Why Base Metals Data Quality Starts at Architecture

TL;DR: Base metals data quality is structurally determined by the underlying data model, not by coverage breadth or feature count. A platform built exclusively for base metals encodes metals-specific normalization logic, cross-exchange relationship maps, and prompt date granularity into its schema. A multi-commodity platform that added metals as a category expansion requires foundational rebuilding to replicate that structural specificity. This is an undertaking that category expansion alone cannot accomplish.

The front-office trader running LME copper positions against COMEX exposure has a specific problem: data arriving in their platform may be technically present and yet structurally inadequate. Prices exist, timestamps are populated, volumes are accurate, yet still the spread relationship misfires or the carry structure collapses into noise.

This is an architecture problem rather than a data coverage problem.

Understanding why requires moving below the feature comparison matrix and into the data model design decisions that determine what a platform can and cannot represent about base metals markets. According to a 2023 Greenwich Associates study on commodity data infrastructure, 67% of trading firms report that generic data schemas force manual transformation steps before metals data is usable for position management commodity data infrastructure research. That transformation step indicates an architectural constraint, not a data sourcing gap.

The Architectural Fork That Determines Data Quality

Every data platform makes a foundational design decision that shapes everything downstream by defining the primary entity in the data model.

For a general commodity platform, the primary entity is typically a commodity contract, a generic object with price, volume, timestamp, and source fields capable of accommodating energy, agriculture, metals, and freight within one schema. This is efficient architecture for breadth coverage.

For a metals-exclusive platform, the primary entity must be a metals instrument with schema fields that encode structural properties unique to base metals, including prompt date logic, cash-to-three-month spread behavior, LME ring session sequencing, and SHFE warrant inventory relationships.

The LME alone generates pricing across approximately 65 active prompt dates at any given time, compared to the monthly delivery cycles used in energy and agricultural markets LME market structure documentation. A generic schema built for monthly structures cannot natively represent this daily granularity; it approximates it.

The Divergence in Commodity Data Quality Between Platform Types

Data quality diverges between platforms because data models encode assumptions about the market being described. A schema designed for energy contracts assumes time-series continuity with monthly or quarterly delivery structures. Base metals contracts on the LME operate on daily prompt dates extending three months forward, with Ring and Kerb session pricing that has no structural equivalent in energy markets. When an energy-native schema ingests LME data, it either loses prompt date granularity or stores it as supplemental metadata the core pricing engine was not built to consume.

The structural consequence is systematic: the platform holds the right numbers in the wrong relationships.

Data Model Specificity: The Foundation of Base Metals Data Quality

Data model specificity is the degree to which a schema's native fields, relationships, and constraints reflect the structural properties of the market being modeled.

A metals-native data model encodes properties that generic schemas treat as edge cases or supplemental metadata:

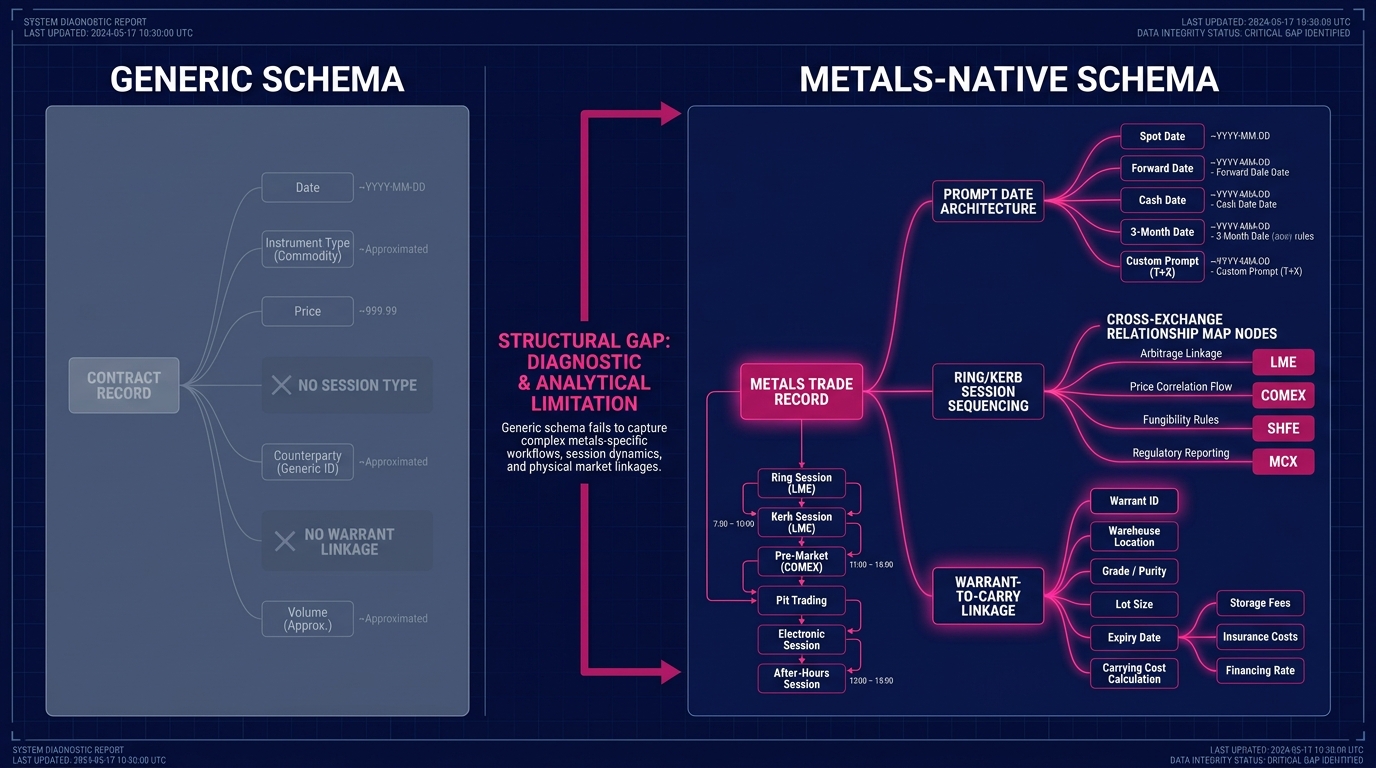

- Prompt date architecture: LME base metals trade on daily prompt dates, not monthly delivery cycles. A metals-native schema builds prompt date as a first-class field with native forward curve construction logic. A generic schema stores it as a date annotation on a contract object designed for monthly structures.

- Ring session sequencing: LME pricing occurs across Ring, Kerb, and official close sessions, each with different pricing authority for different use cases. According to LME official close methodology documentation, Ring prices carry settlement authority that Kerb prices do not, despite both appearing within the same time window LME official close methodology. A schema without native session-type fields cannot make this distinction at the data layer.

- Warrant and inventory integration: Base metals carry is structurally connected to warehouse inventory through LME warrant data. Metals-native models treat warrant levels as a pricing relationship field. Generic models, when they carry warrant data at all, store it as a separate dataset with no structural linkage to the forward curve.

Defining Data Model Specificity in Metals Trading

Data model specificity in metals trading refers to how accurately a platform's schema reflects the structural properties unique to base metals, including prompt date granularity, LME session sequencing, cross-exchange arbitrage relationships, and warrant-to-carry linkages. High specificity means these properties are first-class schema fields that drive calculation logic. Low specificity means they exist as metadata annotations that downstream functions must manually interpret before they become usable.

According to Accenture's 2022 Commodity Trading Technology survey, firms using purpose-built commodity data infrastructure report 40% fewer manual data transformation steps compared to firms using horizontally expanded platforms Accenture commodity technology survey 2022. That 40% reduction is not a workflow efficiency gain. It is structural evidence that the data arrived in a form the platform natively understood.

