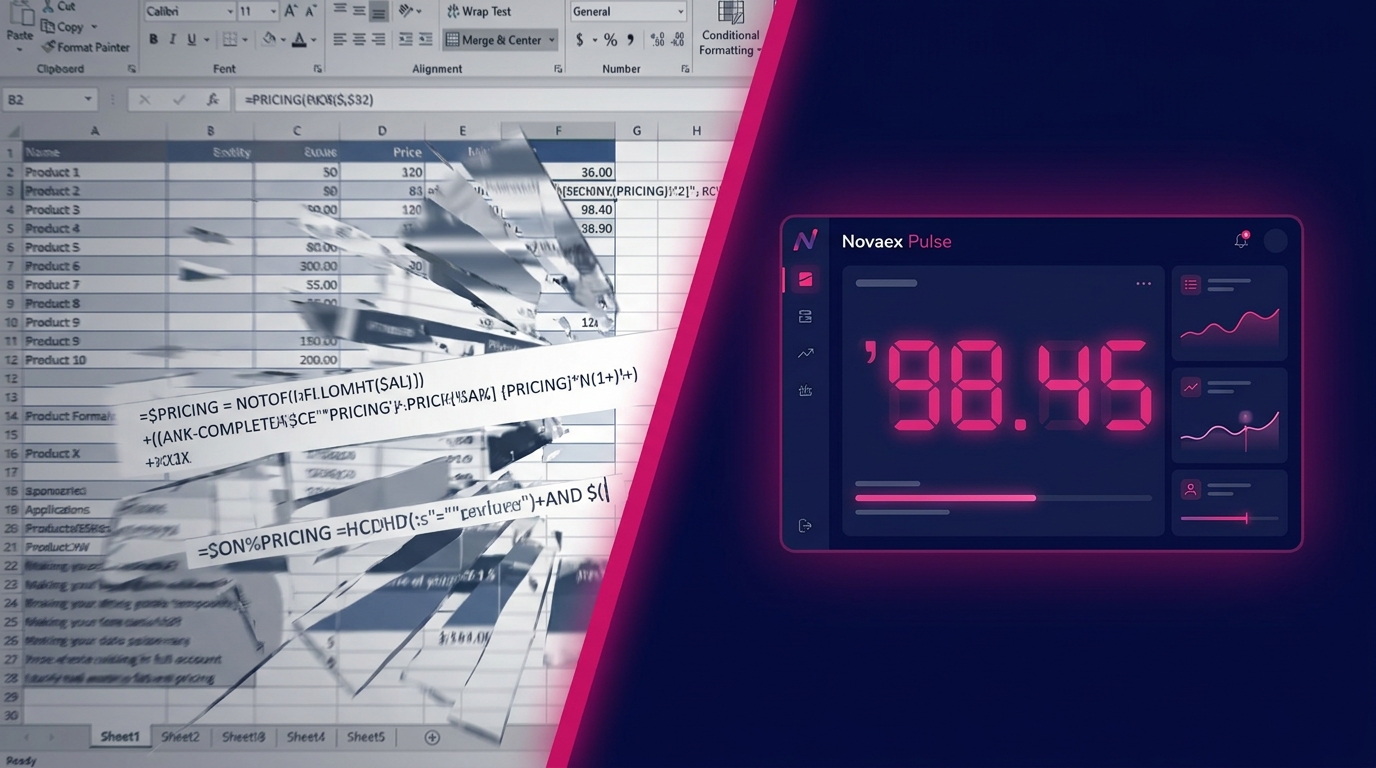

The Total Cost of Spreadsheet Hedging Workflows

Spreadsheet-based hedging workflows carry three distinct cost layers, not one. The full total cost of ownership includes analyst labor hours consumed by manual data management, rework cycles generated by formula errors and version conflicts, and quantifiable opportunity cost from missed hedge window

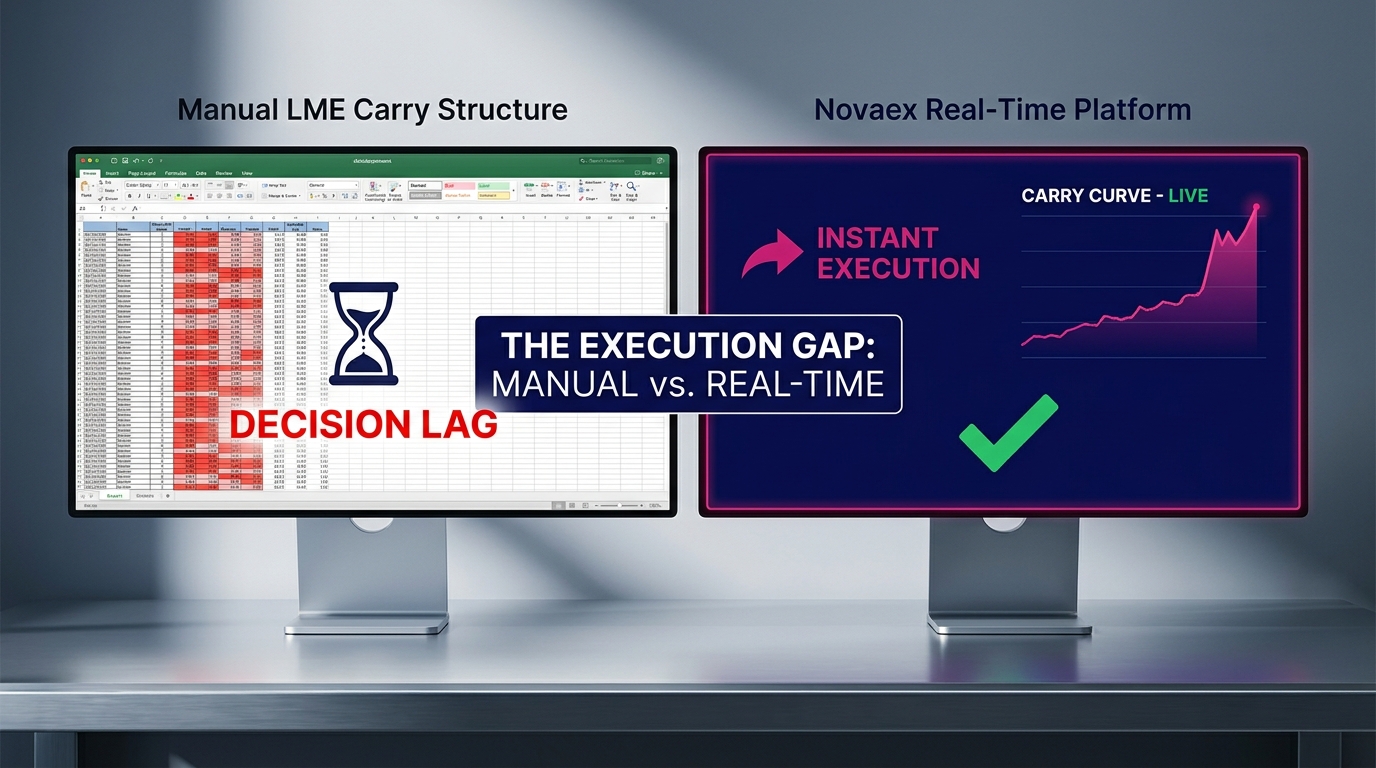

Why Manual LME Carry Recalculation Costs Execution

The LME ring session closes on schedule. The carry structure intelligence it produces does not arrive at the same moment, at least not inside a manual recalculation workflow.

Why LME Position Tracking Breaks in Spreadsheets

Metals hedgers using spreadsheets to track LME positions operate with a structural gap between the tool and the instrument. The gap is not immediately visible in normal markets. It appears at the worst possible time: when prices move fast and hedges need to perform.

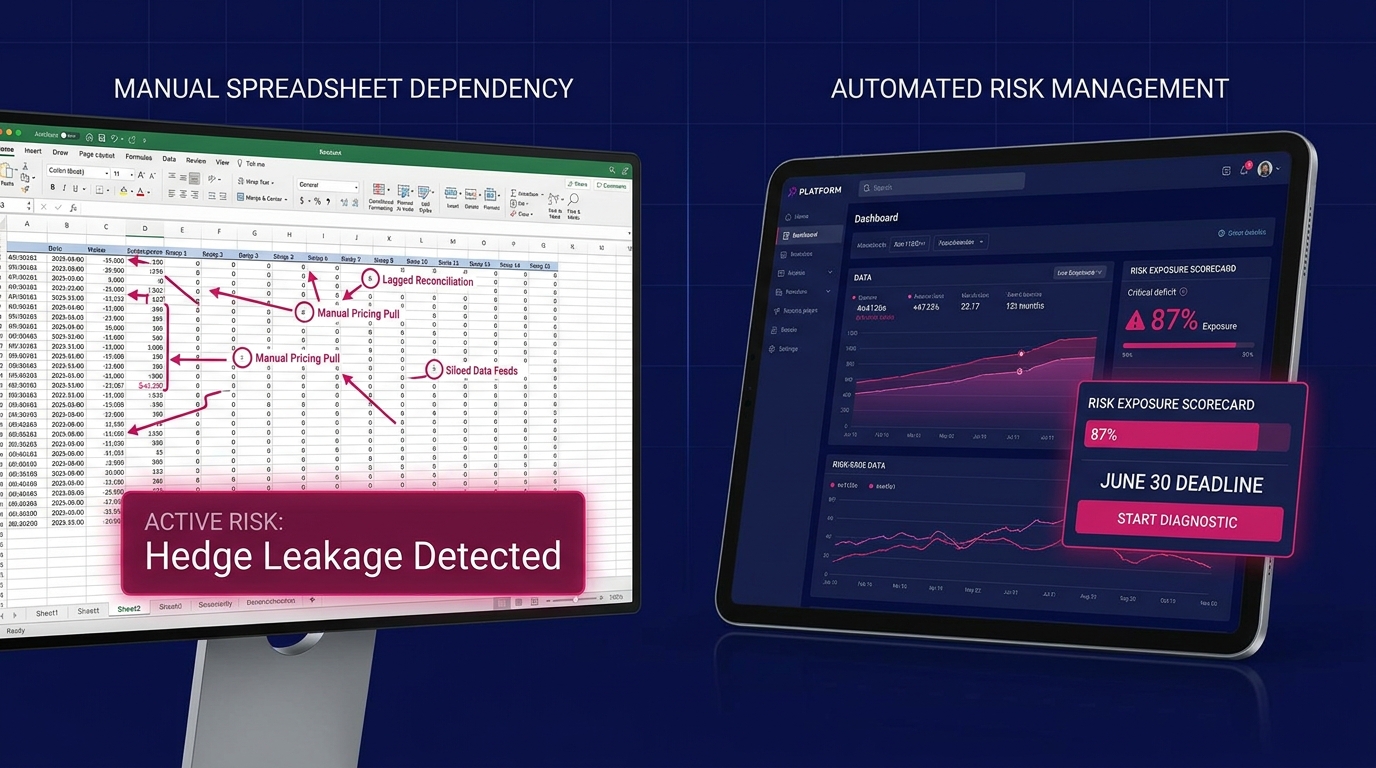

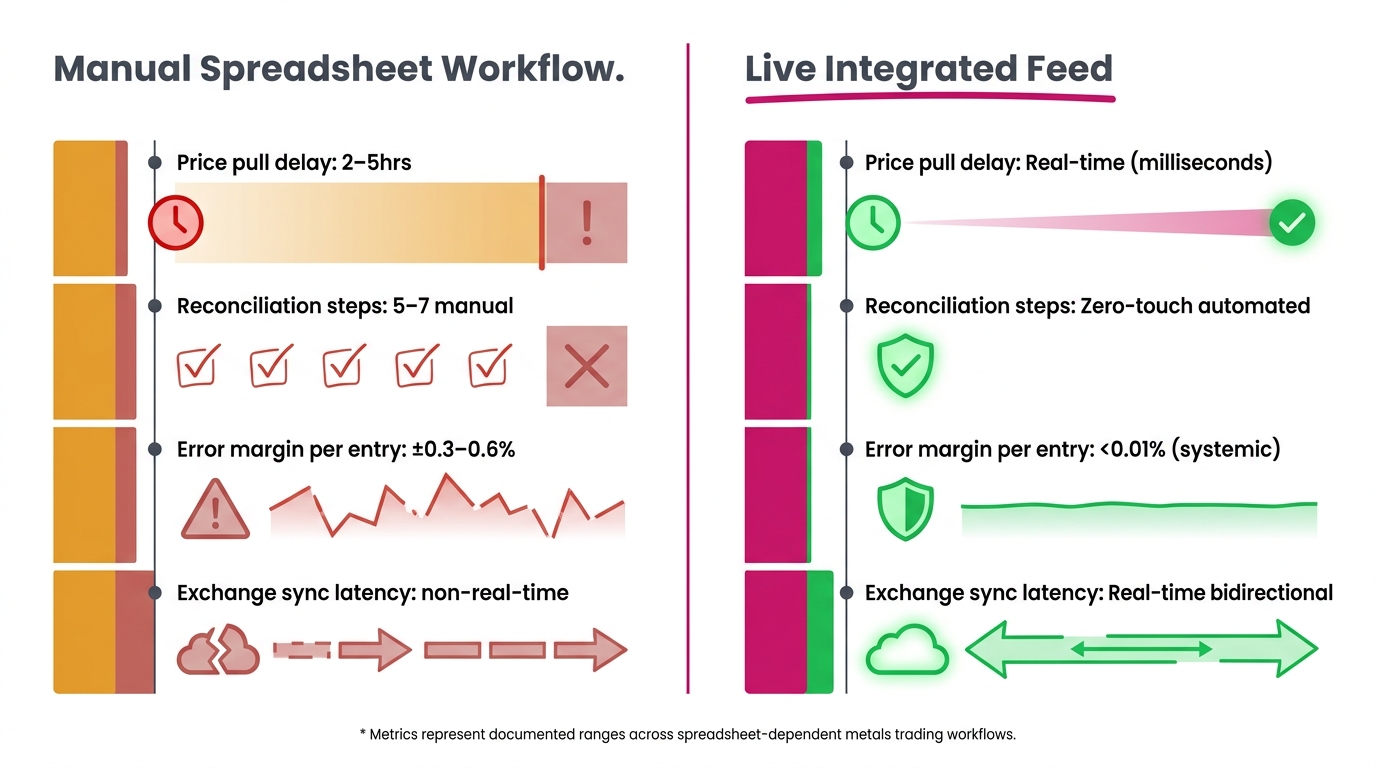

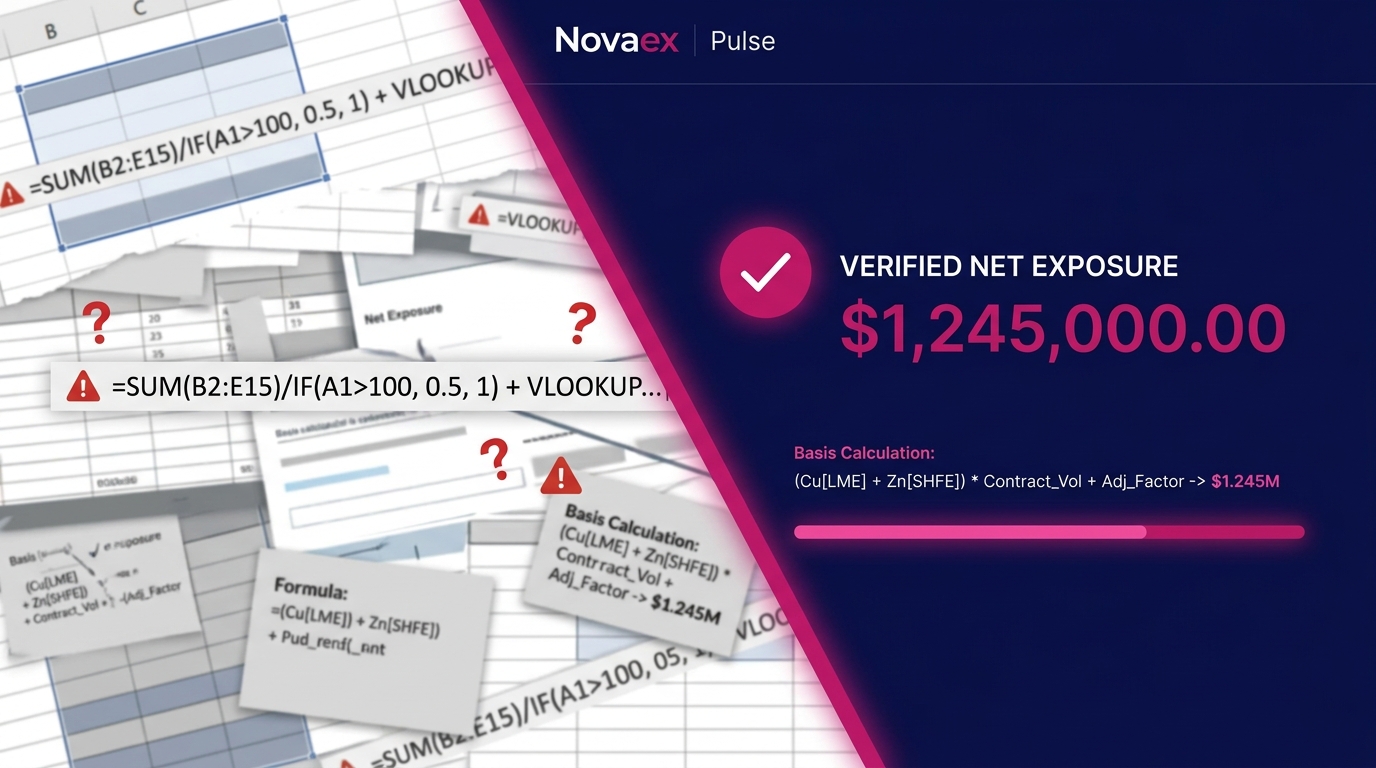

Spreadsheet Risk in Commodity Trading: A Risk Vocabulary

If a position workbook returns an incorrect delta during a volatile LME session, or if forty minutes are lost reconciling two versions of a hedge sheet before a risk call, that is spreadsheet-dependent process risk (SDPR). Most trading desks lack the structured language to classify, report, or preve

Spreadsheet Risk in Metals Trading: A Workflow Audit

Work through each indicator below. Note where your operation sits.

