Your Hedge Ratio Calculation Has a Timestamp Problem

A hedge ratio built on LME and COMEX prices captured at different times is not a complete hedge ratio. It is an approximation with an embedded timing error. This error is one that is fully calculable from the session structure of both exchanges.

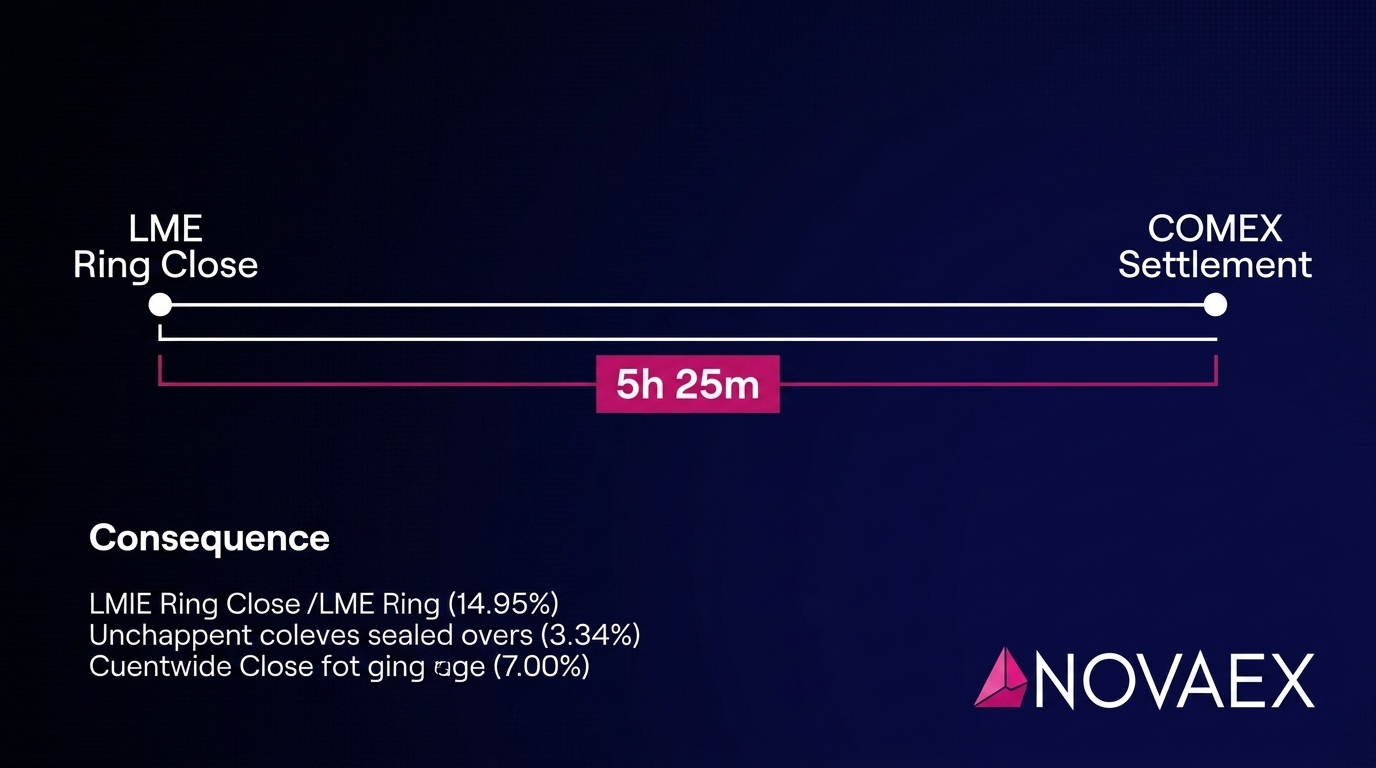

That error is mechanical, not probabilistic. The LME Ring close fixes official copper prices at approximately 12:35 PM London time (7:35 AM ET). COMEX copper settles at 1:00 PM ET. Any calculation assembled from those two sources without explicit timestamp alignment contains the price movement of a five-hour-and-twenty-five-minute window as an unvalidated input error.

What Makes a Hedge Ratio Calculation Wrong

A hedge ratio calculation fails in one of two ways: the formula is wrong, or the inputs are wrong.

Most practitioners focus on the formula. The correct ratio for cross-exchange copper hedging (using LME 3-month as the pricing benchmark against COMEX copper futures) requires the right lot size conversion, the right price ratio, and the right correlation coefficient if volatility-weighting is applied.

