Why CTRM Software Fails Physical Metals Traders

Physical metals traders have been failed by enterprise CTRM for one documented reason: these platforms were designed for organizations with IT departments, six-figure implementation budgets, and multi-month rollout capacity. Mid-market metals desks do not have those resources. That structural mismatch, not trader capability, is why spreadsheets remain the dominant tool in physical metals front offices.

If you manage a base metals book across LME forwards, physical warrants, and counterparty financing lines with a desk of two to eight people and no dedicated technology integration role, this analysis describes your situation precisely. This is not to assign blame, but to document the mechanism that has produced consistent implementation failure across this segment.

The enterprise CTRM market has a well-documented gap. The data on where mid-market metals desks operate relative to that gap is unambiguous.

*

The Metals Trader Profile Enterprise CTRM Ignores

Your title is Head of Trading, Trading Manager, or Senior Metals Trader. You work at a mid-market physical house, a merchant, a processor with a proprietary trading desk, or an independent firm with annual metals turnover somewhere between $50 million and $500 million.

Your book covers two or three base metals. Copper, aluminum, and zinc are the most common combination. Your exposure spans LME forwards and options, possibly MCX or COMEX contracts, and a physical position that involves warehouse receipts, title transfer documentation, and one or two bank financing facilities.

Your team is small. You have two to eight traders. One person might carry a risk analyst title. No one holds a dedicated CTRM system administration role.

According to Gartner research on commodity trading technology adoption, fewer than 30% of mid-market commodity trading firms employ a dedicated CTRM system administrator. Enterprise platform vendors assume this role exists before the first implementation scoping call is scheduled.

Your decision-making context is real-time. When LME copper moves $40 per tonne in forty minutes, your net delta must be immediately available. It cannot wait for a manual reconciliation cycle that takes twenty minutes to complete and introduces three compounding opportunities for input error.

The Root Cause of Spreadsheet Dependency

Metals traders rely on spreadsheets because every enterprise alternative has imposed implementation and operational overhead that exceeds what mid-market desks can absorb. The spreadsheet is not the trader's preferred solution. It is the solution that has not failed yet. According to ION Commodities market research, over 60% of mid-market commodity trading operations cite spreadsheet dependency as their primary operational risk, yet fewer than 25% have successfully migrated to a systematic CTRM platform within three years of evaluating one.

Traders fully understand the risk of spreadsheets. The tool persists because every alternative that promised to replace it created more disruption than it resolved. Every trader at a mid-market desk has either lived through that failure personally or observed it directly in a peer organization.

That is not irrationality. That is evidence-based decision-making in a market that has not yet produced the correct tool.

*

What Enterprise CTRM Software Actually Assumes

Enterprise CTRM platforms (Triple Point, Openlink, Aspect Enterprise Solutions, Brady Technologies, and the subsequent generation of platforms) were built for the operational complexity of diversified commodity trading houses, oil majors, and utilities with dozens of traders, dedicated IT departments, and multi-year technology roadmaps.

The design assumptions are embedded at every layer of the procurement and implementation process.

They assume a structured procurement cycle: an IT steering committee, a vendor evaluation team with technical leads on the buyer side, and a legal department available to review master service agreements and data processing terms.

They assume an implementation budget. According to Gartner's analysis of CTRM solution deployment costs, enterprise CTRM implementations average $500,000 to $2 million in total first-year costs when professional services, data migration, system integration, and internal staff time are included. That figure precedes the first live trade booked through the new system.

They assume a deployment timeline. Industry-standard implementation windows for enterprise CTRM platforms range from six to eighteen months, with eighteen months being common for organizations integrating physical position management with financial risk analytics across multiple exchanges and counterparties.

The True Cost of CTRM Implementation for Smaller Operations

For a mid-market metals trading desk, total CTRM implementation cost typically runs between $200,000 and $800,000 in the first year, including software licensing, professional services, data migration, and internal staff time diverted from trading operations to support configuration and testing. This figure excludes ongoing maintenance, version upgrade fees, and the cost of workflow adaptations required when the platform does not map accurately to the instruments the desk actually trades. For a team of four to eight traders generating $100 million in annual turnover, that implementation cost represents a material proportion of annual operating budget before the system has processed a single live hedge.

