Metals Trading Position Visibility: Raw Tick to Ready Signal

Metals trading position visibility is the process of converting raw price ticks from LME, MCX, COMEX, and SHFE into a unified, decision-ready view of your exposure, without manual synthesis. Novaex accomplishes this through a four-stage translation layer: raw tick ingestion, normalized cross-exchange feed, structured market context assembly, and execution-ready signal delivery. Each stage eliminates a specific layer of interpretive labor that currently falls on the trader.

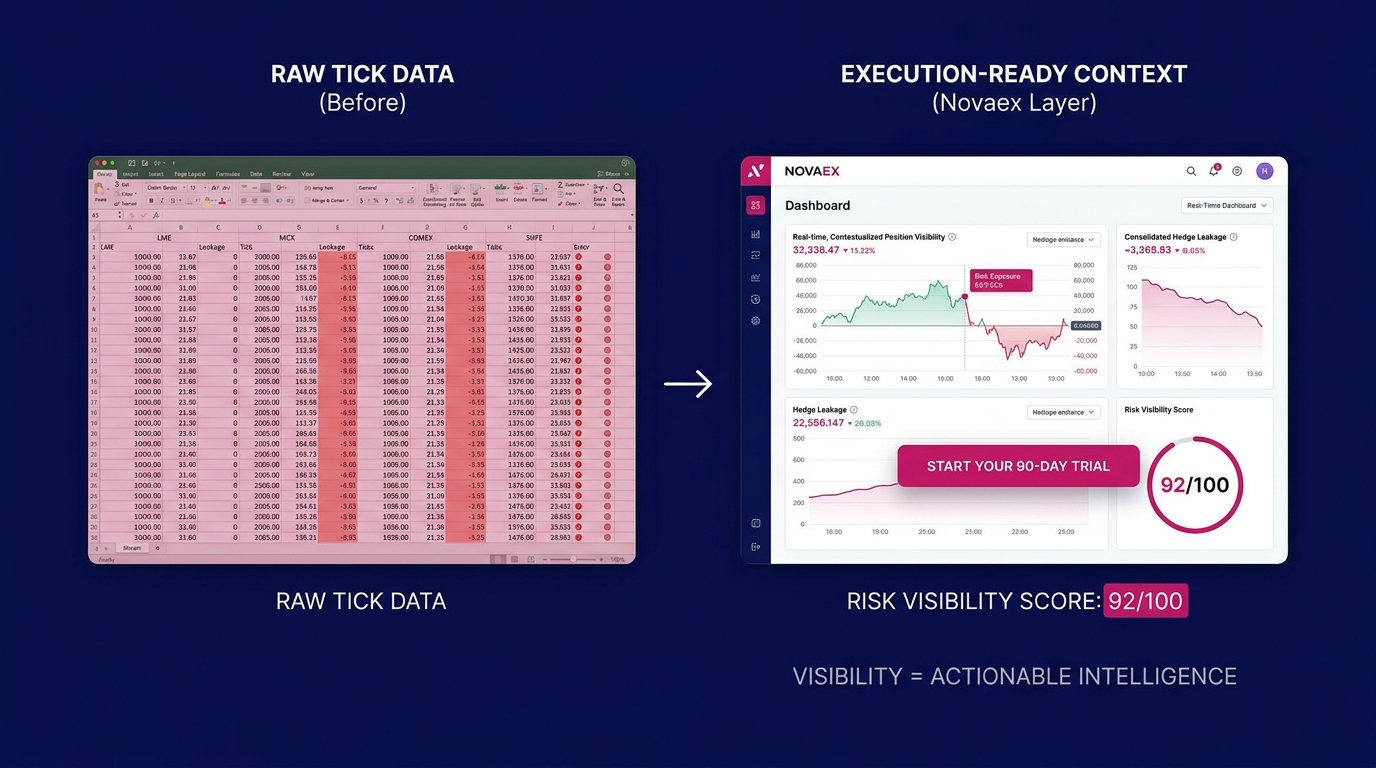

Most platforms terminate the process at stage one, delivering data but failing to provide decision context.

