Spreadsheet Risk in Metals Trading Is Not Background Noise

Spreadsheet-based workflows for LME, MCX, COMEX, and SHFE pricing data carry three documented risk categories: execution latency, data integrity failure, and governance gaps. Most metals trading teams classify these as unavoidable operational background noise. Each is traceable to specific workflow conditions with measurable financial and compliance exposure, and that misclassification is the documented operational condition this analysis examines.

According to the European Spreadsheet Risks Interest Group (EuSpRIG), 88% of spreadsheets contain at least one material error. For most metals trading operations, that statistic is routinely absorbed into operational routine rather than treated as a documented risk condition requiring a structured response. The normalization of spreadsheet risk in metals trading represents a documentable gap between acknowledged error rates and the operational standards those error rates require.

The following sections name the specific failure modes embedded in manual pricing workflows (execution, integrity, and governance) and establish the standard against which those risks should be classified.

Why Spreadsheet Risk in Metals Trading Gets Misclassified

The normalization of spreadsheet risk is a rational response to an environment where credible, depth-first alternatives were not clearly accessible.

For years, the realistic alternatives to manual pricing workflows were multi-commodity platforms promising broad coverage across base metals, energy, and agricultural markets, but delivering generalized intelligence thinly distributed across dozens of instruments. A platform that covered LME, MCX, COMEX, and SHFE at a surface level offered less operational value than a spreadsheet model tunable to a specific workflow, even one carrying structural error risk.

Under those constrained conditions, spreadsheet-based workflows held a functional advantage on flexibility and cost. The associated risk appeared fixed, a structural cost of doing business rather than a documentable, addressable operational gap.

Prevalence is not a risk assessment

The prevalence of a practice does not change its risk profile. Research by Raymond Panko at the University of Hawaii, examining spreadsheet use across two decades of organizational audits, found that between 20% and 40% of spreadsheet models contained material errors affecting decision outputs.

In a trading context, "material errors affecting decision outputs" mean pricing, hedging ratios, position exposure, or margin calculations carrying incorrect values into execution decisions. The industry-wide normalization of that error rate represents a systemic misclassification, not a documented standard of acceptable operational practice.

Accepting a known failure rate as background noise does not reduce the failure rate. It removes the organizational attention required to address it.