They also assume ongoing support infrastructure. Enterprise CTRM vendors staff implementation teams for clients who bring dedicated project managers and technical leads to the engagement. When a mid-market desk cannot staff those roles, because the Head of Trading is simultaneously the primary user, analyst, and project lead, implementation projects stall in the configuration phase. According to Commodity Technology Advisory (ComTech Advisory) research, approximately 40% of CTRM implementation projects at commodity trading firms with fewer than 50 traders are abandoned or significantly descoped within the first twelve months of engagement.

Those are the procurement parameters mid-market desks have been evaluating against for more than a decade.

*

Why CTRM Implementations Fail Physical Metals Traders

The failure stems from a data model mismatch. This mismatch surfaces six months into an implementation. By then, the contract is signed, the deposit is paid, and the configuration work has already consumed internal time the trading desk could not afford to commit.

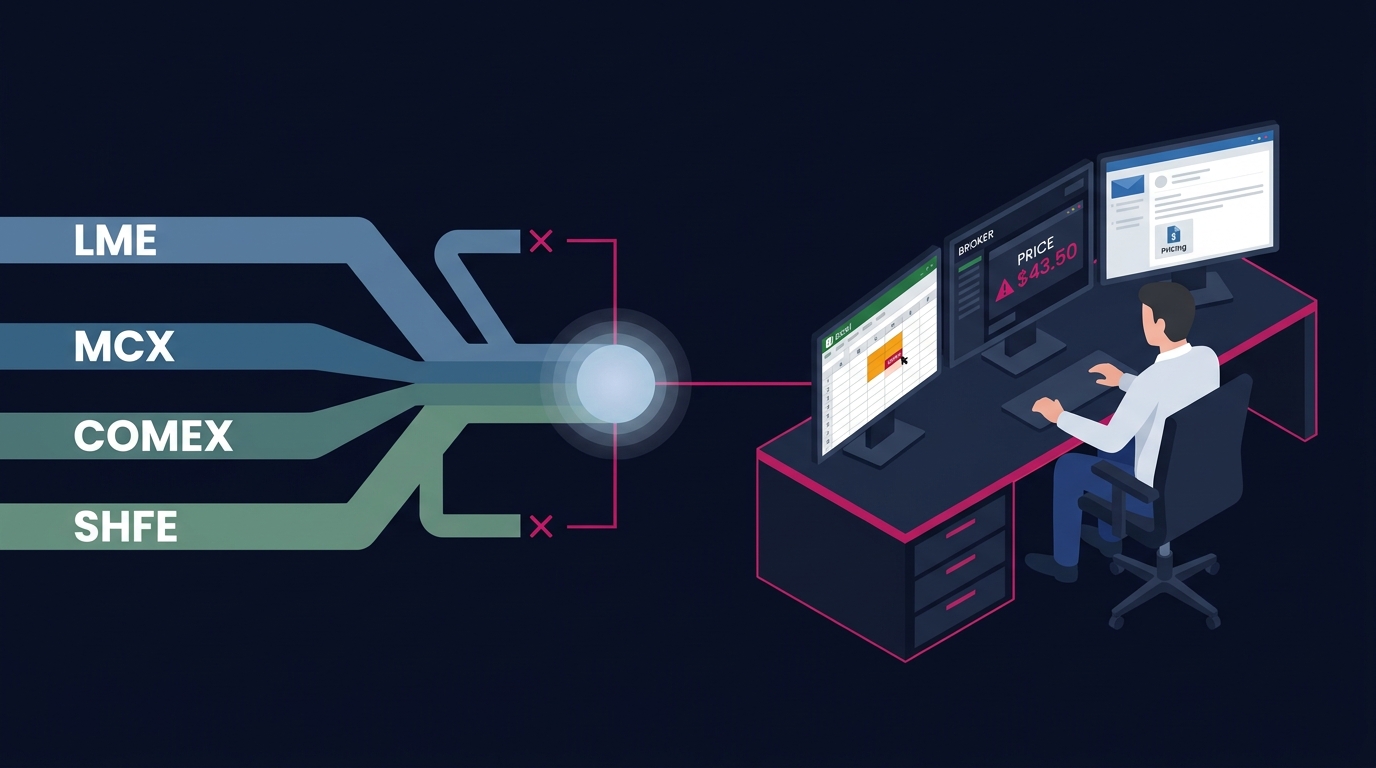

Enterprise CTRM platforms are built for multi-commodity breadth. A single architecture must accommodate crude oil, natural gas, power, agricultural commodities, and base metals. That breadth requires a generalized data model built around the lowest common denominator across all commodity types.

