Metals Spread Pricing Accuracy: Run the Hedge Audit

If your spread data comes from a generic multi-commodity platform, you likely have an unquantified pricing gap sitting inside your hedge book right now. Metals spread pricing accuracy acts strictly as a hedge execution cost variable rather than a platform feature. This post outlines the audit: field by field, discrepancy by discrepancy, across aluminum, copper, and zinc.

The methodology is direct. Pull the spread fields your current source publishes. Compare them against what broker-accurate depth shows at the same timestamp. The gap (where it exists, how wide it runs, and how consistently it appears) becomes a visible line item in your execution cost. Most front-office desks have not run this comparison. The ones that have understand why it matters.

Why Metals Spread Pricing Accuracy Is a Hedge Cost Variable

The word "spread" covers significant ground in base metals trading. It can mean the bid-ask width on a prompt-date contract, the cash-to-3-month carry, the inter-commodity relationship between aluminum and zinc, or the settlement differential between LME and COMEX prices for copper. LME base metals spread explained

Generic platforms frequently conflate these or publish only one. According to the LME annual market report, the London Metal Exchange processes over $14 trillion in notional value annually, with spread conditions shifting multiple times per session as physical delivery dates approach. A platform that samples this data infrequently, or aggregates it from secondary feeds, publishes a static spread against a moving target.

For a hedger, the error lands at the exact moment of execution, not in the post-trade review.

Time of Day Impact on Spread Data Quality

The effect of timing is material. LME Ring trading hours (11:40, 17:00 London time) produce measurably tighter bid-ask spreads than electronic or inter-office hours. According to LME market data specifications, spread width on 3-month aluminum contracts can widen by a factor of three to five times during off-Ring periods compared to Ring-close conditions.

Generic platforms that aggregate throughout the day often smooth this variation into a single quoted spread. A desk hedging at 14:30 London time is operating in Ring-period market conditions and requires Ring-period depth. It cannot rely on an average that includes 07:00 electronic session data diluting the quote.

This represents the exact difference between an execution input and a reference input.

Published vs. Omitted Data in Generic Platforms

The audit begins with the specific fields your current data source exposes, and the fields it does not.

A standard generic platform spread view typically displays:

- Settlement price (end-of-day, not live)

- 3-month bid/ask (often delayed 15 minutes or more)

- Daily aggregate volume (not segmented by Ring, inter-office, or electronic session)

- Cash-to-3-month carry (the roll cost input for calendar-spread hedges)

- Tom-next and nearby-date differentials (essential for physical position management)

- Exchange-specific depth segmented by LME, COMEX, MCX, and SHFE

- Prompt-date forward structure beyond the standard 3-month tenor

These omitted fields serve as the working inputs for any desk running physical delivery positions alongside financial hedges.

