COMEX vs. LME Copper: Curve Architecture and Basis Risk

Summary: COMEX copper futures and LME copper forward contracts are built on structurally different curve architectures. COMEX settles monthly; the LME prices every business day as a distinct daily prompt date. Translating a copper position between the two exchanges without depth-accurate spread data creates basis risk that cannot be measured. Unquantified risk operates outside any governance framework.

Most market participants treat COMEX and LME copper as two prices for the same metal. That operational equivalence is structurally inaccurate.

The two exchanges do not share the same time structure, denomination, delivery framework, or forward curve construction methodology. The COMEX copper LME copper basis risk generated when translating a position between them is real, specific, and entirely quantifiable, but only with the right data. Without it, the exposure is absent from your risk system while remaining present in your P&L.

This analysis documents the structural differences between the two curve architectures and identifies the precise inputs that produce unquantified basis risk at the translation point.

Two Exchanges, Two Structurally Different Instruments

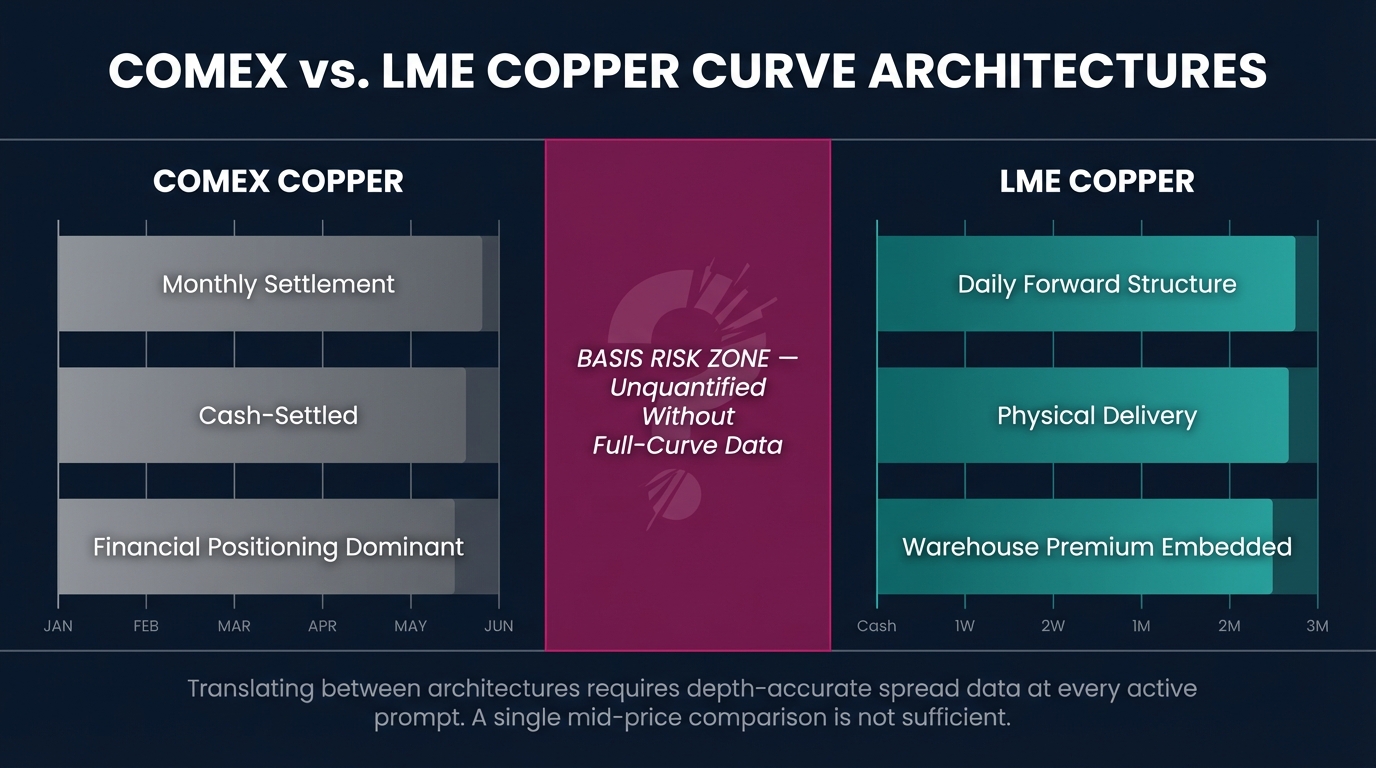

COMEX copper futures COMEX copper futures contract specifications are standardized monthly contracts traded on CME Group, denominated in U.S. cents per pound, with a contract unit of 25,000 pounds (approximately 11.34 metric tonnes). Each contract settles at a fixed monthly expiry date. The curve is a monthly strip.