Metals Intelligence Platform Credibility: One True Signal

When a front-office trading operation signs a multi-year enterprise agreement with an unproven vendor, standard procurement risk management has been deliberately overridden. The condition that produces that behavior is a buyer who has concluded, through direct assessment, that the status quo carries

Why CTRM Software Fails Physical Metals Traders

Physical metals traders have been failed by enterprise CTRM for one documented reason: these platforms were designed for organizations with IT departments, six-figure implementation budgets, and multi-month rollout capacity. Mid-market metals desks do not have those resources. That structural mismat

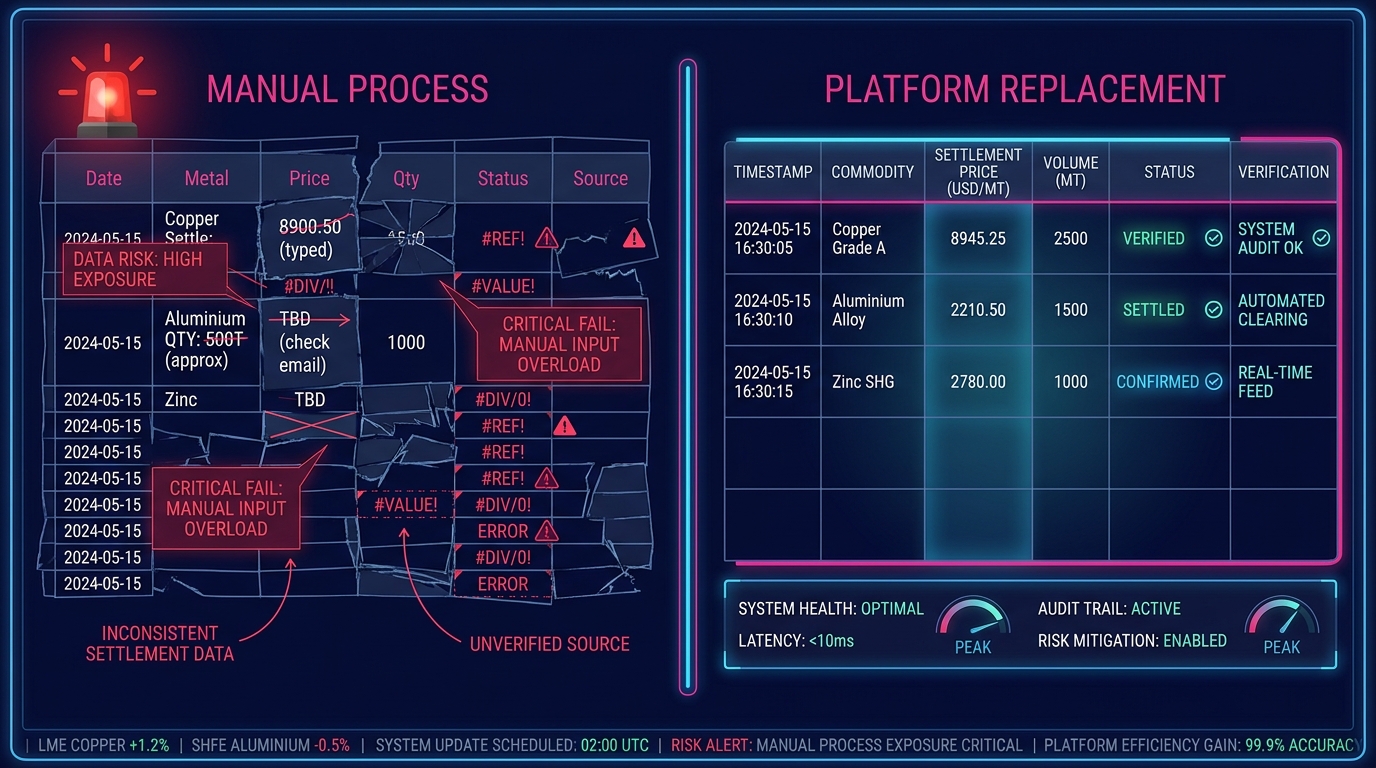

Base Metals Spreadsheet Reconciliation: The Accuracy Gap

Most trading desks have never formally measured the error rate embedded in their spreadsheet reconciliation workflows. According to research compiled by EuSpRIG (European Spreadsheet Risks Interest Group), **88% of spreadsheets in active use contain at least one material error**. In base metals trad

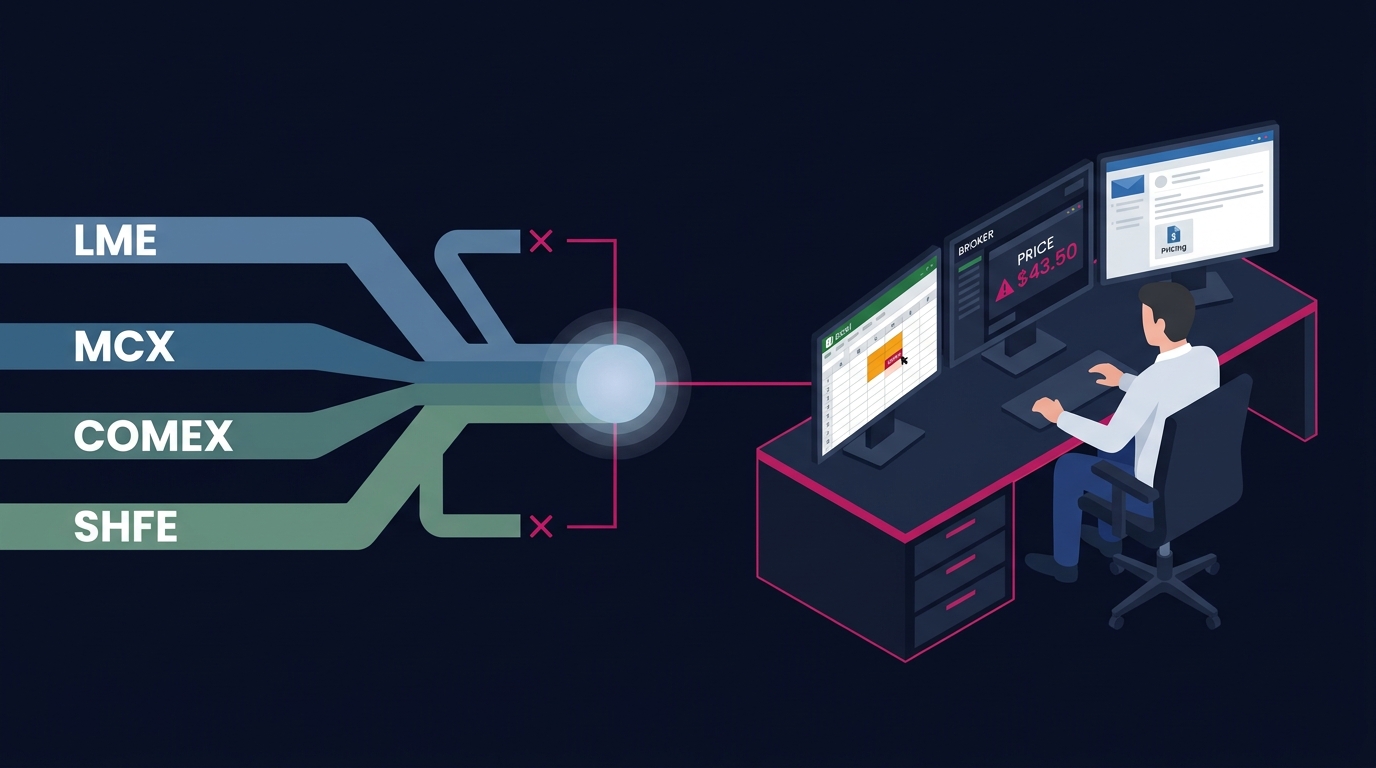

Metals Trading Data Fragmentation Is a Structural Gap

Front-office metals traders have been solving the same problem for decades: prices live in one place, positions live in another. The moment markets move, the gap between them becomes the most consequential exposure point in any active book.

Spreadsheet Risk in Metals Trading Is Not Background Noise

According to the European Spreadsheet Risks Interest Group (EuSpRIG), 88% of spreadsheets contain at least one material error. For most metals trading operations, that statistic is routinely absorbed into operational routine rather than treated as a documented risk condition requiring a structured r

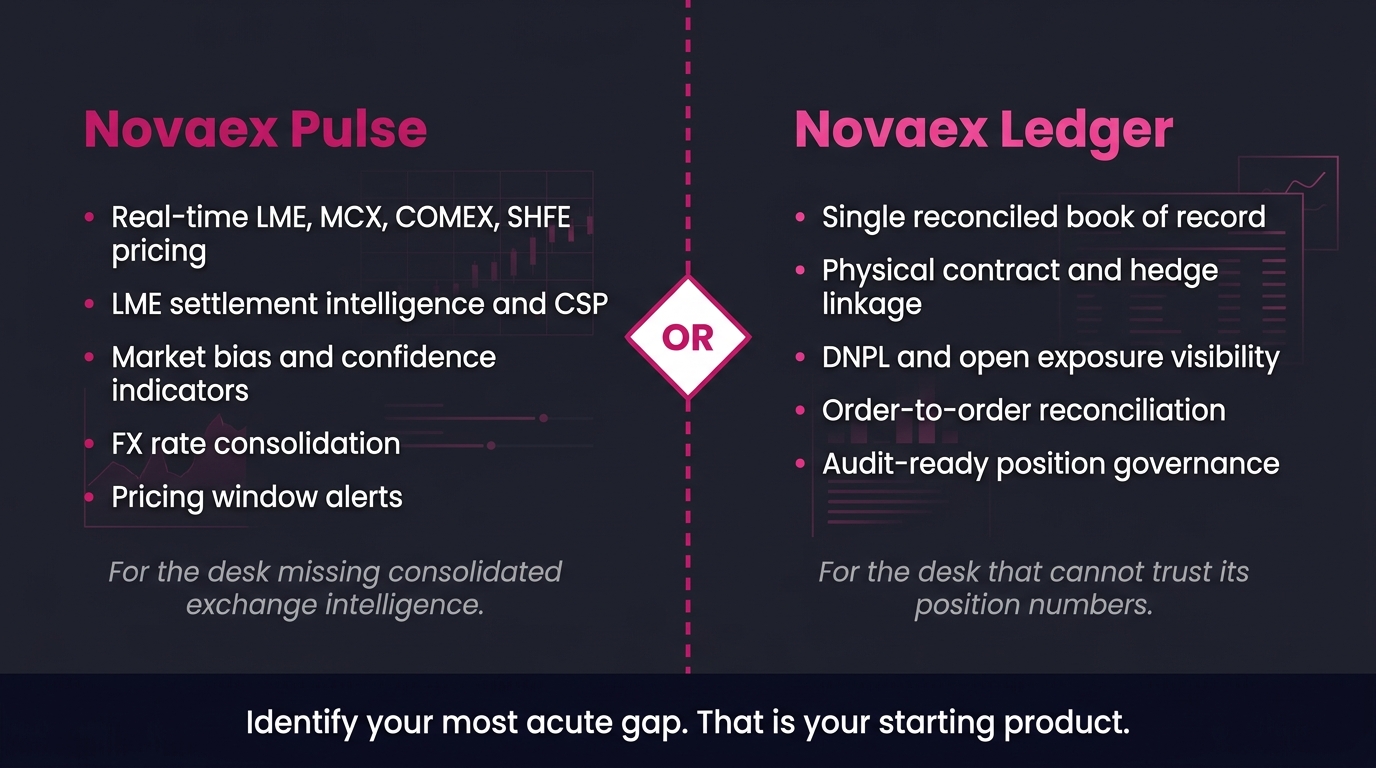

Pulse vs. Ledger: Diagnosing and Resolving Your Metals Trading Workflow Failure

If your firm has a metals trading workflow problem, it belongs to one of two documented categories: degraded market intelligence or unreconciled positions. **Novaex Pulse** is built to resolve the first. **Novaex Ledger** is built to resolve the second. Determining which failure is generating the mo

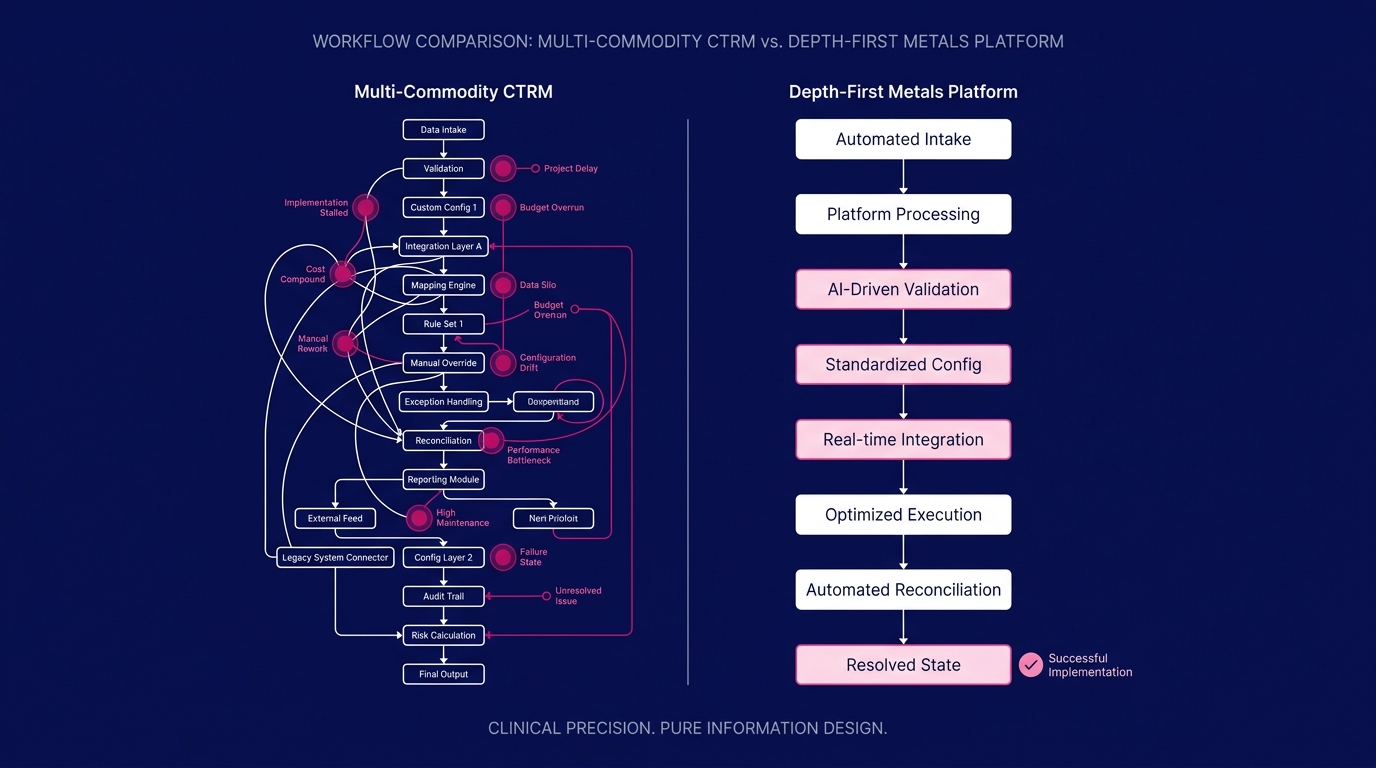

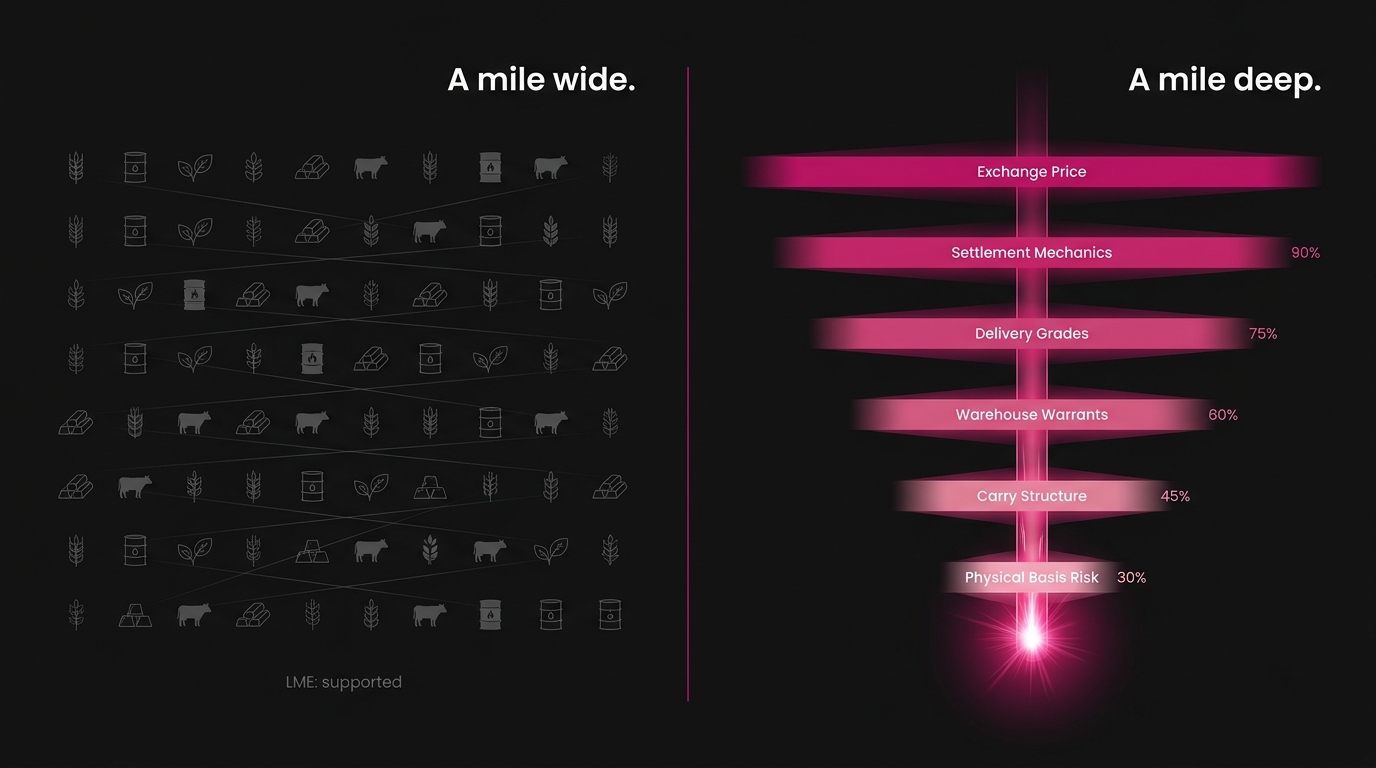

Depth-First Intelligence: The New Metals Trading Standard

Depth-first intelligence (the disciplined mastery of each base metal before expanding to the next) is becoming the structural standard for metals trading platforms. Traders operating on this standard gain compounding advantages in position visibility, risk analytics, and execution support that bread