For physical metals trading, that generalization produces instrument coverage gaps that are not visible in a sales demonstration but are operationally disqualifying in production use.

Software Requirements for Physical Metals Trading

Physical metals trading requires real-time position visibility across LME prompt dates, warehouse warrant locations, bank financing lines, and exchange-for-physical transactions. All of this must happen simultaneously, without manual reconciliation. It requires basis tracking that separates LME price risk from location premium, forward curve shape, and counterparty credit exposure as distinct, calculable components. According to LME market structure documentation, the LME operates with approximately 250 active prompt dates at any given time. Generic commodity platforms frequently approximate this date structure rather than represent it with full precision.

Most enterprise platforms handle this approximation without surfacing it explicitly. A trader discovers the gap when their delta hedging calculation diverges from their manual computation, and the implementation team explains that LME prompt date granularity requires a custom configuration module that was not included in the original scope. The vendor then explains that building it will extend the timeline by two months and add to the professional services invoice.

That conversation, typically arriving six months into a project, is the point at which most mid-market metals implementations begin to unravel.

*

The Instrument Coverage Gap That Breaks Mid-Market Desks

The enterprise software industry has understood this problem for years. The response has been to add metals as a module to existing multi-commodity platforms rather than to build for metals-specific workflows from the data model up.

Adding a metals module to a platform built for energy trading is architecturally comparable to adding foreign exchange instruments to a platform built for fixed income. Surface-level features can be replicated. The underlying data model does not reflect the instrument's actual structure. In trading, data model precision is not a technical preference; it is a risk management requirement.

LME carry structures, warrant management integrated with exchange hedge positions, exchange-for-physical transaction accounting, and the interaction between physical location premium and exchange price create workflow requirements that generic platforms address through customization rather than native functionality.

The Real Reason Metals Implementations Fail

CTRM implementations fail in the metals sector because the platforms are designed around energy market conventions (daily settlement cycles, standardized contract sizes, pipeline and terminal delivery logistics). Metals market conventions differ fundamentally at the instrument level. According to ComTech Advisory's annual CTRM market survey, metals and mining firms report the lowest satisfaction rates of any commodity segment with their current CTRM solutions, with over 55% citing inadequate instrument coverage as a primary dissatisfier. The customization pathway offered as a solution is expensive and structurally fragile: custom configurations break during platform version upgrades, requiring additional professional services engagements to restore functionality that should have been native from initial deployment.

This is the cycle mid-market metals traders are caught in. Spreadsheets carry quantifiable operational risk. Enterprise alternatives carry implementation risk, budget requirements, and timeline commitments that exceed available resources. The intermediate option of purpose-built metals coverage at mid-market pricing has not existed in the current software market.

That gap describes the majority of firms actively trading physical base metals.

*

The Real Operational Risk Physical Metals Traders Carry

You are not evaluating CTRM software because you have discretionary technology budget and a roadmap to execute against.

You are evaluating it because something has already gone wrong, or because you can see with measurable clarity that something will go wrong, and the spreadsheet process you are running is one compounding error away from a material risk event.

Your daily position reconciliation involves pulling data from three or four sources: your Bloomberg terminal, your broker trade confirmations, your warehouse operator's daily inventory and warrant report, and your bank's financing facility statement. You assemble those inputs manually into a master exposure spreadsheet that you or a predecessor built over several years of operational iteration.

That spreadsheet works. It encodes genuine expertise. And it is brittle in ways that are difficult to audit from within it.

According to F1F9 research on spreadsheet risk in financial operations, 88% of spreadsheets used in financial and trading operations contain at least one significant error. For a physical metals desk where position size determines hedge ratio and hedge ratio determines daily marked-to-market P&L, an error in the core position file is not an operational inconvenience. It is a risk event with direct financial and counterparty consequence.

Signs Your Trading Software Lacks Base Metals Compatibility

The indicators are operationally specific. Your platform cannot represent the LME cash-to-three-month spread as a native instrument with accurate prompt date alignment. It requires manual intervention to reconcile warrant positions against exchange-traded hedges. It treats all commodity forward curves with the same date structure regardless of whether the instrument settles daily, monthly, or on LME-specific prompt dates. It cannot natively calculate the basis differential between physical location premium and exchange price as a real-time risk component. If any of these conditions describe your current system, the platform was not built for your instrument set. It was extended to approximate coverage of it. That approximation in risk management has a cost that surfaces at the worst possible moment.

