Metals Trading Position Visibility: Mapping Breaks to Architecture

Every metals trading desk deals with breaks. The two categories that generate the most operational and financial exposure are ledger reconciliation failures and cross-exchange position visibility gaps. These are structural deficiencies built into how most platforms are designed—not configuration problems, not user errors. This analysis maps each break to a specific, named architectural component that eliminates it.

TL;DR: Ledger reconciliation failures trace back to asynchronous event processing in batch-state position engines. Cross-exchange visibility gaps trace back to exchange-native schema fragmentation at the ingest layer. Each break has a defined architectural solution—a Unified Event State Engine and a Normalized Cross-Exchange Position Ledger, respectively—and neither is a workaround. They are the correct architecture.

What a "Break" Actually Costs in Metals Trading

Before we map the architecture, we need to define the cost framework.

A break is any point where the operational state of your book diverges from actual market exposure. In metals trading, breaks carry compounding consequences that distinguish them from breaks in other commodity classes.

LME prompt date structures create daily position roll obligations that compound reconciliation errors across business days. Basis differentials between LME, COMEX, and SHFE mean a single unreconciled lot can cascade into multi-exchange exposure misrepresentation. Physical delivery obligations tied to financial hedge positions make reconciliation a legal and logistical matter, not just an accounting one.

Industry estimates from the Commodity Markets Council place operational risk events in physical commodity trading—including reconciliation errors and position discrepancies—at billions in annual losses across hedged commodity portfolios globally. commodity trading operational risk management

Why Legacy Platforms Institutionalize Breaks

Legacy CTRM platforms were built when multi-day settlement was standard and exchange connectivity meant a daily data feed rather than a live position stream. A 2023 Accenture analysis of commodity trading operations found that over 60% of commodity trading firms rely on manual reconciliation steps for at least one critical position workflow.

That figure is not a performance gap. It's confirmation that the platforms themselves require manual intervention to produce a complete position picture. The break is not incidental—it's a design artifact.

Ledger Reconciliation Failures: Anatomy of the Break

Ledger reconciliation failures in metals trading follow a consistent failure signature. Before we can diagnose the architecture, we need to understand that signature.

The failure sequence happens like this:

- A trade executes on the LME

- The execution record enters the CTRM system via feed or manual entry

- The position engine updates based on that entry

- Settlement data arrives asynchronously—hours later or next-day

- The position engine does not reconcile the execution record against the settlement confirmation

- The ledger holds an unconfirmed position the system treats as confirmed

What Causes Ledger Reconciliation Failures in Commodity Trading?

These failures stem from asynchronous event processing. Trade capture, confirmation, and settlement data are handled by separate system modules without a unified event state engine to govern the sequence. When these modules fall out of sync, the ledger reflects a position that doesn't match exchange records. In metals trading, where LME prompt date precision is mandatory, even a one-lot discrepancy creates audit exposure.

The structural cause runs deeper: most CTRM platforms were built around a batch-processing model where positions are reconciled at end-of-day. ION Group's post-trade operations research shows that intraday position discrepancies are reported by the majority of commodity trading desks operating on batch-reconciliation architectures. In an LME environment with three-month prompt structures and daily ring sessions, batch reconciliation is structurally incompatible with the rhythm of the market. LME prompt date structure and settlement