That distinction defines the operational problem this analysis addresses. A front-office metals trader working copper, aluminum, or zinc across multiple exchanges rarely lacks data. They lack context. The LME three-month copper settlement, the COMEX front-month futures price, the MCX aluminum near-contract, and the SHFE copper continuous contract are all broadcasting simultaneously. The relevant question is whether the system has already done the work of making those numbers mean something before a decision is required.

According to LME annual report the London Metal Exchange, LME base metals trading volumes exceeded $15.7 trillion in notional value in 2023, distributed across more than 180 countries. That volume carries tick-level granularity across six primary base metals. Parsing that stream manually, even with a Bloomberg terminal open, is not a viable workflow. It is a quantifiable source of decision latency and execution risk.

Why Raw Tick Data Is Not a Trading Signal

The foundational gap in most commodity data platforms is the conflation of data delivery with decision synthesis: displaying data is fundamentally different from synthesizing decision context.

A tick is a timestamped price event. The LME publishes three-month copper bids and offers in real time. COMEX publishes HG futures ticks across a rolling contract structure. MCX publishes near-month aluminum and copper contracts denominated in INR. SHFE publishes its own copper continuous contract in RMB, with its own warehousing and delivery specifications.

Each of those tick streams is accurate. None of them, in isolation, describes a position.

The Difference Between Raw Tick Data and Execution-Ready Context

Raw tick data is a price event: copper traded at $9,240/mt on the LME at 10:14:32 UTC. Execution-ready context answers whether that price event changes your hedge ratio, triggers a delta threshold, or creates a roll decision relative to your physical book without requiring manual calculation. The gap between those two states is where traders lose time and where adverse price movement accumulates.

According to a 2022 Accenture capital markets study Accenture Capital Markets study, traders at mid-market firms spend an average of 23% of their decision-making window performing manual data normalization before they can assess a position. Automating that translation layer recaptures 23% of available decision time. This time currently absorbs market movement rather than responding to it.

Where Manual Data Synthesis Fails

Manual synthesis fails because the four major base metals exchanges do not share a common data grammar. LME quotes in USD per metric ton with a specific prompt-date structure. COMEX quotes in USD per pound in contract lots of 25,000 lbs. MCX quotes in INR per kilogram. SHFE quotes in RMB per metric ton.

Before a trader can compare an LME copper position to a SHFE hedge, they must perform unit conversion, currency adjustment, and prompt-date alignment simultaneously. Under market stress, that process introduces measurable latency and compounding error risk. According to FIA market data report the Futures Industry Association, execution errors attributable to manual data handling cost commodity trading firms an estimated $1.2 billion annually across global markets.

Stage One: Raw Tick Ingestion Across LME, MCX, COMEX, and SHFE

The first stage of the metals trading position visibility layer is the raw tick ingestion pipeline. This is not a feed aggregator. It is a structured intake protocol that captures exchange-native data without premature normalization.

Each exchange produces ticks in its own format and latency profile. LME inter-office market data arrives through the LMEselect and LMEbullion reporting infrastructure. COMEX delivers tick data via CME Group's Globex platform in FIX protocol format. MCX publishes market depth and trade data through its own API layer with India-specific session windows. SHFE operates on China Standard Time with a morning session (9:00-11:30 CST) and afternoon session (13:30-15:00 CST), creating a gap structure that requires explicit handling.

Normalizing Cross-Exchange Data While Preserving Precision

Normalization without precision loss requires capturing exchange-native identifiers before translation. Novaex retains the original exchange contract code, session timestamp, lot size, and currency denomination at intake. It then appends normalization metadata rather than replacing source data. A COMEX HG tick is stored as HG, in USD/lb, in 25,000 lb lots, with its CME Globex timestamp intact; the normalization layer sits on top of the source record rather than inside it.