LME copper forward contracts LME copper forward contract specifications are built on an entirely different framework. The LME generates a daily prompt date for every London business day from cash (T+2) through three months forward, then weekly dates out to six months, then monthly dates extending up to 123 months. Any single business day within the first three months is an independently settleable delivery date, not just end-of-month.

This is not an operational difference in the same category as margin conventions or lot sizes. It is a foundational divergence in how the forward curve is populated. That divergence has direct, measurable consequences for every trader holding positions on both exchanges simultaneously.

What Is the Difference Between COMEX Copper Futures and LME Copper Forward Contracts?

COMEX copper futures are exchange-traded standardized contracts settling at monthly expiry dates, while LME copper forward contracts price every business day as a unique, independently settleable prompt date. The two instruments represent different time-bucketing frameworks, not different prices for the same underlying at the same delivery point. Mapping them as structurally equivalent in a position management system introduces misrepresentation before any market movement occurs.

According to CME Group, COMEX copper regularly carries open interest exceeding 130,000 contracts, representing over 1.47 million tonnes of notional copper exposure CME Group open interest data. At that scale, the quality of cross-exchange mapping is a portfolio-level risk issue, not a back-office detail.

The LME Copper Forward Curve Is Not a Monthly Structure

Understanding basis risk requires knowing how daily prompt dates affect curve construction.

On any given trading day, the LME publishes official prices for cash copper, the three-month forward, and every intervening business day as a carry-implied prompt. The curve between cash and three months is not interpolated by convention; it is directly tradeable through tom-next and date-dated forward transactions in the LME lending market LME lending market mechanics.

According to the LME, the exchange provides official settlement prices for over 60 individual prompt dates within the cash-to-three-month window alone on any given trading session. Each price point is independently settleable and independently priced.

This matters for hedgers because a physical delivery obligation falling on a Wednesday three weeks forward is not the same price as a Thursday delivery three weeks forward. The spread between those two adjacent dates is determined by daily borrow and lending rates and the live supply and demand in the LME lending market, not by convention or approximation.

How Do Daily Prompt Dates Affect LME Copper Curve Construction?

Daily prompt dates make the LME copper forward curve a continuous structure where every business day within the near-dated window is an independently priced tenor. This means the LME curve has substantially more price nodes than a monthly-expiry curve like COMEX. Each node carries its own spread relationship to adjacent dates. A position mapped to the nearest monthly bucket loses the granularity of the actual daily carry structure and substitutes a real spread with an assumption.

How COMEX Copper Futures Build Their Curve

The COMEX copper curve is a monthly expiry strip. Contracts are listed for each calendar month, with price discovery concentrated heavily in the front months and liquidity thinning materially beyond the first three active contracts.

According to CME Group's published volume analytics, approximately 70% of COMEX copper futures volume concentrates in the first three listed months CME Group copper volume distribution. The spread between the front month and the second month is a single observable price. There is no mechanism within the COMEX structure to price a position settling on the 14th of a month differently from one settling on the 22nd. Those dates collapse to the same monthly contract.

Contango and backwardation on COMEX are expressed in monthly increments. The term structure is visible at a monthly level. What is structurally absent is intra-month cost of carry with the granularity that a physical trader or cross-exchange hedger requires when one leg of their position is priced off a specific LME prompt date.

What Inputs Drive the Difference Between LME and COMEX Copper Curves?