Execution Risk: How Spreadsheet Latency Costs Real Money in Metals Trading

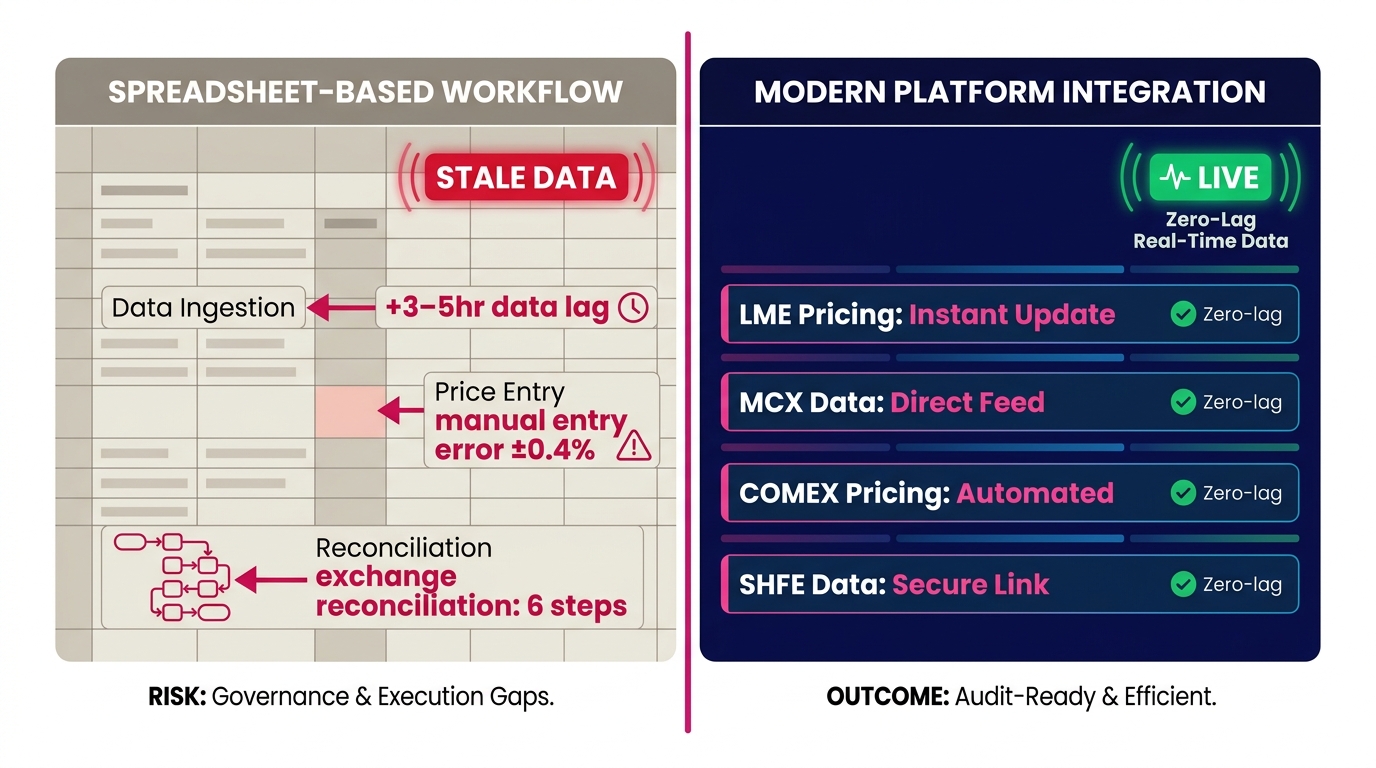

Execution risk in spreadsheet-based metals workflows is rarely a single catastrophic failure. It is the cumulative cost of latency, the time gap between when a price moves on LME, MCX, COMEX, or SHFE and when a trader has an accurate, reconciled number to act on.

LME three-month copper can move $20, $30 per metric ton within a single session on a supply disruption or macro catalyst. At 100 metric tons of exposure, a 15-minute data lag during that move represents $2,000, $3,000 in execution slippage per position per event. That figure compounds across positions, sessions, and a full trading year without appearing as a single attributable loss event in a P&L review.

The impact of spreadsheet latency on metals hedging

Spreadsheet latency affects metals hedging decisions by requiring traders to act on stale reference prices during volatile sessions. The result is hedge execution at prices that diverge from the intended entry point, creating basis risk that was not budgeted and cannot be cleanly attributed to market movement rather than workflow failure.

This is operationally distinct from market risk. Market risk is accepted as part of a trading mandate. Spreadsheet-generated execution slippage is operational overhead misclassified as market exposure, absorbing P&L without triggering the review that would trace its actual origin.

The manual update cycle as a compounding failure mode

Each manual update step in a spreadsheet workflow introduces an independent failure probability. Pulling LME official prices, MCX spot data, COMEX settlement figures, and SHFE closing prices into a single working model typically requires four to six discrete import or copy-paste operations per session.

EuSpRIG's documented case analysis identifies copy-paste errors as the most frequent single source of spreadsheet-related trading losses. The 2003 TransAlta energy incident (where a copy-paste error in a bid spreadsheet produced a $24 million loss on a single power contract transaction) is the most-cited public example. spreadsheet errors in commodity trading history Comparable failures in private metals trading operations are rarely disclosed and rarely attributed to their actual operational origin.

Each manual step introduces a documented failure probability applied repeatedly across every trading session for the duration of the workflow.

Data Integrity Failures: The Governance Gap in Spreadsheet Workflows

Execution risk surfaces in P&L. Data integrity risk is harder to locate because spreadsheets can display numbers that differ from underlying market data.

Causes of data integrity failures

Data integrity failures in commodity trading spreadsheets occur when pricing sources, formula logic, or version states diverge across files, users, or sessions without a reconciliation checkpoint. A trader working from an LME pricing model last refreshed before a ring session has closed is operating on an incorrect basis, but nothing in the spreadsheet's visual presentation signals that condition.

This is the structural problem: spreadsheets present numbers with uniform visual confidence regardless of whether those numbers reflect current market state. A cell displaying $9,240 per metric ton looks identical whether it was populated from a live feed 30 seconds ago or from a manual entry made three sessions prior.