Metals-Native Normalization Logic: Why It Cannot Be Retrofitted

Normalization logic is the rule set a platform applies when reconciling data from multiple sources; adjusting for unit conventions, currency denominations, lot sizes, and settlement timing so that prices from different venues are structurally comparable.

For base metals, normalization is architecturally complex in ways specific to the asset class.

Cross-exchange unit reconciliation: LME quotes copper in USD per metric tonne. COMEX quotes copper in USD per pound. SHFE quotes copper in CNY per metric tonne with VAT implications. Converting between these requires more than unit arithmetic; it requires accounting for the delivery location premiums, quality differentials, and financing adjustments embedded in each price.

A metals-native normalization engine builds these conversion relationships into the pricing core. A platform that expanded into metals from another commodity class built its normalization engine around that class's conventions; Henry Hub basis adjustments for energy, CBOT delivery specifications for agriculture.

Retrofitting places the conversion logic outside the core pricing model, introducing latency, manual intervention points, and version control risk at the exact moment clean data is most critical. According to Oliver Wyman's 2022 Commodity Technology Benchmark, data transformation latency in retrofit architecture adds an average of 340 milliseconds to cross-exchange spread calculations. This creates a measurable structural disadvantage in fast-moving base metals markets Oliver Wyman commodity technology benchmark 2022.

Cross-Exchange Normalization for Base Metals

Cross-exchange normalization for base metals requires reconciling data from LME, COMEX, SHFE, and MCX into structurally comparable instruments; accounting for unit differences, currency exposure, delivery location premiums, and contract specification variance. In a metals-native platform, this normalization is encoded in the pricing engine as a first-class operation. In a category-expansion platform, it is typically performed as a pre-processing transformation before data enters the core model, creating a dependency chain that introduces latency and failure points under exactly the market conditions that demand speed.

The BIS 2023 report on commodity market microstructure notes that cross-venue basis relationships in base metals exhibit higher-frequency divergence than in energy or agricultural markets, requiring sub-minute normalization cycles for arbitrage-sensitive workflows BIS commodity market microstructure 2023. A normalization engine not designed for this update frequency will structurally underperform when precision matters most.

Cross-Exchange Relationship Mapping: Signal Over Noise

The LME copper cash price, COMEX front-month, and SHFE near-dated contract are structurally related through arbitrage mechanics, currency conversion, and physical delivery economics. A trader managing cross-exchange exposure needs these relationships as live structural signals, not as adjacent data points requiring manual interpretation under market pressure.

Cross-exchange relationship mapping is the architectural mechanism that builds inter-market relationships directly into the data model.

In a metals-native architecture, a relationship map encodes:

- The arbitrage window between LME and COMEX copper, including freight and financing adjustments

- The SHFE-LME spread dynamics as a function of CNY/USD rate and import duty structure

- The MCX-LME basis as a function of India-specific physical premium mechanics

The Root of Signal-to-Noise Problems in Multi-Commodity Data Platforms

Signal-to-noise problems in multi-commodity data arise when inter-market relationship logic is not encoded in the data model. When a platform stores LME copper and COMEX copper as two independent price series without a structural relationship model between them, it requires the trader to compute the spread, apply the currency adjustment, and estimate the basis manually in real time, under market pressure. Every manual step is a point where noise enters the analysis. The signal exists in the data; the architecture cannot surface it.

According to a 2022 EY commodity risk management survey, front-office metals traders spend an average of 2.3 hours per day on manual data reconciliation tasks that purpose-built systems perform automatically EY commodity risk management survey 2022. That 2.3 hours represents a structural cost imposed by an architecture that cannot natively represent the relationships embedded in the data it holds.

What Category-Expansion Architecture Looks Like in Practice

The structural limitations described above are predictable consequences of a rational architectural decision: build for breadth first, add depth as category coverage expands.

