LME Copper Contango Is Not Financial Futures Contango

LME copper contango and financial futures contango share a name and almost nothing else in common. The LME's prompt-date architecture, ring-based price discovery, and warehouse-delivery mechanics produce a forward curve that is structurally incompatible with the cost-of-carry model governing financial futures. When pricing workflows import financial futures contango logic into LME copper positions, the resulting cost-of-carry assumptions do not represent a calibration error. They represent a category mismatch between model and instrument.

This distinction carries operational significance because the pricing error is invisible until it compounds. Front-office metals traders operating across both financial and physical markets routinely apply cost-of-carry interpolation to LME copper positions, a technique that functions precisely in Treasury futures, equity index futures, and FX forwards, and fails structurally in LME copper. The failure is a structural model mismatch rather than a simple calibration issue.

This post identifies the structural source of that mismatch, shows exactly where it surfaces in pricing workflows, and outlines the corrections required to price LME copper on its own terms.

The Cost-of-Carry Model and What It Actually Requires

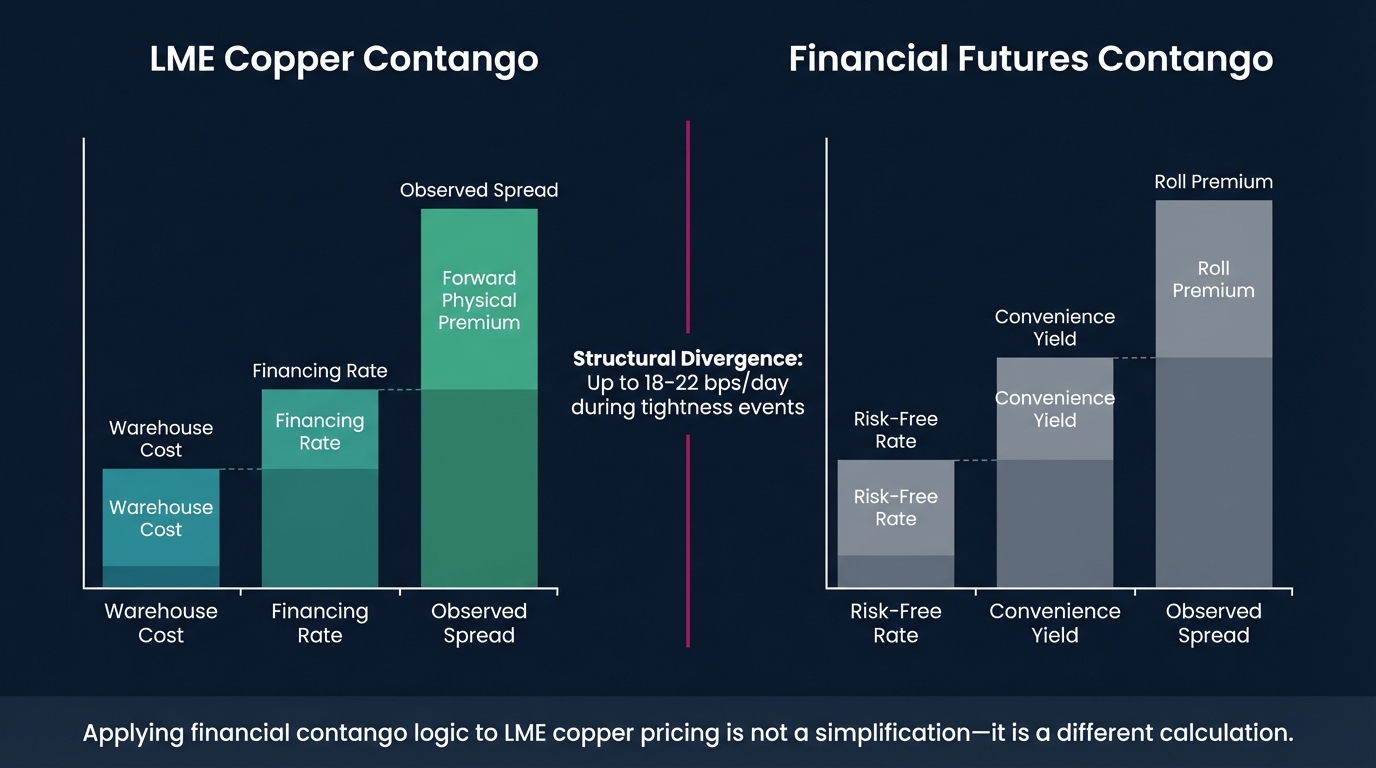

The cost-of-carry framework for financial futures rests on a specific arbitrage condition: the forward price must equal the spot price compounded by net carrying costs over a continuous time horizon. Any deviation is corrected by cash-and-carry arbitrage.

For financial instruments (equity index futures, interest rate futures, currency forwards), this condition holds because delivery is standardized, storage costs are zero or negligible, and financing is available to all market participants at the risk-free rate. According to the CME Group's futures pricing documentation, the fair value of an equity index future is derived entirely from the spot price, the risk-free rate, and the dividend yield. Contango in that context is a direct, measurable function of carry cost.

Even in commodity markets where storage costs are non-trivial, the model remains workable when storage is fungible and uniform. The same tonne stored anywhere costs roughly the same to carry for the same period. The forward curve is theoretically smooth and derivable from a handful of observable inputs.

These are not abstractions. They are the specific conditions the cost-of-carry model requires to function correctly. LME copper satisfies none of them in full.

How LME Copper Contango Is Structurally Different

LME copper contango is a physical market signal, not a carry calculation. Understanding that distinction requires understanding how the LME actually generates its prices, not how a financial exchange would generate analogous prices.