The LME-COMEX curve divergence is driven by four primary structural inputs: (1) prompt date granularity (daily versus monthly), (2) contract denomination (LME prices in USD per metric tonne while COMEX prices in U.S. cents per pound), (3) delivery geography (LME warrants cover a global approved warehouse network while COMEX delivery is U.S.-located), and (4) the LME lending market, which directly prices daily carry spreads with no structural COMEX equivalent. Each input contributes independently to the divergence between the two curves at the position translation point.

The Translation Point: Where COMEX Copper Basis Risk Enters

A trader holding a long COMEX copper futures position and a short LME copper forward position is not, by default, flat. They are holding two positions on structurally different curve architectures, connected only by the assumption that the spread between them is known, stable, and correctly modeled in their risk system.

That assumption is where the COMEX copper LME copper basis risk resides.

The COMEX-LME basis (commonly observed as the arbitrage spread between the COMEX front month and the LME three-month forward) is observable at a point in time. But point-in-time observation is not equivalent to depth-accurate curve modeling. A risk system that captures today's COMEX-LME spread but cannot model how that spread behaves across the full prompt date structure of the LME forward curve is operating with a partial picture of the position it is designed to govern.

According to research published by the International Copper Study Group, copper price divergence between geographically distinct settlement points has historically ranged from $15 to $80 per metric tonne during periods of supply disruption International Copper Study Group annual report. At a position size of 1,000 tonnes, that range represents a P&L variance of $15,000 to $80,000 attributable solely to basis before flat price movement is considered.

Why Does Position Translation Between COMEX and LME Create Basis Risk?

Position translation between COMEX and LME creates basis risk because the two instruments do not share the same time structure, denomination, or delivery terms. When a COMEX monthly futures position is mapped against an LME daily-prompt forward, the resulting hedge contains an unmodeled spread between the specific LME prompt date and the nearest COMEX monthly expiry. If that spread is not explicitly priced and tracked, the position carries residual exposure that does not appear in a standard mark-to-market and cannot be governed by any risk limit in the system.

What "Unquantified" Actually Costs a Copper Trading Desk

Every risk management framework distinguishes between identified risk and unquantified risk. An identified risk (even a large one) can be limit-governed, monitored, and managed. An unquantified risk has no governance mechanism because it does not formally exist in the system reporting structure.

When a position management platform maps an LME copper forward to the nearest COMEX monthly equivalent without modeling the intra-month spread, the result is what risk practitioners call a ghost position: a real economic exposure that does not appear in reported risk metrics and therefore receives no management attention until it surfaces as a P&L variance.

For example, a trader uses COMEX front-month futures to hedge physical copper priced off the LME cash settlement, with physical delivery scheduled for a specific date 12 business days forward. The LME cash price and the COMEX front-month price are not the same instrument. The spread between them (cash-to-front carry on the LME plus the COMEX-LME geographic and structural basis) is the unhedged residual exposure. If that spread is not tracked at daily-prompt granularity, the trader carries exposure that does not appear in any system output.

A 2023 analysis by the Risk Management Association found that basis risk was a contributing factor in over 40% of commodity hedging P&L variances that exceeded initial projections. A significant portion arose from cross-exchange positions where spread data was modeled at insufficient granularity or sourced from a structurally different instrument [LINK: Risk Management Association commodity hedging report].

"Unquantified" means absent from the risk report. What is absent from the risk report cannot be governed.

The Five Inputs That Define the Basis Gap

Asserting that two curves differ is insufficient for risk management purposes. A risk framework requires naming the specific inputs that diverge and measuring each independently. For COMEX copper and LME copper, those inputs are:

1. Prompt Date Granularity

COMEX generates one settlement price per calendar month. The LME generates one official price per business day in the near-dated window. A cross-exchange position spanning a period covered by LME daily prompts is exposed to intra-month carry movements that have no COMEX equivalent and cannot be observed from COMEX data alone.

2. Denomination and Unit Conversion

COMEX prices copper in U.S. cents per pound; the LME prices in U.S. dollars per metric tonne. The conversion factor is fixed at 2,204.62 pounds per metric tonne, but rounding conventions and tick-size mechanics create systematic discrepancies at scale. According to CME Group contract specifications, one COMEX copper tick of $0.0005 per pound equals $12.50 per contract; one LME copper tick of $0.50 per metric tonne equals $12.50 per lot [LINK: CME and LME contract specification comparison]. The dollar equivalence at one tick is coincidental. The pricing mechanisms producing that tick are structurally independent.

