LME Settlement Mechanics: What Most Platforms Miss

Most commodity platforms support LME as a listed exchange. Mastering LME settlement mechanics means modeling the Ring-based official price window, the full prompt date ladder, 750+ approved delivery grades, and warrant-level physical inventory data as an integrated system. These represent categorically different capabilities. The gap between them is where hedging precision degrades.

The London Metal Exchange settles approximately $50 billion in notional value every trading day LME Annual Report, 2023. Most commodity platforms include LME in their coverage.

What that typically includes is settlement price feeds: the exchange in trade entry dropdowns, a field populated with "LME Copper" and a corresponding number.

That is a meaningful starting point. It is not the same as a complete understanding of LME market structure.

Mastering LME settlement mechanics means understanding how that number is generated, what physical obligations it triggers, how grade differentials alter the economic value of a hedge, and what warrant movements in LME-approved warehouses signal about near-term spot dynamics. It means treating the LME not as a data source but as a complete system of pricing, delivery, and position obligation. It requires building platform intelligence around that system.

This distinction defines depth-first metals intelligence. Not a feature comparison. It is a design philosophy.

What "LME Settlement Mechanics" Support Really Means

When a multi-commodity platform claims LME support, it typically delivers three things: LME settlement prices are available, the exchange appears in trade entry dropdowns, and P&L can be calculated against an LME benchmark.

These are essential capabilities. They are also where most platforms stop.

The constraint is architectural rather than intentional. A breadth-first platform is built to cover 40 exchanges and 200 commodities. Genuine depth at that scope requires substantially higher development investment per market, which is an investment most platforms do not make. The result is broad market coverage with limited structural understanding of any individual market's mechanics.

According to a 2023 survey by Energy Risk, over 60% of commodity trading professionals reported that gaps in market-specific data modeling were a primary driver of manual workarounds in their risk workflows Energy Risk, 2023. Those manual workarounds occur at precisely the moment market precision matters most.

For base metals traders, the gap carries material consequences. LME's pricing and settlement structure is unlike any other exchange. A platform that does not model that structure completely provides data that is LME-referenced but not LME-complete. That distinction becomes measurable at settlement.

The LME Official Settlement Price

The LME official settlement price is established during a five-minute Ring trading session, not from electronic order book data. The Ring convenes twice daily, and the prices produced during these sessions become the reference prices for physical contracts, financial settlements, and long-term supply agreements globally.

The official price reflects open-outcry dynamics, Ring member participation, and the specific lots traded during that window, not an algorithm or a volume-weighted average. A platform that models LME settlement as equivalent to an electronic exchange close introduces a structural misrepresentation of the mechanics, creating basis risk in every hedge calculated against it.

The downstream effect is operationally significant. Traders hedging physical supply agreements pegged to LME official prices require their risk system to distinguish between official prices (Ring-derived), closing prices (electronic session), and carry-adjusted prices (date-specific). These are different numbers. Treating them as equivalent generates basis risk that compounds until a delivery or settlement forces it into visibility.

The Prompt Date Structure No Breadth-First Platform Models Completely

Most futures exchanges operate on a standard monthly expiry calendar: fixed dates and predictable planning cycles.

The LME operates differently.

LME copper, aluminum, zinc, nickel, lead, and tin trade on a prompt date structure that includes daily dates for the first three months, weekly dates out to six months, and monthly dates out to three years. This means hundreds of live tradable dates exist simultaneously. Each has its own bid, offer, and carry structure.

The spread between any two prompt dates reflects not just time value but warehouse costs, lending rates, nearby physical tightness, and market positioning. This spread structure (the LME forward curve) is where substantial P&L is generated and lost by physical traders managing rolling hedge programs.

According to LME market data, the three-month copper contract alone averaged over $12 billion in daily notional turnover in 2023 LME Market Data, 2024. The majority of that volume involves spread and carry positioning, not outright directional trades.

The Complexity of LME Prompt Dates

LME prompt dates create hedging complexity because physical delivery and financial settlement obligations both key to specific prompt dates, not month-end averages. A physical trader who fixes a copper purchase against the "three-month price" on a given day establishes a specific prompt date obligation. The corresponding hedge must match that date exactly to avoid a carry mismatch.

