Multi-Exchange Basis Calculation: One Formula, Two Exchanges

When a procurement contract references both LME official settlement and COMEX closing prices, the formula is a precision instrument. Multi-exchange basis calculation requires treating each exchange price as a structurally distinct variable. Pulse's formula engine resolves both within a single contract formula, eliminating manual price table maintenance without conflating two fundamentally different settlement mechanisms.

The critical gap in most platforms is missing architecture, not missing data. This post traces the engineering problem from its root: two exchanges, two settlement mechanisms, one contract formula that must honor both without approximation.

Why LME Official Settlement and COMEX Closing Are Not Interchangeable

The foundational error in multi-exchange formula design is treating "copper price" as a single reference type. Every price reference in a procurement contract carries identity: the exchange that produced it, the mechanism that settled it, the time at which it became final, and the unit in which it is expressed.

LME official settlement is determined during the Ring session at 13:00 London time. It represents the prompt-date cash price established through open-outcry trading. This formally published benchmark carries specific legal weight in physical contract settlement. The LME quotes copper in USD per metric tonne.

COMEX closing price is the settlement price of COMEX copper futures, determined at market close at approximately 13:00 ET (which is 17:00 or 18:00 London time depending on daylight saving time). COMEX quotes copper in US cents per pound. The two prices describe the same underlying metal, but they are structurally different instruments produced by different mechanisms at different times in different units.

What is the difference between LME official settlement and COMEX closing price?

LME official settlement is a cash price set during a specific Ring session at 13:00 London time, while COMEX closing price is a futures settlement determined at market close in New York, five to six hours later. The structural differences in timing, contract basis, currency unit, and pricing convention mean the two prices cannot be used interchangeably in a formula without explicit, variable-level resolution logic.

According to the London Metal Exchange, official settlement prices are published following the Ring session and serve as the contractual benchmark for the majority of global physical metal transactions LME settlement methodology. This is a formally published price with a defined legal function rather than a spot quote pulled from an electronic feed.

The unit difference alone introduces compounding risk. With copper trading around $9,000 per metric tonne on the LME LME copper price data, the COMEX equivalent in cents per pound must be converted using the precise factor of 2,204.623 pounds per metric tonne. A rounding error introduced at the conversion step propagates through every cost-of-metal calculation the contract generates.

The Structure of a Procurement Contract That References Both Exchanges

Not every procurement contract references both exchanges. Dual-exchange references appear when the buyer's cost exposure is split: dollar-denominated physical delivery obligations priced against COMEX, and LME-linked financial hedges held on the London books. The contract formula then becomes a weighted expression of both settlement mechanisms within a single instrument.

A simplified representation of this structure looks like:

Contract Price = [LME Official Settlement × Weight_LME] + [COMEX Closing × Conversion Factor × Weight_COMEX] + Fabrication Premium

Each bracketed term is its own resolution problem. The LME official settlement must be sourced from the correct Ring session on the correct pricing date. The COMEX closing price must reference the correct contract month and be converted to the correct unit before the formula evaluates.

How do procurement contracts reference multiple exchange prices?

Multi-exchange procurement contracts assign specific price references to each exchange using defined pricing periods, contract months, and weighting factors. The formula structure must preserve the identity of each price reference, treating LME official settlement and COMEX closing price as separately resolved values instead of interchangeable inputs or proxies for one another.

According to a 2023 report by the International Copper Study Group, approximately 70% of physical copper transactions reference the LME cash price as their primary benchmark, while a significant portion of North American contracts incorporate COMEX references for local delivery and fabrication premium structures ICSG copper market report. The overlap between these reference populations is precisely where multi-exchange basis calculation becomes a contractual requirement rather than an edge case.

The Engineering Problem: Multi-Exchange Basis Calculation in Practice

The basis in a multi-exchange context is the spread between the LME-settled value and the COMEX-settled value, adjusted for units, timing, and contract month. This is not a static number that can be approximated. The LME-COMEX basis for copper has historically ranged from near-zero to over $150 per metric tonne during periods of regional market stress [LINK: copper basis spread analysis].

