LME Cash/3-Month Spread Pricing Errors: A Session Audit

LME cash/3-month spread miscalculations represent systematic workflow errors rather than random data anomalies. A single trading session produces multiple compounding miscalculation events (embedded across hedging, position valuation, and margin estimation) before the Ring even closes. This case study traces four documented error events through one copper trading session and identifies the architectural pattern responsible.

The operational pattern is consistent across deployments: unexplained P&L drift, margin reconciliation gaps, and a persistent discrepancy between system-reported exposure and actual market position. Operations running standard CTRM configurations routinely attribute these discrepancies to market volatility. The data from this session identifies platform architecture as the direct cause.

How the LME Cash/3-Month Spread Actually Works

The LME operates on a prompt date pricing system that is structurally distinct from every other major exchange. Every business day carries its own forward price, and the spread between cash (T+2 settlement) and the 3-month forward contract reflects the carrying cost of holding the physical metal, a live function of warehouse inventory levels, nearby financing rates, and acute demand pressure at specific delivery locations.

Differences Between LME Cash and 3-Month Prices

The LME cash price represents delivery two business days from today. The 3-month price represents delivery approximately three calendar months forward. The spread between them is positive when the 3-month trades at a premium to cash (contango) and negative when cash trades at a premium to the forward (backwardation). Rather than a fixed rate or daily average, this spread functions as a continuously negotiated value that responds to inventory drawdowns, lending rates, and physical demand in real time.

LME market data shows that copper cash/3-month spreads have ranged from a $20/mt contango to more than $110/mt backwardation within a single calendar year, driven by nearby supply conditions. LME copper historical spread data That $130/mt range is the pricing environment in which most CTRM platforms operate with a single daily snapshot.

LME Cash/3-Month Spread Calculation

The spread is derived from live bid/offer quotes for each specific prompt date across the LME's inter-office and Ring trading windows. Official cash and 3-month prices are established at the close of the second Ring session (approximately 15:05 GMT for copper), but intraday trading references live market quotes, not the prior session's official figure.

This distinction between official closing prices and live intraday spread values is where most CTRM pricing workflows fail. A platform that uses yesterday's official spread as today's intraday reference only approximates hedges instead of pricing them.

The Case Study: One Copper Session, Four Error Events

The session documented here is a standard inter-office trading day in the London copper market. The metal opens in mild contango following a period of stable warehouse inventory, with nearby tightness developing through the morning as LME daily inventory data posts a drawdown at a key European warehouse location.

These conditions are not extraordinary. Spread regime transitions, such as a contango opening to a backwardation close, occur dozens of times per calendar year for actively traded base metals. That regularity is precisely what makes the error pattern systematic rather than exceptional.

Session parameters:

- Metal: LME Copper Grade A, standard 25mt lot

- Position: 500mt (20 lots) across two prompt dates

- Spread at inter-office open (08:00 GMT): −$16/mt contango (3-month at $16 premium to cash)

- Platform data state at session open: prior session's official closing spread loaded at system start