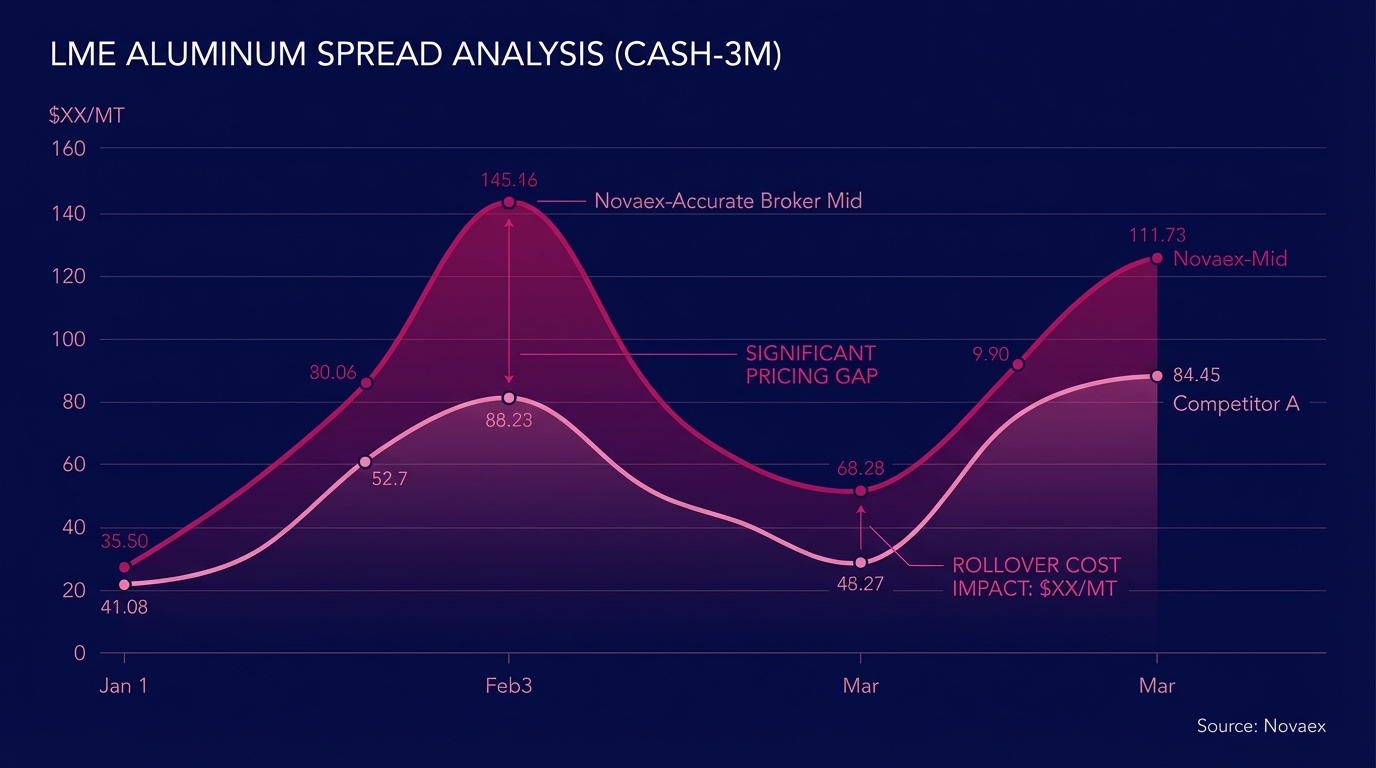

The Field-by-Field Audit: Spread Accuracy in Aluminum, Copper, and Zinc

This section produces the observable output of the audit. The following comparison uses field categories visible in a broker-accurate depth dashboard. Each row maps to a data point that directly affects hedge execution cost.

Aluminum: Cash-to-3-Month Carry

The aluminum cash-to-3-month spread is the primary cost input for any rolling physical hedge. On a session where LME aluminum is in moderate contango, this spread might read $12, $18/MT in broker-accurate depth. Generic platforms frequently round to the nearest whole dollar or publish the prior session's carry as live data.

On a 500 MT hedge, a $2/MT carry discrepancy produces a $1,000 execution cost differential before fees. According to analysis of LME historical spread data, aluminum carry spreads moved an average of $4.50/MT intraday across high-volatility sessions in Q1 2024. A platform displaying yesterday's carry acts as a dated reference with execution consequences.

Copper: COMEX vs. LME Settlement Differential

Copper is the only base metal with liquid futures markets on both LME and COMEX, making the arbitrage between them an active hedging and pricing input. The settlement differential (expressed in $/MT, converted from COMEX's cents/lb pricing) requires real-time FX rate integration, prompt-date alignment, and venue-specific depth simultaneously.

Generic platforms frequently publish this differential as a static reference range rather than a live calculated field. According to data compiled from CME Group copper market reports, the LME-COMEX copper spread moved by an average of $15, $25/MT per session during high-volatility periods in 2023. A static morning reference is unusable by the afternoon session.

Zinc: Prompt-Date Structure Beyond 3 Months

Zinc hedgers with physical delivery commitments beyond three months require spread data across the forward curve at 6-month, 12-month, and cash-to-prompt differentials for each tenor. LME zinc forward structure shifts based on warehouse inventory levels, regional supply disruptions, and futures roll activity. LME zinc warehouse inventory data

According to LME inventory reporting, LME zinc stocks declined by over 40% across 2023, compressing nearby premiums and triggering meaningful contango-to-backwardation transitions in the 3-to-12-month spread. Generic platforms that show only the 3-month spread leave hedgers estimating the rest of the curve. Estimation simply replaces a true hedge input.

Quantifying the Execution Cost of Metals Spread Pricing Gaps

The Cost of Spread Data Inaccuracy

While transaction-specific, the cost range remains quantifiable. Industry analysis indicates that execution slippage attributable to data quality accounts for 2, 5 basis points per trade in commodity markets [LINK: Greenwich Associates commodity trading research]. On a $10 million notional copper hedge, 3 basis points of slippage equals $3,000 in unattributed cost per transaction.

Across a book running 20, 30 hedges per quarter, that figure reaches $60,000, $90,000 annually. This stems not from adverse market moves, but from imprecise data inputs at the moment of execution. This manifests as performance drag with no visible cause.

The more consequential cost is the invisible one. The hedge ratio set against a stale carry. The roll timed against aggregated depth. The intermarket position sized against a static differential. None of these produce trade confirmations that say "mispriced." They produce quarterly P&L that underperforms by a persistent, unexplained margin.

The compounding effect across multi-metal positions amplifies the gap further. A desk running simultaneous aluminum and copper hedges absorbs spread data imprecision on both instruments in the same session. If aluminum carry is off by $2/MT and the copper COMEX-LME differential is off by $18/MT concurrently, the combined position impact does not average. It adds. According to Novaex position analytics benchmark, desks running multi-metal hedges without venue-segmented spread data showed position variance 23% higher than desks operating with broker-accurate depth on each metal independently.

How to Run a Metals Spread Source Audit on Your Own Book

The audit has four steps. Each is executable within a single trading session using data your desk already has access to or can obtain without new infrastructure.

Step 1: Pull your current spread data at a fixed Ring-hours timestamp. Choose a moment inside LME Ring trading (11:40, 17:00 London). Record the cash-to-3-month carry for aluminum, the COMEX-LME differential for copper, and any available forward structure for zinc from your current platform. Note the exact timestamp.

