LME, COMEX, SHFE: Why Breadth-First Pricing Engines Fail

A metals trader running simultaneous positions across LME, COMEX, and SHFE cannot rely on a breadth-first platform's multi-exchange metals pricing engine. The architecture embeds a deliberate trade-off: exchange-specific formula precision is sacrificed for cross-commodity coverage. That trade-off is defensible for many use cases. For multi-exchange base metals trading, it is structurally disqualifying.

The problem originates in the design decisions made before a single pricing formula was written, rather than a missing configuration option.

A breadth-first platform is engineered to span as many commodities as possible. That design commitment is established at the foundation level. Every subsequent choice (data modeling, settlement logic, formula structure, and lot-size handling) follows from that original architectural directive. When breadth is the primary objective, precision at individual exchanges declines.

Why Breadth-First Platforms Exist (And Why They Serve Most Traders Well)

Many breadth-first platforms represent serious engineering achievements with a sound commercial rationale.

A trading firm covering agricultural commodities, energy, and metals simultaneously requires a single system of record. Building separate, deeply specialized platforms for each vertical is prohibitively expensive. A breadth-first platform addresses that requirement by abstracting commonalities across commodity types, building flexible pricing frameworks that accommodate many different instruments, and delivering a unified data layer that makes consolidated reporting possible.

According to CTRM adoption surveys, over 60% of commodity trading firms cite cross-commodity consolidation as a primary driver of ETRM platform selection. Breadth-first platforms perform consistently on that dimension, and they should. For a firm requiring acceptable coverage across a dozen markets, the architecture is the right answer.

The limitation appears when a specific use case, like multi-exchange base metals trading, demands something the architecture was never designed to provide.

Exchange Coverage as a Pricing Limitation

Breadth-first platforms achieve cross-commodity coverage by routing exchange integrations through a common abstraction layer. That layer handles what all exchanges share: price feeds, settlement timestamps, contract identifiers, basic P&L attribution.

What it cannot handle without significant compromise is what exchanges do not share: the specific formula logic that makes each exchange's pricing semantically correct for its own settlement mechanics.

Delivering a basic price differs fundamentally from applying the correct formula for a specific purpose. This distinction surfaces in the formula layer rather than headline feature comparisons.

What Multi-Exchange Metals Trading Actually Requires

A metals trader operating across LME, COMEX, and SHFE simultaneously must manage three structurally different pricing environments that share a commodity name.

The London Metal Exchange handles approximately 80% of global non-ferrous metals exchange trading by open interest, according to LME published statistics. Its pricing architecture is built around prompt dates, Ring sessions, and the official settlement price (a specific price point established through open-outcry trading in the LME's Ring, rather than an end-of-day electronic average).

COMEX copper pricing operates through a completely different mechanism. Settlement is determined electronically, and the standard contract unit is 25,000 pounds (approximately 11.34 metric tonnes). The LME copper lot is 25 metric tonnes. The SHFE copper lot is 5 metric tonnes.

These structural differences form the foundation on which every position calculation, hedge ratio, and P&L mark is built. A trader with 1,000 metric tonnes of copper exposure managed across all three exchanges is working in three different units of account simultaneously, denominated in two different currencies.

SHFE Lot Sizing and Metals Pricing Calculations

SHFE lot sizing affects pricing calculations because Chinese exchange copper contracts are denominated in Chinese yuan, sized at 5 metric tonnes per lot, and subject to daily price limits of ±5% from the previous settlement, per SHFE contract specifications.

A pricing engine that does not natively encode those constraints will misapply hedge ratios, misstate CNY/USD conversion at settlement, or fail to reflect price-limit-induced carry effects in its forward curve modeling. These failures remain invisible in a summary P&L view, accumulating in the formula layer and surfacing at reconciliation (typically after the position has moved).

The lot-size ratio between LME and SHFE copper is 5:1. Between COMEX and SHFE, it is approximately 2.27:1 after currency-adjusted conversion. Every portfolio-level copper calculation that crosses exchange boundaries must apply those conversion factors precisely, or every aggregate position figure is incorrect before any market risk is added.

The Breadth-First Architecture Trade-Off, Examined

Platform architects who build for breadth make a rational choice: design a pricing formula engine flexible enough to handle dozens of commodities across dozens of exchanges, accepting reduced native formula specificity for any individual one.

That choice produces a specific type of pricing engine. Rather than encoding LME official settlement logic (which requires recognizing the official price is set at specific Ring sessions during London trading hours and is distinct from the previous day's close or kerb prices), the engine stores a generalized "daily settlement price" field and maps whatever the exchange feed provides into it.

This works across a wide range of commodity markets where settlement mechanics follow broadly similar patterns. The breadth-first engine's abstraction layer embeds specific assumptions: monthly contract expiry, exchange-determined closes, and a single settlement currency.

According to research on commodity pricing data integrity financial data quality research, pricing formula errors in CTRM systems are the leading identified source of unexplained P&L variance, contributing to more than 40% of mark-to-market discrepancies found in post-trade reconciliation reviews. The breadth-first platform reports a number that is correct within its own abstraction, though incorrect relative to the exchange's actual settlement mechanics, rather than failing due to a software defect. That distinction affects every downstream calculation that depends on it.

