Physical Metals Data Latency: Why Prompt Windows Matter

Physical metals trading data latency functions as a direct delivery cost risk. When a prompt date approaches on the LME, spread decisions require broker-consistent, real-time bid/ask precision. A 30-second delay in that window operates as a measurable cost event. Financial traders can absorb data latency. Physical metals traders cannot, and the architectural reasons for that distinction define what a capable metals platform must deliver.

The Latency Tolerance Gap in Commodity Markets

Financial and physical traders both consume market data. The operational similarity ends there.

A financial trader executing a copper futures position on CME can absorb 500 milliseconds of data latency without a material outcome change. The instrument is cash-settled. There is no delivery obligation. The spread between bid and ask represents a simple transaction cost.

According to a 2023 Bank for International Settlements analysis BIS market microstructure research, price impact for discretionary futures market participants becomes non-linear only at latency thresholds above 1,000 milliseconds. For a financial trader, delayed data creates friction without financial consequence.

Physical metals trading operates under a categorically different specification.

When a trader holds a physical position on the LME and a prompt date is approaching, the spread between cash and the next available date acts as a carry cost that determines whether a delivery obligation gets rolled, delivered against, or incurs a premium that compounds directly into the physical supply chain.

Why Data Latency Matters More in Physical Metals

Data latency matters more in physical metals because the financial outcome of a spread decision is coupled directly to physical delivery logistics. A financial trader's delayed quote costs basis points. A physical trader's delayed quote costs warehouse premiums, financing charges, and potentially a failed or over-cost delivery.

The difference is structural. Financial instruments tolerate asynchronous pricing because settlement is synthetic. Physical instruments require synchronous pricing because settlement is real.

What the Prompt Date Window Requires

The LME operates on a daily prompt date structure: a forward curve where each business day is a specific settlement date out to three months, followed by monthly dates extending further. This structure is unique among major commodity exchanges and creates a data precision requirement that generic market-data platforms consistently underestimate.

Defining the Prompt Date in Metals Trading

A prompt date is the specific future date on which a metals contract requires either physical delivery or a roll instruction. On the LME, every business day within the three-month window is a valid prompt date, meaning a trader can carry delivery obligations or hedge positions settling on any given day. As a prompt date approaches, spread data must be real-time and broker-consistent.

