Depth-First Base Metals Intelligence: A New Standard

Depth-first base metals intelligence is a new platform category defined by complete, systematic mastery of each base metal (copper, aluminum, zinc, nickel, lead, and tin) across every primary exchange before advancing to the next commodity. No existing CTRM or ETRM platform was built this way. Every system covering base metals today arrived at metals through configuration, not construction. That structural difference defines the category boundary.

The daily reality most base metals traders manage is familiar: a front-office copper trader at a mid-market firm runs position visibility in one system, pulls LME settlement prices from a second feed, reconciles SHFE exposure in a spreadsheet, and discovers at the end of the day that none of these sources agreed. This stems from platform architecture rather than workflow.

According to the London Metal Exchange annual statistics London Metal Exchange, base metals futures and options traded on the LME alone represent notional exposure exceeding $15 trillion annually. Yet virtually every platform built to manage that exposure was designed for energy or agricultural markets first and then extended to metals by adding exchange configuration tables.

This post defines the category of depth-first base metals intelligence precisely, names the structural difference between purpose-built and retrofitted systems, and establishes why 2024 marks the first time this category has been built from the ground up.

Why Multi-Commodity Platforms Fall Short for Base Metals Traders

The dominant logic behind multi-commodity platforms has always been coverage breadth. Build a system that handles crude oil, natural gas, corn, and soybeans, then add copper, aluminum, and zinc. Configuration tables absorb the exchange specifications. A currency module handles multi-exchange pricing. The result is a platform that is technically present in base metals and operationally insufficient for them.

This logic produces systems that are well-suited to the markets they were designed for and structurally mismatched for base metals. That distinction is precise and consequential.

The Structural Difference Between Base Metals and Energy Commodities

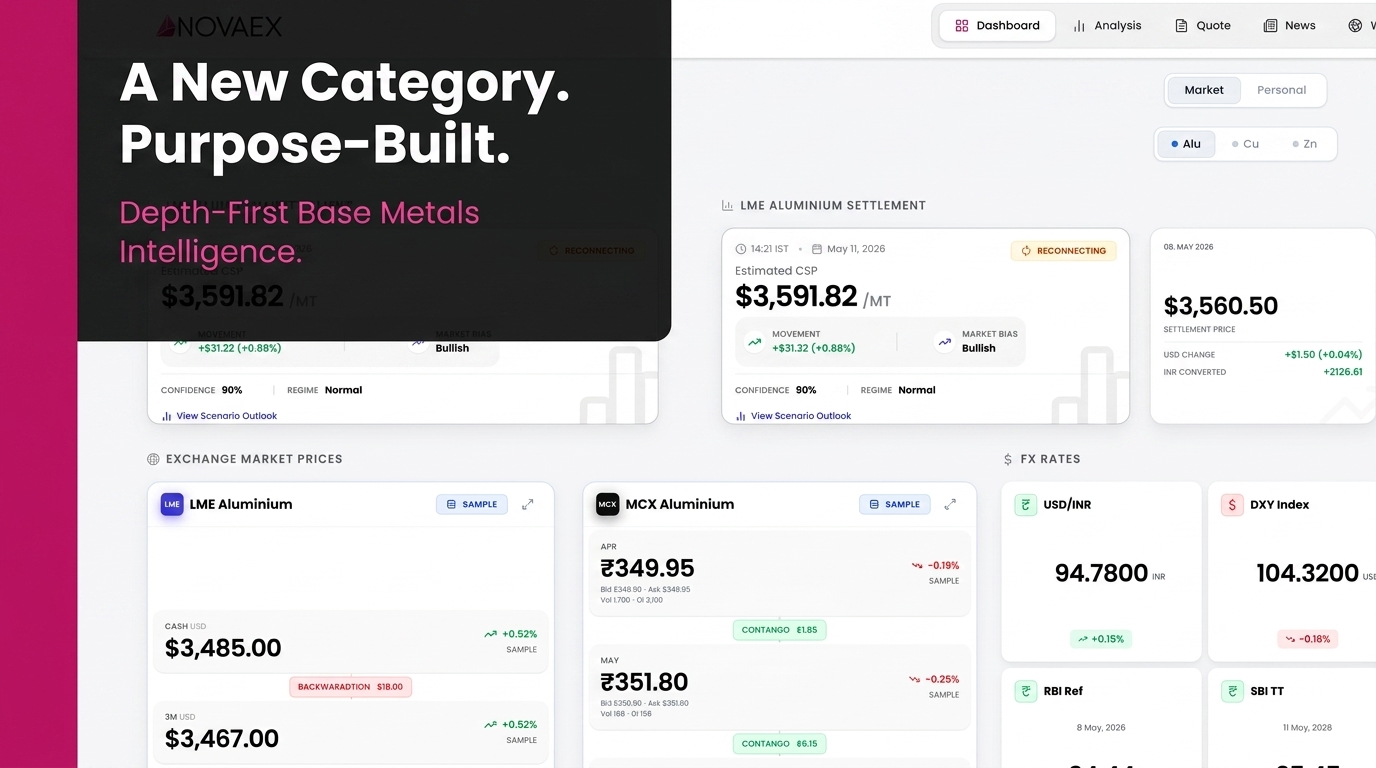

Base metals diverge from energy commodities in three structural dimensions that configuration cannot bridge. First, LME pricing operates on a daily prompt-date curve, not a monthly settlement structure. This creates thousands of unique price points across the forward curve at any given time, a model that energy platforms were not built to represent natively.