The Meaning of LME Contango

On the LME, contango is the premium of a forward prompt date price over the nearby cash price, most commonly quoted as the cash-to-three-month spread. LME contango reflects warehouse stock levels, physical demand tightness at nearby prompt dates, financing costs, and storage charges simultaneously. Rather than being derived from a cost-of-carry formula, it is discovered in the Ring.

The LME Ring operates as a physical open-outcry trading session lasting exactly five minutes per metal, conducted twice daily in London. According to the LME, Ring-official prices set during these sessions form the basis for the majority of physical copper contracts settled globally. These prices emerge from the intersection of real delivery obligations, nearby borrowing pressure, and dealer inventory positions, not from risk-neutral pricing models operating on continuous arbitrage.

The result is a forward curve that can exhibit contango in the three-month forward while simultaneously exhibiting backwardation in specific nearby prompt dates. That coexistence is structurally impossible in a cost-of-carry framework. It is routine in LME copper.

According to LME market data, copper cash-to-three-month spreads have ranged from contango exceeding $150 per tonne to backwardation of over $100 per tonne within single calendar years. These movements are driven primarily by warehouse stock drawdowns and prompt-date tightness, not by changes in financing costs. LME copper spread historical data

A cost-of-carry model anchored in financial futures logic has no mechanism to explain or predict that range. The signal it is designed to capture does not exist in the LME forward curve in the form the model expects.

Prompt Dates and Why They Break the Continuous-Time Model

The LME does not trade rolling monthly contracts. Every business day within the first three months is an individually cleared, separately tradeable prompt date. Beyond three months, prompts shift to weekly intervals, then to monthly dates out to 63 months for copper. LME prompt date calendar structure

LME Prompt Dates vs. Futures Expiration Dates

LME prompt dates are specific settlement dates on which physical delivery can be made or taken against LME warrants. They are not expiration dates in the financial futures sense: there is no automatic roll mechanism, no contract rollover, and no continuous series of standardized delivery months. Each prompt date is an independent settlement obligation, and the spread between adjacent prompt dates reflects the physical market's demand for deferral or acceleration of delivery at that precise date.

This architecture means the LME forward curve carries over 65 distinct pricing nodes in the first three months alone: one for each business day. Each node is subject to independent spread pressure based on physical conditions prevailing at that specific date.

