LME Forward Curve & Calendar Spreads: Metals Reference

The LME forward curve encodes three signals simultaneously: financing cost, physical inventory tightness, and rollover exposure. For base metals traders managing hedge positions across copper, aluminium, zinc, and nickel, misreading any one layer produces basis leakage that compounds across the book. This reference documents the structural data, spread mechanics, and decision thresholds that front-office teams apply when evaluating tenor selection and roll timing.

The cash/3M spread, carrying charge formula, and cross-exchange basis are the three data layers that determine whether a hedge performs or leaks. Everything below is built from published LME, CME Group, and exchange-reported data.

Why the LME Forward Curve Structure Controls Hedge Performance

The forward curve acts as a real-time equilibrium between the cost of carrying physical metal and the premium buyers will pay for immediate delivery.

In a contango market, spot prices sit below forward prices. The market compensates holders for storage, financing, and insurance. In backwardation, spot prices exceed forward prices, signaling physical tightness severe enough that nearby delivery commands a premium over future delivery.

According to LME historical settlement data, the cash-to-3-month spread for copper has ranged from approximately -$1,100/tonne (October 2021 squeeze) to +$180/tonne during the COVID-driven demand collapse of 2020. [LINK: LME copper historical spread data] That $1,280/tonne range across 12 months is the quantitative case against static tenor assumptions in any actively managed book.

Tenor selection operates as a direct cost variable before functioning as a risk mechanism. A 3-month hedge on copper running in a $70/tonne contango market costs the hedger approximately $70/tonne in roll decay per contract cycle. Over a 12-month rolling program, that translates to $280/tonne in cumulative carry cost, a real cash outflow that must be priced into physical contracts before the hedge is placed.

Backwardation Mechanics for Physical Traders

Backwardation signals near-term physical supply shortages severe enough to override all financial carrying cost arguments. For a physical trader long spot copper, backwardation represents a direct P&L benefit: the inventory held commands an immediate-delivery premium the market is actively pricing into the cash spread.

For a trader running a short futures hedge against physical length, backwardation creates carry income if the short is rolled forward at a premium price. The inverse applies to a long futures hedge in backwardation: roll losses accumulate on every cycle until the curve normalizes.

The decision threshold matters operationally. Sustained cash/3M backwardation beyond -$50/tonne in copper has historically corresponded to LME registered warehouse stocks falling below 100,000 tonnes. LME warehouse stock data Below this inventory level, squeeze risk accelerates non-linearly and roll cost assumptions built into physical contracts break down.

LME Contract Reference: Lot Sizes, Tick Values, and Prompt Structure

Understanding tenor decisions begins with the mechanical specifications of each contract. The table below documents the operational parameters front-office teams reference daily.

LME Base Metals Contract Specifications

| Metal | LME Code | Lot Size | Min. Price Move | Prompt Date Granularity |

|-------|----------|----------|-----------------|--------------------------|

| Copper | CA | 25 mt | $0.50/mt ($12.50/lot) | Daily (1, 3M), Weekly (3, 6M), Monthly (7, 63M) |

| Aluminium | AH | 25 mt | $0.50/mt ($12.50/lot) | Daily (1, 3M), Weekly (3, 6M), Monthly (7, 63M) |

| Zinc | ZS | 25 mt | $0.50/mt ($12.50/lot) | Daily (1, 3M), Weekly (3, 6M), Monthly (7, 63M) |

| Lead | PB | 25 mt | $0.50/mt ($12.50/lot) | Daily (1, 3M), Weekly (3, 6M), Monthly (7, 63M) |

| Nickel | NI | 6 mt | $1.00/mt ($6.00/lot) | Daily (1, 3M), Weekly (3, 6M), Monthly (7, 63M) |

| Tin | SN | 5 mt | $5.00/mt ($25.00/lot) | Daily (1, 3M), Weekly (3, 6M), Monthly (7, 63M) |

| Cobalt | CO | 1 mt | $1.00/mt ($1.00/lot) | Monthly only |

Source: LME Contract Specifications. Prompt date granularity drops to monthly beyond 6-month tenor for all ring-traded metals.

