The Break Elimination Framework for Physical Metals Trading

Physical metals trading desks lose measurable margin to seven recurring operational breaks. These are predictable failures with specific mechanisms, documentable costs, and a defined elimination sequence. The break elimination framework names, sequences, and measures each break by margin impact, giving trading desks the shared vocabulary to identify, prioritize, and resolve the operational failures that most platforms leave entirely undocumented.

Position-reconciliation failures, delivery instruction mismatches, and unexplained end-of-day P&L discrepancies are instances of a taxonomy that exists whether or not a desk has named it. The framework makes that taxonomy explicit.

According to a 2022 Ernst & Young survey of commodity trading operations, 67% of commodity trading firms cite data fragmentation as their primary operational risk factor, yet fewer than one in four have a documented taxonomy for the specific break types that fragmentation creates commodity trading operational risk benchmarks.

That absence of taxonomy is itself a cost center. When a break has no name, it has no owner. When it carries no position in a priority stack, it gets addressed in order of noise, not margin.

Why Physical Metals Trading Breaks Go Unnamed

Most trading desks share a version of the same operational pattern. A position does not reconcile. A mark diverges from where the desk traded. A counterparty's settlement confirmation arrives with a date that conflicts with the internal booking.

These events are logged, discussed, and eventually resolved. However, they are rarely named with precision. Without precise naming, the same break recurs. Without sequencing, desks address the visible break rather than the highest-cost break.

The Root Causes of Costly Breaks

The most costly breaks in physical metals trading arise from cross-venue pricing divergence and position-to-hedge coverage drift, rather than from execution errors. These two break types are expensive precisely because they accumulate silently across the entire book before becoming visible, affecting every trade's effective margin rather than isolated transactions.

McKinsey's Global Commodity Trading Survey found that top-quartile trading operations capture 15, 20% more margin than median performers. This differential is attributable primarily to operational precision rather than superior market intelligence McKinsey global commodity trading survey. The precision gap begins with the ability to name what is going wrong.