Carry mismatches are not theoretical. When cash/three-month spreads move from contango to backwardation (as they did significantly during the 2021 to 2022 nickel and aluminum supply disruptions), improperly dated hedges generate unexpected margin and mark-to-market losses that are independent of the trader's directional view.

A depth-first platform models the full prompt date ladder as a live, navigable data structure: every date, every spread, every carry implied by the current curve. That is the complete picture the LME provides.

LME Settlement Mechanics and the Delivery Grade Problem

Here is where the distinction between "LME listed" and "LME understood" becomes financially material.

The LME does not accept a single grade of copper, aluminum, or zinc for delivery. It maintains an approved brand and shape registry that, as of 2024, lists over 750 approved brands and shapes across its base metals complex LME Approved Brands List, 2024. Each approved brand carries a different market premium or discount relative to the LME benchmark price.

These are called physical premiums, and they are not reflected in LME settlement prices. They trade separately, typically in OTC markets referenced against industry benchmarks such as Platts, Metal Bulletin, or CRU.

A physical copper trader does not simply purchase "LME copper." They buy a specific brand and shape (cathodes from a particular smelter, in a specific form, delivered to a defined location). The all-in cost is LME cash price plus a physical premium that may range from $50 to $250 per tonne depending on supply conditions, buyer location, and brand quality.

Delivery Grades and Hedge Impact

The LME price hedges price risk against the LME settlement benchmark, not against the all-in cost of the specific metal being bought or sold physically. If a physical purchase involves a high-premium brand or an off-exchange location, the hedge carries residual premium risk that remains unmanaged unless the platform models that spread explicitly.

According to Fastmarkets data, physical aluminum Midwest premiums ranged from $0.14/lb to $0.26/lb across 2022 to 2023 Fastmarkets, 2023. This swing exceeds $120 per tonne and does not appear in any LME settlement price feed.

A metals trading platform that captures only LME settlement prices is therefore structurally incomplete for physical traders' all-in cost exposure. Depth-first metals intelligence requires modeling the spread between LME benchmark prices and physical market premiums as a first-class data structure. It must be integrated into position and risk calculations, not appended as an optional field.

What LME Warrant Structure Reveals About Physical Markets

LME warrants are among the least discussed and most operationally significant components of the LME system for physical traders.

A warrant is a document of title to a specific lot of metal (a specific quantity, brand, shape, and location) held in an LME-approved warehouse. Warrants are tradable instruments. When a warrant changes hands, physical metal changes ownership. When warrants are cancelled (withdrawn from LME-approved warehousing for delivery), they signal imminent physical off-take.

LME publishes daily warrant and cancelled warrant data for every approved metal and warehouse location. This data functions as one of the most reliable leading indicators of physical supply tightness available in the base metals market.

During the March 2022 nickel crisis, LME nickel warrant levels reached historic lows before the short squeeze that forced a halt in trading Financial Times, March 2022. The signal was present in the published data; whether a given platform surfaced it as usable information is a separate and consequential question.

The Importance of LME Warrants for Physical Traders

For physical traders, warrant levels matter because declining warrant stocks (particularly in key locations) indicate that physical metal is being withdrawn for delivery, which typically precedes spot price increases and backwardation in the prompt date structure.

Cancelled warrants (those flagged for physical withdrawal) function as a particularly sensitive leading indicator. A sustained increase in cancellations in a specific location can signal a developing supply squeeze weeks before it appears in outright price data, providing position-aware traders with meaningful advance notice.

A platform that does not model warrant-level inventory by location, brand, and cancellation status is missing a structural data layer that physical traders rely on daily. For physical metals trading workflows, this is not an advanced analytics feature. It is a foundational data requirement.