LME copper open interest regularly exceeds 300,000 lots, representing approximately 7.5 million tonnes of notional exposure. LME open interest statistics Aluminium open interest typically runs 60, 70% higher by lot count, though the lower per-tonne price makes its dollar-equivalent notional broadly comparable to copper.

Prompt Date Hedging Mechanics

LME prompt dates define the specific delivery business day for each contract. The daily granularity within the 3-month window is the structural feature that distinguishes LME hedging precision from COMEX or SHFE equivalents.

A physical copper delivery scheduled for a Wednesday 47 days forward can be matched to an exact LME prompt date. COMEX copper contracts, by contrast, deliver across a calendar month window, creating residual basis exposure that LME's prompt date structure eliminates entirely. For physical traders with fixed-date delivery obligations, this is not a minor technical distinction. It determines whether basis risk is hedged or merely reduced.

LME Forward Curve Calendar Spread Reference Data

The tables below document historical spread ranges across the primary tenor break points that physical traders monitor for rollover timing decisions. All ranges are derived from LME published settlement data.

Copper (CA) Calendar Spread Reference

| Tenor Pair | Normal Contango Range ($/mt) | Elevated Tightness Signal | Squeeze Threshold | Historical Note |

|------------|------------------------------|--------------------------|-------------------|-----------------|