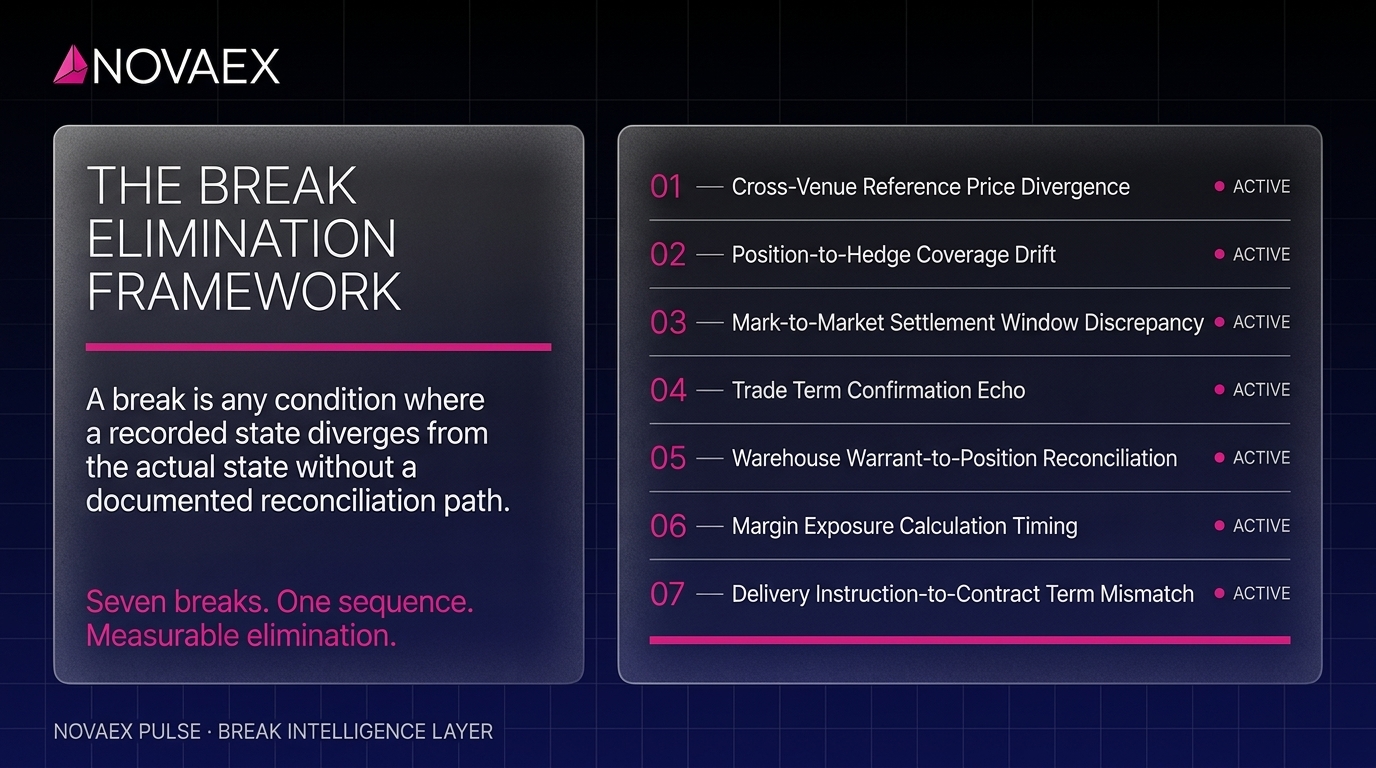

A break, as the term is used throughout this framework, is any condition where a recorded state (position, price, exposure, or delivery term) diverges from the actual state without a documented reconciliation path. A break is an operational failure that creates exposure to market loss, settlement failure, or counterparty dispute. That distinction is operationally significant: breaks are preventable. Market losses are not.

The Break Elimination Framework: Structure and Purpose

The break elimination framework rests on a single operational principle: you cannot eliminate what you have not named. Every break in physical metals trading has a specific mechanism: a point in the workflow where two systems, two data sources, or two sets of contractual terms diverge and the divergence is not caught in real time.

The framework does three things:

- Names each break with a mechanism description precise enough that any member of the desk can identify it when it occurs

- Sequences breaks by margin impact, not by operational occurrence. This helps desks prioritize elimination in order of cost rather than the volume of complaints

- Measures each break by its characteristic exposure signature so that performance against elimination targets can be tracked over time

Physical Metals Trading Breaks 1, 2: The Highest Margin Exposure

Break #1: Cross-Venue Reference Price Divergence Break

Mechanism: A physical contract is priced against one exchange settlement (LME cash, for example) while the hedge is placed on a different venue (COMEX or SHFE) without a real-time basis track between the two reference prices. The basis differential between venues accretes silently until settlement, at which point the desk discovers that the hedge did not cover the actual pricing exposure embedded in the physical contract.

The LME reports that daily copper volumes regularly exceed 400,000 lots (25 tonnes per lot). At this scale, even a 0.1% pricing reference divergence compounds into six-figure exposure within a single trading session LME copper market statistics. This break is the product of a workflow that treats LME, COMEX, SHFE, and MCX as separate data environments rather than as simultaneous components of a single pricing picture for the same underlying metal.

This break ranks first in the taxonomy because it operates at book-wide scope. Every position hedged across venues carries the exposure until the basis is tracked and reconciled in real time.

Break #2: Position-to-Hedge Coverage Drift Break

Mechanism: The aggregate hedged position in the financial book diverges from the running physical position because new purchases, warehouse confirmations, and title transfers are not fed into the hedge ratio calculation in real time. Each unconfirmed delivery, each warrant movement not yet booked, each physical contract amendment creates an incremental uncovered exposure that the risk system does not see.

The characteristic signature of this break is a hedge ratio that appears correct at market open and incorrect at market close, with the discrepancy explained only after the fact by a sequence of unbooked physical events. In fast markets (precisely the conditions under which unhedged exposure is most expensive), the lag between physical event and system update is longest, because the operations staff recording the events are managing the same market volatility the traders are responding to.

The Basel Committee on Banking Supervision has documented that operational failures in commodity trading contribute up to 12% of total trading losses in years with significant market volatility Basel Committee operational risk in commodity trading. Coverage drift is among the primary contributing mechanisms.