Those mechanics are well-documented. The input problem receives far less scrutiny, and it is where most errors live in practice.

The fundamental input requirement for a cross-exchange hedge ratio is price synchronicity: both LME and COMEX prices must reflect the same market moment. When they do not, the price ratio embedded in the formula is wrong, and the hedge ratio derived from it carries that error forward into every position sizing decision built on it.

According to CME Group published market structure data CME Group COMEX copper contract specifications, COMEX copper futures trade on CME Globex on a near-continuous schedule: Sunday through Friday, 6:00 PM ET to 5:00 PM ET the following day. The LME operates on a structurally different schedule with a different price formation mechanism. The gap between those two structures is the origin of the timing error.

Why is my hedge ratio inaccurate with LME and COMEX data?

The most common source of inaccuracy in an LME-COMEX hedge ratio is using prices from different points in the trading day as if they were contemporaneous. The LME Ring sets official copper prices in the London morning, hours before COMEX settlement in the New York afternoon. Any calculation built from an LME Ring price and a COMEX price pulled later contains the intervening price movement as unrecognized basis drift. This drift is directional, measurable, and present in every manually assembled calculation that does not account for the session offset.

The LME, COMEX Session Gap: Where the Timing Error Originates

The London Metal Exchange operates a structured Ring trading schedule unlike any other major futures exchange. Official prices are not derived from continuous electronic matching. They are set during specific intervals within two Ring sessions, conducted in a physical open-outcry format with defined close times.

For copper, the price-setting moment that matters is the second Ring close, at approximately 12:35 PM London time. This is when the LME official cash price, the official 3-month price, and the closing bid-ask structure are fixed. These are the prices that physical contracts reference, that swap settlements use, and that most hedge ratio benchmarks are built against.

At 12:35 PM London time during British Summer Time (BST), New York is operating on Eastern Daylight Time (EDT), five hours behind. The LME Ring close lands at 7:35 AM ET.

COMEX copper futures settle at 1:00 PM ET, the close of open-outcry floor trading COMEX copper settlement time CME Group. The arithmetic is fixed: there is a five-hour-and-twenty-five-minute gap between the moment LME official prices are set and the moment COMEX prices settle for the day.

During that window, COMEX copper trades actively through the full New York morning session. According to CME Group volatility data CME Group copper price volatility statistics, the average intraday range for COMEX copper on a normal trading day is 0.5% to 1.5%. At $9,000/MT copper, a 0.5% move equals $45/MT. A 1.0% move equals $90/MT. Both are fully achievable during a five-hour window, and both flow directly into the price ratio used to calculate your hedge ratio.

What is the timestamp delta between LME and COMEX data?

The timestamp delta is the elapsed time between LME Ring close (approximately 12:35 PM London / 7:35 AM ET) and the moment a COMEX price is captured for use in a hedge ratio calculation. For a trader running calculations at 10:00 AM ET, the delta is approximately two hours and twenty-five minutes. At COMEX settlement, the delta is five hours and twenty-five minutes. The error embedded in the resulting hedge ratio is a direct function of how much copper moved during that specific window on that specific day.

How the Timestamp Delta Corrupts Your Hedge Ratio Arithmetic

The error flows directly through the formula. The simplified cross-exchange hedge ratio for a physical copper position priced on LME 3-month against COMEX futures takes the form:

H = (P_LME / P_COMEX) × (Lot_LME / Lot_COMEX)

Where:

- P_LME = LME 3-month copper price (USD/MT)

- P_COMEX = COMEX copper futures price (USD/MT equivalent)

- Lot_LME = LME lot size (25 MT)

- Lot_COMEX = COMEX lot size (25,000 lbs ≈ 11.34 MT)

The lot size ratio is fixed at approximately 2.205. The price ratio is not. It changes with every tick on either exchange, and it changes asymmetrically during periods when LME official prices are fixed and COMEX continues to trade.

Applying the timestamp delta with concrete values:

- P_LME = $9,050/MT (captured at LME Ring close, 7:35 AM ET)

- P_COMEX at 7:35 AM ET = $9,050/MT (contemporaneous, at parity)

- Copper moves up $50/MT on COMEX during the New York morning session

- A trader assembles their hedge ratio calculation at 11:00 AM ET using the LME Ring price and the current COMEX price

- P_COMEX used = $9,100/MT

Stated hedge ratio: H = (9,050 / 9,100) × 2.205 = 0.9945 × 2.205 = 2.192

Correct hedge ratio (contemporaneous inputs at LME Ring close): H = (9,050 / 9,050) × 2.205 = 1.000 × 2.205 = 2.205

The ratio error: 2.205 − 2.192 = 0.013 contracts per unit of physical exposure.

