How LME Aluminum Spread Carry Costs Break Hedge Ratios

When a commodity platform treats the LME aluminum spread as a date-agnostic indicator rather than a prompt-date-specific carry instrument, it introduces measurable carry-cost errors into every hedge ratio calculation. Physical aluminum traders running 500-tonne positions absorb untracked basis exposure of $700 to $11,700 per position per roll cycle depending on prompt date misalignment. The error has a strictly architectural origin.

The London Metal Exchange publishes aluminum prices across a continuous prompt date structure spanning cash (T+2) through 10 years forward. LME aluminum prompt date structure That structure carries operational significance: each prompt date reflects a specific cost that cannot be accurately approximated by dividing the cash-to-3-month spread by a round number.

Most multi-commodity platforms do precisely that. When a physical aluminum trader builds a hedge ratio on that approximation, the error becomes tangible basis exposure, tracked nowhere and reported to no one.

The Precision Mechanics of LME Aluminum Spreads

Unlike conventional exchange-traded futures contracts with monthly expiry cycles, the LME aluminum contract trades on a prompt date basis, meaning any business day from T+2 (cash) through to the 3-month date (approximately T+63 business days), then on specific third-Wednesday monthly dates out to 63 months, and semi-annual December dates out to 10 years.

LME trading statistics show aluminum as its highest-volume non-ferrous metal contract, averaging over 350,000 lots per day, with each lot representing 25 tonnes of primary aluminum. LME trading statistics That volume is distributed across hundreds of discrete prompt dates simultaneously, each with its own independently tradeable spread.

The spread between any two prompt dates reflects the cost of carry for that specific interval: financing charges, LME-approved warehouse storage fees, and any supply-demand premium or discount embedded in the forward curve. These components do not distribute uniformly across calendar time.

LME Aluminum Spread Pricing Mechanics

An LME aluminum spread is the price differential between two specific prompt dates on the LME forward curve, priced directly through spread trading rather than arithmetic derivation. It reflects the actual financing, storage, and risk-premium costs of holding physical aluminum between those exact two dates. The cash-to-3-month spread is the primary reference point, but intra-period spreads between any two business-day prompts are independently quoted and tradeable.

This pricing mechanism carries weight because carry costs are not uniform across the daily date range. The tom-next spread (T+2 to T+3) regularly trades at an implied daily rate that differs materially from the average daily carry embedded in the cash-to-3-month spread. On days with tight nearby availability, the tom-next can spike to several multiples of the average daily carry while the 3-month price barely moves.

The LME Aluminum Prompt Date Structure

The LME aluminum prompt date structure runs from cash settlement (T+2) through every individual business-day date to the 3-month prompt (approximately T+63 business days), followed by third-Wednesday monthly prompts out to 63 months, and semi-annual December prompts to 10 years forward. Each prompt is a discrete, tradeable settlement date rather than an interpolated position on a curve.

This granularity carries direct operational impact. A physical aluminum buyer with a delivery obligation on a specific date in six weeks does not hold a "6-week position." They hold a position on the exact LME business-day prompt corresponding to that delivery date, and the carry to that prompt is a specific, observable number rather than an estimate derived from the 3-month price.

Platform Misrepresentation of LME Aluminum Spread Carry

Most multi-commodity platforms source a single LME aluminum price, typically the 3-month official price published each day by the LME, and use it as their primary market reference rate. LME official pricing methodology When they need to calculate carry for a specific forward date within the daily prompt window, they interpolate linearly between the cash price and the 3-month price using calendar days.

That methodology contains a core error before any other variable is considered.

The LME cash-to-3-month spread covers approximately 63 business days, rather than 91 calendar days. A platform dividing a $30/tonne contango by 91 calendar days derives a daily carry rate of $0.330/tonne. The correct business-day carry rate for the same spread is $0.476/tonne per business day, a 44% difference in the per-day carry assumption traceable directly to the LME prompt date calendar.

The Root Cause of Commodity Platform Pricing Errors

Generic commodity platforms misrepresent LME aluminum spread carry because they are architecturally built for exchange-traded futures with monthly expiry cycles rather than the continuous business-day prompt date structure of the LME. They treat the 3-month official price as a front-month equivalent and apply linear interpolation for intermediate dates, a methodology appropriate for NYMEX crude oil but structurally incompatible with LME daily prompt mechanics.