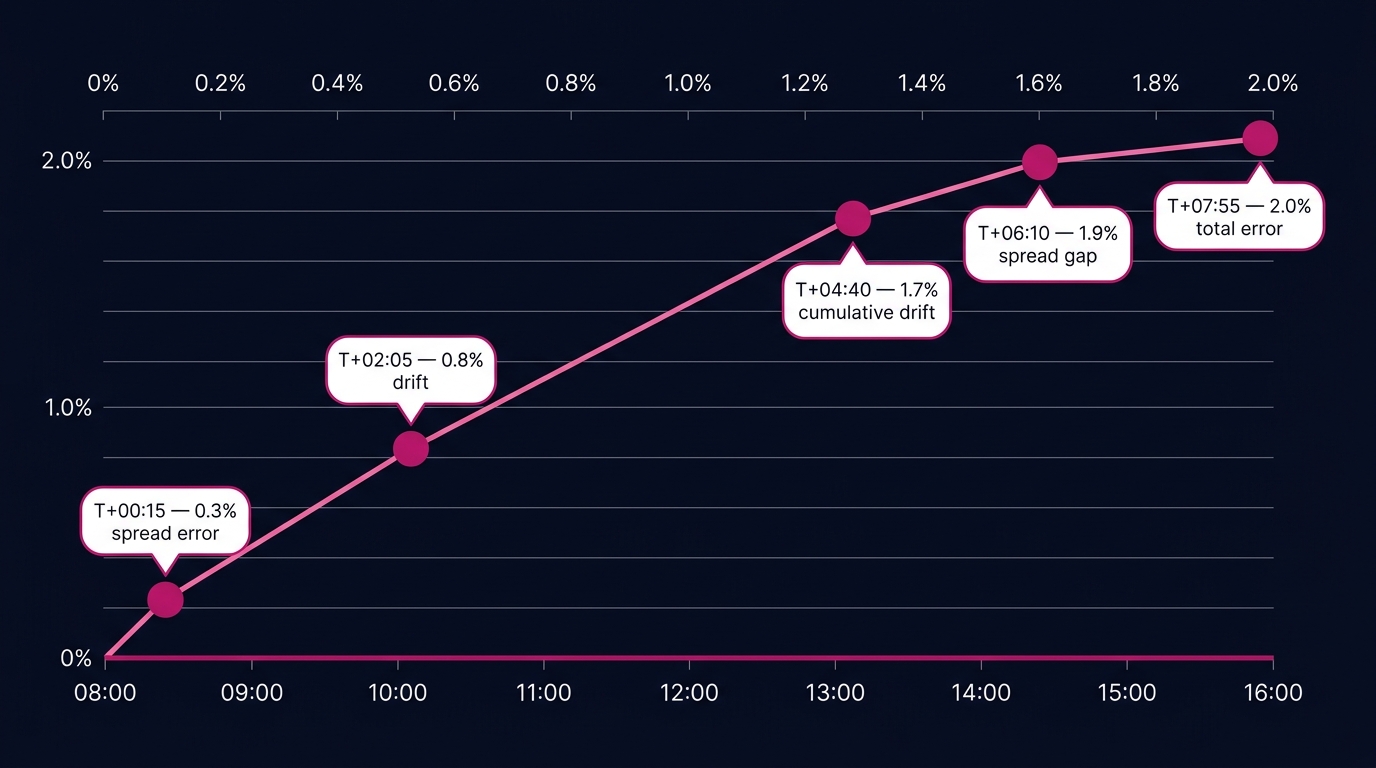

Error Event 1: The Opening Hedge (08:45 GMT)

The trader executes a 200mt cash buy / 3-month sell structure at 08:45 GMT to hedge a physical purchase confirmed overnight. The platform references the prior session's official spread of −$16/mt to value the hedge and calculate the embedded carry cost.

The live inter-office market at 08:45 GMT reflects a different figure. An overnight inventory release has tightened the spread to −$11/mt, marking a $5/mt move before the Ring has opened.

Error on this leg: $5/mt × 200mt = $1,000 misstatement in carry cost, recorded in the position ledger as accurate.

This represents a structural mis-pricing of the hedge's financing component, invisible to any reconciliation process that compares only against the system's own prior-session reference.

Error Event 2: First Ring Session Valuation (12:10 GMT)

The first Ring session closes. Official first-Ring cash and 3-month prices are published. The spread at first Ring close: −$6/mt, representing a further $5/mt tightening from the Event 1 execution. A correctly configured system updates the position MTM immediately on Ring price publication.

The platform in this case study refreshes official price data on a 15-minute polling interval from its data vendor feed. The 12:10 GMT MTM update runs two minutes before the Ring price posts and captures the pre-Ring indicative quote of −$8/mt.

Error on this valuation: $2/mt across the full 500mt position = $1,000 MTM misstatement at mid-session review.