On a 1,000 MT physical copper position, that error produces 13 contracts of unrecognized hedge exposure. The position will be either over-hedged or under-hedged, depending on the direction of the COMEX move during the gap.

How does asynchronous data affect hedge ratio calculations?

Asynchronous data creates a systematic directional bias in the price ratio at the core of the hedge ratio formula. When LME official prices are fixed and COMEX continues to trade, the cross-exchange price ratio drifts from the value it held when both markets were simultaneously active. A rising COMEX against a fixed LME input understates the hedge ratio; a falling COMEX overstates it. The error is not random noise. It has a defined direction each day, determined by the direction of COMEX price movement during the timestamp window.

Quantifying the Error: What Position Size Does to the Math

The hedge ratio error scales linearly with position size. This is not a rounding error that becomes negligible at scale. It compounds as volume increases. The 0.013 contract error per unit of exposure in the 1,000 MT example above comes from a $50/MT COMEX move, which is well within the normal intraday range.

The table below shows how that error scales across position sizes at the same 0.5% ($45/MT) COMEX move assumption on a $9,000/MT copper base:

| Physical Position | Price Ratio Error | Mis-hedged Contract Exposure | Approx. P&L at $50/MT Move |

|---|---|---|---|

| 250 MT | 0.003 | ~3 contracts | ~$21,000 |

| 1,000 MT | 0.013 | ~13 contracts | ~$83,000 |

| 5,000 MT | 0.065 | ~65 contracts | ~$415,000 |

At 65 COMEX contracts of unrecognized exposure (each contract representing 25,000 lbs of copper), a $50/MT move generates approximately $415,000 of unhedged P&L sitting inside a position the trader believes is correctly hedged.

That variance does not appear as a hedge ratio calculation error in most reporting workflows. It surfaces as unexplained basis variance after the fact, allocated to model error or market movement rather than traced to its actual origin: a timestamp gap that was never acknowledged in the calculation.

How do you calculate the error in a cross-exchange hedge ratio?

Calculating the timing error in your hedge ratio requires three values: the LME price at Ring close, the COMEX price used in your calculation, and the COMEX price at the moment of LME Ring close. The error equals the absolute difference between (P_LME / P_COMEX_used) and (P_LME / P_COMEX_at_LME_close), multiplied by the lot size ratio and your position size in lots. If you cannot retrieve a timestamped COMEX price contemporaneous with LME Ring close, the hedge ratio cannot be verified as accurate, and the error is not zero.

Why Manual Data Assembly Makes the Timing Problem Structural

The timestamp delta exists at the exchange level. It is a function of how LME and COMEX are built, not a data quality failure by any individual platform or feed. The error becomes structural to a trading workflow when data is assembled manually, because manual assembly introduces a second layer of timing variance on top of the exchange-level gap.

A trader who pulls LME data at 8:00 AM ET and COMEX data at 10:30 AM ET has not simply used prices from different market states. They have captured prices at different workflow moments, with the gap determined by operational routine rather than any deliberate analytical choice. The timestamp delta in that hedge ratio is not five hours and twenty-five minutes. It is the exchange gap plus two and a half hours of workflow variance.

According to a 2023 survey by the Commodity Technology Advisory Group CTAG commodity trading technology survey 2023, approximately 67% of mid-market commodity trading desks still use at least one manual step in their daily price capture and hedge calculation workflow. Each manual step adds unpredictable timestamp variance on top of the structural exchange gap.

The cumulative error structure is as follows:

- Exchange-level timestamp delta: Fixed at approximately five hours and twenty-five minutes from LME Ring close to COMEX settlement

- Workflow timestamp variance: Variable, determined by the sequence and timing of manual data pulls

- Combined error: Exchange delta plus workflow variance (in the same direction, or compounding, depending on the day)

The workflow variance is the controllable variable. The exchange structure is not. A workflow that does not account for the exchange structure guarantees that its manual variance is layered on top of an already-present timing error. This produces a hedge ratio error that cannot be bounded because neither its floor nor its ceiling is defined.

What causes embedded timing errors in metals hedging?