The Daily Cost of Metals Market Intelligence Gaps

Every metals desk operating four separate data feeds carries a cost that does not appear on any invoice. **The daily cost of operating without consolidated metals market intelligence** (LME, MCX, COMEX, and SHFE synthesized in a single real-time view) consistently runs to multiples of any platform s

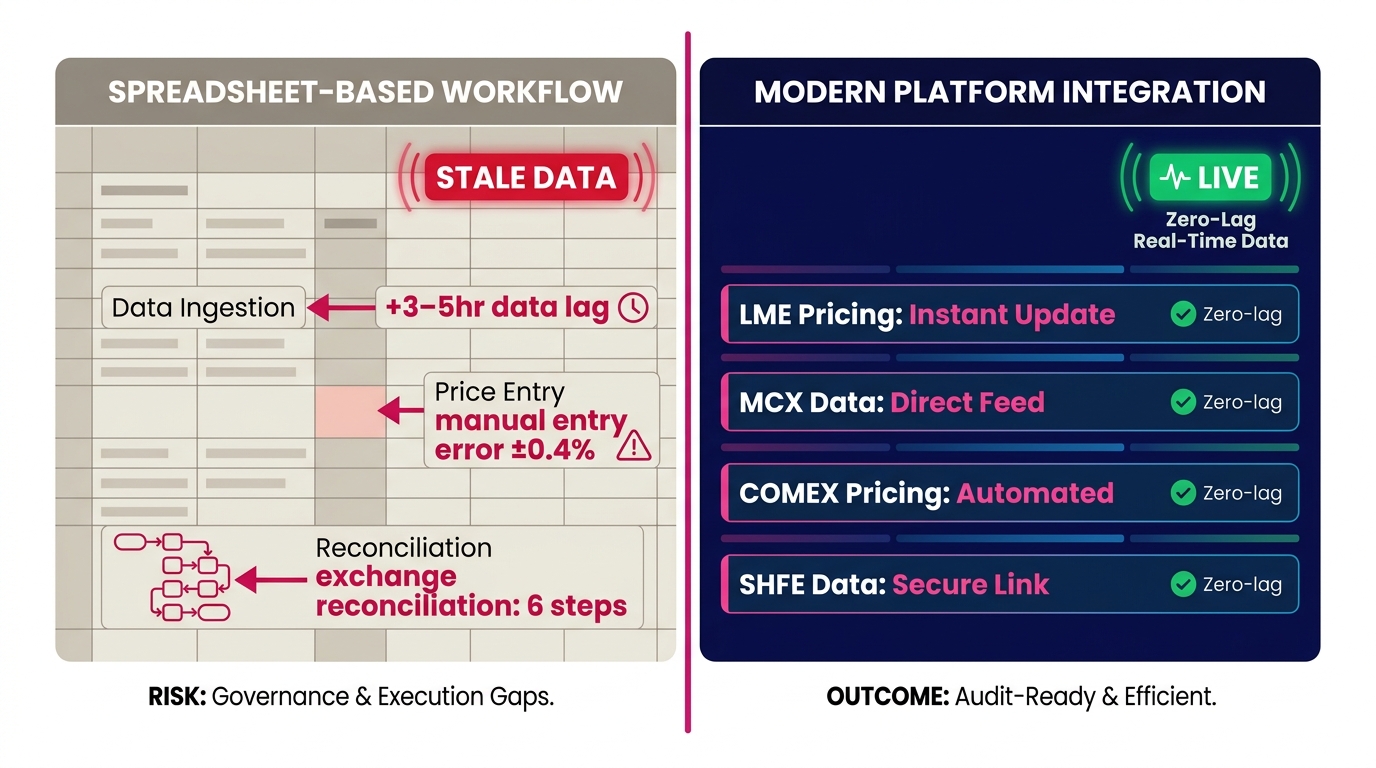

Metals Trading Governance: Three Structural Failures and Their Measurable Costs

Multi-system metals workflows produce three identifiable **metals trading governance failures**: unreconciled positions, delayed SHFE and MCX pricing, and fragmented exposure across books. Each failure is measurable, structurally present in most legacy-platform environments, and traceable to specifi

Manual Reconciliation Hours: Calculate Your Trading Cost

Manual reconciliation hours on a commodity trading desk are a calculable weekly liability rather than an unquantified operational overhead. Most metals desks have never formally measured them. This post provides a structured four-step framework to produce an exact hour and dollar figure for your tea

CFO Audit Controls for Commodity Trading Positions

A CFO certifying financial statements that include commodity trading exposure does not sign off on a general sense of confidence. **The three controls that matter are reconciliation integrity, timestamp immutability, and tamper-evidence**, and every CTRM platform's governance structure must satisfy

The Analyst Hours Lost to Manual Price Table Maintenance

Manual price-table maintenance in metals trading consumes an estimated 6, 12 analyst hours per week per position, hours spent pulling LME settlements, constructing pricing-period averages, and reconciling counterparty invoices. A formula engine configured to specific contract terms eliminates this m

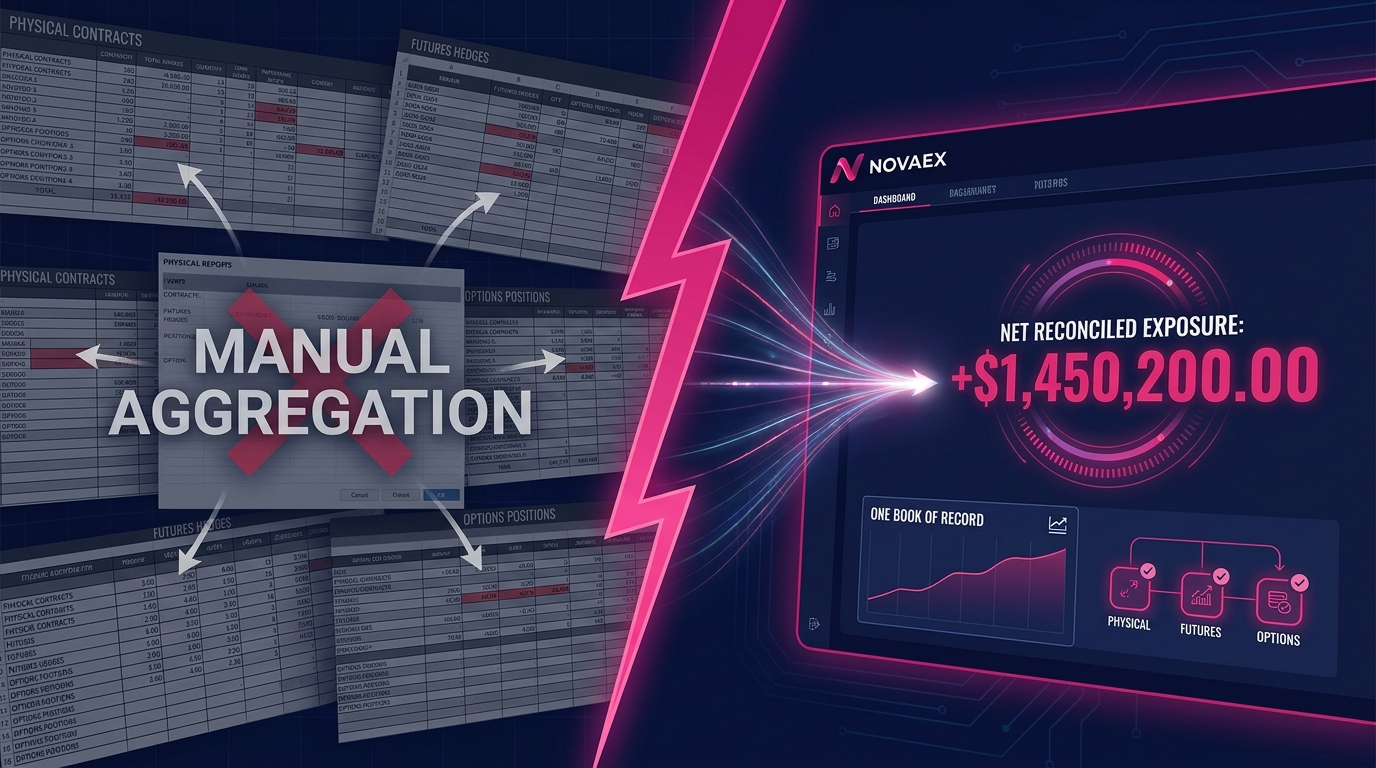

Metals Position Reconciliation: Inside the Single Book

The most direct drain on metals trading desk efficiency is the period before risk reporting when position data from disconnected systems produces contradictory net exposure figures. This recurring discrepancy demands manual resolution precisely when market conditions require trader attention elsewhe

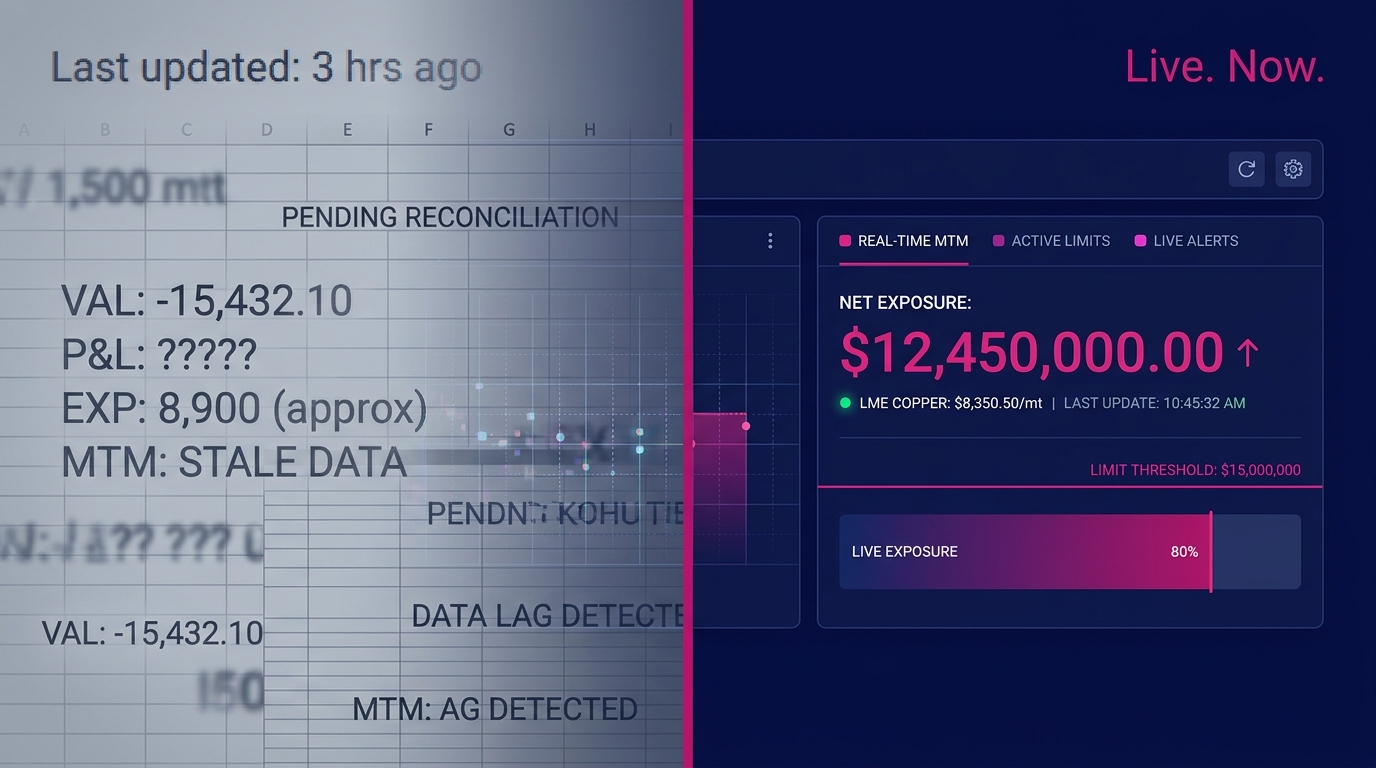

Intraday Position Limits Only Work With Real-Time MTM

TL;DR: Limits enforced against stale mark-to-market data function as historical records of risk already taken rather than live controls. Real-time MTM serves as the operational precondition turning a position limit from a lagging indicator into a live control mechanism.

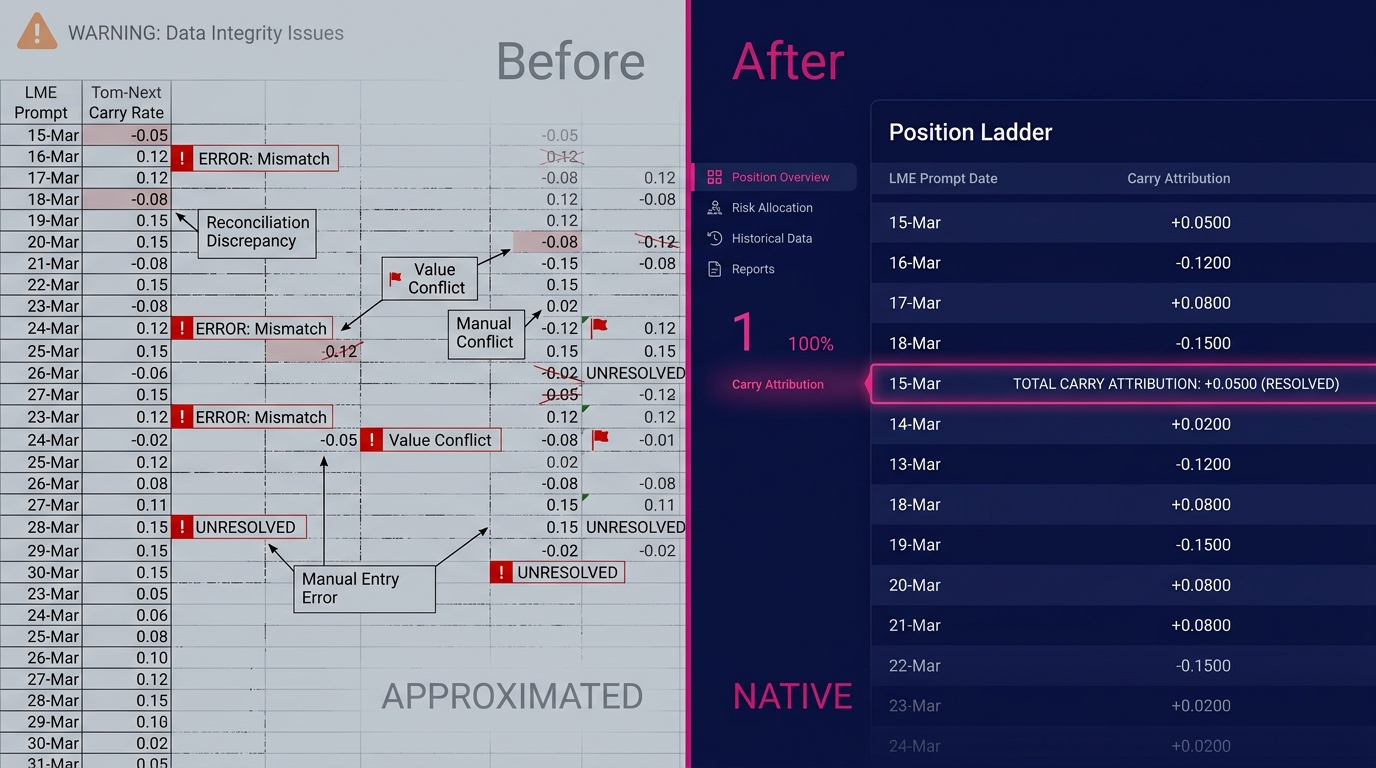

LME Tom-Next Carry Modeling: No Manual Adjustment Required

LME Tom-Next carry is the daily cost of rolling an LME forward position one prompt date forward. Most CTRM platforms approximate it. Novaex models it natively, pulling actual LME forward curve spreads across each daily prompt date and embedding the result directly in your position view and P&L attri