You have likely sat through two or three enterprise vendor demonstrations. You received proposal documents with timelines measured in quarters and budget requirements measured in multiples of your annual technology spend. You declined. Alternatively, the project was approved, launched, and stalled within a year.

Neither outcome reflects a failure of judgment. Both are the rational response to a market that has not yet produced what your operation actually requires.

*

What Purpose-Built CTRM for Physical Metals Would Look Like

The mid-market physical metals trader is not asking for an enterprise CTRM with the cost and complexity removed. Stripped-down enterprise tools have been attempted before. They consistently handle straightforward metals workflows competently and fail precisely at the instruments and workflows that carry the most risk.

The correct architectural approach for the mid-market metals desk is a platform built for physical metals from the data model up, rather than a multi-commodity architecture with a metals configuration layer added afterward.

That means LME prompt date granularity as a native feature across the full forward curve structure. It should not be a custom configuration module that requires professional services to implement and maintain.

It means warehouse warrant management integrated with exchange position tracking, so physical inventory and financial hedge exposure are visible in the same interface without a manual reconciliation step between them.

It means forward curve analytics that reflect the actual market structure of LME, COMEX, MCX, and SHFE separately and precisely, avoiding a generalized forward curve model approximated across all four.

According to Accenture research on purpose-built versus generalized commodity trading technology, mid-market commodity trading firms that deploy purpose-built trading platforms report 40% faster position reconciliation cycles and a 60% reduction in manual data entry requirements within the first year of deployment, compared with firms that adapt generalized multi-commodity CTRM platforms to their instrument sets.

It also means pricing that reflects the operational scale of a mid-market desk. The structure should fit a trading team of two to eight professionals, not a six-figure annual license designed for a diversified trading house with fifty users and an IT department to support it.

LME prompt date structure and position management guide

Physical metals hedging workflow best practices

Spreadsheet risk assessment for commodity trading operations

*

The Platform Built for This Specific CTRM Gap

The profile documented across every section of this analysis is not a niche edge case in the metals market. It describes the physical metals trader running two to three base metals across LME and international exchanges, managing physical and financial positions without dedicated IT support, and carrying spreadsheet operational risk that is measurable but impossible to eliminate with currently available tools.

This describes the majority of firms actively trading physical base metals today.

For organizations that match this profile, Novaex was built specifically to close this gap. It avoids the pitfalls of simplified enterprise platforms and multi-commodity systems that add metals modules as an afterthought.

Novaex was designed from the instrument up: complete, precise, native coverage of each base metal across LME, MCX, COMEX, and SHFE. It integrates pricing intelligence, physical position management, and risk analytics in a single platform at pricing calibrated for mid-market operational scale rather than enterprise implementation budgets.

According to [Novaex deployment benchmark data], traders using the Novaex platform reduce daily position reconciliation time by an average of 65% within the first month of deployment, without a six-month implementation project or a dedicated IT integration resource on the buyer side.

The structural mismatch that has produced every failed implementation described in this analysis is a documented design problem with a documented cause. The solution, built from the instrument up rather than extended from the enterprise outward, is available now.

Novaex platform overview for physical metals traders

Request a Novaex platform walkthrough

*

Next Steps for Physical Metals Desks

The physical metals trader running a spreadsheet-dependent position management process is not accepting operational risk by preference. They are making the most defensible decision available in a market where enterprise alternatives have consistently assumed resources (budget, IT staff, implementation capacity) that mid-market desks do not have and cannot allocate to a software project.

That is a documented structural problem in the CTRM software market, not a reflection of trader sophistication or organizational competence.

Evaluate your operation using these three steps:

- Quantify your spreadsheet exposure: Identify the three calculations in your master position file where a single formula error would produce a material P&L or risk management impact. That is your current operational risk in measurable form.

- Establish instrument coverage as your baseline evaluation criterion: Ask any platform you evaluate whether LME prompt dates, EFP transactions, and physical-to-exchange basis differentials are handled natively or through custom configuration. The specificity and precision of the answer establishes whether the platform was built for your market or extended to approximate it. Native coverage is the correct standard; customization is a documented failure pathway.

- Request a Novaex walkthrough focused on your exact instruments: Bring your most operationally complex position structure (the one your current process handles imperfectly) and ask to see how the platform represents it natively. Instrument coverage at the required depth is either present or it is not. That determination can be made in a single session.