3. Delivery and Warehouse Geography

LME approved warehouses span multiple continents, and physical warrant premiums vary by location. COMEX delivery is concentrated in U.S.-based facilities. A cross-exchange position that treats LME and COMEX prices as interchangeable omits the geographic delivery premium embedded in LME warrant pricing, which can move independently of and at a different rate than the flat copper price.

4. The LME Lending Market

The LME's tom-next and date-dated lending market is the mechanism through which daily carry between adjacent prompt dates is explicitly priced. When the lending market tightens, particularly in backwardation, the spread between adjacent LME prompt dates can widen materially intraday. COMEX has no structurally equivalent instrument. A risk system that models LME daily carries by extrapolating from COMEX monthly spreads is using a structurally different data source to estimate a structurally different market behavior.

5. Settlement and Financing Mechanics

COMEX margins are posted in USD and marked to market daily through CME Clearing. LME contracts involve a combination of initial and variation margin through LME-approved clearing members, with settlement mechanics that differ from CME's daily variation margin cycle. These settlement differences affect the financing cost of maintaining a cross-exchange position over time. This cost must be explicitly modeled within the position's total carry calculation, not assumed to net to zero.

Each of these five inputs is independently measurable. A platform with depth-accurate spread data for both curve architectures can hold each divergence explicitly within the risk framework, where it can be governed and managed rather than absorbed as unexplained P&L.

Quantifying COMEX Copper Basis Risk Requires Depth-Accurate Spread Data

Cross-exchange copper positions are structurally valid, widely used, and commercially rational. The remaining unquantified COMEX copper LME copper basis risk is a solvable data and methodology problem.

A trading operation that manages copper exposure across COMEX and LME with correctly structured spread data can model the following with precision:

- The daily prompt date spread for the LME leg of any cross-exchange position at each relevant tenor

- The COMEX monthly-to-LME-prompt-date basis across the full near-dated window

- The geographic delivery premium embedded in LME warrant pricing relative to COMEX U.S. delivery

- The lending market carry between adjacent LME prompt dates, including behavior under backwardation

- The denomination conversion P&L impact at individual position granularity, not just portfolio level

Can Cross-Exchange Copper Positions Be Accurately Hedged?

Cross-exchange copper positions can be accurately hedged when the risk system has access to depth-accurate spread data for both the LME forward curve at daily prompt resolution and the COMEX futures strip. The hedge is not inherently flawed, but it requires explicit modeling of the five structural divergence inputs identified in this analysis. A platform that collapses either curve to monthly buckets before computing the hedge ratio introduces structural error into the position from the point of entry, and that error compounds as the position ages.

The Risk Is Quantifiable With the Right Data

The structural difference between COMEX copper futures and LME copper forward contracts is a foundational fact about how the two instruments are constructed, how their curves are populated, and what data is required to translate a position between them with integrity.

The basis risk at the translation point becomes unmanageable only when it remains unquantified. This happens when the five specific inputs driving divergence between the two curve architectures are collapsed into a single assumed spread and removed from the governance framework.

Every input is independently measurable. Every component of the basis can be held explicitly in a system built for that precision. The relevant question is whether your platform was built for precision or built to approximate it.

Three immediate steps for any desk carrying cross-exchange copper positions:

- Audit your spread data resolution. If your system maps LME forward positions to the nearest COMEX monthly equivalent, identify every position where the LME prompt date does not align with a COMEX expiry date. Those misaligned positions carry unmeasured basis exposure today, in every open risk report you are currently reviewing.

- Verify your denomination conversion methodology. Confirm that unit conversion between U.S. cents per pound and USD per metric tonne is applied at individual position granularity, and that tick-value discrepancies between the two contract structures are tracked explicitly rather than absorbed into a rounding convention.

- Stress-test your LME carry assumptions. Run your cross-exchange positions against a simulated LME backwardation scenario. If your system P&L does not respond to intra-month prompt date spread widening, your carry model is incomplete, and you are carrying LME lending market exposure that your current risk metrics are not capturing.