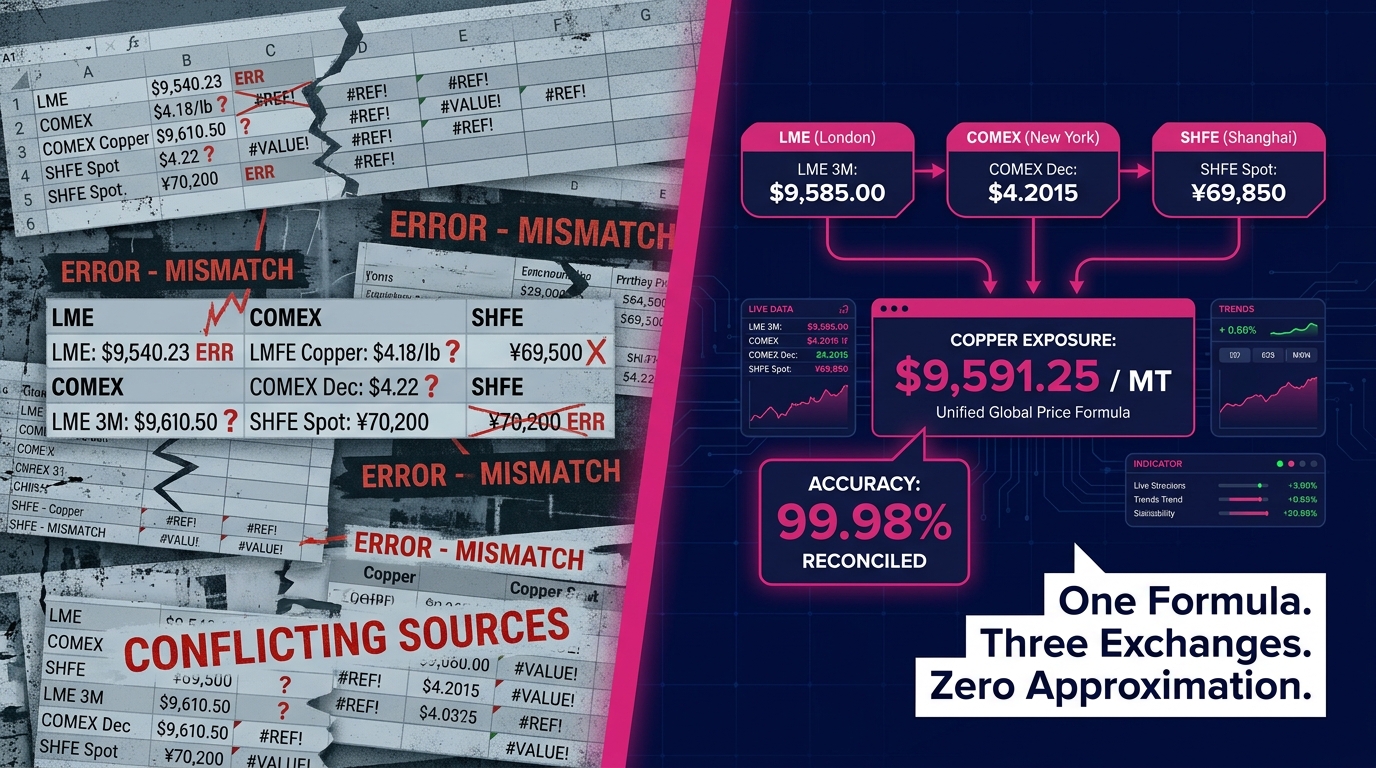

Multi-Exchange Basis Calculation: One Formula, Two Exchanges

When a procurement contract references both LME official settlement and COMEX closing prices, the formula is a precision instrument. **Multi-exchange basis calculation** requires treating each exchange price as a structurally distinct variable. Pulse's formula engine resolves both within a single co

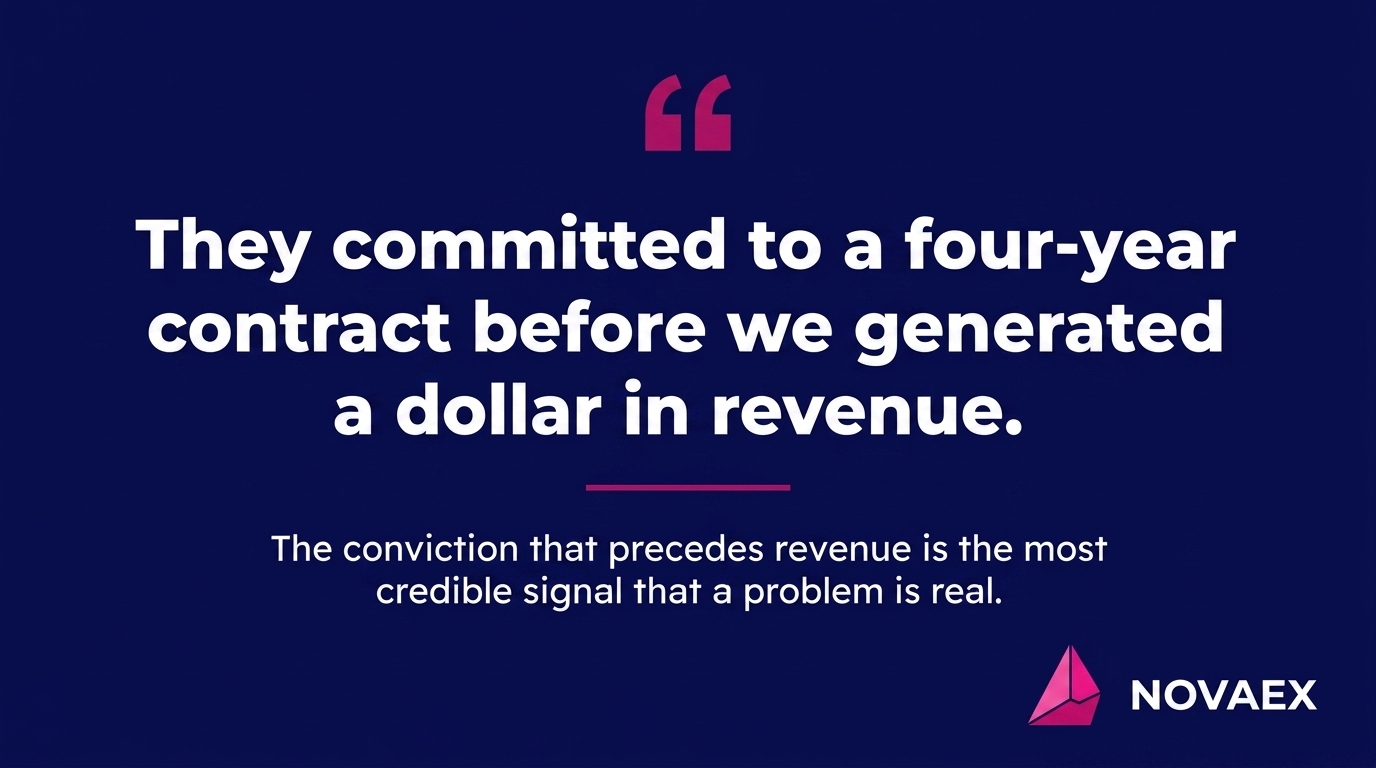

A 4-Year Contract Before Revenue: Enterprise CTRM Proof

Before Novaex generated its first dollar of revenue, an enterprise metals trading firm signed a four-year contract designating Ledger as their primary book of record. That decision bypassed product roadmaps and vendor presentations in favor of operational evidence: specific, auditable, and reproduci

Metals Trading Position Divergence Is a Governance Failure

When front office, back office, and risk management each report a different position from the same portfolio, this represents a fundamental governance failure. **Metals trading position divergence** occurs when three departments process the same trade data through three separate systems, each applyi

LME, COMEX, SHFE: Why Breadth-First Pricing Engines Fail

A metals trader running simultaneous positions across LME, COMEX, and SHFE cannot rely on a breadth-first platform's multi-exchange metals pricing engine. The architecture embeds a deliberate trade-off: exchange-specific formula precision is sacrificed for cross-commodity coverage. That trade-off is

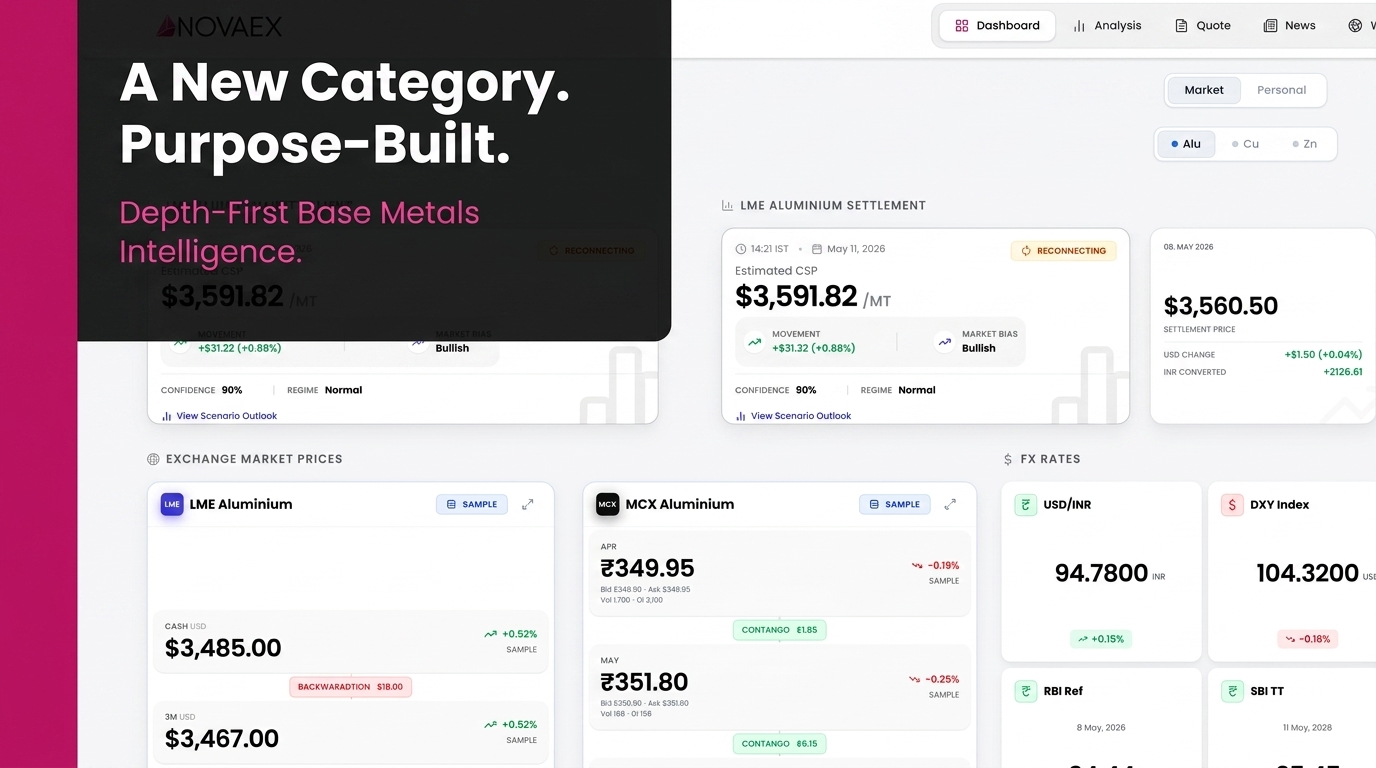

Depth-First Base Metals Intelligence: A New Standard

The daily reality most base metals traders manage is familiar: a front-office copper trader at a mid-market firm runs position visibility in one system, pulls LME settlement prices from a second feed, reconciles SHFE exposure in a spreadsheet, and discovers at the end of the day that none of these s

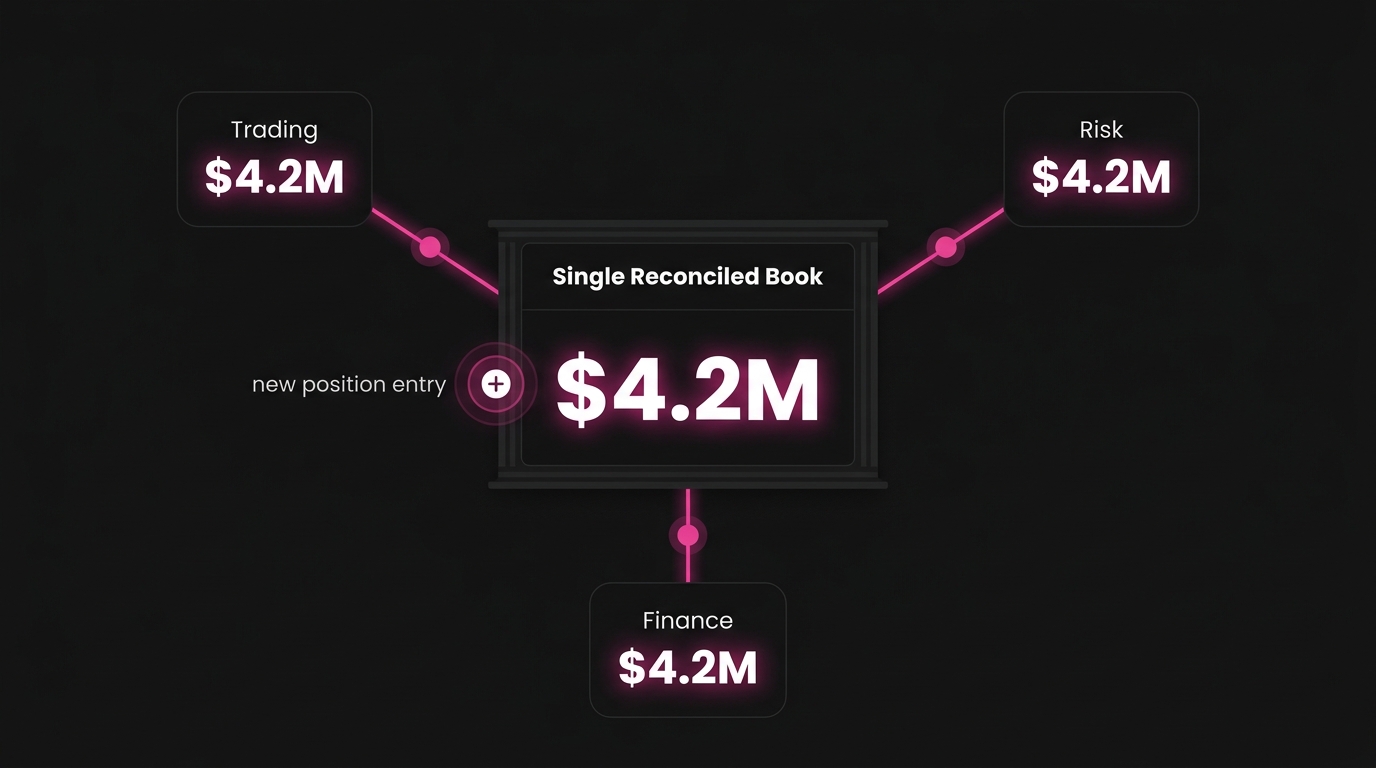

Single Book of Record: Real-Time Position Visibility

When a metals trader enters a new physical position, three teams need the same number at the same moment. A **single book of record** delivers exactly that: one reconciled exposure figure that updates simultaneously for trading, risk, and finance the instant a position is entered, with zero reconcil

LME Settlement Mechanics: What Most Platforms Miss

Most commodity platforms support LME as a listed exchange. Mastering **LME settlement mechanics** means modeling the Ring-based official price window, the full prompt date ladder, 750+ approved delivery grades, and warrant-level physical inventory data as an integrated system. These represent catego

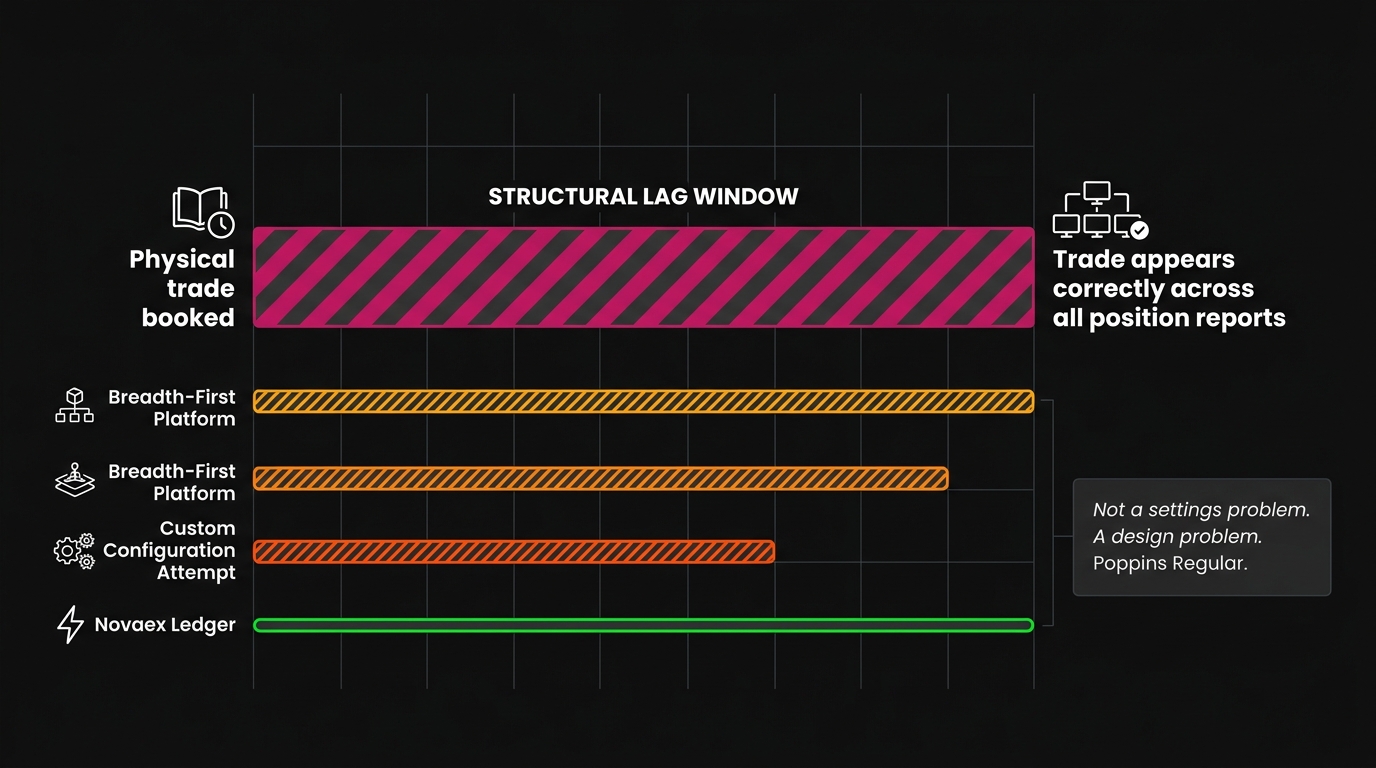

Why Reconciliation Lag Can't Be Configured Away

Reconciliation lag, the gap between when a physical trade is booked and when it appears correctly across all position reports, is not a configuration problem. It is a structural consequence of breadth-first commodity platform architecture. No settings adjustment, no implementation consultant, and no