Industry assessments of CTRM platform architecture indicate multi-commodity platforms consistently apply generic curve-building methods across all covered markets rather than market-specific pricing engines. CTRM platform design analysis The design constraint is resource-driven. A platform covering 40 commodities cannot build a specialist prompt-date pricing engine for each one and remain commercially viable on a generalist model.

The error functions as a structural consequence of prioritizing breadth over depth, a trade-off with a quantifiable cost to aluminum traders at every hedge settlement.

The Hedge Ratio Math: Where Date Misalignment Compounds Error

A hedge ratio for a physical aluminum position requires more than a lot-count equivalent of tonnes. For a physical position with a specific delivery date that does not fall on the 3-month prompt, the effective hedge requires adjustment for the carry differential between the delivery date and the futures settlement date being used as the hedge instrument.

This adjustment depends on the exact spread between the physical delivery date prompt and the futures prompt date. physical commodity hedge ratio methodology Generic platforms that cannot resolve individual daily prompts cannot calculate that spread correctly, meaning they cannot calculate the adjusted hedge ratio correctly.

The Impact of Carry Costs on Hedge Ratios

Carry costs affect aluminum hedge ratios by creating a basis differential between the physical delivery date and the futures settlement date. When this differential is calculated using the wrong daily carry rate, the hedge covers a different exposure than the physical position carries, leaving residual basis risk that fails to appear in any position report until the position settles. The magnitude of the error is directly proportional to the number of misaligned days multiplied by the error in the daily carry rate.