This architecture preserves auditability and allows position reconciliation against exchange-reported data without translation artifacts. According to CME Group market statistics CME Group, COMEX copper open interest regularly exceeds 200,000 contracts, representing approximately 5 million metric tons of notional copper exposure. Capturing that with full precision at the tick level before any normalization is the technical precondition for everything that follows.

Stage Two: Building the Normalized Cross-Exchange Metals Feed

Stage two converts the four exchange-native tick streams into a single normalized feed denominated in a common unit, currency, and time reference. This is where the translation work becomes operationally consequential.

Novaex's normalization engine performs four simultaneous operations:

- Unit harmonization: All prices convert to USD per metric ton (USD/mt), the standard reference unit for base metals hedging. COMEX HG ticks (USD/lb) multiply by 2,204.62. MCX ticks (INR/kg) convert using a live FX rate and multiply by 1,000. SHFE ticks (RMB/mt) convert using the PBOC daily midrate.

- Prompt-date alignment: LME's prompt-date structure differs fundamentally from COMEX's rolling monthly contracts. The normalization layer maps each contract to its equivalent prompt date, enabling like-for-like spread analysis across exchanges.

- Session gap bridging: SHFE's trading hours create natural gaps in the normalized feed. Novaex flags these gaps explicitly rather than interpolating. This is a critical distinction for traders who need to distinguish between a live price and a carried-forward price.

- Latency tagging: Each normalized tick retains its exchange-specific latency metadata, allowing assessment of data freshness at a glance without leaving the normalized view.

According to Reuters metals market analysis Reuters market analysis, the LME-SHFE copper spread is one of the most actively arbitraged relationships in base metals, with institutional traders targeting spreads as narrow as $40-$60/mt. Detecting those spreads in real time across exchange-native data formats requires a normalized feed as the operational foundation.

Stage Three: Structured Market Context Assembly

Stage three is where metals trading position visibility becomes technically distinctive. Platforms that terminate at stage two deliver a normalized feed and characterize that as market intelligence. Structured market context assembly is a categorically different operation.

In stage three, Novaex overlays three additional data dimensions onto the normalized price feed:

1. Open Interest and Volume Context

A price movement without volume context is analytically incomplete. LME aluminum ticking down $35/mt on low open interest carries different implications than the same move on a 15% open interest increase. The context layer annotates each price movement with the OI and volume data required to assess whether it reflects conviction or noise.

2. Warehouse Stock Positioning

LME warrant data, SHFE warehouse stock reports, and COMEX certified stocks are ingested and mapped to the normalized price feed. According to LME warehouse statistics the LME, aluminum warehouse stocks have historically moved LME cash prices by $8-$12/mt per 50,000 metric ton inventory change. That relationship is embedded in the context layer as a quantified signal, not a qualitative note in a separate report.

3. Physical Delivery Alignment

For traders managing physical positions alongside financial hedges, the context layer tracks exchange delivery specifications (LME approved brands and delivery locations, COMEX eligible vault inventory, SHFE standard and nonstandard warrant ratios) and flags when the financial position diverges from deliverable physical specifications.

Position Visibility vs. Traditional Dashboards

Position visibility synthesizes specific exposure against live market context. It does not display prices and require the trader to perform the synthesis. A dashboard shows copper at $9,240/mt. Position visibility shows that a 500 mt long LME position is +$18,500 against entry, that COMEX is trading at a $42/mt premium indicating potential arbitrage risk, and that LME cash-to-three-month contango has widened 12% in the past session, all without a single manual calculation. The dashboard presents inputs. Position visibility delivers outputs.

Stage Four: The Execution-Ready Signal

Stage four is the translation layer's final output: the execution-ready signal. This is the point where structured market context becomes clear, executable instruction.

An execution-ready signal answers three operational questions with precision:

- Current delta: Net exposure in USD/mt equivalent across all four exchanges, adjusted for prompt-date weighting and lot-size normalization.

- Threshold triggers: Whether a price move, spread change, OI shift, or warehouse stock event has triggered a pre-defined threshold in the trader's position management parameters.