When a formula references both exchanges without explicit variable isolation, three specific failure modes emerge:

- Timing mismatch: LME official settlement is captured at 13:00 London; COMEX closes five to six hours later. If a system pulls prices from a single daily timestamp rather than respecting each exchange's settlement time, it introduces a structural error before the formula has even run.

- Unit conflation: Treating COMEX cents-per-pound as equivalent to LME dollars-per-tonne without precise conversion produces a number that is mathematically coherent but commercially incorrect. The formula executes cleanly and returns an invalid result.

- Contract month misalignment: LME cash and COMEX front-month futures do not always reference equivalent delivery periods. Assigning COMEX M1 where LME 3-month is contractually intended misprices the basis by the full term structure spread. This number can exceed $30 per metric tonne in backwardated markets.

What causes errors in multi-exchange basis calculations?

Errors in multi-exchange basis calculations originate from three structural sources: timestamp mismatches between exchange settlement times, unit conversion failures between LME dollar-per-tonne and COMEX cent-per-pound conventions, and contract month misalignment between LME cash or 3-month tenor and COMEX futures months. Each failure mode is a formula architecture problem, meaning better data feeds alone do not resolve it.

A 2022 analysis by Accenture's commodity risk practice found that manual data handling in commodity trading and procurement workflows contributes to pricing errors in approximately 34% of contract reconciliations Accenture commodity operations report. In multi-exchange contracts, that error rate compounds because each exchange introduces its own source dimension, timing dimension, and unit dimension, creating three independent failure surfaces operating simultaneously.

How Pulse's Formula Engine Isolates Each Exchange Variable

Pulse's formula engine is built on the principle that every price reference in a contract formula must be resolved independently before it participates in a calculation. This functions as a structural requirement for formula correctness in any multi-exchange basis calculation.

Each variable in a Pulse formula carries four attributes assigned at the variable level, not inside the formula expression:

- Exchange identity: LME, COMEX, MCX, SHFE: resolved as a named exchange source rather than a generic price feed

- Settlement type: Official settlement, closing price, fixing, or index: each settlement mechanism treated as a distinct type

- Pricing date rule: Which session, which date offset, which pricing period average applies to this specific variable

- Unit and currency normalization: Applied at the variable level before the formula evaluates, so the formula never performs conversion arithmetic

Can a single formula handle both LME and COMEX reference prices?

Yes, but only if the formula engine resolves each exchange reference as a structurally isolated variable. Pulse achieves this by assigning exchange identity, settlement type, pricing date rule, and unit normalization to each price variable before formula evaluation. The formula then operates on normalized, comparable values rather than raw exchange outputs requiring in-formula transformation.

This architecture makes the formula structure auditable in a way that conversion-inside-formula designs cannot achieve. A trader reviewing the contract can trace each variable back to its exact exchange source, settlement timestamp, and normalized unit without reconstructing any intermediate steps. According to the CME Group, disputes arising from settlement price discrepancies in physical delivery contracts represent a consistent source of counterparty friction in base metals markets CME Group metals settlement documentation. Variable-level resolution eliminates the ambiguity at the source of that friction.