In multi-exchange workflows covering LME, MCX, COMEX, and SHFE simultaneously, the divergence risk multiplies rather than adds. Each exchange operates with distinct settlement timing, price types (official, closing, settlement, spot) and session structures that do not align. A model correctly capturing LME official prices may systematically apply COMEX closing prices where SHFE settlement values are required, producing outputs that appear internally consistent without being externally accurate.

According to a study published in the Journal of Organizational and End User Computing, 94% of spreadsheets examined in post-event audits contained errors significant enough to affect the decision outputs they were designed to support. spreadsheet error research in financial workflows The operative word is "post-event." These errors were identified only after a failure created sufficient organizational pressure to trigger a review.

Pre-event, they were classified as background noise.

Auditability and Compliance: What Spreadsheet-Based Workflows Cannot Document

Governance risk in metals trading extends beyond calculation accuracy. It includes the capacity to reconstruct, at any point in time, exactly what price inputs supported a specific trading or hedging decision, and to demonstrate that those inputs were sourced appropriately and applied consistently.

Regulatory frameworks governing commodity trading, including CFTC requirements for swap dealers and commodity pool operators, MiFID II obligations in European markets, and exchange-specific position reporting standards, increasingly require firms to demonstrate that pricing data used in trade execution was current, sourced from a recognized provider, and applied consistently across positions and time periods. [LINK: CFTC record-keeping requirements for commodity traders]

How spreadsheets create compliance gaps

Spreadsheets create compliance gaps in commodity trading because they do not natively record when data was entered, who entered it, what source was referenced, or whether the version in use at the moment of a specific decision was the version that was later saved, shared, or modified.

A spreadsheet updated after a trade is executed (even to correct a factual error) overwrites the data state that existed at the moment of decision. Without version-controlled audit trails, that reconstruction is structurally unavailable. The CFTC's enforcement history includes cases where firms could not produce contemporaneous records of the pricing basis for hedging decisions, with enforcement actions predicated on documentation failures rather than intentional misconduct.

The multi-user version control problem

Metals trading teams operating across time zones (managing positions against LME London sessions, SHFE Shanghai opens, and COMEX New York closes) often distribute spreadsheet models across multiple users in multiple locations. Each user's copy can diverge from every other user's copy without any system-level mechanism to detect, flag, or timestamp that divergence.

According to PwC's Global Economic Crime and Fraud Survey, operational control failures, including data governance gaps, account for a material share of commodity trading losses that are publicly attributed to market conditions but trace operationally to documentation and data management failures. PwC commodity trading operational risk report The governance exposure does not require a regulatory inquiry to become consequential. It is present from the moment the undocumented practice begins.

How Spreadsheet Risk Compounds Across LME, MCX, COMEX, and SHFE

A metals trading operation hedging across multiple exchanges does not experience spreadsheet risk additively. It experiences it multiplicatively.

Each exchange introduces distinct pricing conventions, lot sizes, currency denominations, and settlement mechanics that require precise, consistent conversion logic. LME aluminum is priced in USD per metric ton with a unique prompt date structure. MCX aluminum is priced in INR per kilogram with domestic delivery specifications. COMEX copper uses USD per pound with its own futures contract structure. SHFE prices in CNY per metric ton with delivery grades and specifications that differ materially from LME standards.

A spreadsheet model converting across these conventions introduces at least four categories of compounding error risk:

- Currency conversion timing mismatch: applying the prior session's FX rate to a current SHFE CNY price, creating a conversion error that scales linearly with position size

- Unit conversion errors: applying per-pound COMEX logic to per-metric-ton LME positions, a structural formula error that can persist without detection through multiple trading cycles

- Settlement date misalignment: comparing LME cash prices against COMEX spot when the active hedging instrument is a three-month forward, creating a tenor mismatch that distorts hedge effectiveness calculations

- Session overlap miscapture: using pre-session reference prices for a market that has already moved materially on the day, particularly acute during SHFE opens that precede LME ring sessions

The normalization of spreadsheet risk

Metals trading teams normalize spreadsheet risk because the failures are typically not visible in real time. Errors affecting hedging ratios or pricing basis generally surface in reconciliation, sometimes days after positions have been adjusted or closed, making attribution difficult and P&L impact diffuse.