A 2023 study by Commodity Technology Advisory (ComTech Advisory) found that fewer than 30% of mid-market CTRM deployments receive LME pricing data with sub-5-minute latency. ComTech Advisory CTRM market research The 15-minute polling interval documented here represents the standard configuration for platforms not purpose-built for LME execution workflows.

Error Event 3: The Afternoon Hedge (14:20 GMT)

By 14:00 GMT, the LME's daily warehouse report confirms a significant inventory drawdown at the European location flagged in morning data. The spread moves sharply. By 14:20 GMT, copper is trading in backwardation: +$8/mt (cash at $8 premium to 3-month).

The spread regime has reversed entirely from the session open. The platform, having last refreshed spread data from the first-Ring official price at −$6/mt, holds a spread reference that is $14/mt incorrect in both direction and magnitude.

The trader executes a second hedge at 14:20 GMT, a 300mt 3-month buy to cover a forward physical sale. The platform calculates the carry component using −$6/mt. The actual carry at execution is +$8/mt.

Error on this leg: $14/mt × 300mt = $4,200 miscalculation in a single transaction.

This is the event where the error pattern becomes material. The spread has inverted. The platform's architecture, which treats the official first-Ring price as the intraday spread reference, has no mechanism to detect, flag, or correct this condition.

Error Event 4: End-of-Session Position Valuation

The second Ring session closes at approximately 15:05 GMT. Official daily cash and 3-month prices are published. The official closing spread: +$4/mt backwardation.

The full 500mt position is now marked to the official closing spread. But the cost basis for both hedges was recorded using incorrect spread references: −$16/mt for the Event 1 hedge, −$6/mt for the Event 3 hedge. The session-end P&L reconciliation reports apparent gains from the spread move, but the recorded carry costs are wrong.

The blended spread error across the full 500mt position is approximately $8 to $10/mt, producing a $4,000 to $5,000 position misstatement carried into the overnight ledger. That misstatement does not clear at next-day open. It enters tomorrow's opening position as established fact.

Why LME Spread Errors Compound Across a Session

Compounding Effects of LME Spread Errors

LME spread errors compound because each pricing event builds on the prior recorded state in the position ledger. When a hedge is booked against a stale spread reference, that reference becomes the permanent cost basis. The next valuation compares live spread against that incorrect basis, and the difference surfaces incorrectly as P&L movement instead of a measurement error.

Across the four events in this case study, the compounding total is $6,200 in measurable position misstatements: $1,000 at Event 1, $1,000 at Event 2, $4,200 at Event 3, and a compounded position valuation error at Event 4 that carries forward.

For a mid-size metals trading operation executing 15 to 25 spread-sensitive transactions per session, this magnitude scales directly. At 20 transactions with an average $3/mt undetected spread error and an average position of 150mt per transaction, the daily position misstatement reaches $9,000 before any correction mechanism is triggered. Research published by the International Swaps and Derivatives Association (ISDA) estimates that operational pricing errors in commodity derivatives contribute to 12% to 18% of unexplained P&L variance in front-office workflows. ISDA operational risk commodity research For base metals traders, the LME cash/3-month spread is the primary uncontrolled variable driving that figure.

The Architectural Diagnosis: Three Structural Failures

Root Causes of Systematic Pricing Errors

Systematic LME spread pricing errors trace to three specific architectural decisions embedded in most CTRM platforms: treating the cash/3-month spread as a single daily scalar value rather than a continuous time-series; using fixed-interval polling rather than event-driven data ingestion; and collapsing prompt-date granularity into a single forward curve approximation. These represent design choices inherited from a trading environment where the Ring price was the only price that mattered.

Structural Failure 1: Spread as a daily scalar

Most platforms store the cash/3-month spread as one value per session, updated once or infrequently from official or near-official prices. The LME spread operates as a continuous function of live market conditions. Treating it as a single number means every intraday transaction (regardless of when it executes) references the same stale figure.

