Base Metals Spreadsheet Reconciliation: The Accuracy Gap

Most trading desks have never formally measured the error rate embedded in their spreadsheet reconciliation workflows. According to research compiled by EuSpRIG (European Spreadsheet Risks Interest Group), 88% of spreadsheets in active use contain at least one material error. In base metals trading, where prices move across LME, COMEX, MCX, and SHFE simultaneously, a single stale cell or misapplied formula quickly impacts downstream calculations.

The assumption that manual base metals spreadsheet reconciliation is "accurate enough" persists primarily because the consequences remain latent until they materialize, rather than through testing against a defined standard.

This analysis documents the specific error rates and data-lag intervals that characterize spreadsheet-dependent workflows in base metals pricing, measuring each failure mode against the same metric on both sides for analytical credibility.

What "Accurate Enough" Means in Base Metals Pricing

In base metals trading, accuracy represents a tolerance interval measured against live market conditions.

A metals desk reconciling copper positions across LME and COMEX compares structurally different instruments. The LME copper cash price references a T+2 settlement date against a rolling prompt structure, while the COMEX copper futures price references a specific expiration month with fixed delivery terms. The basis between these two prices moves continuously throughout the trading day.

According to CME Group historical data, the LME-COMEX copper basis has ranged from -$200 to +$400 per tonne over rolling 12-month periods, driven by nearby futures positioning, exchange-specific warehouse dynamics, and physical delivery flows. This variance constitutes a live market signal.

A spreadsheet model that captures these prices at different times (even 15 minutes apart) compares two different moments in a moving market while presenting the result as a static position.