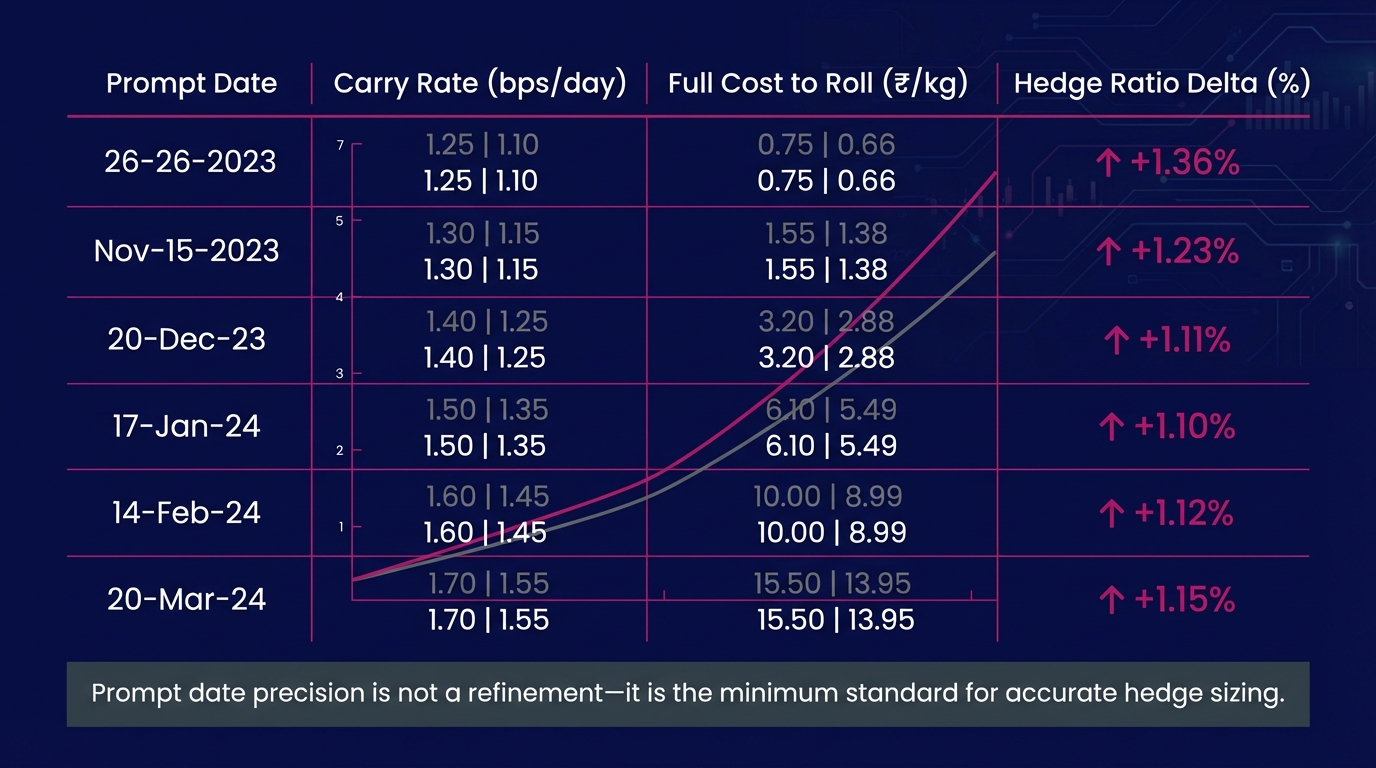

If a physical trader holds a 500-tonne long position with a delivery obligation on a specific business-day prompt 47 business days forward, inside the 3-month window but not on the 3-month prompt, their hedge requires a 3-month futures position adjusted for the 16-business-day carry between their delivery date and the 3-month prompt.

At a cash-to-3M contango of $30/tonne over 63 business days, the carry calculation diverges immediately between a precision engine and a calendar-day interpolation:

- Correct carry (63 business days): 16 days × $0.476/tonne = $7.62/tonne

- Platform carry (91 calendar days): 16 days × $0.330/tonne = $5.28/tonne

- Error per tonne: $2.34/tonne

- 500-tonne position: $1,170 untracked basis exposure per hedge

Quantifying the Hedge Ratio Miscalculation in Basis Points

Expressing this error in basis points requires relating it to the total hedged position value. On a 500-tonne aluminum position at $2,400/tonne, position value is $1.2 million. The $1,170 carry error represents approximately 9.75 basis points of position value, derived from calendar-day interpolation alone before any other platform approximation is accounted for.

The Financial Cost of Miscalculated Hedge Ratios

Under normal contango conditions ($25 to $35/tonne cash-to-3M), calendar-day interpolation error on a standard 500-tonne position produces 8 to 12 basis points of untracked basis exposure per hedge per roll cycle. Under elevated contango conditions, such as the 2020 to 2021 warehousing cycle when LME cash-to-3-month aluminum spreads reached $45 to $55/tonne, the same calculation pushes basis-point exposure above 18 to 22 bps per position per roll. LME aluminum historical spread data

On a book of 10 rolling 500-tonne hedges at $2,400/tonne aluminum, that range translates to $11,700 to $31,900 in cumulative untracked basis exposure per roll cycle. This exposure fails to trigger any risk alert on the platform generating it because the system lacks visibility into the error it produces.

The more operationally significant consequence is where this exposure appears. Because generic platforms do not report carry-cost misalignment as a risk event, the exposure surfaces as unexplained P&L variance at settlement, attributed by trading desks to "market conditions" or "basis movement" rather than to a systematic pricing methodology failure. A 2022 CTRM Center survey notes unexplained basis variances at settlement rank among the top three reconciliation challenges reported by commodity trading firms. CTRM Center industry survey Carry-cost misrepresentation in spread pricing is a primary structural contributor to that problem for metals books specifically.

For a rolling hedge book, where positions are regularly rolled from expiring prompts to forward prompts each quarter, the error compounds with each cycle. A trader running a 12-month rolling hedge program on 2,000 tonnes with quarterly rolls, under mid-range contango conditions, absorbs:

- 4 roll cycles × 2,000 tonnes × $2.00/tonne carry error = $16,000/year in systematically untracked basis exposure

Structural Limitations of Generic Commodity Platforms

The issue stems from resource allocation under a multi-commodity business model rather than engineering capability. Covering 40+ commodities at the depth each market demands lacks architectural compatibility with how software development resources scale.

An LME aluminum spread pricing engine that eliminates carry-cost error requires:

- Full prompt date resolution from cash to 10 years forward for every tradeable business-day and monthly date, rather than a single 3-month anchor with interpolation.

- Real-time spread pricing for every inter-prompt interval, with independent tom-next and date-specific spread handling.

- LME business-day calendaring aligned to the LME official holiday schedule, preventing the generic weekday logic that miscounts days between prompts.