Second, base metals trade simultaneously across four primary exchanges (LME, COMEX, SHFE, and MCX) with price relationships that constitute live arbitrage signals. According to CME Group market data CME Group, COMEX copper open interest regularly exceeds 200,000 contracts, while SHFE copper maintains an independent pricing model driven by Chinese physical demand. A trader managing cross-exchange exposure requires these feeds integrated into a single risk view in real time instead of being reconciled manually across separate data sources.

Third, physical delivery in base metals involves LME warrants, approved warehouse locations, and brand premiums. These specifications determine whether a physical settlement resolves at par, premium, or discount. Agricultural platforms understand physical delivery. Warrant-based delivery with exchange-approved brand designations has no direct equivalent in grain or oilseed markets. No configuration layer closes that gap.

This results in a structural failure rather than a circumstantial one. According to ComTech Advisory CTRM research ComTech Advisory, metals-specific CTRM implementations consistently overrun both timelines and budgets, with metals workflow gaps cited as a leading root cause across multiple independent assessments. Configuration layers delay the problem. They do not solve it.

Defining Depth-First Base Metals Intelligence

Depth-first base metals intelligence is the methodology and platform category defined by a single operating principle: master each base metal completely (its pricing mechanics, physical structure, multi-exchange relationships, hedging conventions, and position workflows) before advancing to the next commodity.

The term depth-first is borrowed deliberately from computer science, where a depth-first search exhausts one branch completely before backtracking. Applied to commodity intelligence, the principle is precise: copper is not covered until every dimension of copper (LME cash, LME 3-month, COMEX nearby, SHFE front-month, physical premiums, warrant availability, and cross-exchange basis) is modeled, sourced, and integrated. Then aluminum. Then zinc.

This is the structural opposite of the breadth-first architecture that has defined multi-commodity platforms for three decades.

The Impact of Depth-First Design on Daily Workflows

For a front-office metals trader, depth-first intelligence means the platform delivers insights that retrofitted systems cannot. The system instantly identifies the real-time cross-exchange copper position, net of all hedges across LME and COMEX. It tracks the current cash-to-three-month spread against historical backwardation levels that preceded previous physical premium adjustments. It also maps LME warrant positions relative to approved warehouse stock levels by location.

These queries form the operational core of base metals trading and happen under intense time pressure.

According to the World Bank Commodity Markets Outlook World Bank Commodity Markets Outlook, copper prices recorded intraday volatility exceeding 3% on more than 40 trading sessions in 2023 alone. This frequency makes manual reconciliation across fragmented systems operationally dangerous. A depth-first platform answers these questions from a single integrated data model. A retrofitted platform answers some of them, partially, after manual intervention.

The Structural Difference: Design vs. Configuration

The clearest way to identify a retrofitted system is to examine where its data model begins.

Energy and agricultural CTRM platforms were designed around a settlement-date pricing model: prices are assigned to delivery months, positions aggregate by month, and P&L calculates against monthly benchmarks. This model is correct for crude oil, natural gas, and most agricultural contracts. It is structurally insufficient for LME base metals.

LME contracts price against prompt dates: any business day up to three months forward, and specific monthly dates beyond that. A copper position booked today may price against a prompt date seventeen business days out. The pricing engine must maintain a continuous daily forward curve, not a monthly strip, requiring a different foundational data structure rather than an additional configuration field.

Handling LME Prompt Dates Natively

A purpose-built metals platform treats the LME daily prompt-date curve as a first-class data object. It functions as a native structure in the pricing engine from day one. Every position, every hedge, every P&L calculation references this curve directly. There is no translation layer between the platform's internal model and LME's actual pricing structure.

Retrofitted platforms handle LME prompt dates through approximations: daily price imports that overwrite monthly buckets, interpolation scripts between settlement dates, or manual end-of-day adjustments. These workarounds function in stable markets. According to LME market reports LME market data, copper has recorded intraday price moves exceeding $200 per tonne during periods of geopolitical supply disruption. These are precisely the conditions under which manual reconciliation introduces material position risk.

The gap between purpose-built and retrofitted systems stems from design origin rather than features. No amount of configuration closes the distance between a monthly settlement engine and a daily prompt-date curve.

Why This Category Did Not Exist Before Now

The absence of depth-first base metals intelligence as a named, built category before 2024 has a clear explanation: the platforms that could have built it chose breadth instead.

The CTRM market is dominated by vendors whose growth strategy has consistently prioritized horizontal expansion. According to MarketsandMarkets CTRM research MarketsandMarkets, the global commodity management software market is projected to reach $1.4 billion by 2028, driven primarily by multi-commodity platform consolidation. The economics of that market reward breadth: more commodities, more asset classes, more buyers. Depth is a harder commercial argument when procurement decisions are evaluated against feature checklist coverage.