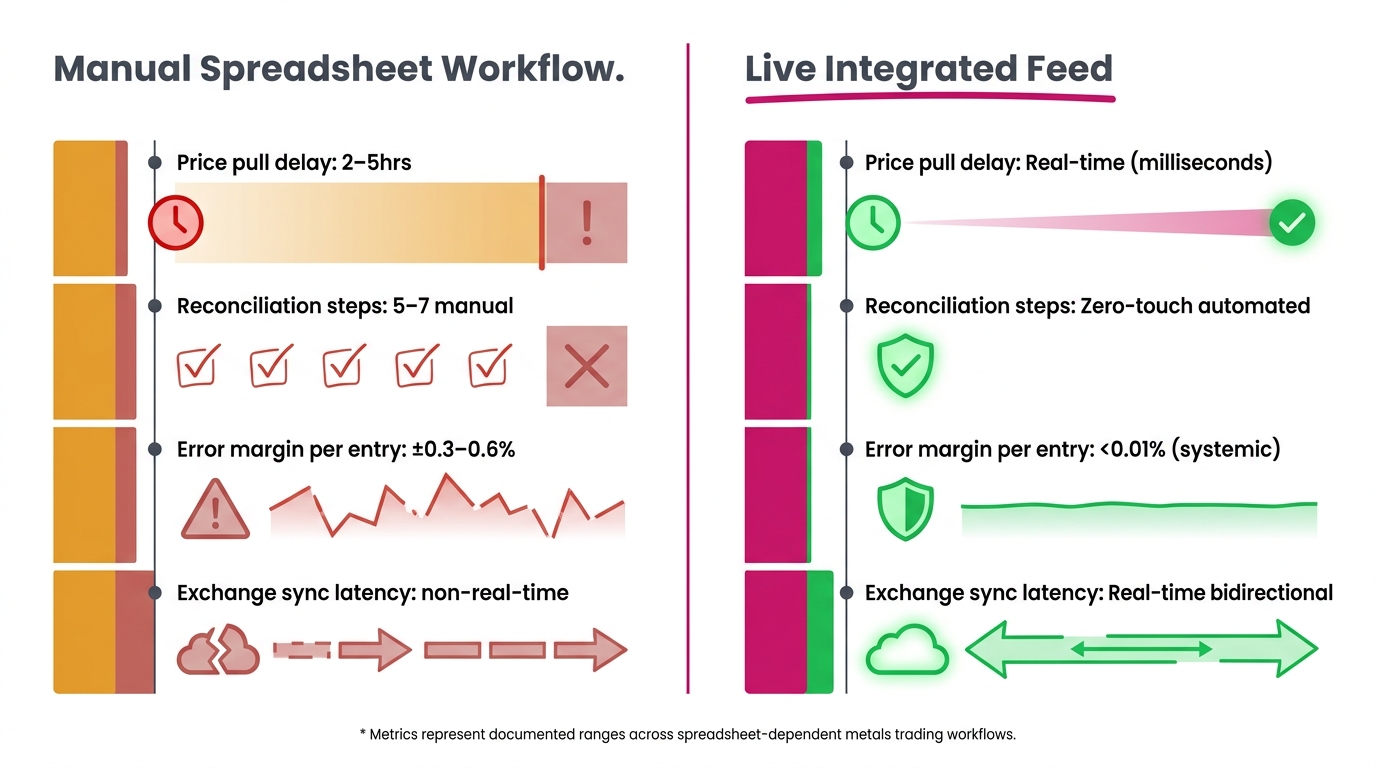

Data-Lag Tolerances in Metals Trading

For operational hedging decisions, adjusting delta hedges, sizing new positions, and calculating margin requirements, a data lag of more than five minutes introduces material basis uncertainty. For position marking, regulatory frameworks including FCA MAR guidance and CFTC Part 20 reporting expectations treat valuations as requiring prices as close to real-time as operationally feasible.

The practical benchmark requires a price that a counterparty would accept as current. Relying on the assumption that the market has remained static means the benchmark has already failed.

The practical standard for an active metals desk is sub-minute data refresh for live positions. Spreadsheet workflows, by design, cannot meet that standard without automated data feeds. When automated feeds are present, the spreadsheet itself becomes the failure point rather than the data source.

Documented Error Rates in Base Metals Spreadsheet Reconciliation

The research on spreadsheet reliability is not anecdotal. Professor Ray Panko of the University of Hawaii, whose peer-reviewed work on spreadsheet errors spans two decades, found that experienced users make errors in approximately 1% of individual cells in complex workbooks, with error rates rising to 5% for cells containing conditional logic, nested IF statements, or multi-step lookup functions.

Panko spreadsheet error research University of Hawaii

In a base metals reconciliation workbook, consider a conservative cell count: 12 price inputs across four exchanges and three metals, 8 basis spread calculations, 4 FX conversion cells, 6 lot-size normalization cells, and 15 position aggregation cells. That is 45 cells before risk summary outputs. At a 1% error rate, statistical expectation places at least one error in every third full reconciliation cycle.

EuSpRIG's compiled research across financial services institutions found that 88% of spreadsheets in active use contain at least one material error. A "material" error is defined as an error that would change a reported figure by more than 1% if corrected.

The Impact of Formula Errors on Hedging Positions

A formula error in a metals hedging spreadsheet typically manifests in one of three forms: a misaligned hedge ratio, an incorrect lot-size conversion, or a stale price carried forward from a prior session without being overwritten. Each affects delta exposure differently, but none announces itself through an alert or exception flag.

A copper position hedged at the wrong ratio by 2% (well within the statistical error range for a mid-complexity workbook) on a 500-tonne book translates to 10 tonnes of unintended exposure. At $9,000 per tonne, that is $90,000 in unhedged notional value that remains undetected in the position. The hedged P&L drifts from expected behavior. The investigation begins after the fact, when market conditions that created the drift may no longer be recoverable.

The error manifests as unexplained P&L attribution, allowing it to persist across multiple update cycles before identification.

Data-Lag Intervals in Multi-Exchange Spreadsheet Workflows

Error rates address accuracy at a single point in time. Data lag addresses the accuracy of timing: the interval between when a price exists in the market and when it appears in a reconciliation model.

