MCX Copper vs SHFE Copper: Curve Divergence Explained

MCX copper and SHFE copper are not localized versions of the same instrument. Each exchange carries distinct structural premiums (driven by denomination effects, warehousing rules, and delivery specifications) that diverge significantly from one another and from LME copper. Applying a single global copper price across both venues produces systematic mispricing. This post documents the mechanics of that divergence with quantifiable evidence.

The premium differential between the two exchanges is observable as a chart and traceable to specific structural variables: India's import parity pricing regime, INR denomination effects, China's VAT treatment, bonded warehouse inventory mechanics, and RMB financing trade economics. Understanding each exchange on its own terms is a prerequisite for managing cross-venue copper exposure with precision.

Why MCX and SHFE Copper Require Separate Curve Frameworks

The default assumption in multi-commodity analytics; that LME copper provides a global benchmark from which all other copper prices derive via simple basis adjustment; fails operationally. MCX copper and SHFE copper each embed structural premiums that cannot be explained or predicted from the LME curve alone.

According to the World Bureau of Metal Statistics, global refined copper consumption reached approximately 26 million metric tons in 2023, with China accounting for roughly 55% of that total and India representing the fastest-growing demand center outside Asia. These two markets operate through distinct exchange mechanisms, regulatory frameworks, and delivery infrastructures that imprint themselves directly on futures curve shape.

LME copper basis vs MCX and SHFE historical spread

This structural divergence provides valuable market signal. When the MCX copper front-month basis to LME copper widened to approximately 4, 6% in late 2022 during periods of INR depreciation, traders operating from a uniform global copper price were either leaving premium on the table or absorbing unintended currency risk. The same mechanism plays out on SHFE copper when domestic bonded warehouse stocks shift relative to exchange-registered inventory.

Each exchange requires its own analytical framework.

The Limits of LME as a Universal Copper Benchmark

LME copper is a Grade A cathode contract priced in USD with global delivery points. MCX and SHFE each introduce local demand conditions, currency regimes, and physical delivery specifications that LME pricing does not capture. The basis to LME fluctuates as a variable driven by exchange-specific structural factors that require dedicated curve analysis, not a scalar adjustment applied uniformly across venues.

MCX Copper: Import Parity, INR Denomination, and Delivery Mechanics

MCX (Multi Commodity Exchange of India) copper futures are denominated in Indian Rupees per kilogram. The contract specifies Grade A electrolytic copper cathode conforming to IS:191 or BS:6017 standards, with delivery at MCX-approved warehouses across India including Mumbai, Delhi, Chennai, and Kolkata.

The critical pricing input for MCX copper is import parity pricing. India is a net importer of refined copper, which means the domestic physical price anchors to LME copper plus ocean freight, insurance, import duty (currently 5% on refined copper cathode under India's tariff schedule), GST at 18%, and port handling costs. According to India's Ministry of Commerce, India imported approximately 580,000 metric tons of refined copper in FY2023, making its futures market structurally tied to import-linked pricing rather than domestic mine production economics.