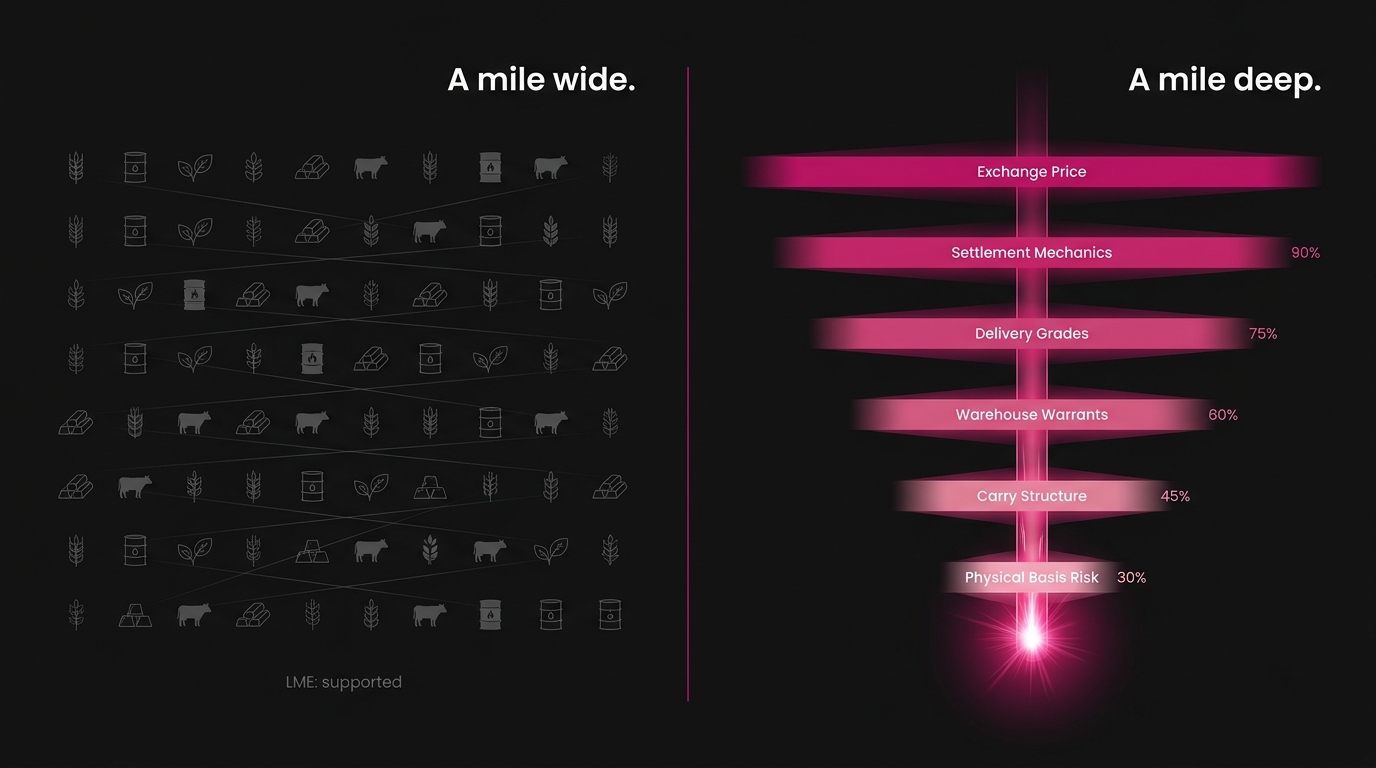

Depth-First Intelligence: A Design Philosophy, Not a Feature List

The four mechanics described above (Ring-based official price determination, full prompt date ladder, delivery grade premium structures, and warrant-level inventory signals) are not independent features. They constitute a system. The LME functions as a system.

Depth-first metals intelligence is the design philosophy that begins from this fact.

It means building a platform that understands the LME as a complete market system, not as a price feed with optional extensions. The prompt date ladder, delivery grade registry, and warrant data are modeled in the core data architecture, not appended to a generic commodity framework designed for agricultural futures or energy swaps.

Breadth-first design makes an explicit architectural trade-off: coverage over depth. It allows a platform to list 40 markets while modeling the structural mechanics of none completely. For certain use cases, that trade-off is appropriate. For front-office base metals traders where hedging precision has direct P&L consequences, it is not.

Defining Depth-First Metals Intelligence

A depth-first platform is designed to completely model a single commodity's full market structure (pricing mechanics, settlement obligations, physical delivery system, and risk factors) before expanding to the next commodity. For LME base metals, that means the Ring price, the prompt date ladder, the approved brand registry, and the warrant system are modeled as an integrated intelligence layer, not assembled from generic data components.