Why Metals Trading Spreadsheets Fail at LME, COMEX, SHFE

Multi-tab spreadsheet formulas collapse under concurrent data loads during live metals trading. This failure mode is structural, not situational. When LME, COMEX, and SHFE pricing windows overlap, simultaneous RTD feed updates exceed Excel's single-threaded calculation engine's processing capacity,

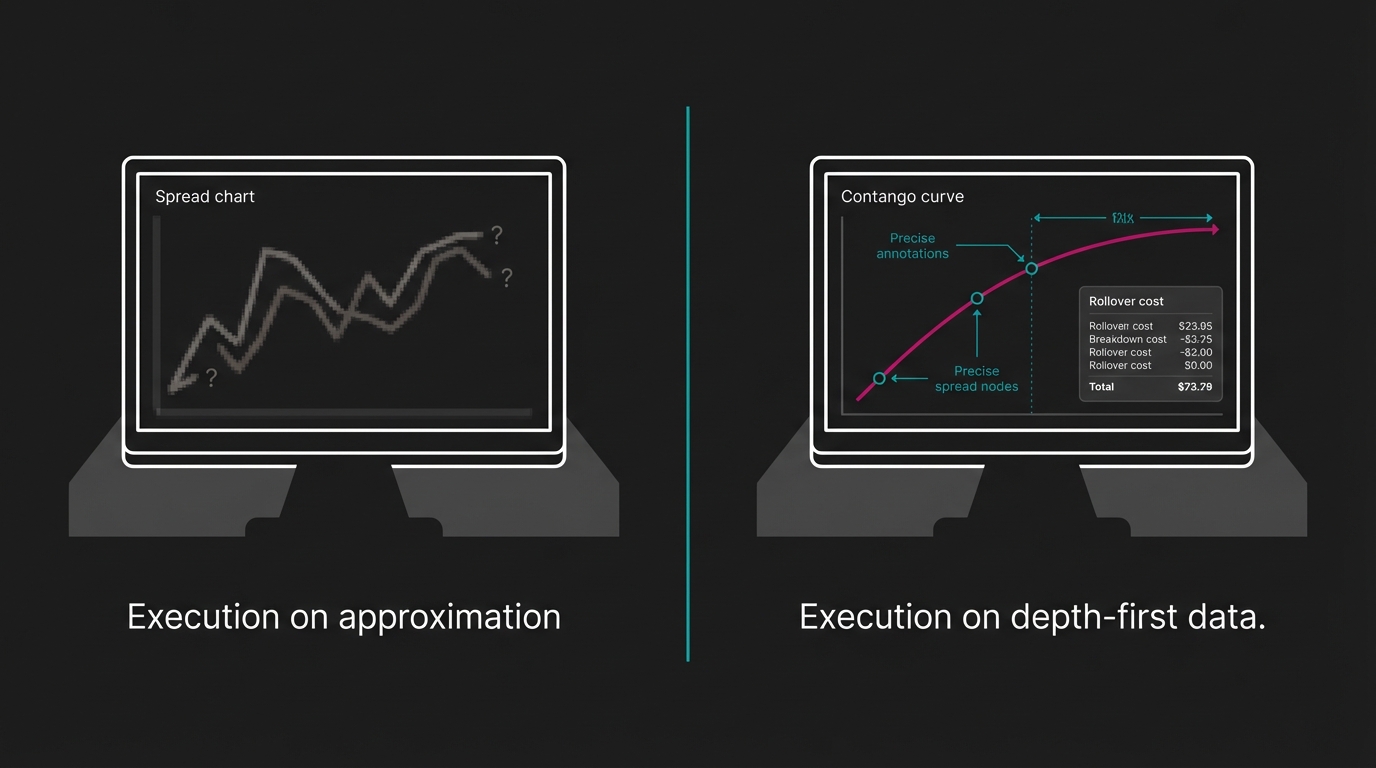

The LME Rollover Cost Spreadsheets Cannot Calculate

Spreadsheets cannot produce accurate LME rollover costs because the required data does not exist in any cell. Without live bid/ask depth and broker-accurate inter-month spread differentials, every rollover estimate is a structured approximation. If someone in your network manages metals exposure thr

Enterprise CTRM Cost: What Six Figures Actually Buys

Enterprise CTRM implementations carry a total first-year spend of $500,000 to $2 million and require 9, 18 months before a trader logs a single live position. These platforms were engineered for organizational compliance and multi-commodity book governance, rather than spread accuracy or rollover co

Metals Hedge Execution Data: Where Two Standards Diverge

The quality of your hedge execution is determined before you place the trade. **Metals hedge execution data** that reflects actual broker-quoted spreads across LME, COMEX, MCX, and SHFE gives traders a significantly different starting position than indicative pricing sourced from aggregated multi-co

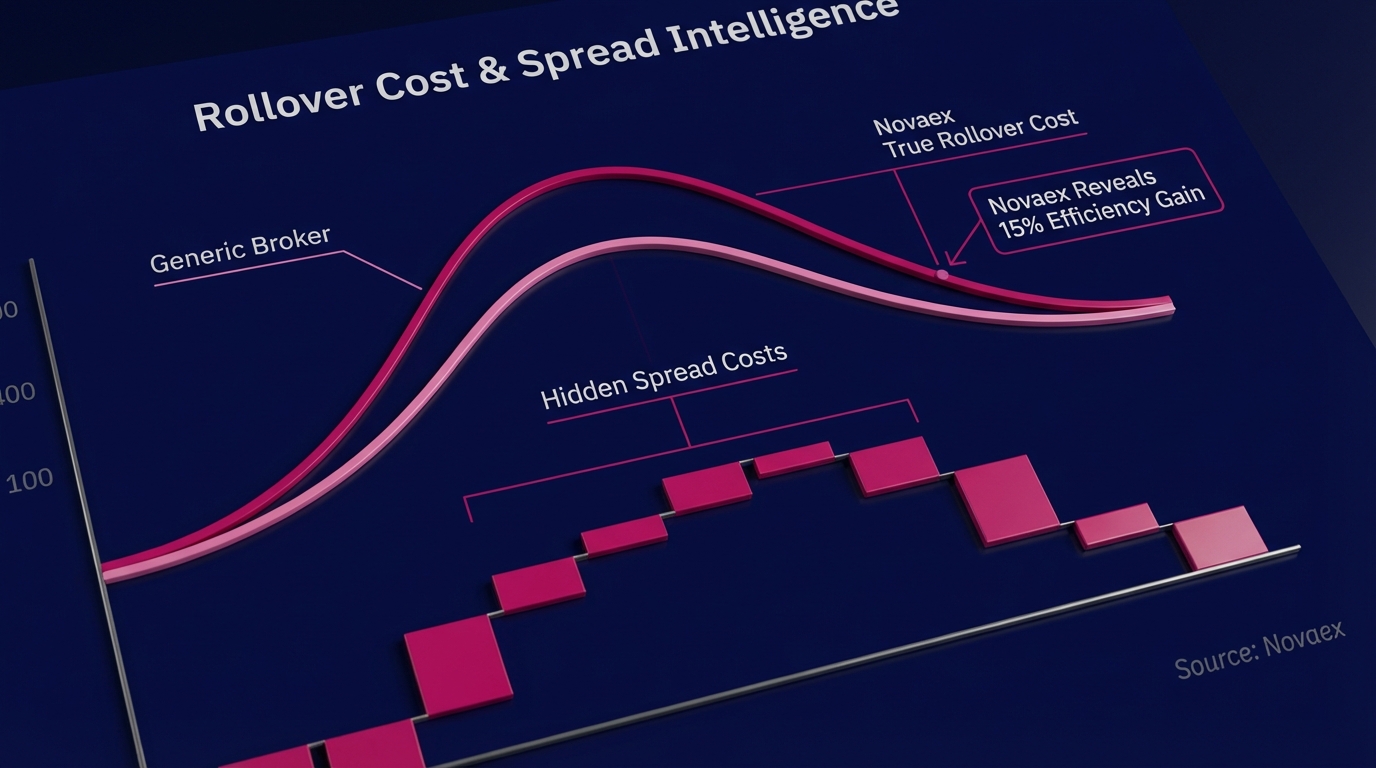

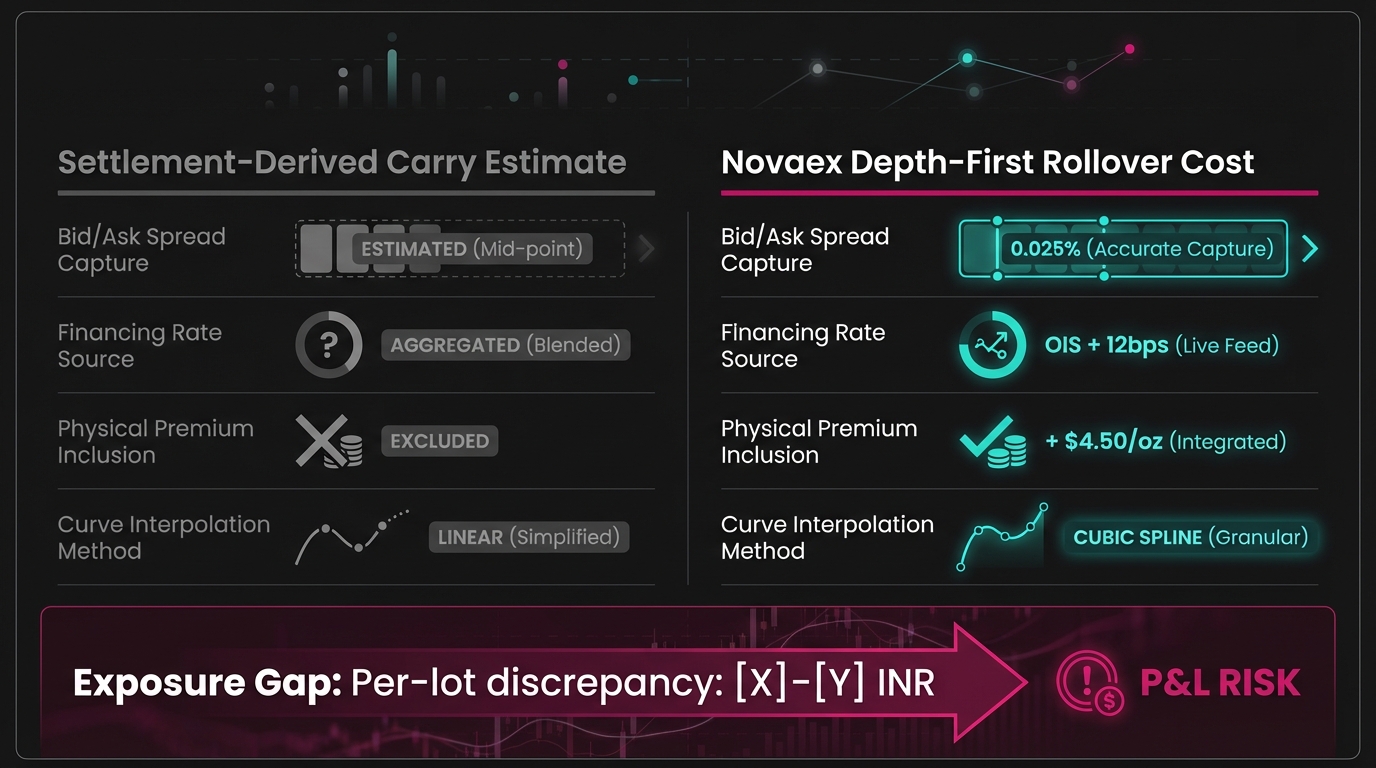

Rollover Cost Calculation: The Inputs a Settlement-Based Approach Does Not Capture

Most trading desks treat their platform's rollover estimate as a close approximation. The data is more specific than that. The gap between a settlement-derived carry estimate and a depth-first rollover cost calculation is not rounding error; it is a structural input omission that compounds with ever

Metals Spread Pricing Accuracy: Run the Hedge Audit

If your spread data comes from a generic multi-commodity platform, you likely have an unquantified pricing gap sitting inside your hedge book right now. **Metals spread pricing accuracy** acts strictly as a hedge execution cost variable rather than a platform feature. This post outlines the audit: f

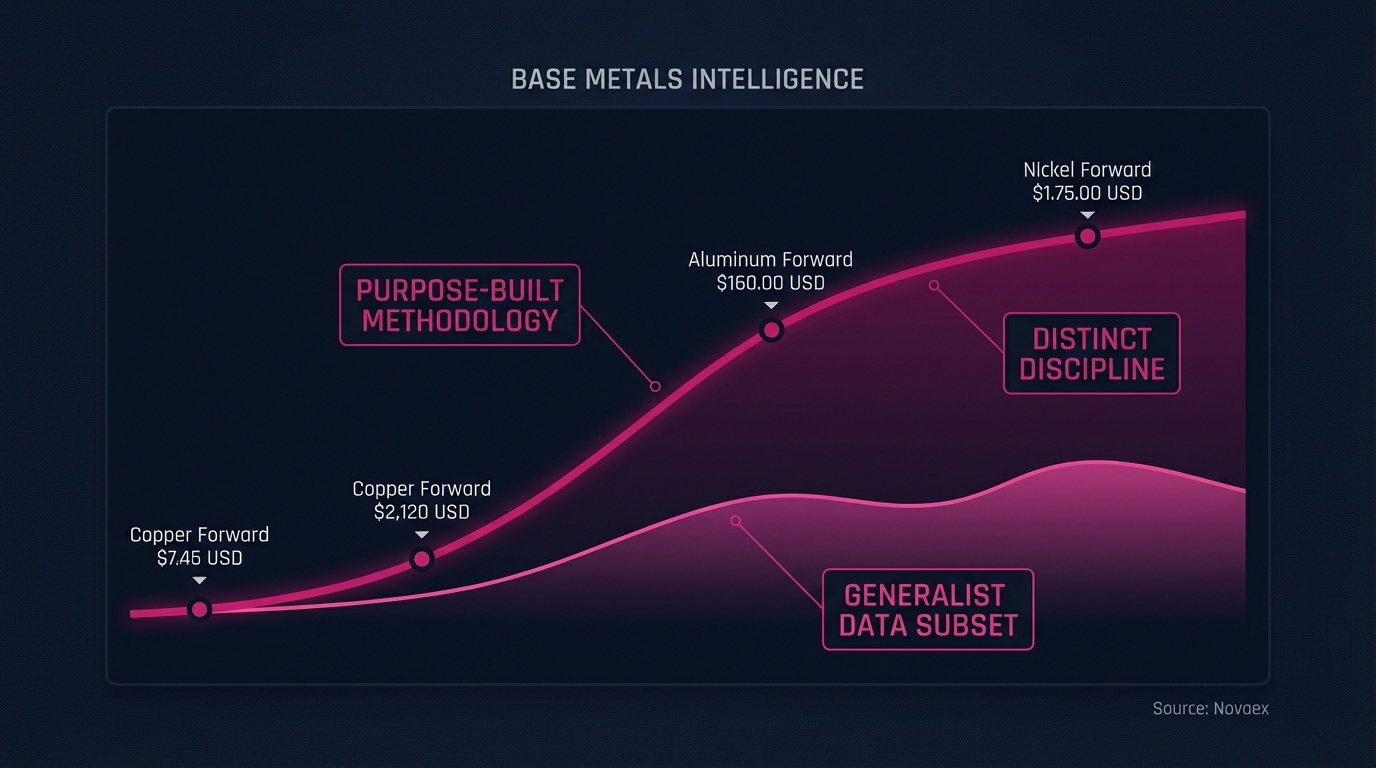

Base Metals Intelligence Is Not a Commodities Data Subset

Most commodity platforms approach coverage as a mapping problem: identify markets, ingest feeds, display outputs. The result is predictable: diluted intelligence distributed across every market while none is fully mastered. For a front-office metals trader managing LME positions under time pressure,