A financial futures trader modeling LME copper as a monthly rolling contract with a smooth cost-of-carry term structure will interpolate between the wrong anchors, smoothing over the spread volatility that actually drives hedging costs and systematically mispricing the carry between any two hedge dates that do not align precisely with the three-month benchmark.

According to analysis of LME spread dynamics, prompt-date-specific tightness has produced spread variations of $20, $40 per tonne over three-day windows, entirely invisible to any model that treats the LME curve as a continuous, smooth structure. LME prompt spread analysis

For a 500-tonne copper position, that spread variation represents $10,000, $20,000 in realized carry cost that a financial futures model would not predict, capture, or flag. That is not noise. That is a systematic, directional pricing error concentrated at exactly the moments when physical conditions are most stressed.

LME Copper Contango and the Warehouse Premium Interaction

A financial futures practitioner familiar with commodity markets might note that storage costs are already accounted for in the cost-of-carry model. That observation is accurate for markets where storage is fungible, uniform, and independent of delivery timing. LME copper does not meet those conditions.

Warehouse Premium Effects on LME Copper Contango

LME warehouse premiums (the regional premiums above the LME cash price required to acquire physical copper at a specific location and in a specific warrant form) interact directly and structurally with contango in ways that cannot be separated analytically. When warehouse stocks concentrate in a single location or under a single dominant brand, premiums rise and nearby spreads tighten, compressing or inverting contango at specific prompt dates even when the headline three-month spread remains positive.

According to LME warehouse data, registered copper stocks have ranged from below 50,000 tonnes to over 700,000 tonnes within the same 18-month period, a greater than 14-fold range that directly drives the relationship between cash and forward prices across the entire prompt-date structure. LME copper warrant and stock data

Published LME tariff schedules put registered warehouse storage costs for copper at approximately $0.40, $0.46 per tonne per day. But that figure understates total carry cost when load-out queues develop at high-stock warehouses. Extended load-out queues delay physical delivery timelines and increase effective holding costs independently of the official tariff rate, a dynamic that has no equivalent in financial futures markets.

A cost-of-carry model using the published storage tariff as its carrying cost input will underestimate realized carry during load-out queue periods and overestimate it when nearby stocks are scarce and physical sellers accept lower premiums for prompt delivery. Neither error is bounded or predictable in advance from the model's own inputs.

According to physical metals market research, delivered copper costs have diverged from LME-cash-plus-carry estimates by $50, $150 per tonne during periods of elevated warehouse premiums, a divergence that a financial carry model structurally cannot resolve because it has no variable to represent location-specific, warrant-specific premium dynamics. copper physical premium research

Where the Conflation Produces Measurable Pricing Errors

The structural incompatibility described above is not theoretical. It surfaces in three specific, identifiable places in a standard pricing workflow.

LME Contango vs. Cost of Carry

LME contango diverges from the cost of carry because physical market participants set it based on real delivery obligations, not by arbitrageurs enforcing a no-arbitrage pricing relationship. When nearby prompt dates face genuine tightness (because stocks are low, warrants are concentrated, or borrowing demand is elevated), the contango compresses or inverts regardless of what risk-free rates and storage tariffs would theoretically imply. The mechanism that enforces the cost-of-carry relationship in financial futures does not operate with the same force in a physically delivered, warehouse-linked forward market.

Error one: Hedging date interpolation. Traders who interpolate between the LME cash price and the three-month forward to price hedges at intermediate prompt dates assume the curve is smooth between those two anchors. It is not. The daily prompt structure creates independent spread levels at each business day. Smooth interpolation between cash and three-month produces hedge prices that can be $5, $25 per tonne away from the actual tradeable market at any given intermediate prompt. LME copper hedging date pricing

Error two: Roll cost estimation. Financial futures traders estimate roll cost from the prevailing contango level at the time of the roll. On the LME, the spread at the time a hedge is entered is not the spread that will prevail when that prompt date is reached. Spread behavior at a specific future prompt depends on physical conditions at that date. This is a forward-looking variable that the current three-month contango level does not forecast. According to research published in the Journal of Futures Markets, physical commodity spread dynamics diverge from financial carry predictions by up to 40% during periods of inventory stress.