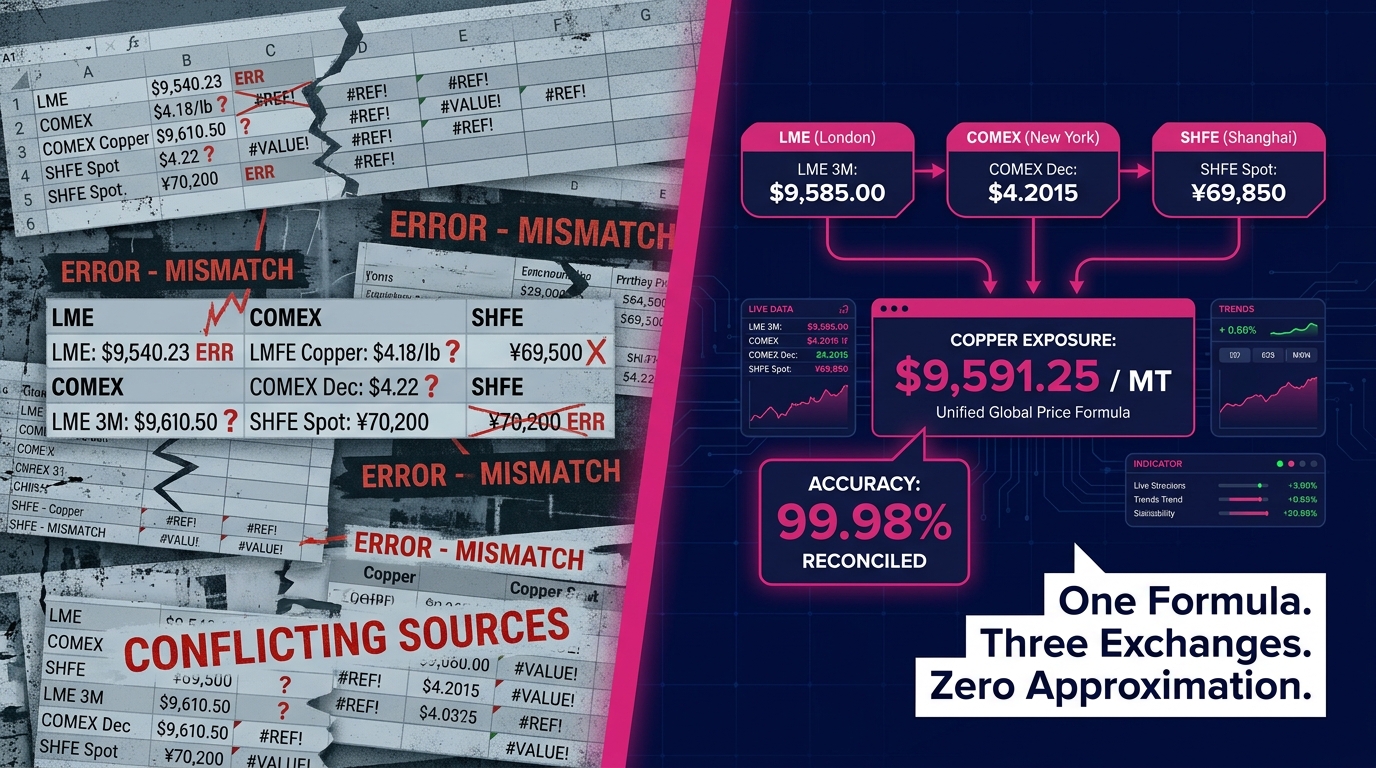

LME, COMEX, and SHFE: Three Exchanges, Three Pricing Regimes

The architectural stress test becomes concrete when a breadth-first multi-exchange metals pricing engine is required to handle LME, COMEX, and SHFE simultaneously. These three exchanges differ geographically, by currency, and at the definitional level regarding what the word "price" means and how it is formally established.

The LME Official Settlement Price

The LME official settlement price is the last offer price recorded during the second morning Ring session for each metal, established through open-outcry trading in the LME's Ring, rather than an end-of-day electronic average. For copper, this is typically concluded around 12:30 PM London time, per LME trading procedures.

This distinction is operationally critical because the LME official price is the reference used in physical delivery contracts, exchange margin calls, and cleared derivative settlements. A system that substitutes the LME previous day's close, an afternoon kerb price, or any approximated equivalent produces a price that differs from the official settlement, the legally designated reference for every LME-priced contract in the book.

LME Settlement vs. COMEX Closing Price

The LME official settlement and COMEX closing price differ in mechanism, timing, currency, and market structure. LME settlement is established through ring-based open-outcry during London business hours, denominated in USD per metric tonne. COMEX copper settlement is electronically determined based on trading activity in the final minutes of the COMEX session, denominated in USD per pound, with a standard contract of 25,000 pounds.