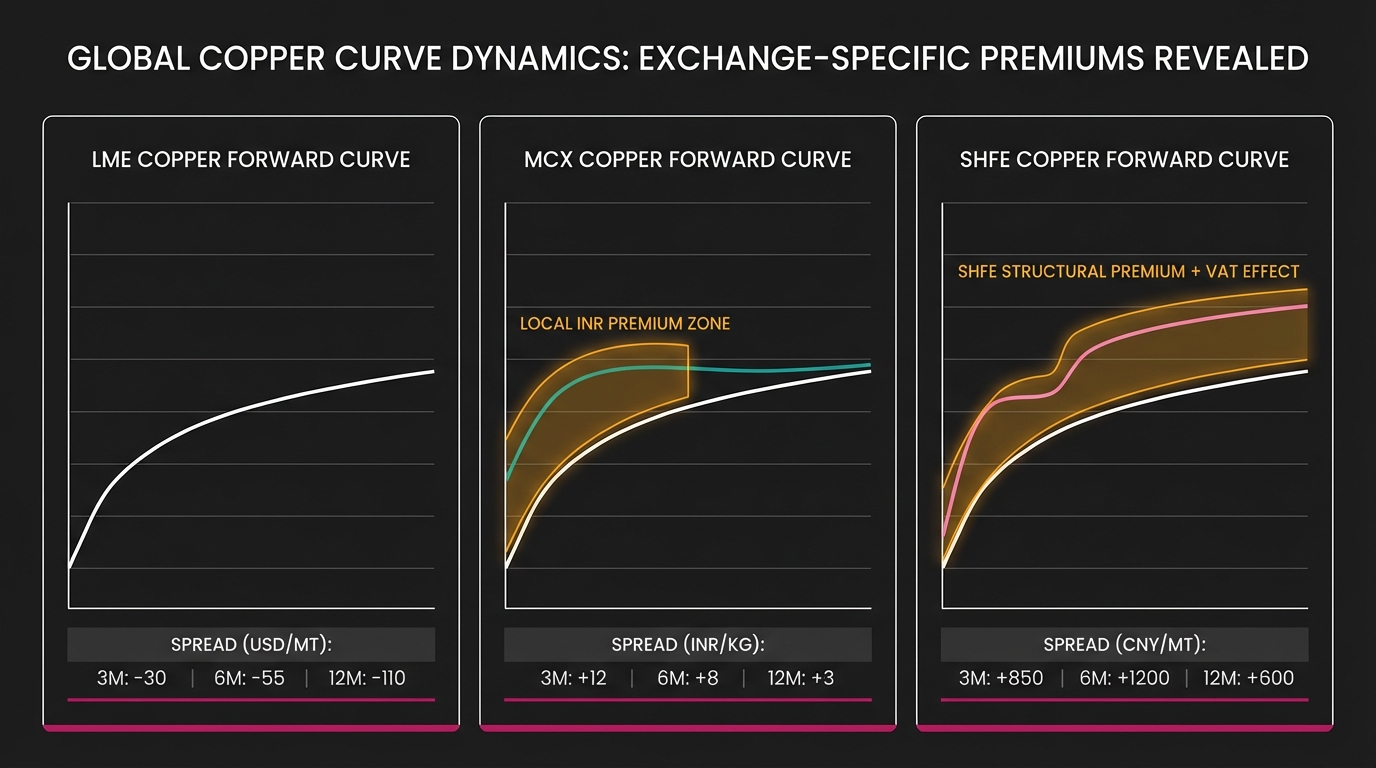

This import parity structure creates a persistent structural premium in the MCX curve. When LME copper is at $9,000/MT, the corresponding MCX price in INR/kg reflects LME base price converted at USD/INR spot, import duty at approximately 5% on CIF value, GST at 18% on assessable value, ocean freight and insurance at approximately $80, 120/MT depending on origin, and port and handling costs at approximately $30, 50/MT equivalent.

The aggregate import parity premium has historically ranged between 8, 14% above LME copper in INR terms. That range is not static. It compresses when domestic supply is adequate and widens when port congestion, currency depreciation, or tariff adjustments intervene.

The Impact of INR Depreciation on MCX Copper Pricing

INR depreciation increases the MCX copper price in rupee terms without any change in LME USD pricing. A 5% depreciation in USD/INR translates directly into a 5% increase in MCX copper's INR base before duties and taxes are applied, compounding the import parity effect. According to Reserve Bank of India data, the INR depreciated approximately 8.3% against the USD between January 2022 and December 2022, contributing materially to MCX copper's outperformance versus LME copper on a local-currency basis during that period.

This currency transmission mechanism means MCX copper curve analysis requires an embedded FX view. A trader hedging Indian copper exposure on MCX without explicitly modeling INR volatility is carrying unquantified basis risk; risk that does not appear in an LME-equivalent copper P&L.

MCX Copper Delivery Specifications

MCX specifies delivery of Grade A electrolytic copper cathode (IS:191/BS:6017 compliant) in lot sizes of 1 MT. The exchange maintains a Quality Premium/Discount schedule for off-spec deliveries. Warehouse vault receipts are transferable within the MCX system, but the physical logistics of Indian warehouse operations differ substantially from LME warrant mechanics. Warehouse queue risks and domestic logistics costs can create temporary disconnects between MCX futures prices and physical prices at specific delivery points, a microstructure variable that has no LME analog.