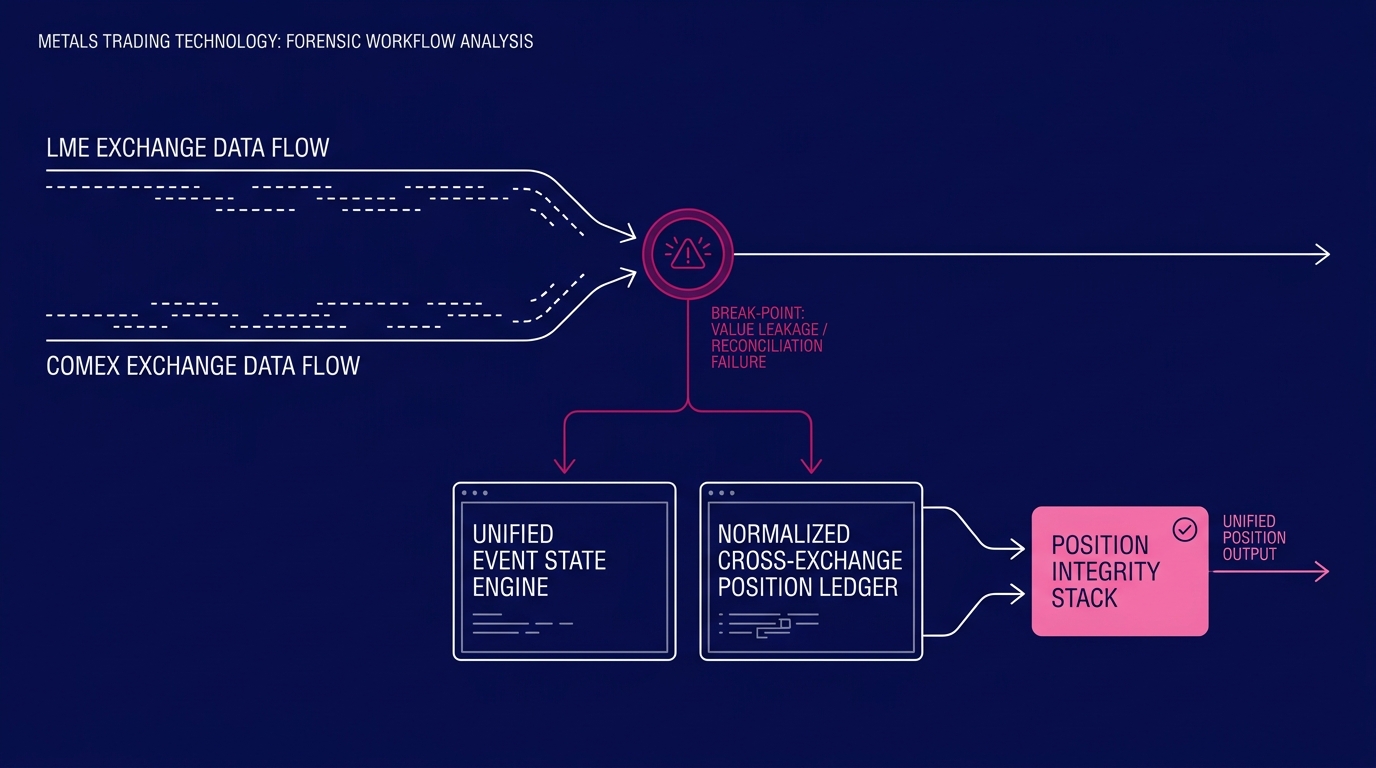

The Named Solution Component: Unified Event State Engine

The architectural fix for ledger reconciliation failures requires replacing the batch model entirely with a Unified Event State Engine (USE).

A USE processes every transaction event—execution, confirmation, settlement, and amendment—as a single ordered sequence in real time. Position state updates atomically: the system cannot hold a confirmed position record without a matching settlement event.

The operational consequence is concrete. When an LME execution occurs, the position record is flagged as execution-confirmed but settlement-pending until the clearinghouse confirmation arrives. The ledger never reflects a settled position that hasn't actually settled. Reconciliation becomes automated and continuous—not manual and periodic.

This isn't just theory—it's a buildable architecture component with defined event processing behavior at each state transition. It is the standard against which any position management platform should be evaluated.

Cross-Exchange Position Visibility Gaps: The Structural Problem

Cross-exchange position visibility gaps are the second primary break category—and the more operationally consequential of the two, because the failure is less visible in daily operations.

A metals trader running a delta-neutral LME/COMEX spread hedge holds positions across two exchanges with fundamentally different structural conventions:

- Lot sizes: LME copper at 25 metric tons versus COMEX copper at approximately 11.34 metric tons per contract

- Prompt date conventions: LME daily prompts versus COMEX monthly expiries

- Margin timing: LME same-day margin calls versus COMEX T+1 in most broker arrangements

- Price benchmarks: LME official settlement versus COMEX futures settlement with materially different liquidity profiles

A platform that cannot consolidate these positions into a single live view doesn't give a trader a spread position. It gives them two separate positions they must manually translate into a spread. That translation step is precisely where breaks occur.

How Cross-Exchange Position Visibility Gaps Affect Hedging Decisions

Cross-exchange position visibility gaps force traders to calculate net exposure manually across exchange-specific position reports, introducing both latency and error risk into every hedging decision. When markets move, a trader without a consolidated LME/COMEX copper position in a single interface cannot execute a delta adjustment without first completing a manual consolidation step. In fast-moving markets, that step costs minutes the market won't spare.

The downstream effect compounds: without consolidated real-time visibility, stop-loss triggers, margin call projections, and basis risk calculations all operate on stale or incomplete data. Risk management research consistently identifies position visibility gaps as a major driver of commodity trading losses under routine market conditions—not just under stress.

Why Legacy CTRM Platforms Fail at Cross-Exchange Position Consolidation

Legacy CTRM platforms fail at cross-exchange consolidation because they ingest exchange data through exchange-native schemas that are never fully normalized. LME data arrives in one format, COMEX data in another, and the platform stores them in separate data models. The "consolidated view" most legacy systems offer is a reporting layer that aggregates these separate models at query time—not a unified position state.

This means the consolidated view is always a snapshot, never live. It is only as current as the last scheduled aggregation job—typically running on minute or five-minute intervals rather than the event-by-event basis active hedging requires. CTRM platform architecture comparison

The Named Solution Component: Normalized Cross-Exchange Position Ledger

The architectural fix is a Normalized Cross-Exchange Position Ledger (NCEL): a position data model that ingests exchange-native data from LME, COMEX, MCX, and SHFE, normalizing it to a single position schema at the point of ingestion.