Physical Metals Trading Breaks 3, 4: Timing and Confirmation Discrepancies

Creating P&L Exposure Through Timing Discrepancies

Mark-to-market timing discrepancies create P&L exposure when different segments of the same book are valued against settlement snapshots taken at different times or against different price references: LME official versus LME closing versus a 3-month forward. The resulting P&L is internally inconsistent and cannot accurately represent actual market exposure, causing risk limits to be applied against a composite number that does not correspond to any single point in the market.

Break #3: Mark-to-Market Settlement Window Discrepancy Break

Mechanism: Spot positions, forward positions, and options delta are marked using different settlement snapshots. Some are drawn at LME ring close, others at COMEX settlement, and others at a system refresh during an intraday price spike. The aggregate P&L reported to the desk and to risk management reflects a composite of these different settlement windows, not a consistent market state.

The cost is not confined to the P&L misstatement itself. It extends to the trading decisions made against a false number: positions held or reduced based on exposure figures that do not accurately represent what the desk owns at current market prices. According to the International Commodity Trading Association, settlement discrepancies in physical commodity trades add 0.2, 0.5 basis points of drag per trade, a figure that aggregates into millions annually for desks executing at volume ICTA physical commodity settlement efficiency.

Break #4: Trade Term Confirmation Echo Break

Mechanism: The internal booking of a physical trade captures terms (pricing period, settlement date, delivery location, quality specification, lot tolerance) that differ by one or more parameters from the counterparty's confirmation. The discrepancy is not surfaced until pre-settlement matching, at which point it becomes a dispute requiring negotiation, adjustment, or in worst cases, a delivery failure.

This break is named an echo because the internal booking and the counterparty confirmation are similar enough to pass a superficial review. The divergence lives in a single field: a date boundary, a tolerance percentage, or a pricing period definition that only becomes material when delivery is imminent. Research from the Commodity Markets Council indicates that physical delivery disputes cost commodity desks an average of $150,000 per incident when including renegotiation costs, storage accrual, and opportunity losses Commodity Markets Council delivery dispute cost analysis.

Physical Metals Trading Breaks 5, 7: Reconciliation and Delivery Exposure

Understanding Warehouse Warrant Reconciliation Breaks

A warehouse warrant reconciliation break occurs when the number and specification of warrants held in a registered LME or exchange-approved warehouse does not match the physical inventory position recorded in the trading system. The break creates a phantom inventory (an asset present in one record but absent in the other) which inflates apparent hedge coverage and understates actual unhedged exposure until a manual count corrects the discrepancy.

Break #5: Warehouse Warrant-to-Position Reconciliation Break

Mechanism: Warrant transfers, cancellations, and new registrations are processed by the warehouse management system on a lag (often same-day or next-day) while the trading system reflects the position as booked at trade execution. Any warrant movement occurring between booking and system update creates a transient position discrepancy that, in fast markets, represents real unhedged exposure that the desk cannot see.

According to Roper Technologies' CTRM market research, firms using integrated trading platforms reduce reconciliation-related breaks by an estimated 60, 70% compared to operations dependent on spreadsheet-based workflows Roper Technologies CTRM platform performance research. The warrant reconciliation break is among the most direct beneficiaries of that integration because it is driven entirely by data latency, not by trading complexity.

Break #6: Margin Exposure Calculation Timing Break

Mechanism: Initial margin and variation margin requirements are calculated against end-of-day settlement prices while the desk runs active intraday positions against live markets. The margin exposure reported to risk management and treasury is stale by hours at exactly the moment a fast-moving market demands accurate liquidity visibility.

The signature of this break is a liquidity surprise: a margin call arrives at a level the desk did not see approaching because the exposure calculation did not reflect the intraday price move that triggered it. In base metals markets where intraday copper volatility can exceed 2, 3% during LME ring sessions LME intraday volatility data, the gap between a stale margin calculation and a live margin requirement is quantifiable and preventable.

Break #7: Delivery Instruction-to-Contract Term Mismatch Break

Mechanism: The delivery instruction issued to the warehouse or logistics counterparty specifies a shape, location, or date that does not match the contractual commitment. The break surfaces at the point of physical delivery as a dispute over whether the delivered material satisfies the contract, triggering storage accrual, renegotiation costs, or outright rejection.