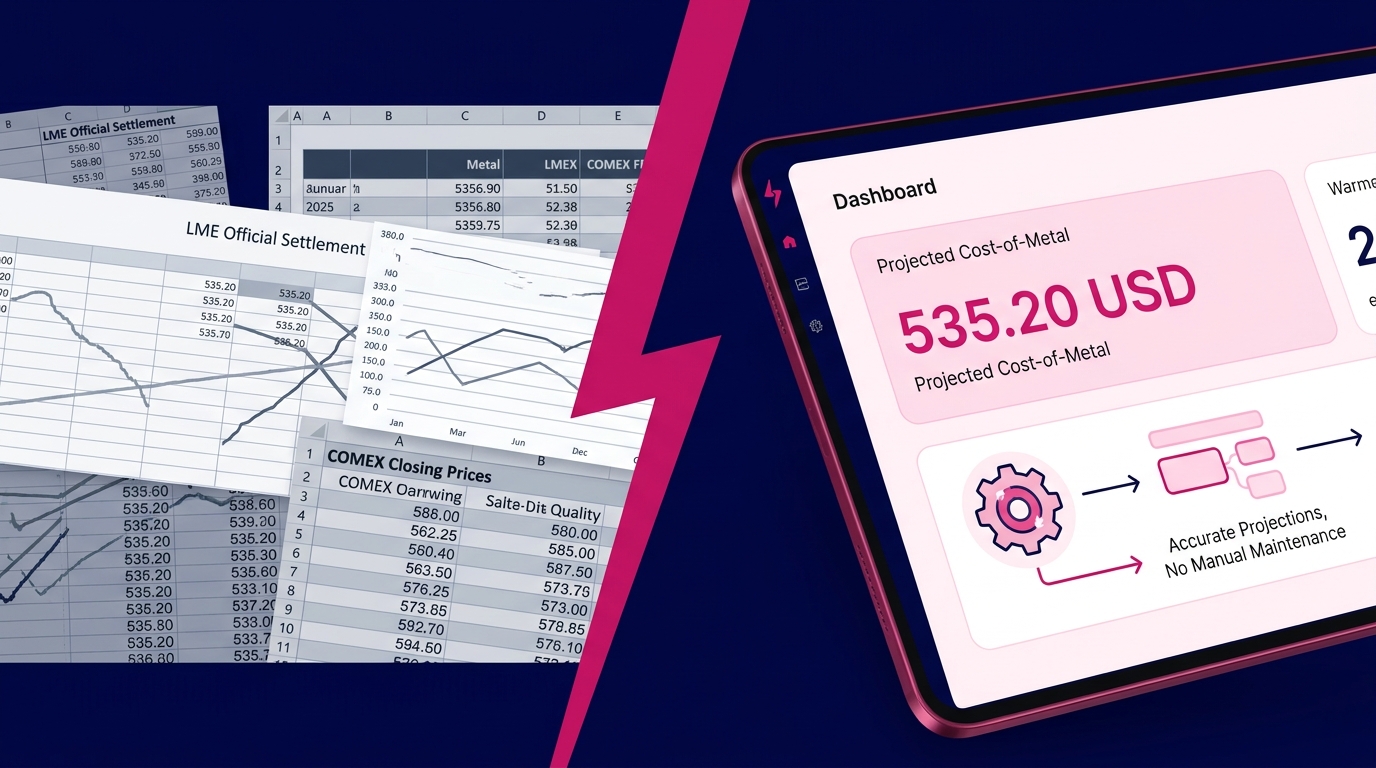

Eliminating Manual Price Table Maintenance Through Formula Architecture

Manual price table maintenance is the legacy response to multi-exchange complexity. The workflow is familiar to anyone who has managed it: download LME settlement files after 13:00 London, download COMEX settlement files after 18:00 London, perform unit conversion, reconcile pricing dates, paste values into a pricing model, run the contract calculation, and check for errors before the next session.

This workflow presents two compounding problems. First, it is operationally slow. By the time prices are reconciled across two exchanges, the window for accurate forward projections has often closed. Second, it is structurally fragile. Each manual step is an independent opportunity for the unit conversion, date offset, or contract month assignment to produce a plausible but incorrect output.

How does a formula engine eliminate manual price table maintenance?

A formula engine eliminates manual price table maintenance by connecting price variables directly to exchange data feeds, applying settlement type, pricing date rule, and unit normalization automatically at the variable level. The formula evaluates against current resolved data without requiring a human to retrieve, convert, or reconcile prices between sessions or across exchanges.

According to a 2021 ISDA operational risk survey, manual data handling in financial and commodity contract workflows increases operational risk exposure by an estimated 40% compared to automated feed-driven processes ISDA operational risk report. For procurement contracts with daily pricing windows, that exposure compounds session by session. Each manual reconciliation introduces a new risk event.