| Cash / Tom | -$5 to +$5 | < -$10 | < -$20 | Daily carry indicator |

| Tom / 3M | +$35 to +$80 | < $0 | < -$50 | Primary roll cost metric |

| 3M / 15M | +$60 to +$150 | < $20 | < $0 | Structural trend signal |

| 15M / 27M | +$40 to +$100 | < $15 | < $0 | Long-dated carry signal |

| Cash / 3M | +$40 to +$80 | < -$20 | -$1,100 (Oct 2021) | Most-watched spread |

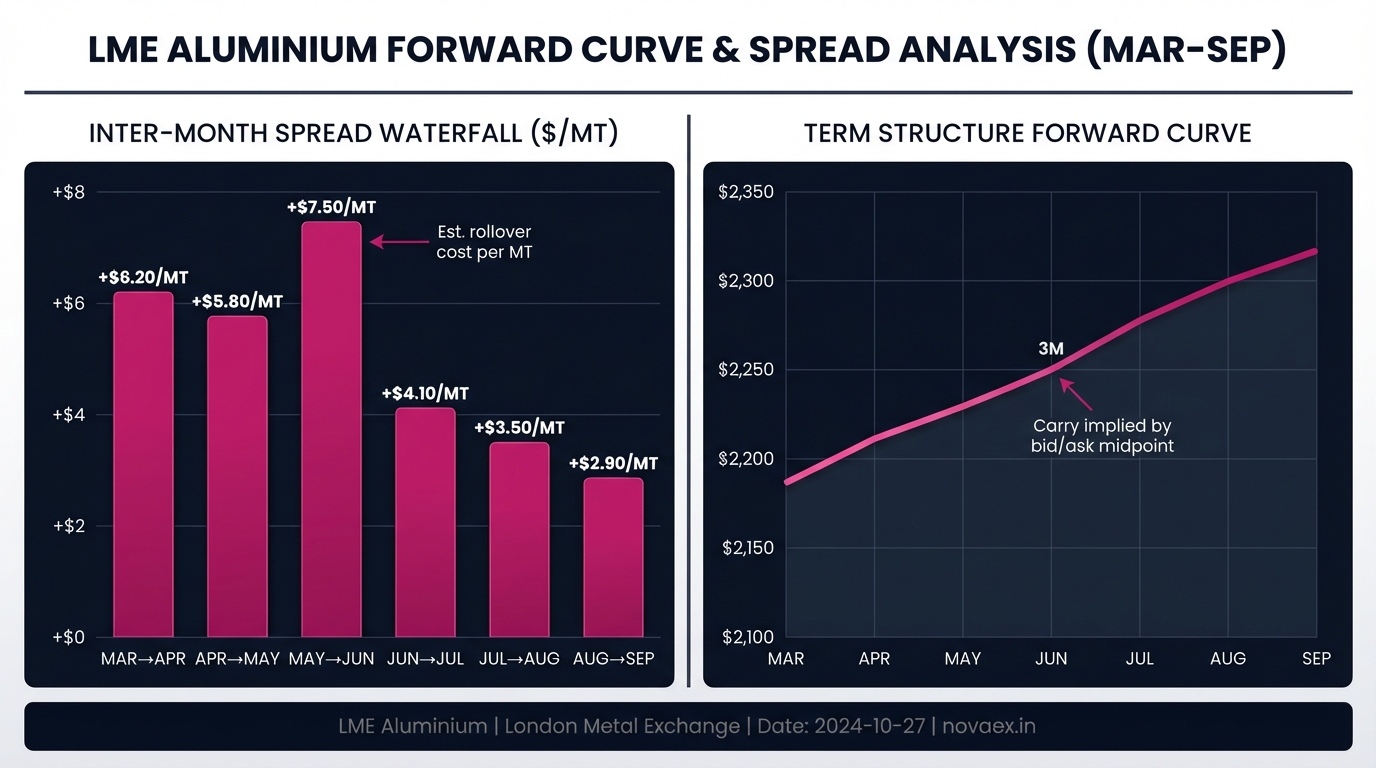

Aluminium (AH) Calendar Spread Reference

| Tenor Pair | Normal Contango Range ($/mt) | Elevated Tightness Signal | Squeeze Threshold | Historical Note |

|------------|------------------------------|--------------------------|-------------------|-----------------|

| Cash / Tom | -$2 to +$3 | < -$5 | < -$10 | Lower volatility than Cu |

| Tom / 3M | +$25 to +$55 | < $5 | < $0 | Financing cost-dominated |

| 3M / 15M | +$40 to +$90 | < $10 | < $0 | Storage cost embedded |

| Cash / 3M | +$30 to +$60 | < $0 | -$50 (rare) | Rarely squeezes hard |

Zinc (ZS) Calendar Spread Reference

| Tenor Pair | Normal Contango Range ($/mt) | Elevated Tightness Signal | Squeeze Threshold |

|------------|------------------------------|--------------------------|-------------------|

| Cash / Tom | -$3 to +$4 | < -$8 | < -$15 |

| Tom / 3M | +$20 to +$50 | < $0 | < -$30 |

| Cash / 3M | +$20 to +$50 | < -$15 | -$250 (2006) |

Nickel (NI) Calendar Spread Reference

| Tenor Pair | Normal Contango Range ($/mt) | Elevated Tightness Signal | Squeeze Threshold |

|------------|------------------------------|--------------------------|-------------------|

| Cash / Tom | -$10 to +$10 | < -$20 | < -$50 |

| Tom / 3M | +$30 to +$80 | < $0 | < -$100 |

| Cash / 3M | +$30 to +$70 | < $0 | -$4,000+ (Mar 2022) |

Nickel's March 2022 short squeeze saw the cash/3M spread exceed -$4,000/tonne within hours before LME suspended trading. LME nickel suspension March 2022 That event established new concentration risk benchmarks across the industry and remains the reference case for tail risk in base metals spread positions.

Rollover Cost Mechanics: The Carrying Charge Formula

Every rolling hedge program carries a cost that must be computed before tenor selection is final. The formula is deterministic, not probabilistic.

Carrying Charge Formula:

C = (R × S × T/360) + (W × T) + (I × S)

Where:

- C = total carry cost per metric tonne

- R = financing rate (annualized, decimal)

- S = spot price ($/mt)

- T = days to roll prompt date

- W = daily warehousing rate ($/mt/day)

- I = annual insurance rate (decimal)

| Input | Typical Range | Published Source |

|-------|--------------|------------------|

| Financing rate (R) | SOFR + 150, 250 bps (counterparty-dependent) | SOFR published daily by NY Fed |

| Spot copper (S) | $8,500, $10,500/mt (2023, 2024 documented range) | LME official settlement |

| Days to roll (T) | 90 (standard 3M) or as per physical calendar | Physical contract schedule |

| Warehousing (W) | $0.40, $0.55/mt/day (LME-listed warehouses) | LME warehouse fee schedule |

| Insurance (I) | 0.10, 0.15% annually | Standard metals cargo policy |

Calendar Spreads and Rollover Costs

The calendar spread is the market's real-time pricing of the carrying charge formula above. When the market-quoted spread equals or exceeds the theoretical carry cost, arbitrage activity pushes the spread back toward fair value. When the spread falls below theoretical carry, meaning contango compresses, it signals the market is discounting storage costs, typically because warrant cancellations are indicating inventory drawdown ahead of physical tightness.