The term deliberately inverts the industry default. Most platforms expand coverage first and add structural depth in response to feature requests. Depth-first platforms build complete market understanding as the foundation, because incomplete understanding, at trading scale, introduces systematic basis risk that compounds across every trade, every roll, and every settlement.

Novaex was built by a trader who spent four years documenting exactly where commodity platforms fell short of base metals workflows, not in theory, but in live trading decisions where the gaps had measurable P&L consequences. The depth-first methodology is the direct product of that documentation. Novaex founding story

What the Intelligence Gap Costs in Real Trading Scenarios

Here is what the gap between LME-listed and LME-complete coverage costs in practice.

Scenario 1: The rolling hedge mismatch. A copper fabricator hedges forward purchases using a three-month LME benchmark. Their platform represents the curve in monthly buckets. When they roll the hedge, the platform calculates roll cost against a monthly average. The actual roll trades against a specific prompt date. Fastmarkets estimated that imprecise rolling practices cost industrial hedgers an average of 0.3 to 0.8% of notional hedge value annually through avoidable carry drag Fastmarkets Metals Risk Report, 2022. On a $50 million annual hedge book, that is $150,000 to $400,000 in preventable leakage.

Scenario 2: The grade premium blind spot. An aluminum buyer fixes an LME price for 500 tonnes of primary aluminum. Their platform shows full hedge coverage against LME price risk. The physical contract specifies a high-demand European brand at a port premium of $180 per tonne. The platform does not model physical premiums. The $90,000 premium exposure is not visible in the risk view until the invoice arrives.

Scenario 3: The warrant signal missed. LME aluminum cancelled warrants increase 40% in a key European location over three consecutive trading days. A trader on a breadth-first platform sees LME aluminum prices in their system but does not see the cancellation data because the platform does not model it. A trader on a depth-first platform receives the signal as a highlighted shift in physical inventory posture, a potential backwardation trigger, days before it moves the cash spread.

Three scenarios. Three systematic gaps. None of them visible if LME coverage is measured by whether the exchange name appears in a dropdown.

The Standard Novaex Is Building and How to Apply It

The base metals industry has operated for decades with an implicit tolerance for platform gaps. Traders filled those gaps with spreadsheets, Bloomberg terminals, proprietary tools, and expertise that resided in individuals rather than systems.

That tolerance reflects the absence of a better alternative. When platforms are predominantly breadth-first by design, the gap between stated coverage and structural understanding becomes an accepted operating cost.

According to Oliver Wyman, the global metals trading and risk management software market is projected to grow 12% annually through 2028, driven primarily by demand for integrated physical and financial position management Oliver Wyman Commodities Report, 2023. That growth reflects recognized, unmet need. The relevant question is whether the products meeting that demand will be built to the structural depth the market requires.

Depth-first design holds that systematic gaps are not an acceptable permanent condition. A platform covering base metals should model the LME the way a Ring dealer models the LME: as a complete system of interconnected obligations, pricing mechanics, and physical signals.

The criteria that define depth-first LME coverage are specific and measurable:

- Full prompt date ladder: Daily dates for months 1 to 3, weekly through month 6, monthly to 36 months

- Delivery grade registry: 750+ LME-approved brands with associated premium and discount tracking

- Warrant-level inventory: Daily stock, cancelled warrant, and live warrant data by location and brand

- Ring-derived official prices: Distinguished from electronic session prices in all P&L and risk calculations

- Physical premium integration: OTC premium benchmarks modeled alongside LME settlement in all-in cost calculations

Apply these criteria to any platform claiming LME coverage. The distinction between "listed" and "complete" becomes immediately measurable. Novaex platform overview

Here is how to build on what you have read:

- Map your current platform's LME coverage against the five criteria above and identify which layers are absent from your current risk view.

- Quantify your largest basis exposure from the three scenarios described (rolling mismatch, grade premium blind spot, or warrant signal gap) and estimate what that exposure costs annually across your book.

- Request a depth-first demonstration built around your specific LME workflow, not a generic product tour, to see the mechanics in a live trading context. Novaex demo request

Depth-first metals intelligence is a precise claim. The mechanics described here define it and provide the criteria for evaluating whether any platform actually delivers it.