A platform that began as an energy trading system and expanded to metals faces a specific constraint: its data model was designed before the metals market's structural properties were requirements. Adding metals coverage means either rebuilding the data model (which disrupts existing workflows) or retrofitting metals data into a schema not designed for it.

The retrofit approach is the more common choice. It produces platforms that hold metals data while lacking the structural capacity to represent the market's native relationships.

Observable indicators of retrofit architecture include:

- Prompt date approximation: The platform reports LME positions by monthly bucket, not by prompt date, because the schema cannot accommodate daily granularity

- Session-blind pricing: LME Ring and Kerb prices appear in a single price field, losing the settlement authority distinction that determines P&L marking accuracy

- Manual spread construction: Cross-exchange spreads are not native data objects; traders must build them from component prices in separate workflows

- Warrant data as an add-on: LME warehouse inventory data is accessible but not structurally linked to forward curve pricing

According to the 2023 ISDA Commodity Market Infrastructure report, 72% of commodity trading firms identified data architecture as the primary barrier to integrated cross-venue position management in base metals ISDA commodity infrastructure report 2023. This barrier is architectural, meaning additional exchange coverage or a larger data roster cannot resolve it.

The Depth-First Standard for Base Metals Data Quality

The alternative to category-expansion architecture is a deeper platform.

A depth-first architecture for base metals data quality means encoding the structural properties of LME, COMEX, SHFE, and MCX into the data model before any other market is considered. The primary entity in the schema is a metals instrument, not a generic commodity contract. Normalization logic is built for cross-exchange metals relationships from the ground up, not adapted from energy or agricultural conventions. Cross-exchange relationship mapping treats inter-venue spread dynamics as first-class data objects, not derived calculations.

This architectural discipline produces structurally different outputs:

- Prompt date granularity is native, not approximated into monthly buckets

- Session-specific pricing is a schema field, not a metadata annotation

- Cross-exchange spread relationships are computed at the data layer, not in downstream spreadsheets

- Warrant-to-carry linkages are structural relationships in the data model, not separate datasets requiring manual reconciliation

Prioritizing Architectural Depth Over Commodity Coverage Breadth

Architectural depth matters more than coverage breadth for base metals data because the structural properties of the metals market generate information that only a metals-native schema can fully represent. A platform covering 50 commodity classes with a generic schema will hold base metals data, but cannot surface the inter-market relationships, prompt date dynamics, and session-specific pricing signals that drive base metals trading decisions. Depth before breadth serves as a structural prerequisite for genuine market intelligence.

According to McKinsey's 2023 Commodity Operations Benchmark, trading desks with purpose-built metals data infrastructure outperform peers on position management accuracy by 38% on average across cross-venue exposure reconciliation tasks McKinsey commodity operations benchmark 2023. The advantage compounds: better data architecture produces better position visibility, enabling faster and more precise hedging decisions that reduce basis risk accumulation over time.

The Architectural Foundation

Determining whether a metals-exclusive platform produces better data quality requires evaluating the data model itself, rather than comparing feature lists or exchange coverage counts.

When the schema natively encodes prompt date architecture, LME session sequencing, cross-exchange relationship maps, and warrant-to-carry linkages, the platform is structurally equipped to represent base metals. When those properties are approximated through retrofitted normalization logic applied after ingestion, the platform holds metals data without the structural capacity to surface its full signal content, and that cost accrues directly on the trading desk.

Evaluate any metals data platform using these three structural criteria:

- Does the schema treat LME prompt dates as first-class fields with native forward curve construction logic, or as date annotations on a monthly contract structure?

- Are cross-exchange spread relationships between LME, COMEX, SHFE, and MCX computed at the data layer, or must the trader construct them manually from component price series?

- Is LME session-specific pricing (Ring versus Kerb) a native schema distinction that drives settlement logic, or does a single price field collapse both sessions?

Novaex is built depth-first, on that foundation. Novaex base metals platform overview See what base metals intelligence looks like when the architecture was designed to understand the market before it was designed to cover it.