In a spreadsheet-dependent workflow, data lag accumulates across three compounding sources:

- Source extraction delay: The interval between a live market price and its delivery to a workbook, including terminal refresh cycles, scheduled CSV exports, or manual screen reads.

- Manual entry delay: The time required to copy a price from a source into a workbook. Independent studies on manual data entry in financial operations document average latencies of 3 to 5 minutes per full update cycle for multi-source reconciliation workflows.

- Model recalculation delay: In workbooks exceeding 50,000 cells with multiple chain dependencies, Excel recalculation time is measurable, particularly when triggered by the simultaneous update of multiple input cells.

Structural Data Lag Between LME and COMEX Settlements

The LME sets its official copper cash price during the second ring session, which closes at approximately 12:50 PM London time. COMEX copper settles at 12:00 PM New York time (17:00 GMT during British Summer Time and 16:00 GMT during standard time). This places COMEX settlement 4 to 5 hours after LME official prices are declared, depending on the time of year.

A spreadsheet that uses LME official prices alongside COMEX settlement prices in the same reconciliation model is structurally comparing prices from different points in the trading day. This lag is structurally built into the settlement architecture of the exchanges themselves. Any reconciliation model that does not account for this through intraday pricing rather than settlement pricing is measuring a gap it has not defined.

SHFE adds a further structural consideration: its afternoon session closes at 3:00 PM CST, which is 7:00 AM or 8:00 AM London time, before LME ring trading has opened. Any SHFE price used in a same-day LME reconciliation is, by definition, from a prior session.

Cross-Exchange Arithmetic: Where Spreadsheet Models Break Down

The LME, COMEX, SHFE, and MCX do not share a common price infrastructure. Each exchange specifies distinct lot sizes, pricing currencies, settlement conventions, and contract structures. Every cross-exchange comparison requires a chain of conversions before the comparison carries analytical meaning.

- LME copper: USD per tonne, 25-tonne lots, cash-to-3-month rolling curve

- COMEX copper: USD per pound, 25,000-pound lots (~11.34 tonnes), monthly futures expiration

- SHFE copper: CNY per tonne, 5-tonne lots, monthly expiration with bonded/non-bonded delivery distinction

- MCX copper: INR per kilogram, 1-tonne lots, monthly expiration

A spreadsheet reconciliation must execute unit conversions (pounds to tonnes, kilograms to tonnes), currency conversions (CNY/USD, INR/USD at the appropriate rate and timestamp), lot-size normalizations to a common unit, and prompt-date alignment across four distinct settlement structures simultaneously, correctly, and in every update cycle.

LME, SHFE, and COMEX Price Divergence

The LME-SHFE spread, sometimes referred to as the "China premium", reflects Chinese import arbitrage economics: bonded warehouse stocks, VAT treatment on imported copper, SHFE delivery specifications, and CNY/USD cross-rate movements. It is a genuine market signal. The LME-COMEX spread, by contrast, reflects North American physical delivery premiums, COMEX warehouse positioning, and dollar-denominated futures curve dynamics.

In a spreadsheet model, a formula error in the CNY/USD conversion rate or the SHFE lot-size normalization produces a number that resembles a spread move. Distinguishing a real basis shift from a calculation artifact requires auditing the model before acting on the signal. This introduces a workflow cost that exists solely because the tool is not designed for the task.

According to research published in the Journal of Applied Finance, currency conversion errors account for approximately 23% of identified errors in multi-currency financial spreadsheet models. In a four-currency base metals reconciliation, that error vector is present in every single update cycle.

How Errors Compound Across a Live Metals Book

A single pricing error in a base metals spreadsheet does not remain contained at the instrument level. Position management workbooks are hierarchical: instrument-level prices feed lot calculations, which feed position summaries, which feed margin estimates, which feed risk-limit utilization monitoring.

At each aggregation level, an upstream error multiplies by the weight of the downstream calculation.