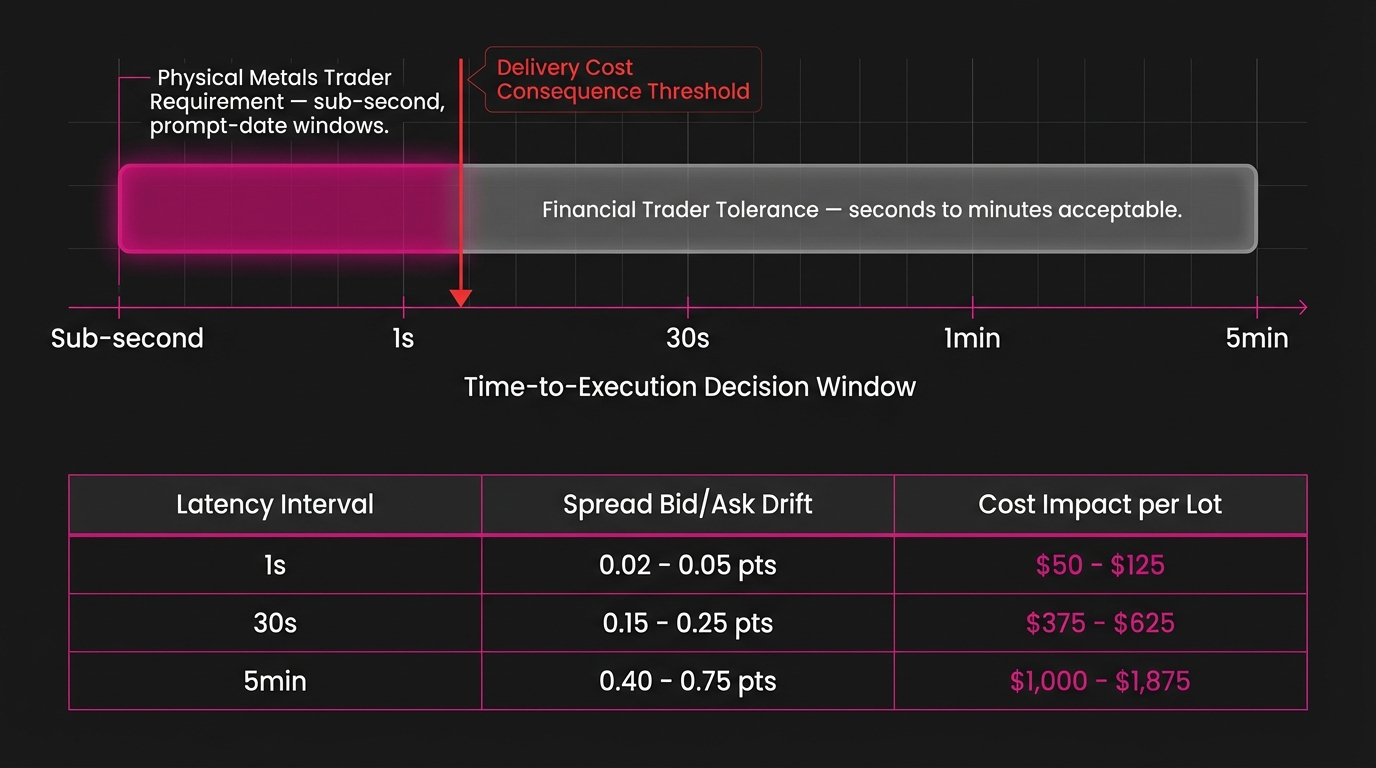

The 48-hour window before a prompt date is when spread decisions carry the highest cost sensitivity. During this period, LME ring brokers widen or tighten bid/ask spreads on Tom-Next and date-to-date carries based on live inventory levels, lending conditions, and borrowing demand in real time.

According to LME historical market data LME market statistics, the cash-to-three-month spread on copper has ranged from contango of approximately $50/t to backwardation exceeding $1,000/t during periods of extreme inventory tightness. This spread range can compress or expand within a single ring session of five minutes.

A trader relying on data delayed by 60 seconds in this environment is executing a spread decision against a price that no longer reflects live broker market conditions. This variance translates directly into carry cost overpayment with no recovery mechanism.

Tom-Next and Forward-to-Prompt: Where Latency Becomes a Cost Event

Tom-Next (Tomorrow-to-Next) is the single-day carry between tomorrow's date and the next business day. On the LME, it is the most granular expression of the lending and borrowing market, and the most latency-sensitive data point in physical metals trading.

Dynamics of the Tom-Next Window in LME Trading

During the Tom-Next window, ring brokers quote single-day carries that reflect real-time lending conditions, nearby inventory levels, and short-term financing rates. These quotes shift by $1, $3 per tonne within minutes during tight prompt periods. A trader executing a roll using data from 30 seconds prior is not transacting against current market conditions. They are transacting against conditions that have already moved.

Forward-to-prompt represents the multi-day carry decision: rolling a position from a forward date toward a specific approaching prompt. As the forward date converges on the cash or prompt date, each individual date-to-date spread must be evaluated using real-time broker-sourced pricing. A five-day forward-to-prompt roll requires precision across five consecutive spread data points, each one subject to the same latency risk as the Tom-Next itself.

According to commodity carry-cost analytics research commodity trading risk management literature, a 5-day forward-to-prompt roll on a 1,000-tonne copper position using stale spread data can generate carry cost variance of $3,000, $15,000 per roll event depending on market backwardation depth and prompt date tightness. This forms a P&L line item driven directly by data architecture quality.

Translating Latency into Delivery Costs

Spread decision latency translates to delivery costs through a direct mechanism: a trader executing a Tom-Next or date-to-date roll at a price reflecting stale data is paying a premium the live market no longer justifies, or missing a discount the live market is currently offering. At scale, these variance events accumulate into measurable P&L drag that does not appear in any single transaction but compounds across an active physical trading book.