The result is a three-decade absence of a platform built with depth-first methodology as its organizing architectural principle for base metals trading.

Previous Attempts at Metals Coverage

No platform has previously built depth-first coverage for base metals as a founding architecture. Several vendors have built metals modules with genuine strength in specific areas: some maintain capable LME pricing engines, others have mature physical delivery workflows, a few offer multi-exchange position consolidation. None were built from a single integrated architecture with depth-first methodology as the organizing principle across pricing intelligence, position management, and risk analytics simultaneously.

The distinction is between having depth in isolated components and being built for depth end-to-end. A platform with a strong LME pricing module that connects to a general-purpose position management engine still requires a translation layer between exchange-native pricing and portfolio reporting. That translation layer is where accuracy degrades and manual intervention begins. Depth-first base metals intelligence eliminates the translation layer by design instead of attempting to improve it.

Novaex: The Founding Instance of Depth-First Base Metals Intelligence

Novaex was built by a trader who spent four years inside existing platforms searching for one that genuinely understood base metals. The search ended with a conclusion that became a design specification: the platform that metals traders need does not exist, because no one had built it from a depth-first starting point.

The Novaex architecture begins with a complete model of LME pricing structure (daily prompt dates, cash-to-three-month spreads, monthly averages, and forward curve movements) as the native data layer. Every subsequent function is built on that layer: position management that aggregates across LME, COMEX, SHFE, and MCX using exchange-native pricing; risk analytics that calculate exposure against the actual prompt-date curve; and execution support that surfaces the data a trader needs at the precise moment a decision must be made.

Rather than adding a metals module to an existing platform, Novaex derives its entire architecture from what base metals actually require.

Supported Exchanges and Metals

Novaex covers the six primary base metals (copper, aluminum, zinc, nickel, lead, and tin) across four exchanges: LME, COMEX, SHFE, and MCX. According to LME base metals statistics LME data, these six metals account for more than 95% of global non-ferrous metals exchange trading volume, representing the complete operational universe for base metals trading organizations.

Coverage depth defines the architecture. Each metal is modeled with its complete exchange-specific pricing structure, physical delivery conventions, and cross-exchange relationship history before the platform advances to the next metal. The platform covers what it knows and knows what it covers completely.

What Depth-First Base Metals Intelligence Changes for Trading Organizations

The operational consequences of a depth-first architecture are measurable at the desk level.

A metals trading operation running on a retrofitted multi-commodity platform allocates a significant share of its daily workflow to data reconciliation. This includes pulling settlement prices from exchange feeds, cross-referencing position reports from the CTRM, adjusting for prompt-date pricing the system approximates rather than calculates natively. According to Accenture commodity trading research Accenture's commodity trading operations research, front-office traders in commodity-intensive firms spend up to 35% of their time on data management tasks that purpose-built technology should structurally eliminate.

Depth-first intelligence eliminates these tasks at the architecture level. Instead of adding a reconciliation module, it builds a data model where reconciliation between the market and the platform is unnecessary.

For mid-market metals trading organizations, the commercial consequence is direct. Novaex is built on the principle that hedge-fund-level base metals analytics should not require hedge-fund-level infrastructure budgets. The pricing tier that previously restricted integrated pricing intelligence, position management, and risk analytics to enterprise-scale buyers becomes accessible to the organizations that need it most: physical traders, mid-market merchants, and specialist hedge funds whose entire edge depends on knowing base metals with precision.

The depth-first category exists specifically to close that gap.

The Depth-First Base Metals Intelligence Standard, Defined

Every new platform category requires a definition precise enough to distinguish it from adjacent categories. Depth-first base metals intelligence is defined by three criteria:

- Native base metals data architecture. The pricing engine was built for LME prompt dates, multi-exchange arbitrage, and warrant-based physical delivery from the ground up, rather than adapted from an energy or agricultural pricing model through configuration.

- Integrated intelligence across three functions. Pricing intelligence, position management, and risk analytics share a single data model. There is no translation layer between what the market prices and what the platform reports.

- Commodity-complete before commodity-broad. Each base metal is fully modeled across all primary exchanges, all pricing dimensions, and all physical delivery specifications before the platform expands to new commodities.

When a metals trader rebuilds a position report in a spreadsheet because the CTRM returned incorrect prompt-date math, the fault lies with a platform built for a different market operating outside its native design scope.

When a risk manager waits until the end of the day for a consolidated cross-exchange view because real-time LME and SHFE feeds terminate in separate systems, it represents an architecture failure.

Depth-first base metals intelligence names the problem with precision. Novaex is the platform that resolves it structurally.

See the architecture in practice.

Novaex platform demo Schedule a platform walkthrough to see a native LME prompt-date pricing engine, integrated cross-exchange position management across LME, COMEX, SHFE, and MCX, and real-time risk analytics built on a single base metals data model that is strictly purpose-built.

The category exists. The platform is live. Evaluate whether your current system was built for your market, or built for someone else's and configured to approximate yours.