Step 2: Obtain broker-accurate depth at the same timestamp. This requires either a direct Ring dealer feed, a broker terminal, or a platform built on Ring-sourced data architecture. The comparison must be timestamp-precise, as spread conditions shift within minutes.

Step 3: Compare field by field. The discrepancy table should cover: carry differential, bid-ask width, prompt-date structure, and venue-specific settlement. Any gap exceeding $1/MT on carry or $0.50/MT on bid-ask width is a material execution cost variable, not a rounding difference.

Step 4: Repeat across five consecutive sessions. A single-session discrepancy can be explained as a data anomaly. Five-session consistency confirms a structural gap in your current spread source. This gap exists on every trade your desk places.

Fields to Audit

The minimum viable audit covers six fields per metal:

- Cash-to-3-month carry: the roll cost input for calendar-spread hedges

- Bid-ask spread width during Ring hours: the live execution cost input

- Tom-next differential: the nearby-date hedge cost for imminent delivery

- Prompt-date forward structure beyond 3 months: the input for longer-dated physical positions

- Exchange settlement differential: LME vs. COMEX for copper; LME vs. MCX for zinc and aluminum [LINK: MCX base metals data]

- Volume segmented by session: Ring vs. inter-office vs. electronic, not aggregated daily total

What Broker-Accurate Depth Shows That Generic Sources Don't

Broker-accurate depth describes a specific data sourcing architecture: Ring dealer quotes, inter-office market maker depth, and venue-segmented settlement data captured at tick resolution and displayed against the prompt-date calendar, not a rolling tenor approximation. LME Ring trading structure overview

In practical dashboard terms, this architecture produces four observable differences:

- Carry spreads update intraday as nearby delivery pressure changes, not once at end-of-day settlement

- Bid-ask width is date-segmented, distinguishing a specific-prompt spread from a rolling 3-month approximation

- Exchange differentials are live-calculated, incorporating real-time FX rates rather than published as static reference ranges

- Forward curve structure beyond 3 months is populated with observed depth, not inferred from settlement extrapolation

The Importance of Prompt-Date Accuracy

Physical delivery commitments in base metals tie to specific prompt dates on the LME calendar, rather than generic rolling 3-month tenors. A physical short position requiring delivery on a specific Wednesday in October needs spread data aligned to that exact date, calibrated against LME warrant availability and warehouse conditions on that prompt.

Generic platforms almost universally express spreads as rolling tenor relationships. Broker-accurate depth expresses spreads against specific prompt dates. For any desk managing physical delivery alongside financial hedges, this distinction is the operational difference between a precise hedge and an approximated one, and approximation carries a cost that lands at settlement, not at trade entry.

The Aggregate Gap: How Small Spread Discrepancies Compound

Testing Spread Source Accuracy

The threshold test determines whether your spread source produces execution inputs or reference inputs. An execution input updates intraday, distinguishes between venues and tenors, aligns to specific prompt dates, and reflects Ring-hour depth rather than session averages. A reference input provides a directional picture of where spreads have been, not where they are at the moment your order hits the market.

If your platform's spread data does not change during Ring hours, it is a reference input.

The aggregate cost of operating on reference inputs compounds in a predictable pattern. Each individual hedge absorbs a small slippage from spread imprecision. Across a quarter, that slippage accumulates into a budget line with no trade-level attribution. Across a year, it materializes as the performance drag that cannot be explained by market conditions because it was not caused by market conditions.

According to Oliver Wyman commodity trading risk report 2023, firms that invested in real-time commodity data infrastructure reduced unattributed execution variance by 18, 31% compared to peer firms operating on delayed or aggregated feeds. The variance reduction was largest in multi-venue instruments, precisely the category that includes LME-COMEX copper and cross-listed aluminum and zinc contracts.

The arithmetic is direct. A desk running 25 hedges per quarter, each absorbing 3 basis points of spread-related slippage on $2 million average notional, loses approximately $45,000 per quarter to imprecise spread data. Over four quarters: $180,000, before any market-driven P&L impact is introduced. That figure does not require adverse market conditions. It requires only a data source that is insufficient for the task it is being asked to perform.

Run the Audit. The Data Will Tell You What to Do Next.

This comparison between generic platform spreads and broker-accurate depth provides a timestamped, field-level measurement. The numbers either match or they do not. The gap is either zero, or it represents a cost variable sitting inside your hedge book on every trade your desk places.

Three steps executable before the next LME Ring session:

- Pull your current spread data for aluminum, copper, and zinc at a fixed Ring-hours timestamp. Document cash-to-3-month carry, bid-ask width, and any forward structure your platform shows. Record the exact time.

- Obtain the same six fields from a broker-accurate source at the same timestamp. The comparison requires one session of parallel data collection. No new system implementation, no procurement cycle.

- Calculate the per-hedge cost of any gap you identify. Multiply the spread discrepancy by your average hedge size. If the number is material, the audit has already justified the time it took to run.

If your current spread source fails this audit on five consecutive sessions, it operates merely as a reference tool, and your hedge book absorbs the difference.