This practical exposure explains why major physical trading houses invest in direct LME ring broker connectivity rather than relying on aggregated market data platforms with normalization delays built into their data pipelines. The cost consequence is well understood by any desk that has audited its carry execution against live broker quotes.

Real-Time Defined: An Operational Specification for Metals Data

In market data, "real-time" is frequently asserted without operational precision. Every platform claims it. Few define it to a measurable engineering standard. For physical metals trading, real-time has a specific technical meaning that must be stated as a strict specification.

Defining Real-Time for Metals Trading Data

For physical metals trading, real-time means broker-consistent bid/ask data delivered with sub-5-second latency during active LME ring sessions and the inter-office market. It means the spread shown in a trading platform must match (within defined tolerance) the spread a ring broker would quote on a live call at that exact moment. Any divergence between platform-displayed spread and broker-quoted spread is a data quality failure with quantifiable cost consequences.

This definition excludes three data architectures that platforms routinely and incorrectly label as real-time:

- Aggregated mid-price feeds with normalized 15, 30 second update cycles that smooth volatility and eliminate the precision a prompt-window decision requires

- End-of-ring snapshot data presented as intra-session pricing, which reflects where the market was at the close of a ring, not where it is in the inter-office market between sessions

- Delayed exchange feeds with vendor-side normalization buffers that introduce latency before data reaches the platform display layer

According to a 2022 Coalition Greenwich industry report [LINK: Coalition Greenwich commodities data research], 67% of commodity traders using multi-asset platforms reported that displayed bid/ask spreads diverged from broker-quoted spreads by more than 10 basis points during high-volatility sessions. That divergence does not remain in the data layer. It transfers directly into execution quality and carry cost outcomes.

The operational standard for physical metals data is not "as fast as possible." It is "broker-consistent during prompt windows." This precision requirement demands direct market connectivity, not downstream data aggregation passed through a generic normalization pipeline.

Broker-Consistent Pricing and Its Role in Physical Metals Trading

Broker-consistent bid/ask data is the reference standard against which all physical metals spread decisions must be validated. This is an architectural requirement driven by how the LME market functions.

The LME operates through a ring of Category 1 member firms LME member categories who provide primary liquidity in the inter-office market. The bid/ask spread quoted by these ring dealers is the reference against which physical traders execute date-to-date carries, Tom-Next rolls, and forward-to-prompt decisions. The inter-office market accounts for approximately 70% of total LME daily volume LME annual statistics, with the majority of that activity concentrated in the daily carry and spread market. This is the exact segment where physical metals data quality carries the greatest cost consequence.

The operational consequence is direct and calculable. A trader executing a 500-tonne zinc Tom-Next roll using platform spread data that diverges from the live broker market by $2/t has not transacted at the best available price. They have transacted at a price that existed 30, 90 seconds prior. In a tight prompt market, that divergence represents $1,000 in avoidable carry cost on a single roll event. Across a quarter of active rolling activity, these events accumulate into a systematic carry efficiency deficit.

According to commodity trading execution quality research commodity execution quality research, systematic spread data divergence of 5, 10 basis points costs active physical trading desks an estimated 8, 15 basis points in annual carry efficiency. This drag compounds directly with position size and roll frequency.

Data architecture for physical metals is therefore a first-principles engineering specification. A platform either sources data directly from the broker market, or it introduces a latency gap with a quantifiable cost consequence. The distinction between those two architectures is well-defined and measurable.

Why Legacy Platforms Fail the Physical Metals Latency Test

Legacy multi-commodity platforms fail physical metals traders on data latency for a structural reason: they were not built around the LME's daily prompt date structure or the broker market's live pricing dynamics.

Generic CTRM/ETRM platforms treat metals data as equivalent to energy or agricultural commodity data: a single prompt, exchange-settled, with normalized price feeds sufficient for position valuation. This architectural assumption is correct for those markets and demonstrably incorrect for LME-traded physical metals. These platforms were built to solve a different problem and adapted, rather than designed from the LME's actual mechanics.