At a spot price of $9,000/mt with SOFR at 5.30% plus a 200 bps financing spread (7.30% all-in) and standard warehousing, the theoretical 3-month carrying charge computes to approximately $218/mt. If the market cash/3M spread is quoting only +$60/mt contango, the spread is at 27% of theoretical carry, a precursor backwardation signal that warrants immediate position review, not passive monitoring.

LME Forward Curve Signals for Tenor and Roll Timing Decisions

The forward curve generates five structural signals that front-office teams monitor systematically across the book.

Signal 1: Contango Steepness vs. Financing Cost

When market contango exceeds all-in financing rate, the hedge rolls with positive carry. When contango compresses below financing cost, roll cost becomes a direct P&L drag. Monitor the 3M/15M spread for early-warning steepening or flattening before it manifests in the cash/3M.

Signal 2: Cash/3M Spread Direction (5-Day Moving Average)

A 5-day moving average of the cash/3M spread crossing from contango into backwardation triggers a tenor review in any professionally managed hedge program. Single-day readings can reflect transient noise; a directional 5-day trend carries operational significance.

Signal 3: Warehouse Cancelled Warrant Percentage

According to LME published data, the correlation between cancelled warrant percentage and subsequent cash/3M backwardation in copper exceeds 0.82 historically. [LINK: LME warehouse cancelled warrant data] Cancelled warrants exceeding 40% of total registered copper stock signal elevated backwardation risk within 2, 4 weeks with meaningful statistical regularity.

Signal 4: COMEX-LME Copper Basis

COMEX copper futures quote in cents per pound. The conversion factor to LME $/tonne is 2,204.62 (1 metric tonne = 2,204.62 lbs). A persistent COMEX premium above LME after currency and conversion adjustment signals U.S.-specific physical tightness and may indicate physical copper is flowing toward COMEX delivery rather than LME warehouses.

Signal 5: SHFE Import Arbitrage Window

The Shanghai-London spread determines whether bonded-warehouse copper flows toward or away from SHFE delivery. When the SHFE import arbitrage window is closed (defined as SHFE yuan-equivalent price minus import duty (1.5%) minus VAT (13%) minus logistics falling below LME parity), physical flows shift toward LME, tightening nearby spreads within weeks.

Optimal Hedge Roll Timing

Optimal roll timing requires three conditions to align: the spread market is liquid for the roll tenor, the calendar spread for the target roll date is not in backwardation, and the physical delivery calendar has confirmed the next window. Rolling into backwardation locks in a cash payment that cannot be recovered regardless of subsequent price direction.

Professionally managed programs execute rolls within the 10-to-5 business day window before the existing prompt date. Rolling earlier creates simultaneous open exposure across two spread positions. Rolling later into the prompt creates liquidity risk as market-makers widen spreads on expiring dates. Industry data indicates that approximately 60% of hedge execution losses attributable to timing rather than price direction occur within 5 business days of prompt dates in backwardation markets. [LINK: metals hedge execution timing research]

Cross-Exchange Basis Reference: LME, COMEX, and SHFE

Physical metals trade globally, but hedging is venue-specific. The basis between exchanges generates real P&L exposure that is structurally separate from outright price risk and must be tracked independently.