SHFE Copper: RMB Denomination, Bonded Warehouse Mechanics, and VAT Effects

SHFE (Shanghai Futures Exchange) copper futures are denominated in Chinese Yuan (RMB) per metric ton. The contract specifies Grade A standard copper cathode conforming to GB/T 467-2010 (Standard Grade Cu-CATH-1), delivered at SHFE-registered warehouses located domestically within China including Shanghai, Guangdong, Jiangsu, and Zhejiang.

SHFE copper is the world's largest copper futures market by volume. According to SHFE exchange data, average daily volume in copper futures regularly exceeds 200,000 contracts, representing notional turnover comparable to aggregate global LME volumes. The structural premium in SHFE copper is driven by three distinct mechanisms that operate simultaneously and interact with each other.

Mechanism 1: VAT Inclusion in SHFE Copper Pricing

SHFE copper prices are quoted inclusive of China's 13% Value Added Tax. This is the single most mechanically important difference between SHFE and LME copper pricing. A naive USD/RMB conversion of SHFE copper to LME copper will overstate the SHFE price by 13% unless VAT is stripped first. Any spread analysis between the two exchanges is analytically invalid without this adjustment.

Mechanism 2: Bonded Warehouse vs. Domestic Inventory Split

China maintains two distinct copper inventory pools: exchange-registered domestic warehouse stocks (VAT-paid, reflected in official SHFE inventory data) and bonded warehouse stocks in the Shanghai Free Trade Zone (VAT-deferred, not reflected in SHFE warrant data). According to Shanghai Metals Market (SMM) data, bonded copper stocks have at times exceeded 500,000 MT. This shadow inventory position affects spot premiums without appearing in SHFE official numbers.

Mechanism 3: RMB Financing Trade Economics

SHFE copper has historically served as a financing vehicle in China. Traders import copper, pledge it as collateral for RMB loans, and reinvest proceeds, effectively a carry trade funded by the USD/CNY interest rate differential. According to Bank for International Settlements estimates, copper financing deals in China have at times represented 20, 40% of total bonded copper inventory. This financing demand creates a premium structurally unrelated to physical supply-demand fundamentals and entirely absent from the MCX copper curve.

Drivers of the SHFE Copper Premium Over LME

After VAT adjustment and USD conversion, SHFE copper has historically traded at a premium of $50, $200/MT to LME copper during periods of strong Chinese domestic demand. This premium reflects domestic demand pull, logistics costs for delivering copper into China's physical market, and the financing component embedded in SHFE prices. The premium narrows or inverts during periods of demand weakness or Chinese credit tightening, neither of which has a direct parallel in MCX copper pricing dynamics.

SHFE Warehousing Rules vs. LME Warrant Mechanics

SHFE warehouse receipts are non-transferable outside the SHFE system and are specific to registered domestic warehouses, unlike LME warrants, which are globally transferable instruments. SHFE receipts cannot be used for delivery in other jurisdictions. Location premiums and discounts apply based on proximity to consumption centers, and queue dynamics at SHFE Shanghai warehouses can create intraday basis dislocations that must be monitored independently from the outright price. The mechanics of holding, transferring, or canceling SHFE receipts introduce operational risks with no LME equivalent.

Measuring the Structural Premium Divergence Between MCX and SHFE Copper

The MCX-SHFE copper spread requires multi-step normalization before it becomes analytically usable. Raw price comparison produces a number; normalized comparison produces a tradeable signal.

Step 1: VAT Adjustment for SHFE

Divide SHFE copper price by 1.13 to strip VAT. This produces the pre-tax SHFE price on a comparable ex-tax basis.

Step 2: Currency Normalization

Convert both prices to USD/MT using contemporaneous USD/INR (for MCX) and USD/CNY (for SHFE) spot rates. Apply reverse import duty adjustments to strip MCX's duty-inclusive pricing back to a CIF equivalent.