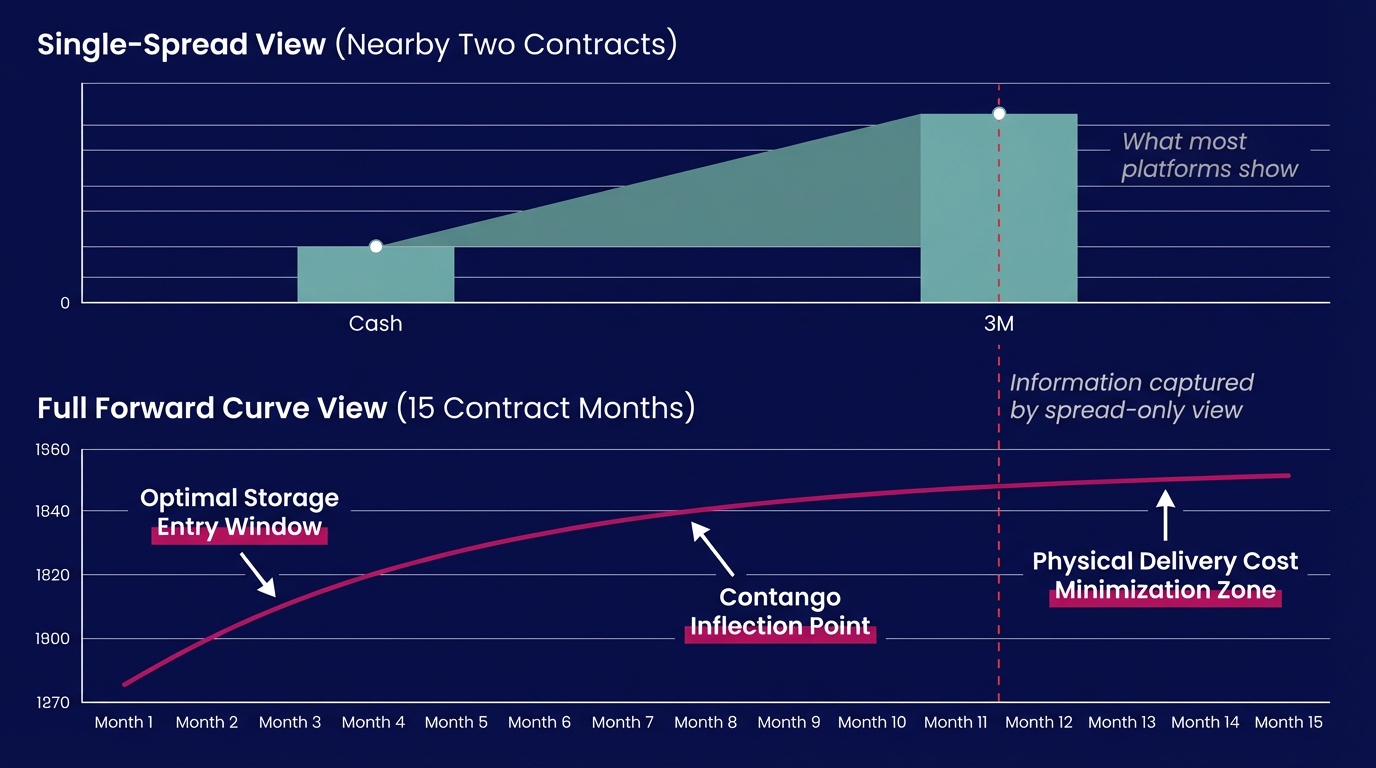

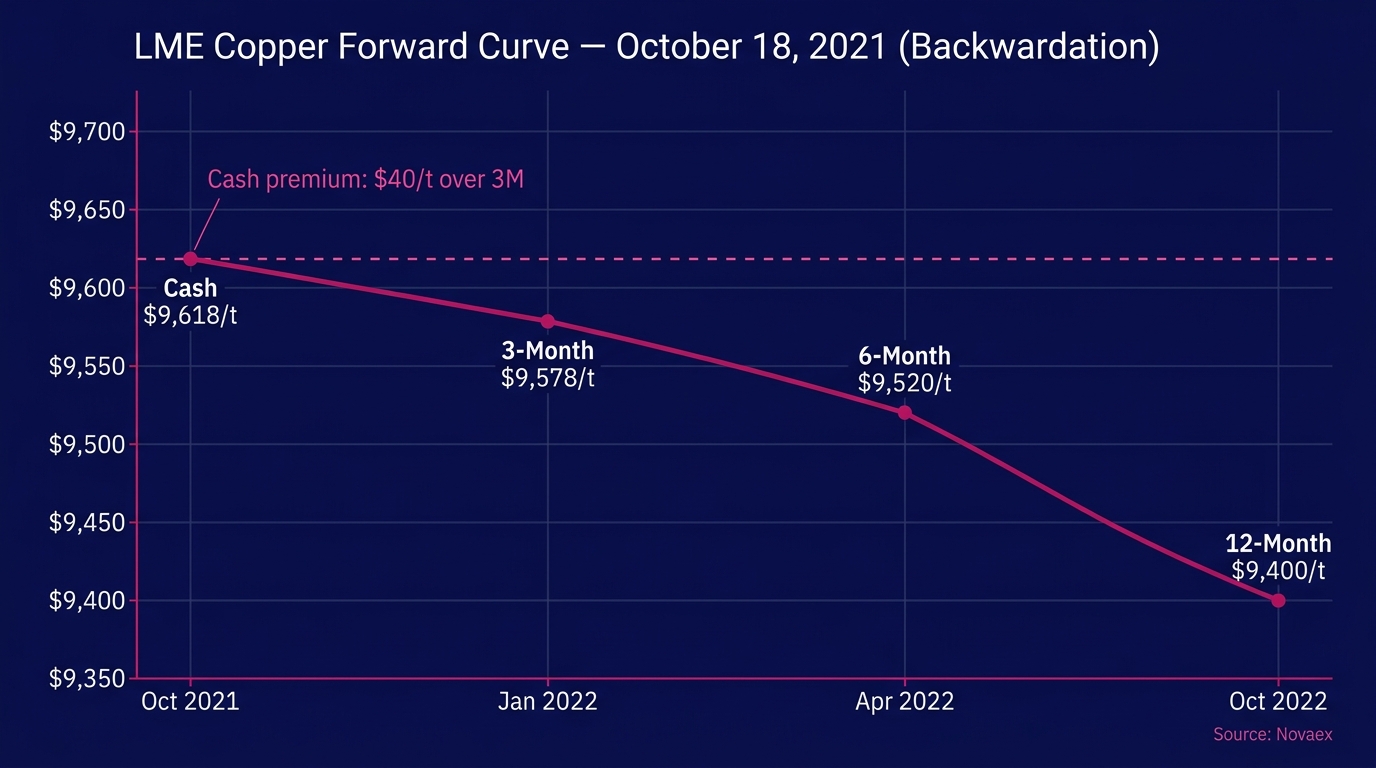

Copper Forward Curve: Why Spread Charts Miss the Mark

A single nearby spread tells you whether the copper forward curve is in contango or backwardation today. The full forward curve tells you *where* that structure changes, *how steeply*, and *how long* it persists. This information determines whether storing metal for three months profits more than st

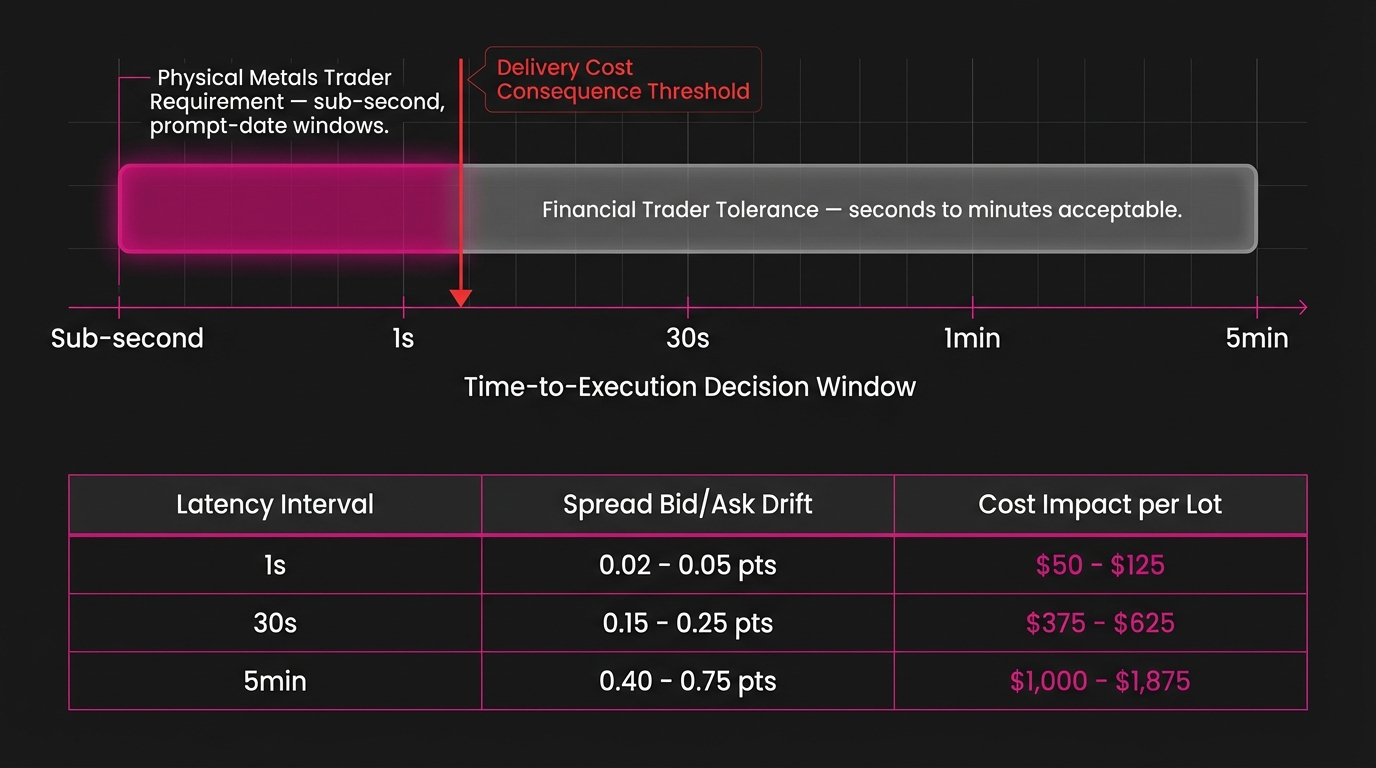

Physical Metals Data Latency: Why Prompt Windows Matter

Physical metals trading data latency functions as a direct delivery cost risk. When a prompt date approaches on the LME, spread decisions require broker-consistent, real-time bid/ask precision. A 30-second delay in that window operates as a measurable cost event. Financial traders can absorb data la

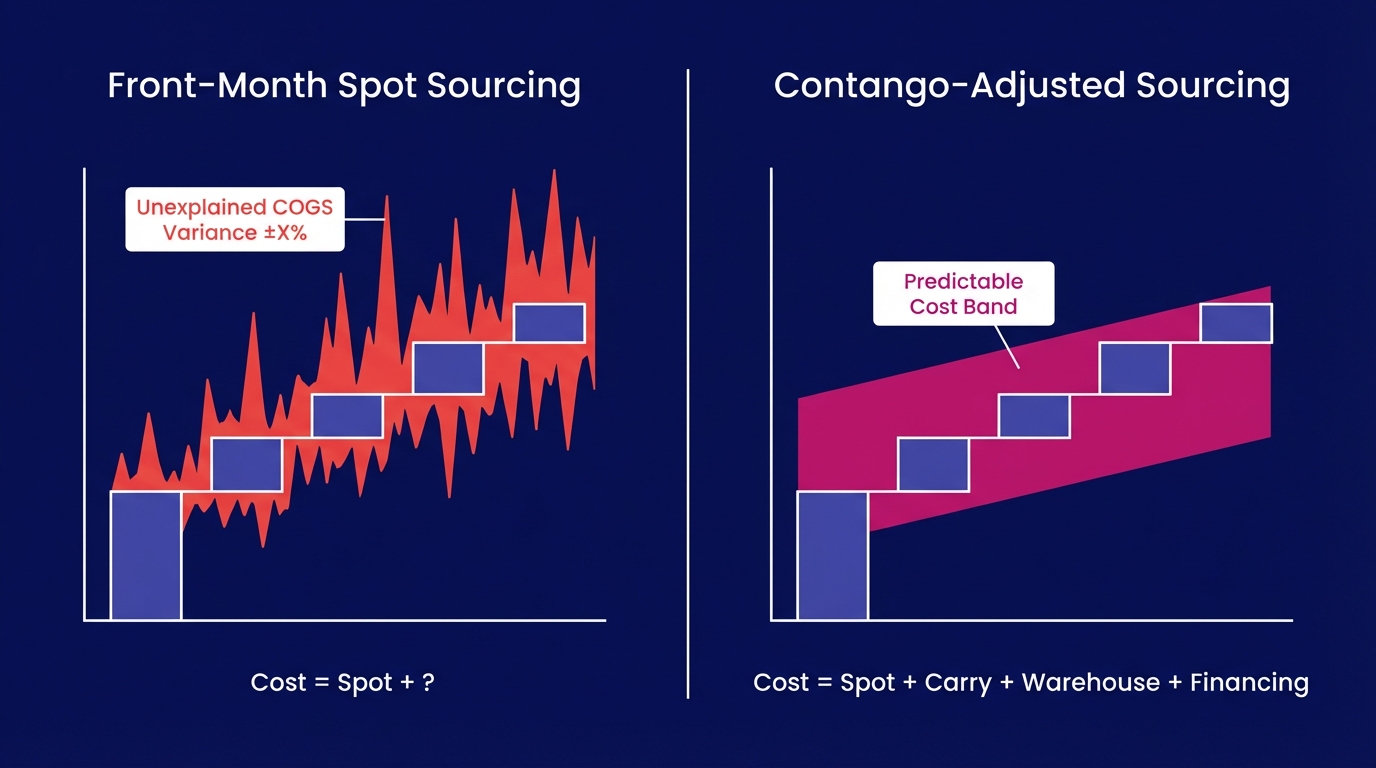

How Aluminum Contango Creates Hidden COGS Variance

Manufacturers who benchmark aluminum purchases against front-month spot prices (rather than the forward curve) embed contango-driven cost errors directly into COGS. When LME aluminum trades in contango, sourcing decisions anchored to cash prices systematically understate true delivered cost, generat

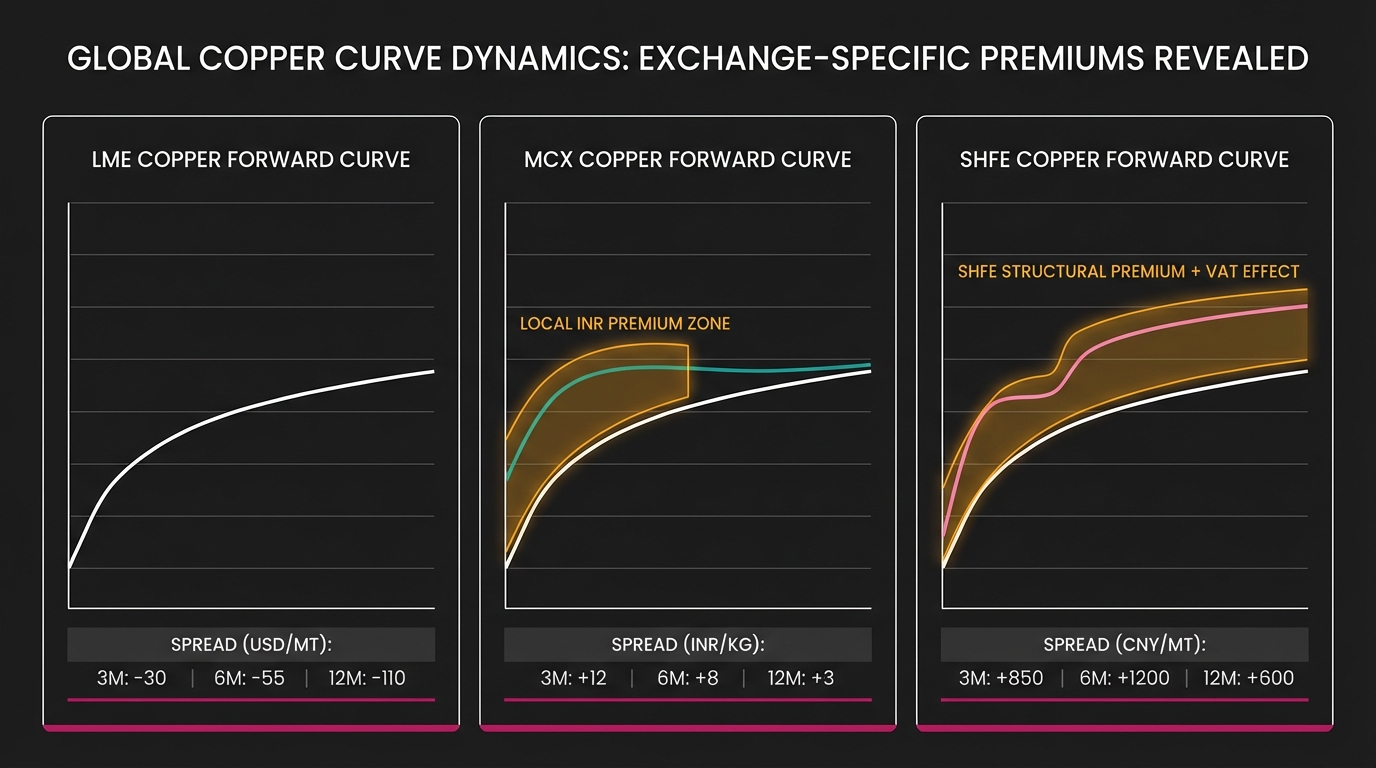

MCX Copper vs SHFE Copper: Curve Divergence Explained

MCX copper and SHFE copper are not localized versions of the same instrument. Each exchange carries distinct structural premiums (driven by denomination effects, warehousing rules, and delivery specifications) that diverge significantly from one another and from LME copper. Applying a single global

Aluminum Rollover Cost: Beyond the Prompt-Date Spread

LME stock reports show aluminum holdings at LME-approved warehouses averaged over 500,000 metric tonnes across 2023. This establishes warehouse rent as a structurally significant cost variable on any physical-linked position, rather than a rounding error. When the prompt spread trades at near-flat c

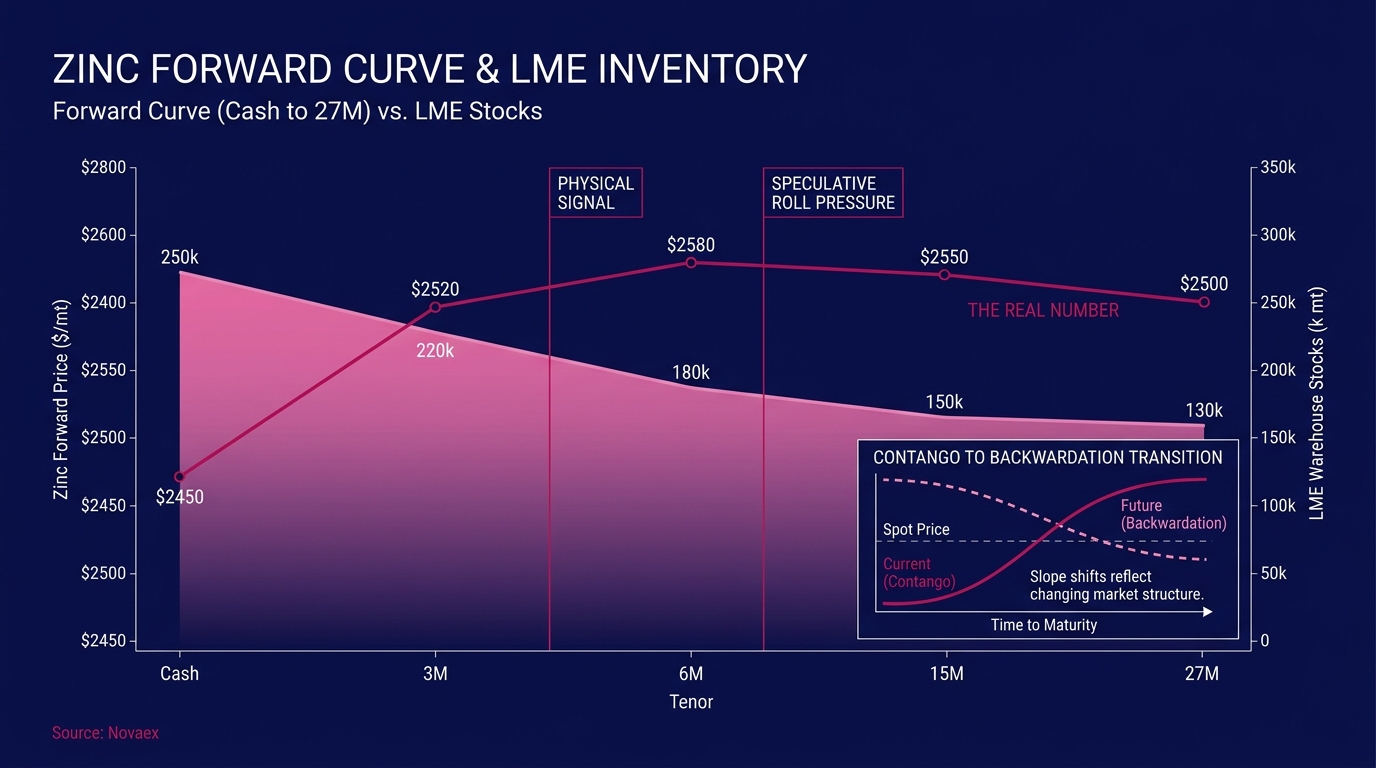

Zinc Forward Curve: Two Signals Every Buyer Must Read

To avoid these losses, buyers must identify both signal layers precisely, apply them to historical zinc curve episodes where they diverged, and establish what reading the zinc forward curve properly requires in practice.