This break ranks lowest in the taxonomy by margin impact per occurrence. Its cost is bounded: it affects specific deliveries rather than the entire book simultaneously. The cross-venue and coverage drift breaks above it can affect every position at once. That difference in scope determines the sequencing.

How Break Elimination Compounds: The Sequence Dependency

The Compounding Effect of Break Elimination

This is the structural insight that makes sequencing by margin impact the correct approach. The seven breaks are not independent events. Cross-venue reference price divergence (Break #1) introduces the incorrect price reference that surfaces later as a mark-to-market settlement discrepancy (Break #3). Coverage drift (Break #2) that goes uncorrected distorts the hedge ratio used to calculate margin exposure (Break #6).

The sequence dependency means that eliminating breaks at the top of the taxonomy produces compounding recovery. A desk that resolves Break #1 does not simply stop losing margin to cross-venue divergence; it also reduces the frequency and severity of downstream breaks that the divergence was generating as a secondary effect.

The Accenture benchmarking data substantiates this pattern: top-performing commodity trading operations do not simply have fewer breaks in aggregate. They have fewer active breaks at the top of their taxonomy, and their lower-tier breaks are less severe because they are not being compounded by upstream failures that were never resolved.

This is the structural argument against fixing the loudest break first. The loudest break (the one generating the most desk-level conversation) and the most expensive break are rarely the same event. A framework without explicit sequencing by margin impact will consistently solve for noise over cost.

Applying the Break Elimination Framework to a Physical Metals Desk

Core Vocabulary for Break Elimination

A metals trading desk requires six terms as the operational foundation of break elimination: break (the divergence condition between recorded and actual state), discrepancy (the measured difference between two records), exposure (the market risk created by an unresolved break), loss (the realized margin cost of exposure that was not eliminated), reconciliation (the process of resolving a discrepancy to a single confirmed state), and elimination (permanent removal of the mechanism that generates a break type). These six terms allow a desk to communicate about operational failures with precision, without ambiguity about what is being described or who is responsible for resolving it.

Implementing break elimination begins with adoption of the taxonomy, not with a technology procurement decision. The seven breaks described here exist in desks running advanced CTRM platforms and in desks running spreadsheets. The platform affects the speed and automation of detection. It does not change the existence of the breaks or the cost of leaving them unnamed.

The implementation sequence follows the taxonomy directly:

- Document current break frequency and cost for each of the seven break types against the desk's actual operations. Use the mechanism descriptions above as diagnostic criteria, not generic categories.

- Assign ownership to each break type: a named individual responsible for detection, escalation, and elimination of that break class across the book.

- Set elimination targets in measurable terms: reduction in frequency per month, reduction in average exposure per occurrence, or reduction in time-to-detection from market event to risk system visibility.

- Evaluate platform capability against elimination targets, not feature lists. The relevant question is whether that reconciliation module detects Cross-Venue Reference Price Divergence in real time, before the session closes on the exposure.

The Cost of Unnamed Breaks: A Practical Conclusion

Seven breaks. One sequence. Every physical metals trading desk is already experiencing some subset of them, most without a shared name for what they are observing and without a priority stack for what to eliminate first.

The break elimination framework does not require a system change to begin delivering value. It requires that a desk stop treating operational failures as undifferentiated events and start treating them as what they are: breaks with specific mechanisms, measurable exposures, and compounding costs that follow a predictable sequence from book-wide pricing divergence down to individual delivery instruction discrepancies.

Three immediate steps to apply this framework:

- Name the breaks your desk has experienced this quarter using the seven mechanism descriptions above. Identify which break types have recurred more than once. Recurrence is evidence of an unresolved mechanism rather than an anomaly.

- Sequence your active breaks by margin impact, not by the volume of desk-level discussion they generate. The loudest break and the most expensive break are rarely the same event.

- Evaluate your current platform's detection capability against the top two breaks in your sequenced list. Evaluate this precisely where your margin loss is greatest rather than across the full taxonomy at once.

Novaex physical metals trading platform overview LME base metals position management guide CTRM platform evaluation framework for base metals