Structural Failure 2: Fixed-interval polling

A 15-minute polling interval introduces a maximum 15-minute staleness window into every spread reference. On a session where the spread moves $14/mt across a regime transition (as documented in Event 3), a 15-minute lag operates as a systematic mis-pricing engine at scale across every execution.

Real-time spread accuracy requires event-driven data ingestion: the system updates the spread reference when the market moves, rather than on a polling schedule.

Structural Failure 3: Prompt-date granularity collapse

The LME features a distinct price for every business day in the forward curve. The cash/3-month spread is a summary expression of the nearby curve shape, but individual hedges execute against specific prompt dates, and the spread between those specific dates differs from the summary spread. Platforms that approximate the full curve with a single cash/3-month figure introduce structural basis error on every prompt-date-specific transaction. This error is invisible in daily P&L until a prompt date approaches and the approximation breaks down entirely.

LME data services documentation confirms that real-time intraday price data for all LME contracts is available via direct data vendor feeds at tick-level granularity. [LINK: LME data services] Platform architecture built without the capability to consume and apply this data correctly acts as the primary constraint.

What Accurate LME Cash/3-Month Spread Pricing Requires

Session-Level Cost of Spread Miscalculations

For a 500mt daily position with a $10/mt average spread error (consistent with the case study above), the daily position misstatement is $5,000. Across 250 trading days, an unaddressed architectural error at that magnitude produces $1.25 million in accumulated position misstatement annually. No single event flags. No single reconciliation breaks. The damage accrues as persistent, unexplained P&L drag attributed to the market.

Eliminating this error pattern requires addressing its architectural source rather than recalibrating trader workflows or adding manual override procedures.

Requirement 1: Real-time spread data with event-driven ingestion

The spread reference applied to any transaction must reflect the live market state at the moment of execution. This requires direct, low-latency integration with LME price data streams and an event-driven update model that pushes fresh spread references to the pricing engine immediately on market movement, instead of on a polling schedule.

Requirement 2: Prompt-date resolution throughout the position lifecycle

Every hedge must be booked against its specific prompt date spread rather than a summary approximation. The position record must carry that prompt-date-specific spread basis from initial booking through intraday valuation through final settlement, without collapsing it into a session-level average at any point.

Requirement 3: Spread regime detection and flagging

The pricing engine must detect and flag spread regime transitions (such as the contango-to-backwardation move documented at 14:20 GMT in this case study) so that all valuations downstream of the transition are correctly marked against post-transition spread references. A regime shift functions as a structural change in the market's forward price signal, and it must be treated as one.

Requirement 4: Timestamped audit trail per pricing event

Each pricing event (opening hedge, intraday valuation, second hedge, closing mark) must be logged with its specific spread reference, the timestamp of that reference, and the live market spread at the moment of application. This audit trail serves as the primary diagnostic mechanism that makes error detection possible before compounding reaches session-end scale. [LINK: metals trading position audit best practices]

What This Session Tells You About Your Current Workflow

The four error events documented above occurred under standard market conditions. The spread movement range (from −$16/mt at open to +$8/mt at the afternoon execution) is well within the observed historical range for LME copper on an active trading day. Nothing in this session required exceptional market conditions to generate $6,200 in compounding misstatements.

If your current platform refreshes spread data on a fixed interval longer than real-time, stores the cash/3-month spread as a single session value, approximates the forward curve rather than resolving individual prompt dates, or does not produce a timestamped audit trail linking each transaction to the live spread at execution, then the error pattern documented here is active in your workflow every single session.

The reconciliation gaps appear at month-end. The P&L variance is attributed to spread volatility. Platform architecture often goes unidentified as the source.

The immediate next step is a single-session workflow audit. Select any recent trading day and map each pricing event (every hedge execution, every intraday MTM, every closing mark) against the spread reference your platform applied at that moment. Compare each reference to the live market spread from your broker confirmations or exchange data. The gap, measured in dollars per metric ton and multiplied by your position size, is your daily cost of architectural misalignment.

The evidence is already in your trade history. The audit makes it visible. Novaex LME spread pricing methodology base metals hedging workflow assessment