- Separate treatment of tom-next carries versus the average daily carry implied by the cash-to-3M spread.

- Physical delivery date integration that maps actual warehouse delivery schedules to exact LME prompt dates for hedge ratio calculation.

A platform covering 40 markets will not, by design, build five separate specialist pricing engines for the nuances of LME base metals market structure. The resource allocation structure does not support that outcome. A depth-first approach, where the aluminum spread engine is built to the exact specification the LME market operates at before any other commodity is added, provides the required architecture for a pricing engine that resolves this problem at the level of precision the market demands.

Requirements for Accurate LME Aluminum Spread Pricing

Accurate LME aluminum spread carry calculation requires correct structural application rather than basic data sourcing. The LME publishes official cash, tom-next, and 3-month prices daily, and inter-prompt spreads are tradeable and observable throughout the session. The requirement centers on whether the platform receiving that data applies it with the correct structure.

A precision LME aluminum spread engine operates on the following non-negotiable requirements:

Prompt date resolution must be complete. Every LME business-day prompt from cash to 3 months must be individually addressable and independently priceable. Third-Wednesday monthly prompts out to 63 months must resolve to actual calendar dates against the LME published holiday schedule, rather than a generic third-Wednesday approximation.

Carry calculations must use LME business-day counts. The cash-to-3M spread divides by 63 business days, rather than 91 calendar days. The difference in the resulting daily carry rate is 44%, traceable directly to the LME published settlement structure. Any system using calendar days applies a known, observable error at the foundation of every carry calculation.

Tom-next and intra-period nearby spreads must be handled independently. The implied daily carry in the tom-next spread differs structurally from the average daily carry in the cash-to-3M spread. Using the cash-to-3M average for nearby hedge ratio calculations introduces an additional error layer on top of the calendar-day problem.

Physical delivery date must drive the hedge calculation, rather than the nearest standardized futures prompt. LME physical hedging guidance states the ideal hedge for a physical aluminum position uses the prompt date matching the physical delivery date as the primary carry reference. LME physical hedging guidance Any mismatch between the physical prompt and the hedge prompt creates residual basis risk. It must be quantified, not absorbed silently.

The hedge ratio error documented throughout this post stems directly from platforms that cannot resolve the LME aluminum prompt date structure at the granularity the market operates at, and therefore cannot provide the inputs a correct hedge ratio calculation requires.

Novaex operates on the principle that each commodity must be understood completely before a platform earns the right to claim it covers that market. Novaex depth-first methodology For LME aluminum, that means a spread pricing engine with full prompt date resolution, LME-calendar business-day counting, independent tom-next handling, and physical delivery date integration, rather than a 3-month price with a linear interpolation overlay.

The LME Spread Calendar as a Precision Instrument

The LME aluminum spread calendar serves as a sequenced pricing structure where every prompt date carries a specific, observable cost, and every hedge ratio that depends on carry must be calculated against the actual structure rather than a smoothed approximation designed for multi-commodity platform convenience.

Physical aluminum traders absorbing carry-cost errors from date-agnostic platforms face analytically incomplete data delivered by generic systems designed for a different problem.

Accurate hedge ratio calculation requires true platform precision rather than trader methodology adjustment.

Immediate diagnostic steps for physical aluminum traders:

- Audit current hedge ratios against actual LME prompt date carries. For each delivery date in your book, compare the carry your platform assumes against the observable cash-to-prompt spread for the same date on the same day. The gap is the carry error your platform embeds in your positions.

- Quantify the calendar-day versus business-day carry discrepancy on your last three rolls. Divide your observed cash-to-3M contango by both 91 calendar days and 63 business days. The difference between the two daily carry rates, multiplied by the days between your delivery prompt and the 3-month prompt, is the minimum systematic error floor your platform has applied.

- Map your delivery dates to their exact LME prompt dates. Measure the spread between each delivery prompt and the 3-month prompt used as your hedge reference. That spread differential, multiplied by your position size, is your current untracked basis exposure, carried silently in every position in your book.

Novaex runs those calculations against the full LME aluminum prompt date structure in real time. Novaex aluminum pricing platform The LME spread calendar is a precision instrument. The platform you use to trade against it should be built to treat it as one.