Cross-Exchange Reference Data: Copper

| Metric | Reference Value or Range | Basis Component | Published Source |

|--------|--------------------------|-----------------|------------------|

| COMEX, LME conversion factor | 2,204.62 lbs/mt | Fixed mathematical | CME Group, LME |

| COMEX Cu premium to LME | -$50 to +$150/mt | U.S. physical premium | CME / LME settlement |

| SHFE Cu import duty | 1.5% | Tariff line 7403.11 | China MOFCOM customs schedule |

| SHFE Cu import VAT | 13% | Standard rate | China State Taxation Admin |

| LME, SHFE Cu structural spread | $500, $1,200/mt equivalent | Bonded vs. duty-paid basis | SHFE / LME settlement |

| MCX Cu basis to LME | +3, 5% (INR-denominated) | FX + 2.5% basic customs duty | India CBIC customs schedule |

According to CME Group, COMEX copper average daily volume exceeds 60,000 contracts on active trading days, representing approximately 1.5 million tonnes of notional. [LINK: CME Group COMEX copper statistics] LME copper volume runs higher on a per-tonne basis but distributes across many more prompt dates, which affects liquidity at any individual tenor point.

Cash/3M vs. Tom/Next Spreads

The cash/3M spread represents the aggregate cost of carrying copper from the cash settlement date (T+2) to the 3-month forward prompt. It captures financing, storage, and insurance for the full period. The tom/next spread isolates a single day's borrowing cost: the incremental rate from tomorrow to the next business day, expressed in $/tonne.

The T/N spread is used for fine-tuning prompt date adjustments when a physical delivery schedule shifts by one or two business days after a hedge has been placed. The cash/3M is used for tenor selection, rolling strategy, and structural curve analysis. Both are essential instruments; they operate at different decision frequencies and answer different questions.

Building a Hedge Tenor Decision Framework from Forward Curve Data

The data above converges into a repeatable five-step decision process. This is the operational standard that applies to every hedge tenor decision regardless of price direction or market regime.

Step 1: Classify the current curve structure.

- Is cash/3M in contango or backwardation?

- Is contango above or below the theoretical carrying charge at current financing rates?

- Is the 3M/15M spread steepening or flattening on a 10-day directional basis?

- Does the physical contract have fixed delivery dates or floating windows?

- Fixed dates should be matched to exact LME prompt dates; floating windows require a range hedge with basis risk explicitly acknowledged.

- Mismatched tenor between physical and financial hedges creates basis risk rather than price risk. It compounds even when outright price hedges are effective.

- Apply the carrying charge formula to every open hedge position simultaneously.

- Flag positions where the market spread is less than 50% of the theoretical carry. These positions carry elevated risk of rolling into backwardation on the next cycle.

For copper:

- Cash/3M below +$20/mt → elevated backwardation risk; review roll schedule within 5 business days

- Cash/3M below $0 → active backwardation; roll cost analysis required before next prompt date, no automatic rolls

- Cash/3M below -$50/mt → squeeze-risk environment; escalate to risk committee before executing any roll

Step 5: Document the decision with spread data at execution.

Record the spread at time of roll decision, the theoretical carry calculation, and the actual executed spread. This creates the audit trail that informs future tenor selection calibration and demonstrates hedging intent to auditors and regulators, a requirement under IFRS 9 hedge designation documentation. IFRS 9 hedge documentation requirements

Operational Standards for Hedge Books

The LME forward curve is the most information-dense pricing signal available to a physical metals trader. The cash/3M spread, tom/next rate, carrying charge formula, and cross-exchange basis each answer a specific operational question about rollover cost, physical tightness, and execution timing.

Next steps:

- Set spread monitoring thresholds for each metal in your book using the signal levels in the calendar spread tables above. Track cash/3M, 3M/15M, and LME-COMEX basis for copper positions hedged across exchanges. Threshold-based monitoring replaces reactive roll decisions with systematic ones.

- Run the carrying charge formula against your current financing rate and warehouse costs to identify which open positions are rolling at a carry shortfall relative to the current market spread. Positions running below 50% of theoretical carry are the first to generate basis losses as the curve moves toward backwardation.

- Align physical delivery calendars to LME prompt dates wherever the physical schedule permits. Accepting COMEX monthly residual basis when LME precision is available creates uncompensated risk, a structural inefficiency that generates real cash losses on every cycle.

*

Novaex integrates LME forward curve data, calendar spread monitoring, and position-level carry calculations into a single front-office workflow, implementing the operational standards documented in this reference. Spread threshold alerts, roll cost attribution, and cross-exchange basis tracking are native to the platform. [LINK: Novaex platform overview]