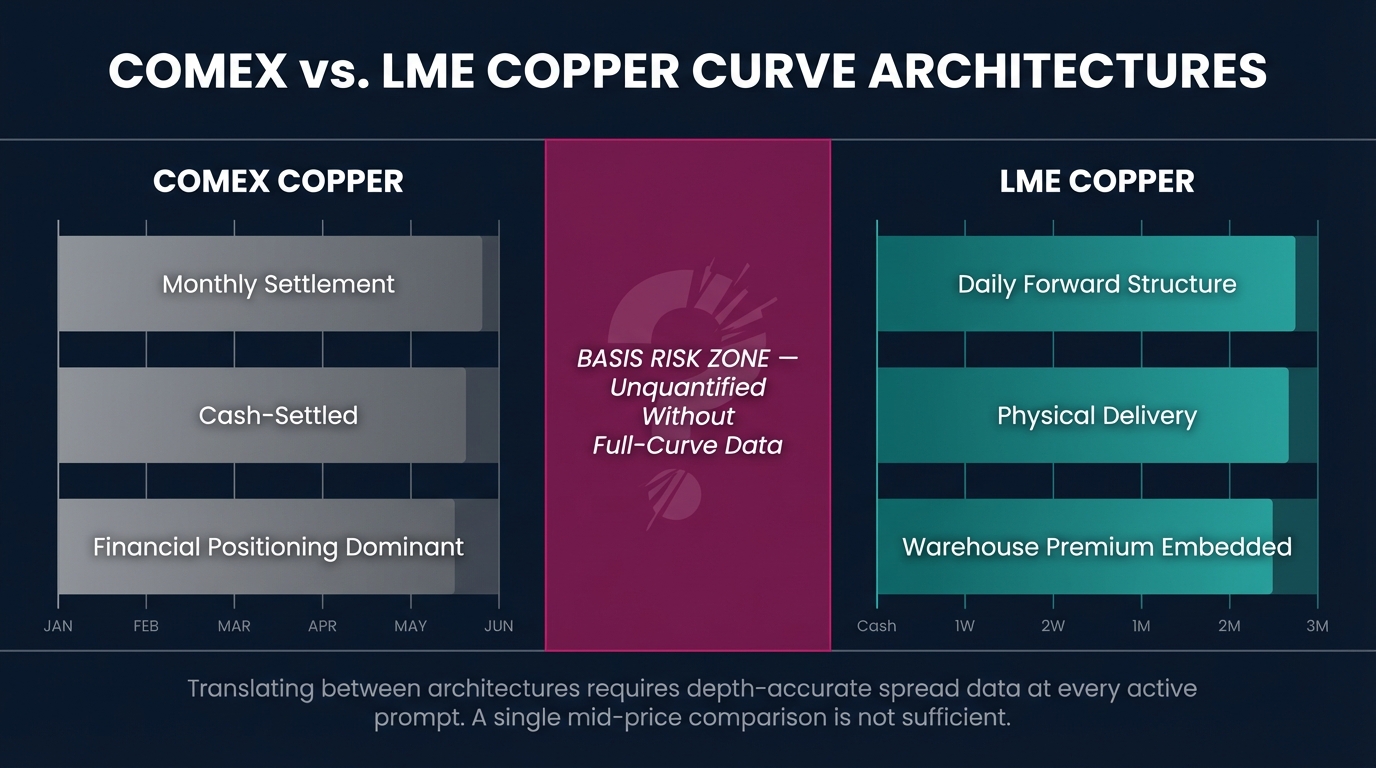

COMEX vs. LME Copper: Curve Architecture and Basis Risk

Most market participants treat COMEX and LME copper as two prices for the same metal. That operational equivalence is structurally inaccurate.

Copper Backwardation Forward Curve: The Delivery Timing Edge

When LME copper cash trades at a premium to the 3-month forward price, that gap carries a specific physical supply signal. This signal has a direct dollar value attached to every delivery timing decision in the position book. **Copper backwardation on the forward curve, read with full curve visibili

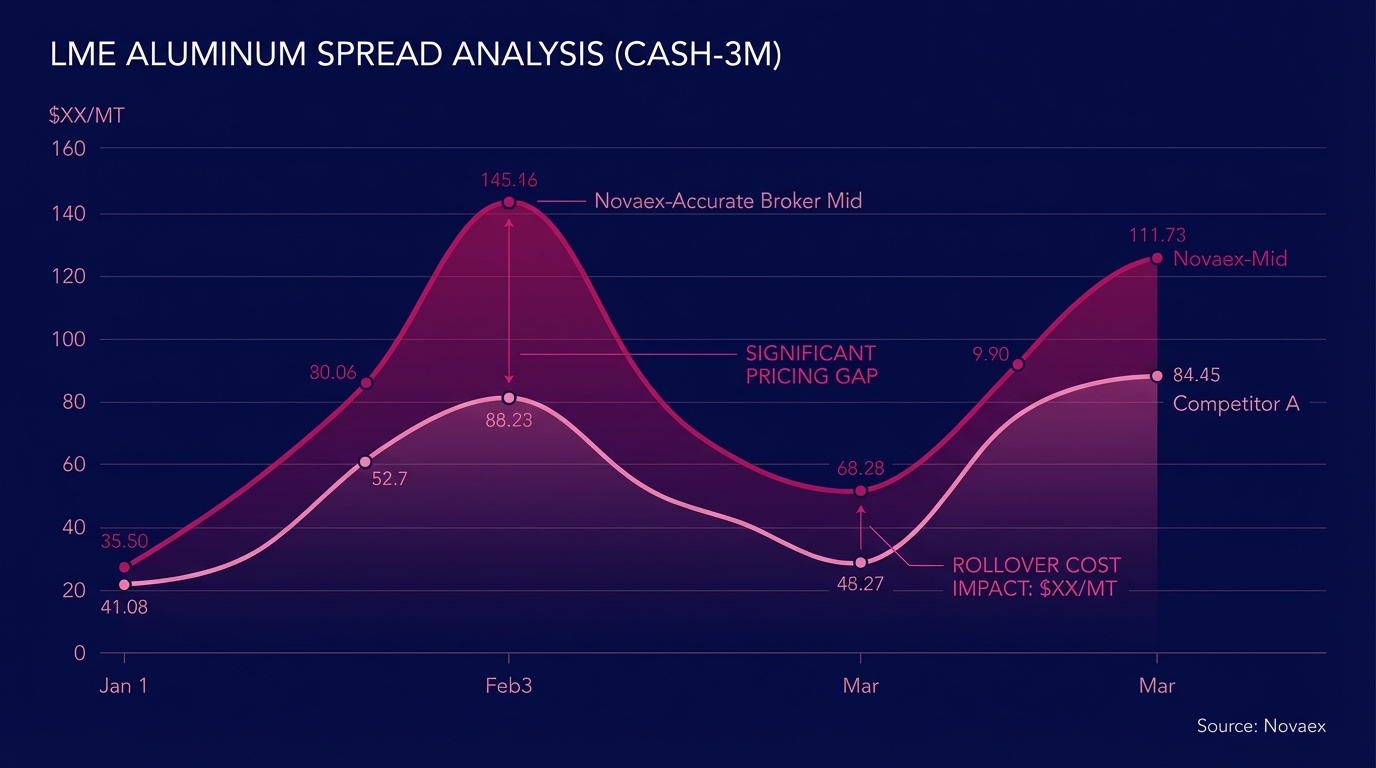

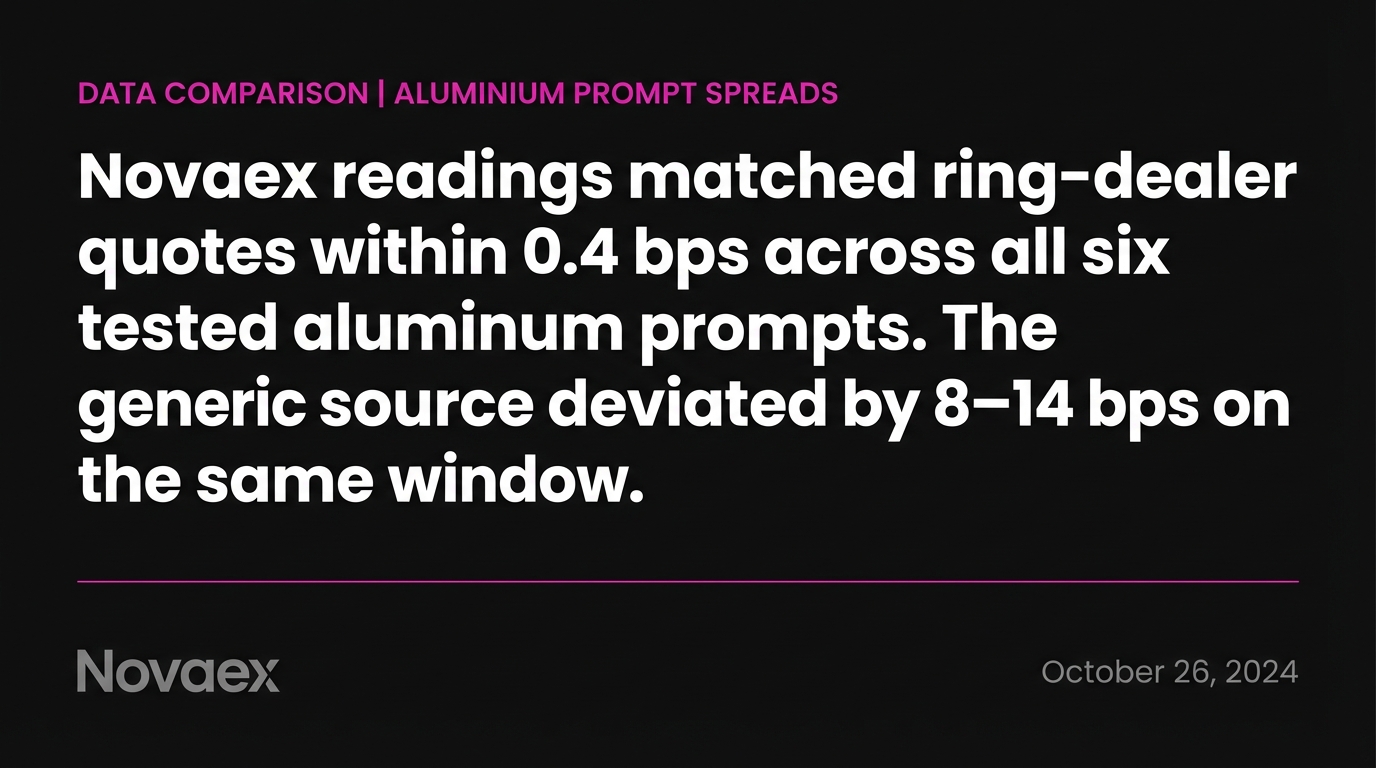

LME Aluminum Spread Accuracy: Novaex vs. Generic Sources

When Novaex aluminum spread readings are placed beside broker-quoted LME prompts from the same Ring session, near-term deviation holds below 4 basis points. A generic composite feed tested against the same five prompt windows shows 4 to 17 basis-point divergence, a gap that widens with tenor and com

Zinc Rollover Costs: What Front-Month Price Hides

This analysis traces exactly how zinc rollover costs accumulate across a multi-month physical position, quantifying each prompt date's contribution to the total cost basis.

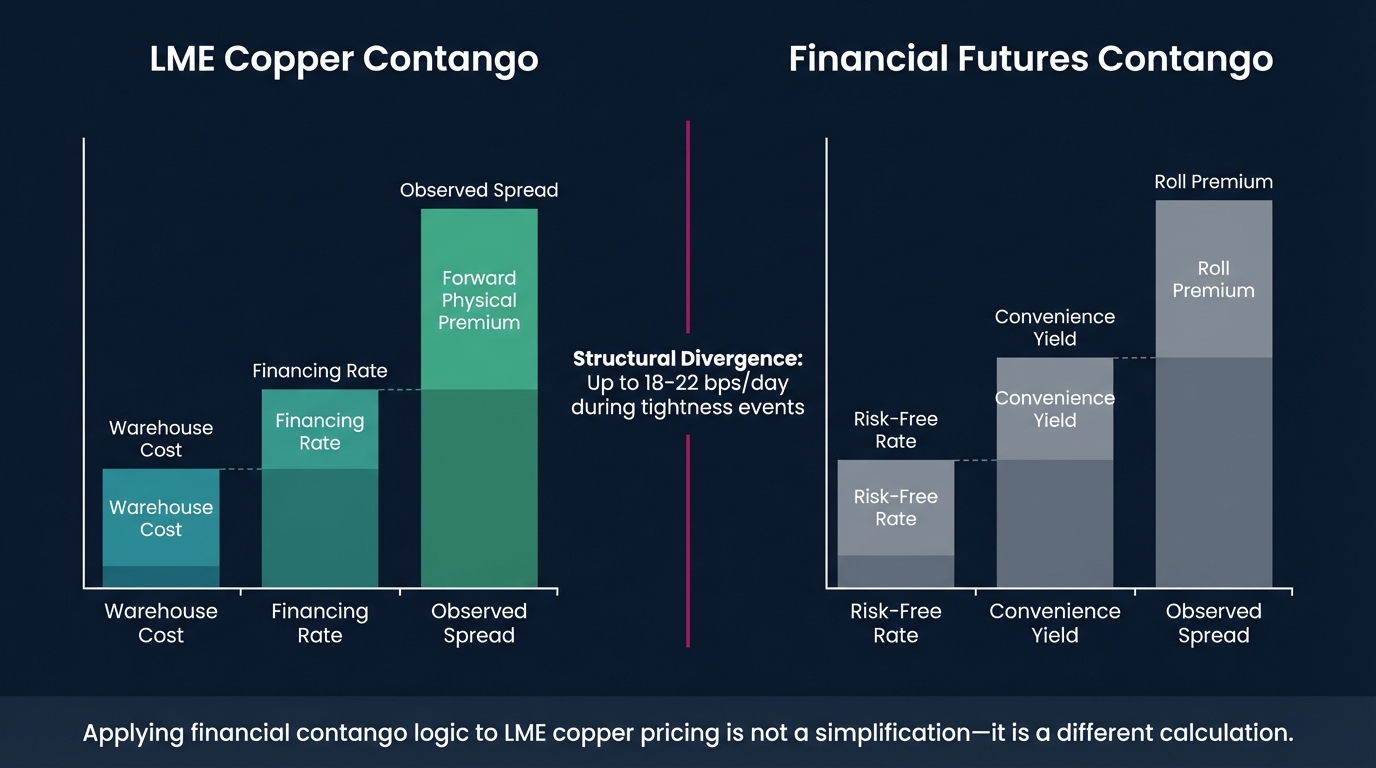

LME Copper Contango Is Not Financial Futures Contango

LME copper contango and financial futures contango share a name and almost nothing else in common. The LME's prompt-date architecture, ring-based price discovery, and warehouse-delivery mechanics produce a forward curve that is structurally incompatible with the cost-of-carry model governing financi

How LME Aluminum Spread Carry Costs Break Hedge Ratios

When a commodity platform treats the LME aluminum spread as a date-agnostic indicator rather than a prompt-date-specific carry instrument, it introduces measurable carry-cost errors into every hedge ratio calculation. Physical aluminum traders running 500-tonne positions absorb untracked basis expos

LME Forward Curve & Calendar Spreads: Metals Reference

The cash/3M spread, carrying charge formula, and cross-exchange basis are the three data layers that determine whether a hedge performs or leaks. Everything below is built from published LME, CME Group, and exchange-reported data.