Consider a 1% price error on copper in a multi-metal book where copper represents 60% of gross notional exposure. If total book notional is $50 million, copper notional is $30 million. A 1% copper price misstatement produces a $300,000 error in position value, which then flows into every downstream output: P&L, delta, margin utilization, and limit headroom. A risk manager reviewing limit utilization against a $300,000-distorted position summary is making decisions against a model that has already failed.

According to operational risk guidance from the Basel Committee on Banking Supervision, model errors (including spreadsheet-based calculation errors) are among the top three sources of documented operational loss events in commodity trading operations.

Basel Committee operational risk in commodity trading

The True Cost of Spreadsheet Errors

The direct cost of a spreadsheet error is the P&L impact of the decision made on incorrect information. The indirect cost, which is harder to quantify but consistently larger, includes the time spent investigating unexplained P&L attribution, the after-hours reconciliation needed to close positions correctly, and the erosion of confidence in a risk system that has produced incorrect outputs.

A 2019 survey by Accenture found that commodity trading professionals spend an average of 14 hours per week on manual data management and reconciliation tasks. This time is entirely unproductive from a market-participation standpoint and directly attributable to workflow architecture rather than market complexity.

At a fully-loaded cost of $150/hour for a front-office professional, that is $2,100 per week, per trader, in workflow friction. Across a desk of five traders, that is over $500,000 annually in costs that exist only because the reconciliation tool is not fit for purpose.

Base Metals Reconciliation: What Accurate Actually Requires

The measurement is direct: manually maintained base metals spreadsheet reconciliation degrades as a function of the number of data sources it must integrate, the frequency of update cycles it must sustain, and the formula complexity required to normalize cross-exchange data into comparable outputs.

Accurate base metals reconciliation across LME, COMEX, SHFE, and MCX requires a defined set of operational capabilities:

- Sub-minute price refresh from all four exchanges simultaneously, without manual extraction steps

- Automated unit, currency, and lot-size normalization with auditable, timestamped conversion rates

- Prompt-date alignment logic that accounts for LME rolling prompt conventions versus COMEX and SHFE fixed expiration months

- Immutable calculation logic that cannot be overwritten by manual entry or cell-level editing

- Full audit trail that timestamps every price capture, flags data gaps, and records every change to position inputs

None of these requirements are technically unachievable. All of them are operationally impractical in a spreadsheet environment because a tool built for general-purpose calculation is being used as a substitute for purpose-built reconciliation infrastructure.

Metals trading desks must evaluate how many update cycles they complete with a statistically predictable error rate before the consequences become visible in P&L, rather than assuming theoretical capability under ideal conditions.

Conclusion: The Numbers Define the Standard

The case against "accurate enough" relies on consistent statistics across independent research streams.

88% of spreadsheets contain material errors. A 1% cell error rate compounds at every aggregation level in a position book. Manual data entry introduces 3 to 5 minutes of lag per cycle. LME-to-COMEX settlement architecture creates a structural 4 to 5 hour divergence window. SHFE closes before LME opens. Currency conversion errors account for 23% of identified errors in multi-currency models. Manual reconciliation tasks consume an estimated 14 hours per trader per week.

These figures provide a measurement standard. A trading desk that can document its reconciliation workflow against each of these metrics (and demonstrate that its error rates and lag intervals are within defined tolerances) has evidence of accuracy. A desk that has never measured these variables operates on assumption alone.

Three steps to quantify your own exposure:

- Audit one week of reconciliation workbooks: Record every manual cell override, identify its downstream effect, and calculate the aggregate notional exposure it touched.

- Measure your actual data-lag interval: Time the interval between a price move on LME and the moment that move appears in your live position model, including extraction, entry, and recalculation time.

- Apply the 1% error rate to your largest position: Identify the dollar figure that sits in the statistical error window of a single update cycle, then decide whether that figure is an acceptable operational risk.