By the time reconciliation flags a discrepancy, the connection to its operational origin in a specific spreadsheet workflow step has been obscured by subsequent market movement and position management. The loss is absorbed into general book variance rather than traced to a documentable, preventable workflow condition. That delayed attribution cycle is the structural mechanism of normalization.

The Organizational Cost of Spreadsheet Risk in Metals Trading

When spreadsheet risk in metals trading is classified as background noise rather than a documented operational liability, it does not remain static. It compounds with trading volume, headcount, and workflow complexity.

According to Gartner research, poor data quality costs organizations an average of $12.9 million annually across industries. In commodity trading, where the economic density of individual decisions significantly exceeds most business contexts, the cost per data quality failure scales accordingly and concentrates in ways that aggregate risk metrics do not capture. Gartner data quality cost research

The organizational cost of spreadsheet risk in metals trading operates across three compounding dimensions:

- Direct financial cost: execution slippage, hedging basis errors, and reconciliation-driven position corrections that absorb P&L without traceable attribution to their operational cause

- Operational overhead cost: the time cost of manual data entry, error correction cycles, and cross-user version management that displaces the analytical work that generates trading edge

- Governance cost: the latent compliance and audit exposure created by undocumented pricing workflows, quantified only at the moment of a regulatory inquiry, counterparty dispute, or internal control review

The true cost of spreadsheet errors

The true cost of spreadsheet errors in metals trading is not captured by the direct P&L impact of identified mistakes. It includes the hedging decisions made on incorrect inputs that produced acceptable outcomes, decisions that built organizational confidence in a flawed process, increasing the probability of future failures and making them systematically harder to detect.

This is the compounding mechanism that makes normalized spreadsheet risk particularly consequential in a trading context: it generates false confidence signals alongside real operational failures, producing a total risk profile that is structurally underestimated at every management review interval. A workflow that has not produced a visible, attributable failure remains unaudited rather than validated.

From Risk Normalization to Documented Operational Standard

The path from spreadsheet risk normalization to a documented operational standard does not begin with a platform replacement decision. It begins with a change in how the risk is categorized internally, moving from implicit acceptance to explicit documentation.

The first step is specific documentation of the failure modes present in active pricing workflows, including:

- Which data sources feed the model, and when they were last updated relative to the position decisions they supported in a given session

- Which formula chains involve manual inputs, and how frequently those inputs have been verified against primary source data

- What version control and access logging currently exists, and whether it would satisfy a regulatory reconstruction request under CFTC or MiFID II standards

Replacing spreadsheet-based metals pricing workflows

Effective infrastructure for metals pricing workflows delivers three capabilities that spreadsheets structurally cannot provide. First, they enable real-time data ingestion from LME, MCX, COMEX, and SHFE with timestamped, source-attributed price records. Second, they maintain a version-controlled position and calculation history that satisfies regulatory audit reconstruction requirements. Finally, they feature integrated hedge analytics that apply consistent pricing logic across exchange conventions without manual conversion steps.

The standard requires operational infrastructure matched to the documented risk profile of a multi-exchange base metals trading operation. This infrastructure treats every pricing decision as a recorded, attributable event rather than an undocumented manual process dependent on individual operator precision.

LME pricing data integration for base metals trading

metals trading position management and risk analytics

CTRM platform for base metals hedging workflows

The Starting Point Is Reclassification

Spreadsheet risk in metals trading normalized under conditions where depth-first, operationally credible alternatives to manual workflows were not clearly available. That context is worth documenting accurately. It explains how the current operational state developed without attributing it to negligence or inadequate judgment.

It does not change the risk classification. The execution latency, data integrity failures, and governance gaps documented here are not hypothetical vulnerabilities. They are operational failure modes with documented precedents, traceable mechanics, and measurable costs that compound across LME, MCX, COMEX, and SHFE workflows without generating a single visible event that forces a structured review.

Three actions to take now:

- Audit one active spreadsheet model against the four compounding error categories identified above (currency conversion timing, unit conversion logic, settlement date alignment, and session state accuracy) and document the findings

- Map the current version control and data sourcing state for pricing inputs used in hedging decisions made in the last 30 days, and assess whether those records would satisfy a regulatory reconstruction request

- Review reconciliation exceptions from the last quarter and identify how many trace operationally to spreadsheet workflow conditions rather than market movement

Novaex base metals platform overview