- Execution path: Which exchange, contract, and prompt date offers the most efficient hedge leg, given current spread relationships and liquidity depth across LME, MCX, COMEX, and SHFE.

The Importance of Execution Speed in Metals

Metals markets combine high notional value with genuinely global, near-continuous price formation across four major exchanges. A 20-minute delay in executing a copper hedge on a 500 mt position can represent $15,000-$30,000 in adverse price movement at historical one-day volatility levels. This figure is highly calculable. According to [LINK: World Bureau of Metal Statistics] the World Bureau of Metal Statistics, global refined copper consumption in 2023 was approximately 26 million metric tons, with the majority of physical pricing referenced to LME cash or COMEX spot, meaning latency costs accrue against an enormous underlying market.

According to TABB Group trading research the TABB Group, front-office traders at commodity firms who operate with pre-defined execution frameworks reduce average hedge initiation time by 34% compared to those using discretionary, manually assembled workflows. Execution-ready signals operationalize that framework at the signal level, not just the policy level.

What Metals Trading Position Visibility Changes About Your Workflow

The practical impact of a four-stage translation layer becomes highly visible during volatility events like copper short squeezes, aluminum supply disruptions, and zinc inventory builds.

In those conditions, the manual synthesis workflow (opening four platforms, converting units, aligning prompt dates, checking OI, comparing spreads, and calculating delta) requires 8 to 15 minutes under pressure. The four-stage translation layer completes the same synthesis continuously in the background, so the trader arrives at the signal rather than the data.

A concrete scenario illustrates the operational difference: LME three-month aluminum drops $28/mt in 18 minutes on a Wednesday morning. SHFE aluminum is in its session gap. MCX has not yet responded. COMEX aluminum futures are thin. A trader working raw data from four feeds faces a synthesis problem with a compressing decision window. A trader operating with a position visibility layer has an exposure statement: current delta, last confirmed SHFE close, spread-implied carry, and the closest liquid hedge leg without a manual calculation in the chain.

According to [LINK: McKinsey commodity analytics] McKinsey's commodity analytics research, firms that have implemented automated position synthesis tools report a 40% reduction in decision latency during market stress events and a measurable improvement in hedge ratio accuracy over rolling 90-day periods. This operational shift eliminates the interpretive bottleneck that sits between market event and trading decision.

The Standard for Metals Trading Position Visibility

Metals trading position visibility is a specific technical achievement: the conversion of raw tick data from LME, MCX, COMEX, and SHFE into execution-ready context through a four-stage translation layer that handles unit normalization, prompt-date alignment, session gap management, and structured market context assembly before the trader sees the output.

The true quality of that layer emerges when LME copper moves $150/mt in a single session, when SHFE imposes overnight margin increases, or when COMEX certified stocks drop below a six-week low. Novaex was built with those conditions as the design requirement.

The depth-first methodology (mastering each base metal before expanding to additional commodities) means every normalization rule, every OI threshold, and every warehouse stock correlation embedded in stages two and three was derived from the specific behavioral characteristics of that metal on that exchange. LME aluminum carries a different volatility structure, different backwardation patterns, and different warehouse stock sensitivities than LME copper. Treating them identically at the normalization layer produces context errors precisely when context matters most. Novaex applies distinct rules for each.

Three immediate steps to evaluate your current workflow:

- Time how long it takes to produce a cross-exchange delta statement during an active market session, including unit conversion, prompt-date alignment, and OI context. That figure is your current synthesis latency, and it is the baseline against which the four-stage translation layer should be measured.

- Identify the last three instances where market movement preceded hedge execution by more than 10 minutes. Calculate the cost of that latency at the actual price change per metric ton and your position size. The figure will establish whether the problem is operational or acceptable.

- Novaex platform demonstration Request a Novaex workflow demonstration focused specifically on the stage three to stage four transition (structured context to execution-ready signal) to observe the translation mechanism operating against live LME, MCX, COMEX, and SHFE data.