Pulse's integration with LME official settlement data and COMEX closing prices functions as a formula input layer rather than a data display layer. When LME publishes official settlement following the 13:00 Ring session, that value becomes an available resolved input for any formula variable referencing LME official settlement. When COMEX closes in New York, the same occurs for COMEX variables. The formula evaluates only when both inputs are resolved, avoiding stale data from a previous session.

Multi-Exchange Basis Calculation as a Traceable Audit Chain

The downstream benefit of structurally isolated variables extends beyond formula accuracy. It produces auditability as a natural architectural output. In procurement contracts, that auditability is not optional. When a counterparty disputes a contract price, resolution depends on demonstrating exactly which settlement price was used, from which exchange, on which pricing date, under which pricing period rule.

A formula engine that resolves variables independently generates that audit chain without requiring reconstruction. Pulse's formula log captures each calculation at four levels:

- Variable resolution timestamp: When each price variable was resolved against its exchange data source

- Settled value and raw unit: The exact value as published by the exchange, in the unit in which it was published, before normalization

- Normalized value: The value after unit and currency normalization, before formula evaluation. This represents the intermediate step most legacy systems cannot reproduce

- Formula evaluation output: The calculated contract price, with each resolved variable and its contribution visible

A 2023 Deloitte survey of commodity trading operations found that 58% of post-trade disputes in physical metals markets involved disagreements over pricing period application or price source interpretation [LINK: Deloitte commodity post-trade operations report]. A traceable formula architecture with variable-level resolution logs directly reduces the surface area on which those disputes can form.

Cost-of-Metal Projections Are Only as Correct as the Formula That Generates Them

The formula mechanics described throughout this post serve a single commercial purpose: producing accurate cost-of-metal projections. That purpose is downstream of everything else discussed here, and it is entirely dependent on the formula structure being correct.

A cost-of-metal projection built on a formula that conflates LME official settlement with COMEX closing, or that performs unit conversion inside the formula rather than at the variable level, carries structural error that compounds across a portfolio of contracts and across time. The output has the appearance of a projection. It functions as noise.

With properly isolated multi-exchange variables, Pulse generates cost-of-metal projections that reflect the exact settlement logic of each referenced exchange. A procurement team running forward projections against a pricing curve sees LME-referenced exposure valued at LME settlement rates and COMEX-referenced exposure valued at COMEX closing rates, avoiding a blended approximation that obscures which exchange is driving cost in any given period.

Base metals procurement operations managing contracts worth $50 million or more annually can see cost-of-metal variance exceeding $500,000 from a single misapplied unit conversion factor compounded across a year of daily settlements base metals procurement cost modeling. The formula architecture serves as the concrete mechanism that determines whether projections are commercially actionable or require manual adjustment before they can be used.

The Architectural Argument

Multi-exchange basis calculation requires a specific formula architecture. This architecture isolates exchange variables, resolves settlement type and unit normalization before formula evaluation, and generates a traceable resolution chain as a structural output.

Most platforms fall short of this standard not because of data access limitations, but because of formula design decisions. When a system treats price as a single variable type regardless of exchange source, it transfers the structural resolution work to the user. Manual price table maintenance is not a workflow inefficiency. It is the symptom of a formula architecture that delegates its own responsibilities to a spreadsheet.

Three concrete steps for procurement teams to take now:

- Audit your current multi-exchange formula structure: Identify whether your formula performs unit conversion inside the expression or at the variable level. This single distinction determines your structural error exposure in every contract that references both LME and COMEX.

- Map your settlement type references: Confirm that LME official settlement and COMEX closing price are referenced as distinct settlement types in your contract terms instead of generic daily prices that a system can satisfy with any available quote.

- Test your pricing period audit trail: Request a variable-level resolution log for a recent multi-exchange contract calculation from your current system. If the system cannot produce one, dispute resolution depends on manual reconstruction. This manual work reintroduces exactly the error modes the formula was supposed to prevent.

Pulse formula engine technical overview LME official settlement data integration COMEX closing price feed documentation multi-exchange contract configuration guide