The failure manifests in three specific and consistent patterns:

- Position valuation using end-of-day or delayed intra-day prices: Acceptable for mark-to-market accounting, insufficient for live spread execution decisions during a 48-hour prompt window where conditions change within minutes.

- Spread calculation using synthetic mid-prices: Algorithmically derived from bid and ask without confirming against broker-sourced data, creating a systematic divergence that worsens precisely when market volatility is highest.

- Prompt date handling that treats all forward dates equivalently: Failing to apply higher data precision requirements as the prompt window approaches, at the exact moment when that precision carries the greatest cost consequence.

According to a 2023 Accenture Commodity Trading survey Accenture CTRM market research, 43% of physical commodity traders identified inaccurate or delayed spread data as a primary driver of manual workarounds in their trading workflow. These workarounds (mid-session calls to brokers, manual Bloomberg terminal cross-checks, spreadsheet verification layers) represent the measurable cost of a platform that cannot meet the physical metals data specification.

Every manual verification step introduces human latency into a decision the platform should resolve automatically and accurately. In a 48-hour prompt window across an active physical book, those steps accumulate into systematic execution degradation that quantifies directly into carry P&L, and does not appear as a platform deficiency in any vendor's product review.

The Depth-First Standard for Physical Metals Data Architecture

The architectural case for physical metals data focuses on building data infrastructure that understands the specific pricing structure of the LME, and treats broker-consistent, prompt-window precision as a strict, non-negotiable specification.

Depth-first metals platform design starts from this requirement: the platform must deliver broker-consistent bid/ask data during all LME ring sessions and the inter-office market, with specific precision requirements applied during the 48-hour approach to any prompt date on a trader's active book.

This translates into four concrete architectural requirements:

- Direct broker connectivity rather than downstream aggregated feeds that introduce normalization delay between the market and the trader's display

- Prompt-date-weighted data refresh logic that increases validation frequency as the prompt window narrows, applying the highest precision where cost sensitivity is highest

- Real-time spread validation comparing platform-displayed data against broker-sourced reference prices with defined divergence tolerance thresholds that trigger alerts before execution

- Automated carry cost calculation using live Tom-Next and date-to-date spreads (not end-of-session averages or synthetic mid-prices) so roll decisions are evaluated against current market conditions

The Novaex platform was designed to this specification, developed from four years of active front-office metals trading before a single line of platform code was written. That foundation established a clear gap between what physical metals traders require and what multi-commodity platforms deliver. This represents a structural architectural gap.

According to Oliver Wyman commodity trading research [LINK: Oliver Wyman commodity trading technology], firms achieving tight data-to-decision integration in carry and spread execution reduce systematic carry cost drag by 12, 18% annually. This figure translates directly into bottom-line P&L improvement for physical trading desks operating at scale, without changing strategy or risk appetite.

Novaex platform architecture overview

Conclusion: A Specification, Not a Preference

Physical metals trading data latency operates as a strict cost engineering specification with direct, non-recoverable delivery consequences. The prompt date window demands broker-consistent, real-time bid/ask precision because the financial outcomes of spread decisions in that window are immediate, calculable, and tied directly to physical delivery mechanics that tolerate no abstraction.

The distinction between a financial trader's latency tolerance and a physical metals trader's precision requirement follows from first principles. Different settlement mechanics, different delivery obligations, different cost consequence structures, and different data specifications. These distinctions are technical in nature, derived from physical settlement mechanics, and the data architecture required to meet them is well-defined.

Three immediate steps for physical metals trading desks:

- Audit your current platform against live broker quotes during your next prompt approach. Measure the actual spread divergence under real conditions rather than vendor-provided benchmark scenarios.

- Document every manual verification step your team takes during prompt windows. Each call to a broker and each Bloomberg cross-check acts as a quantifiable measure of your platform's data gap.

- Evaluate whether your CTRM/ETRM platform's data architecture was designed for LME prompt date structure or adapted from a generic commodity data model that treats all forward dates as equivalent. The answer determines whether your carry cost drag is recoverable.

Schedule a Novaex platform demonstration to see broker-consistent physical metals data applied to live prompt date scenarios, and evaluate the depth-first data architecture standard against what your desk currently relies on.