Embedded timing errors in base metals hedging have two simultaneous origins. The first is structural: LME and COMEX price formation occurs at different times of day, creating a minimum timestamp delta that no manual workflow can eliminate without timestamp-matched data pulls. The second is operational: manual data assembly adds unpredictable variance on top of the structural gap, converting a defined exchange-level error into an undefined compound error. The result is a hedge ratio calculation with an error floor set by the exchange gap and an error ceiling set by the accumulation of workflow delays. Neither element is visible in the output of the calculation itself.

What Synchronous Data Actually Requires for Hedge Ratio Accuracy

Eliminating the timing error does not require eliminating the exchange gap. The gap is structural and permanent. What it requires is accounting for the gap explicitly through one of two defensible approaches.

Approach 1: Timestamp-matched Ring close calculation

Use LME 3-month prices captured at the exact moment of Ring close (12:35 PM London, 7:35 AM ET) paired with a COMEX price pulled at that same calendar moment. This is the only approach that uses LME official prices in a genuinely contemporaneous hedge ratio. The resulting calculation reflects the price relationship that existed when both exchanges were simultaneously active and LME pricing was being set.

Approach 2: LME Select to COMEX settlement alignment

LME Select electronic trading runs until 7:00 PM London (2:00 PM ET) LME Select trading hours. COMEX settlement at 1:00 PM ET falls within the LME Select window. A hedge ratio built on a COMEX settlement price paired with a live LME Select price at 1:00 PM ET reduces the timestamp delta to near-zero. This approach is valid, but it requires a data feed that timestamps LME Select prices precisely. It requires a system that does not simply serve the prior Ring close as the default "LME price" when the Ring session is no longer active.

Neither approach is achievable through a workflow that pulls prices from separate sources at uncoordinated intervals. Both require a system that serves LME and COMEX prices from a unified, timestamped data layer where pulls are either simultaneous or explicitly offset-corrected against the exchange session structure.

According to financial market data infrastructure research published by the BIS Markets Committee BIS market data infrastructure report, price data served from separate non-unified feeds creates average asynchronous deltas of three to eight minutes even in automated systems. Automated workflows are not immune to timestamp error when they pull from architecturally separate data sources without explicit synchronization logic.

The Standard Your Hedge Ratio Calculation Must Meet

A hedge ratio calculation built on LME and COMEX inputs must be able to answer one verifiable question on demand: at what time was each price captured, and do those timestamps reflect the same market moment?

If that question cannot be answered; if the calculation cannot produce a timestamp for each input; the hedge ratio it generates cannot be validated as accurate. It is an approximation with an error that is a function of price movement during the timestamp gap and the size of the position it is applied to.

Copper markets are continuous, meaning some approximation exists in any practical workflow. The necessary standard is verifiability: a hedge ratio calculation is only as defensible as the audit trail on its inputs.

For base metals hedging specifically, that audit trail requirement is more demanding than in single-exchange workflows. LME and COMEX operate in different time zones, with different price formation mechanics, different session structures, and different feed behaviors when markets are not in active session. A platform built to handle that complexity must treat timestamp alignment as a first-class data architecture problem, not a background assumption absorbed into a "close enough" workflow.

That is the fundamental standard for hedge ratio accuracy: not asserting that the calculation is always right, but building the infrastructure that makes it verifiable every time it runs.

The LME Ring closes at 12:35 PM London (7:35 AM ET). COMEX settles at 1:00 PM ET. Any hedge ratio assembled from those two sources without explicit timestamp alignment carries the price movement of a five-hour-and-twenty-five-minute window as an unvalidated input error. The magnitude of that error is the product of the COMEX move during the gap and your position size. The direction of that error follows the direction of COMEX movement during the window.

The next step is to apply this framework to your own calculation.

Three immediate actions:

- Pull the timestamps on your last three hedge ratio input records. Confirm whether LME and COMEX prices were captured contemporaneously or at different workflow moments, and calculate the COMEX price movement during each gap.

- Apply the formula in this analysis to your actual position size and yesterday's timestamp delta to determine the magnitude of the ratio error in your most recent calculation.

- Evaluate whether your current data infrastructure can serve timestamp-aligned LME and COMEX prices in a unified pull, or whether eliminating workflow-level variance requires an architecture change.

If you want to understand what timestamp-aligned, audit-ready base metals data infrastructure looks like operationally, Novaex platform overview Novaex was built specifically to solve this problem at the data layer, before it reaches the hedge ratio formula. Novaex contact or demo request Start with the architecture.