In an NCEL architecture:

- LME lot sizes are converted to metric ton equivalents on ingest

- COMEX positions are expressed in the same metric ton equivalent using a defined FX rate model

- Prompt dates are normalized to a common calendar convention

- Margin obligations are calculated against a unified margin model, rather than exchange-specific models queried in sequence

How the Two Primary Breaks Interact

Ledger reconciliation failures and cross-exchange visibility gaps don't operate independently. They interact, multiplying exposure through a specific, traceable failure chain:

- An LME position carries a reconciliation break: execution-confirmed, settlement-pending, incorrectly marked as fully settled

- That position feeds into the cross-exchange consolidation layer

- The NCEL ingests a broken position record

- The consolidated position view reflects incorrect data—not a normalization failure, but corrupted input

- Every calculation downstream—delta, basis, margin—executes against bad inputs

This interdependency is why the solution architecture must treat these two components as a unified system. An NCEL without a properly functioning USE feeding it is only as reliable as the worst-reconciled exchange position in the book.

The Position Integrity Stack: Architecture That Addresses Both Breaks

When a Unified Event State Engine and a Normalized Cross-Exchange Position Ledger operate together, they form a Position Integrity Stack: the infrastructure on which every active position management, risk analytics, and reporting capability must be built.

The stack operates in a defined sequence:

- Event capture layer: Every trade event across every connected exchange is captured in real time with full audit metadata

- State resolution layer (USE): Events are sequenced and resolved against existing position state. No position is marked settled until settlement events confirm it

- Normalization layer (NCEL): Resolved positions are normalized to a common schema across exchanges, lot sizes, currencies, and calendar conventions

- Unified position state layer: A single, live position record per instrument exists at all times—queryable, auditable, and complete

How Position Visibility Connects to Ledger Integrity in Metals Trading

Position visibility and ledger integrity are the same problem viewed from different angles. Position visibility describes what the trader sees; ledger integrity determines whether what they see is accurate. A platform can achieve high position visibility—rich dashboards, multi-exchange views, real-time price overlays—while still carrying ledger integrity failures that render the visible data wrong. Both capabilities must be built on the same underlying event and normalization architecture to be simultaneously trustworthy.

What the Break Elimination Framework Reveals About Platform Selection

The break elimination framework—mapping specific workflow failures to named architectural components—exposes a flaw in how commodity trading platforms are typically evaluated.

Most platform evaluations focus on feature surfaces: Does it have an LME interface? Does it display real-time P&L? Does it support physical and financial position types? These are necessary questions, but they are the wrong starting point.

The correct starting point is the position integrity stack. A platform with every feature in the demo but no USE under the hood produces ledger reconciliation failures. A platform with multi-exchange dashboards but no NCEL behind them shows traders a consolidated position that is not, in fact, consolidated.

Gartner's Market Guide for CTRM software finds that fewer than one-third of evaluated CTRM platforms achieve high ratings on real-time position integrity across multi-exchange environments. Feature breadth is widely available. Infrastructure depth is not. Gartner CTRM market guide

What Is a Break Elimination Framework in CTRM?

A break elimination framework in CTRM is a structured methodology for identifying specific points where a trading system's operational state diverges from actual market exposure, and mapping each divergence to a defined architectural component that eliminates it. Unlike gap analysis, which identifies what is missing, break elimination identifies what is actively wrong and specifies the exact system component required to correct it. In metals trading, this framework consistently surfaces two primary break categories: ledger reconciliation failures and cross-exchange position visibility gaps.

This reflects the core principle of a depth-first approach to commodity intelligence: before a platform can deliver reliable analytics, reliable risk calculations, or reliable P&L attribution, it must achieve position integrity. Depth before breadth. Infrastructure before features. depth-first commodity intelligence methodology

The break elimination framework is not a diagnostic exercise that ends with a checklist. It is the design specification for what must be built.

The Architectural Question the Position Integrity Stack Creates

The position integrity stack—a USE feeding an NCEL, operating as a coherent infrastructure layer—defines the baseline requirement for reliable metals trading operations across LME, COMEX, MCX, and SHFE.

It is a necessary condition, but not a sufficient one.

| Break | Root Cause | Named Solution Component |

|---|---|---|

| Ledger reconciliation failure | Asynchronous event processing; batch-state position engine | Unified Event State Engine (USE) |

| Cross-exchange visibility gap | Exchange-native schema fragmentation; query-time aggregation | Normalized Cross-Exchange Position Ledger (NCEL) |

| Cascading P&L attribution error | USE/NCEL interdependency failure; corrupted input data | Position Integrity Stack (USE + NCEL as unified layer) |

Once a platform achieves real-time ledger reconciliation and normalized cross-exchange position consolidation, trading desks can shift attention from determining their position to executing strategy. This requires pricing intelligence native to the platform's position model—an integrated intelligence layer that treats position state and market intelligence as a single, unified data problem rather than a separate analytics layer querying data via API.

This demands a base metals pricing model built to be position-aware rather than market-reporting-aware, operating natively against a normalized, cross-exchange, real-time position state. The next layer of this architecture addresses that specific design problem directly. Novaex base metals pricing intelligence architecture