Error three: Warehouse premium exclusion. Pricing workflows derived from financial futures logic treat the LME cash price as the full cost basis, with contango added for carry. This framework has no slot for the warehouse premium. In markets where premiums are elevated, excluding them undervalues total acquisition cost by $50, $150 per tonne, an error that scales linearly with position size and is invisible to any workflow that does not model the premium as a primary variable. physical copper premium workflow

These are not estimation errors within a correct model. They are category errors, outputs of a framework applied outside the domain for which it was designed.

Correcting the Workflow: Pricing LME Copper on Its Own Terms

Recognizing the structural non-equivalence is the necessary first step. Correcting the pricing workflow requires replacing financial futures carry logic with LME-native mechanics at three distinct levels.

Modeling LME Copper Forward Prices

Model LME copper forward prices by treating each prompt date as an independent pricing node, referenced against Ring-official cash and three-month prices and adjusted by the actual borrowing or lending spread for that specific date, not interpolated from a smooth carry curve. Warehouse premiums must be modeled as a structurally separate variable with its own drivers, not as an additive adjustment to an LME-cash-plus-carry base. Any workflow that collapses these into a single cost-of-carry calculation will produce the errors described above.

Level one: Prompt-date-specific spread pricing. Consume the actual bid/offer spread for each prompt date from LME interoffice trading rather than interpolating from the three-month forward. Each prompt's spread reflects conditions at that date. Interpolation between benchmark dates papers over the physical market information embedded in the spread structure. LME interoffice spread data sources

Level two: Separate the LME price from the warehouse premium. Model the LME cash price and the physical warehouse premium as two distinct variables with distinct drivers. Contango movements do not translate linearly into premium movements. During periods of rising warehouse stocks, contango may widen while premiums fall simultaneously. A single aggregated copper price variable cannot capture that relationship.

Level three: Replace roll cost estimates with borrowing spread mechanics. When deferring or accelerating an LME position, the cost is the borrowing or lending spread for that specific prompt, not a generalized contango estimate. According to the LME's published pricing conventions, tom-next and cash-next borrowing rates can diverge significantly from the implied three-month carry rate during periods of prompt tightness. Pricing workflows that use the three-month contango as a roll cost proxy will systematically misstate the realized cost of date management for nearby positions.

According to operational reviews of physical metals trading firms, organizations that separately manage prompt-date spread execution and three-month benchmark carry report materially lower hedge execution slippage compared to those applying generalized carry models to LME positions. metals trading operational benchmarks

The operational requirement is direct: pricing LME copper correctly requires infrastructure capable of resolving individual prompt dates as independent nodes, consuming Ring-official prices as the source of truth, and treating warehouse premiums as a primary input, not deriving forward prices from a cost-of-carry formula designed for a different class of instrument.

The Distinction Is Foundational, Not Cosmetic

LME copper contango tells you something real about the physical copper market: where stocks sit, how tight nearby dates are, and what the market requires to defer delivery. Financial futures contango tells you something equally real about financing costs and roll dynamics in a continuous-time arbitrage environment.

These are different signals from different mechanisms. Using one to proxy the other produces errors that are not random: they are systematic, directional, and proportional to the degree of physical market stress. The errors are largest exactly when accurate pricing matters most.

For any organization whose current pricing workflow routes LME copper through financial futures carry assumptions, the diagnostic step is concrete: map every point in the workflow where a contango assumption is applied and identify whether that assumption is sourced from LME prompt-date mechanics or from a financial carry model. That mapping will locate the error precisely.

Novaex is built for this level of operational precision. The depth-first methodology applied to LME copper means every prompt date, every Ring-official price, and every warehouse premium functions as a primary data element in the pricing workflow, not a downstream approximation from a framework designed for a different class of instrument. Novaex LME copper pricing platform

Novaex resolves the incompatibility between physical LME mechanics and financial carry logic in live trading operations. Map the structural gaps in your current LME copper pricing workflow today.