Step 3: Quality and Specification Alignment

Both MCX (Grade A, IS:191) and SHFE (Cu-CATH-1, GB/T 467-2010) specify copper of ≥99.95% purity, broadly equivalent to LME Grade A copper cathode. No material quality premium or discount adjustment is required between the two.

Step 4: Logistics and Insurance Normalization

Apply estimated freight differentials based on relevant shipping routes (Chilean or Zambian cathode to Indian ports versus to Chinese ports) to build a comparable CIF basis for both exchanges.

After this normalization, the residual spread between MCX and SHFE copper represents the structural premium divergence attributable to differential demand intensity between China and India, exchange-specific financing effects (SHFE financing premium versus the absence of financing demand in MCX), inventory regime differences (SHFE bonded overhang versus MCX import-driven scarcity), and local regulatory factors including Indian import duty changes and Chinese credit conditions.

In 2022, this normalized residual spread ranged from approximately -$80/MT to +$180/MT, with the SHFE premium to MCX expanding sharply during Q1 2022 as Chinese post-lockdown restocking demand accelerated, then compressing through Q3 2022 as SHFE inventory rose and Indian import demand remained constrained by INR weakness. This is a substantial spread that cannot be managed with a single global copper price.

Curve Shape Divergence: Contango, Backwardation, and Term Structure

The spread analysis above addresses the spot-month basis. The divergence extends across the full forward curve, and the term structure signals are not synchronized between the two exchanges.

SHFE copper term structure reflects Chinese credit conditions, domestic seasonal demand (construction activity peaks in spring and autumn), and financing trade economics. SHFE copper frequently shows mild contango in its front three months (reflecting financing costs and warehousing charges) before flattening, with occasional sharp backwardation during periods of acute domestic tightness.

MCX copper term structure reflects Indian import economics. Because India imports on a CIF basis at rolling spot-plus-premium prices, the MCX forward curve tends to embed a rolling import cost premium that increases monotonically across tenors when the INR is in secular depreciation. During periods of INR stability, the MCX curve flattens considerably, independent of any change in the SHFE curve shape.

According to analysis from base metals desks at major trading houses, the correlation between SHFE copper 3-month futures and MCX copper 3-month futures (both converted to USD) has ranged between 0.72 and 0.88 over rolling 12-month windows. That is high enough to confirm co-movement driven by the common LME anchor but low enough that treating them as the same instrument introduces basis risk of 200, 400 basis points in active hedge periods.

Reading MCX and SHFE Curve Shape as Independent Signals

MCX copper curve steepness is a signal about expected INR depreciation and Indian import demand trajectory, not about global copper supply. SHFE copper curve shape signals Chinese domestic demand intensity, credit conditions, and bonded inventory incentives. Reading either curve through the other's lens produces misattributed signals. The curve shapes carry different information because the markets they represent have different structural drivers.

Operational Implications for Cross-Venue Copper Hedging

For a front-office metals trader managing copper exposure across Indian and Chinese markets simultaneously, the analytical implications are direct and immediate.

Position-Level Basis Tracking

A long MCX copper physical position hedged on SHFE copper futures is not a clean hedge. The MCX-SHFE residual spread documented above, ranging from -$80 to +$180/MT normalized, represents unhedged basis risk that must be tracked at the position level as a standalone metric. Analytics platforms that roll all copper positions into a single LME-equivalent bucket do not simplify this risk. They obscure it, leaving the trader to absorb it through unexplained P&L variance.

copper cross-venue basis risk management

Rolling Methodology

MCX copper lot sizes (1 MT) and SHFE copper lot sizes (5 MT) require different roll strategies. SHFE active contract months (January, March, May, July, September, November) do not align perfectly with MCX active months, creating roll-date basis risk that must be modeled explicitly rather than assumed away.