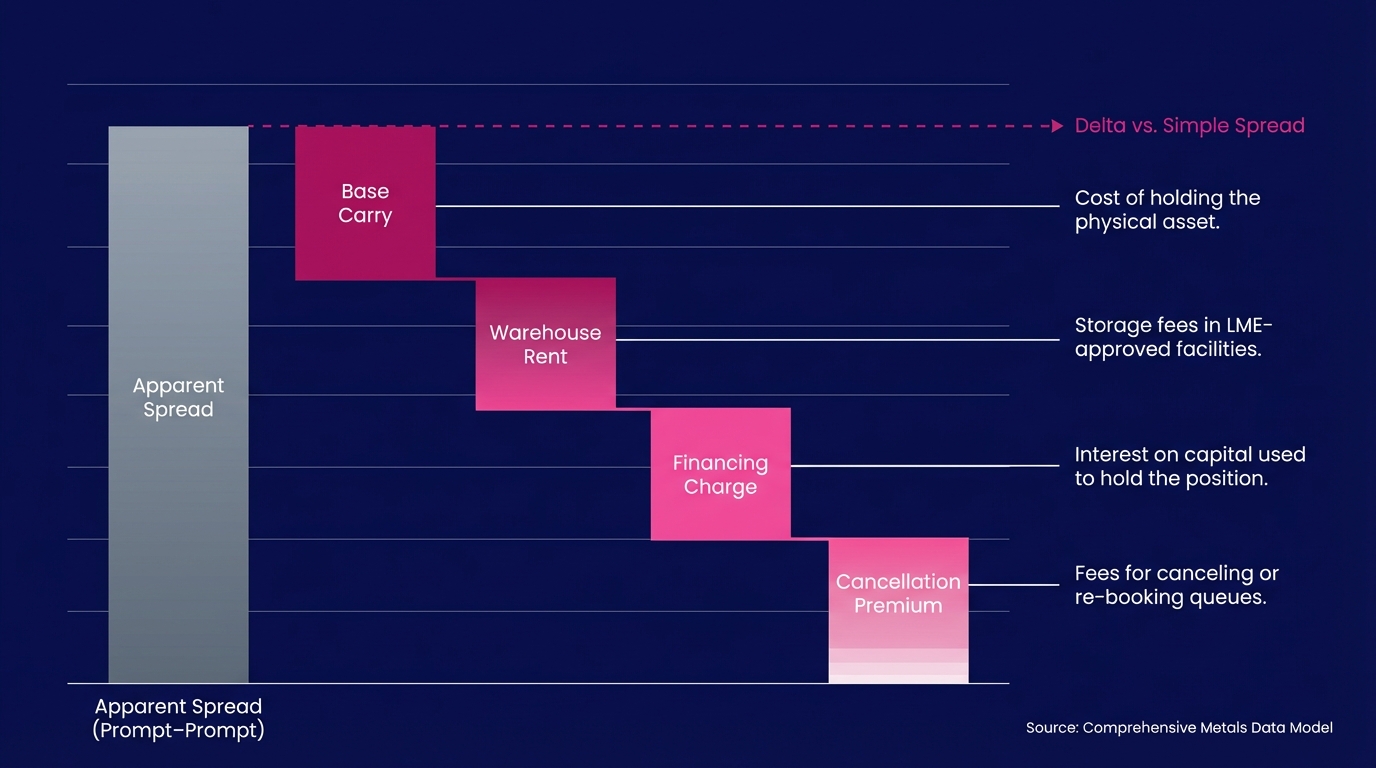

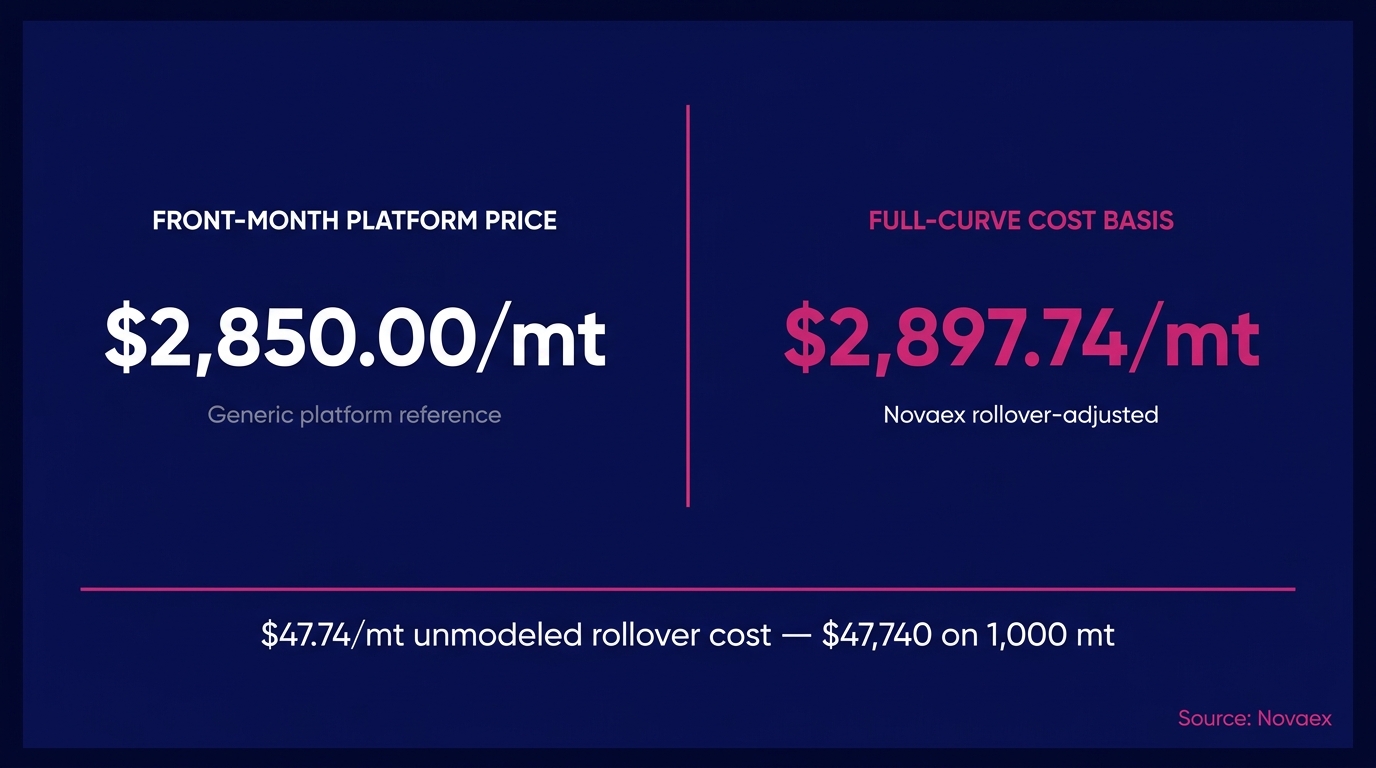

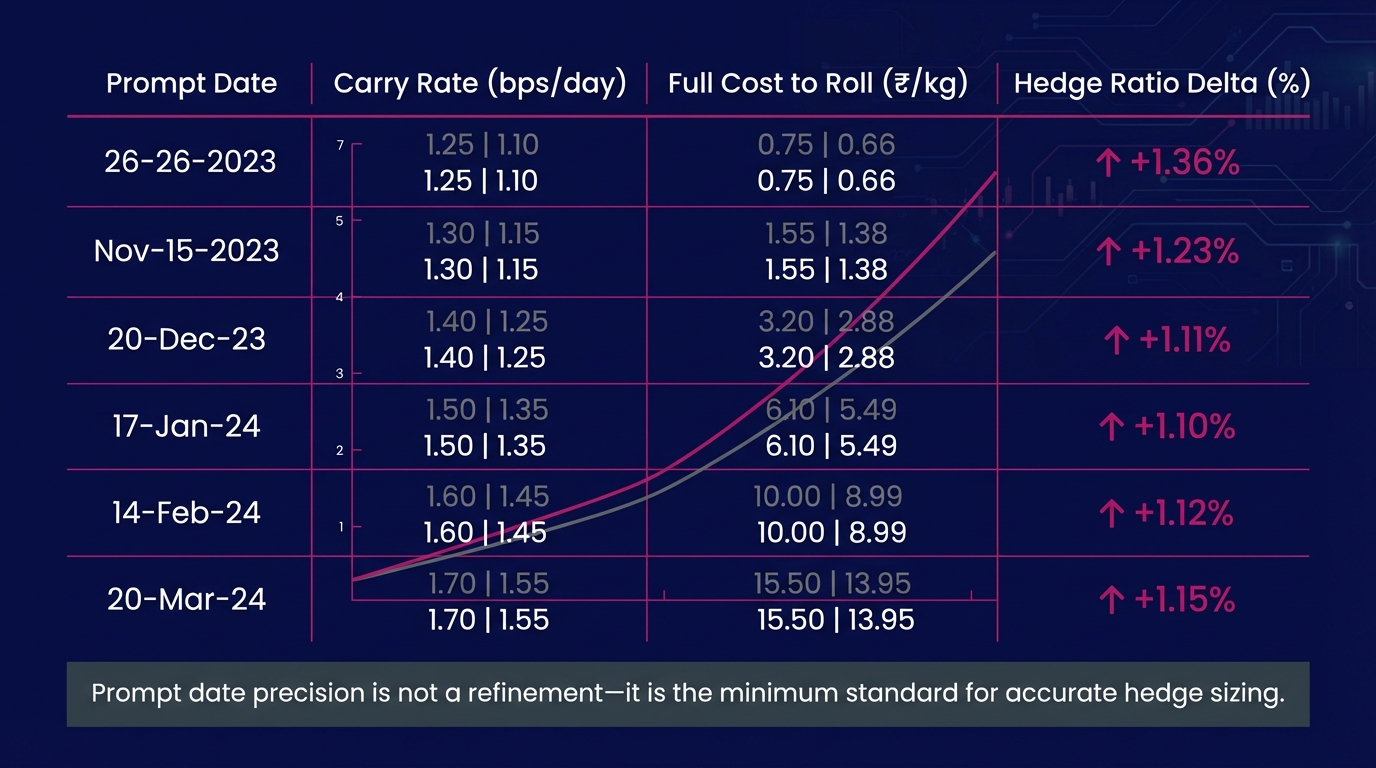

LME Copper Rollover Cost: The $15/MT Platform Shortfall

When a metals trader calculates LME copper rollover costs on a 3-month Copper Grade A position, the complete figure is **$47.80 per metric ton**. Standard multi-commodity platforms return $32.50/MT. The $15.30 difference (a **32% underestimate**) stems from the systematic exclusion of two cost compo

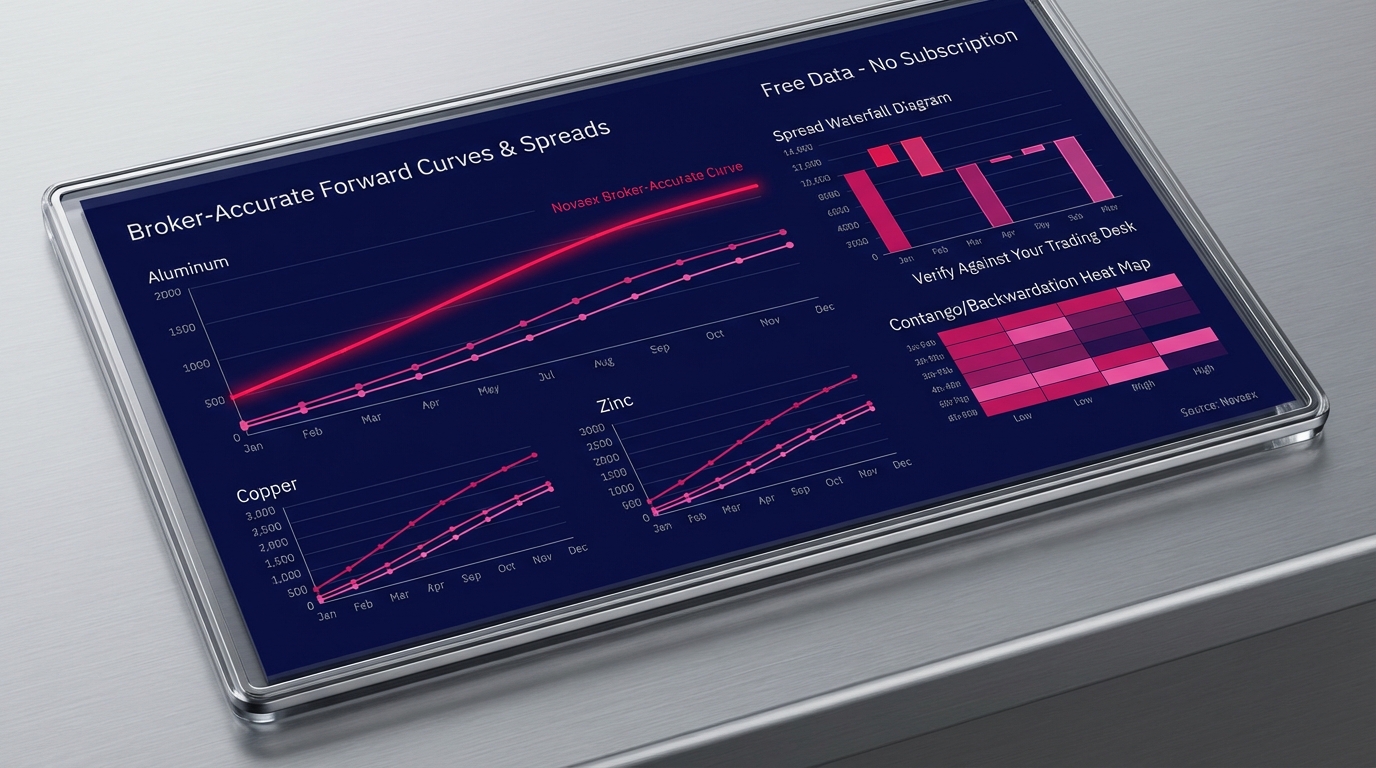

Broker-Accurate LME Forward Curves: Aluminum, Copper, Zinc

Novaex publishes broker-accurate forward curves for aluminum, copper, and zinc, simultaneously, at no cost. The term structures match what your broker desk produces, from cash through the 3-month benchmark to the outer dated prompts. Take the LME Copper December/March calendar spread visible on the

The Real Problem in Commodity Buying: Decisions Trapped in Spreadsheets

Every commodity team I know does three things brilliantly: negotiate, move fast, and hustle. But the decision layer is broken. Prices change by the minute; approvals take days.

Novaex × NVIDIA Inception Program: Clarity in a Volatile Market

Pricing and risk decisions shouldn't live in spreadsheets and email threads. We're building Novaex, an AI decision engine that brings live pricing, exposure, approvals and hedge actions into one place.

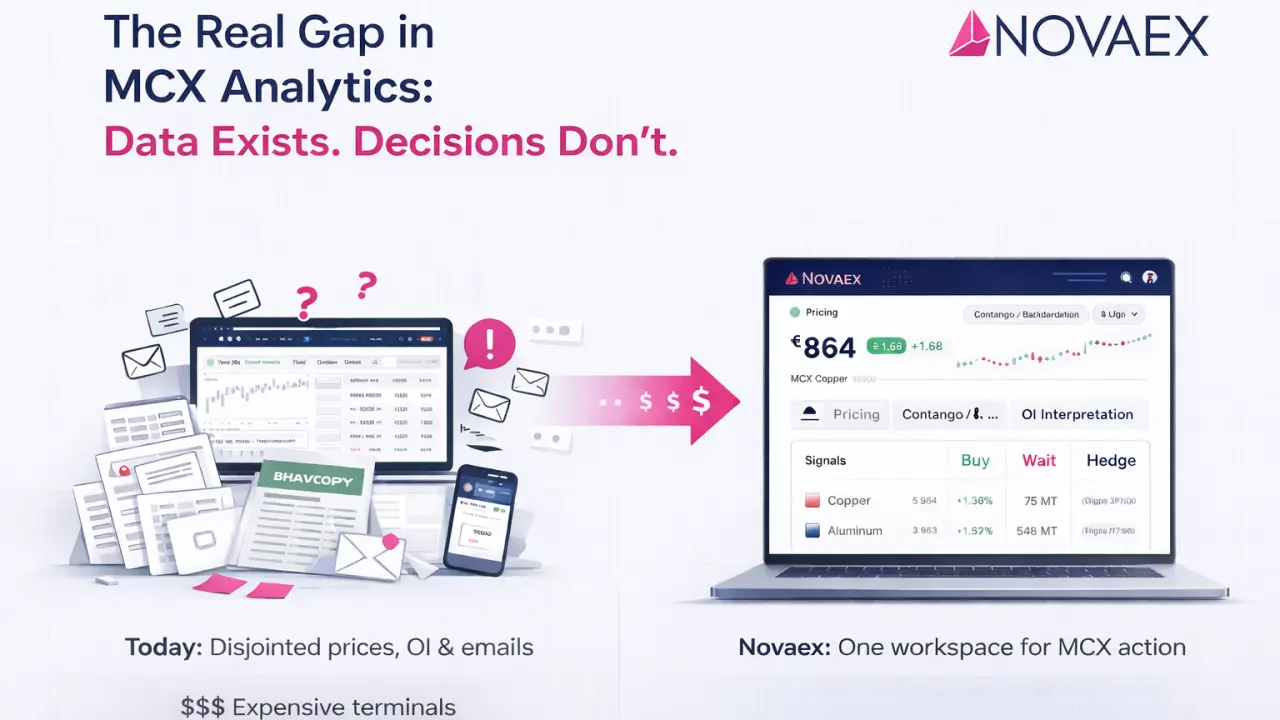

The Real Gap in MCX Analytics: Data Exists. Decisions Don't.

Most commodity teams in India aren't short on numbers. They're short on context and workflow. The tools available today fall into two extremes — and neither delivers the decision layer buyers need.