Real-Time Data Requirements

The MCX-SHFE structural premium divergence is not static. It moves intraday as USD/INR and USD/CNY rates update, as SHFE inventory reports publish (daily, 6:00 PM Shanghai time), and as MCX warehouse receipt data refreshes. According to front-office workflow surveys conducted by Commodity Technology Advisory (ComTech Advisory), 68% of base metals traders cite data fragmentation as the primary source of manual reconciliation work during high-volatility periods, which is precisely when basis tracking matters most.

real-time multi-exchange copper data integration

Required Data Inputs for Tracking the MCX-SHFE Copper Spread

Minimum required inputs for live MCX-SHFE copper spread tracking are: MCX copper front-month and term prices in INR/kg, SHFE copper active contract prices in RMB/MT, USD/INR and USD/CNY real-time FX rates, SHFE daily warehouse inventory (domestic and bonded separately), MCX approved warehouse stock levels, and current Indian import duty and GST schedules. Any platform that cannot integrate all six data streams simultaneously cannot produce a valid MCX-SHFE spread in real time. It can only produce an approximation, and approximations carry silent basis risk.

Building an Exchange-Specific Copper Intelligence Framework

The evidence documented above supports one operational conclusion: MCX copper and SHFE copper require independent curve models with exchange-specific parameters, not shared inputs derived from an LME template.

A depth-first approach to copper analytics builds the complete instrument profile for each exchange before attempting cross-venue comparison. The model architecture required for each is distinct.

MCX Copper Model Inputs:

- LME copper USD price (base anchor)

- USD/INR spot and forward curve

- Indian import duty schedule (currently 5% on refined cathode)

- GST rate (currently 18%)

- CIF freight estimates for Chile/Zambia to Indian ports

- Domestic MCX warehouse stock levels by location

- Indian seasonal demand patterns (construction, electrical, auto sectors)

- LME copper USD price (base anchor)

- USD/CNY spot and forward curve

- VAT rate (currently 13%)

- Bonded warehouse stocks (SMM data, separate from SHFE registered)

- SHFE domestic registered inventory by warehouse location

- Chinese credit conditions proxy (shadow banking activity, CNY credit impulse)

- Financing trade economics (USD/CNY rate differential, copper import premium)

These two models produce independent curve outputs. Cross-venue spread analysis then operates on the normalized outputs, not on raw price feeds. According to Novaex's internal exchange specification database, there are at least 14 distinct structural variables that differentiate the MCX copper curve from the SHFE copper curve. Platforms that collapse these into a single global copper curve do not simplify the problem. They transfer the analytical burden to the trader as manual reconciliation work, arriving exactly when markets are moving fastest and manual effort is most costly.

The front-office trader managing both Indian and Chinese copper exposure needs a platform that has already done this work. MCX curve intelligence and SHFE curve intelligence must exist as separate, complete analytical modules with exchange-specific inputs, not as fields in a generic multi-commodity template designed for breadth rather than depth.

Conclusion

MCX copper and SHFE copper are structurally distinct instruments with measurable, quantifiable premium divergences that cannot be reconciled by applying a single LME-based copper price. The MCX curve embeds Indian import parity economics and INR denomination effects. The SHFE curve embeds Chinese domestic consumption premiums, VAT mechanics, bonded warehouse inventory dynamics, and financing-driven demand. The normalized residual spread between the two ranged from -$80 to +$180/MT in recent years. This $260/MT range represents material basis risk for any cross-venue copper hedge operating without exchange-specific curve intelligence.

Three immediate steps for traders managing both MCX and SHFE copper exposure:

- Build VAT-adjusted, duty-stripped spread tracking for the MCX-SHFE basis as a standalone risk metric (not as a residual to the LME curve) and monitor it with the same discipline as outright price risk

- Separate curve analysis by exchange with exchange-specific model inputs, monitoring SHFE bonded inventory and MCX warehouse receipts as independent data streams on their own publication schedules

- Audit your platform's exchange specification depth. If your analytics layer cannot demonstrate exchange-specific structural variables for MCX and SHFE copper independently, the basis risk is being absorbed silently into your P&L

Novaex was built on the premise that every market deserves complete analytical treatment before a platform can reliably claim to cover it. For copper, that means MCX curve intelligence and SHFE curve intelligence developed independently. Each must be complete on its own terms, traceable to exchange-specific fundamentals, and never reduced to a local footnote on the LME benchmark. That is the depth-first standard, and it is the standard that produces reliable cross-venue copper intelligence.