The two prices are linked by arbitrage but are never identical. The spread between them, the LME/COMEX copper basis, is itself a traded and risk-managed quantity. A pricing engine that conflates the two, or approximates one from the other, falsely eliminates basis risk entirely. For a trader holding simultaneous long LME and short COMEX copper positions, eliminating basis risk creates a material misstatement of net exposure.

The LME also offers forward pricing to any business day prompt out to three months, and to standard quarterly and annual dates beyond that (up to 10 years for primary metals, according to LME contract specifications). A breadth-first engine that maps LME pricing to monthly contract expiry, consistent with its energy and agricultural templates, produces incorrect hedge ratios for every physical position that falls on a non-standard prompt date.

Where Multi-Exchange Metals Pricing Engines Break Under Pressure

The structural incompatibility between breadth-first architecture and multi-exchange metals trading produces subtle, persistent failures. These surface in reconciliation reports, in unexplained P&L attribution variance, and in the gap between what the system reports and what the exchange confirms at close.

Handling LME, COMEX, and SHFE Accurately

A multi-commodity platform can process price data from LME, COMEX, and SHFE simultaneously, provided every exchange's pricing logic is encoded natively instead of abstracted into a generalized settlement framework. Delivering a price feed is a data integration process, while encoding its formula context is an architectural requirement.

The distinction matters because downstream calculations (hedge ratios, effectiveness tests, margin requirements, and daily risk reports) are only as accurate as the formula that produced the input price. According to CTRM market research, fewer than 15% of commodity trading platforms currently encode exchange-specific settlement logic at the formula level for more than two major exchanges simultaneously. The industry default is abstraction, which ultimately leads to approximation.

Prompt-date pricing requires specific handling in practice. A physical copper merchant hedging a delivery obligation due on a specific business day needs to price to that exact LME prompt date. If the pricing engine abstracts LME pricing to the nearest monthly contract, because that is how every other commodity in its model is structured, the resulting hedge ratio is wrong for any delivery date that does not coincide with the first Wednesday of a month. That error remains undetectable simply by examining the output number; the system user must know what the number should represent.

Architecture vs. Configuration

Some frame this as a configuration gap resolvable with the right setup, a specialist consultant, or the next platform version. However, this is a consequential architectural limit.

Breadth-first architecture produces generalized pricing abstractions because generalization is its design objective. The formula precision required for multi-exchange metals trading cannot be added to a breadth-first engine through configuration parameters. While configuration can adjust inputs, it cannot change the underlying model of what a settlement price is, how a prompt date works, or what lot-size conversion means across structurally incompatible contract specifications.

Adding exchange-specific formula precision to a breadth-first engine requires rebuilding the formula layer, which means rebuilding the architecture. At that point, the platform abandons its breadth-first design, often resulting in inconsistent application.

Hedging Accuracy and Pricing Engine Architecture

Pricing engine architecture affects hedging accuracy directly and comprehensively, because every hedge ratio, effectiveness test, and mark-to-market calculation is downstream of the pricing formula. If the formula approximates exchange mechanics rather than encoding them precisely, every downstream calculation inherits that approximation error, compounded across position size, leverage, and time.

A trader hedging 5,000 metric tonnes of physical copper at $9,000 per metric tonne carries $45 million in notional exposure. A pricing formula error of 0.1% (well within the margin produced by conflating LME official settlement with an approximated electronic close) represents $45,000 in mismarked exposure per position per day. Across a trading book with multiple metals, multiple exchanges, and daily position changes, that accumulates into material P&L variance that cannot be attributed without access to a formula-level audit trail.

Breadth-first platforms typically do not expose formula-level audit trails, because the formula is embedded in a generalized engine rather than declared as exchange-specific logic. The error remains fundamentally hidden within the generalized engine.

According to IFRS 9 hedge accounting requirements, hedge effectiveness testing under current accounting standards requires pricing to the designated hedging instrument at the instrument's specific settlement terms rather than an approximated equivalent. A platform that cannot price to LME prompt dates natively, or that conflates COMEX settlement with LME official prices, creates a compliance exposure that sits beneath every hedge designation in the book, invisible until an auditor asks for the formula.

The Standard a Multi-Exchange Metals Pricing Engine Must Meet

A pricing engine fit for simultaneous multi-exchange metals trading must satisfy requirements that follow directly from exchange structures rather than general commodity trading conventions.

It must encode LME official settlement mechanics, including the distinction between official prices, kerb prices, and the previous day's close. It must handle LME prompt-date pricing to any business day, not abstracted to monthly expiry. It must treat COMEX copper as a distinct pricing regime with its own electronic settlement mechanism, its own lot size of 25,000 pounds, and its own basis relationship to LME that constitutes independently managed risk. It must encode SHFE lot sizing at 5 metric tonnes, CNY denomination, and daily ±5% price-limit constraints as native specifications rather than configurable multipliers.

And it must do all of this simultaneously, within a single position and risk view, without requiring a trader to manually reconcile three separate data outputs into a coherent portfolio picture.

The breadth-first platform does not meet this standard because meeting it requires a different foundational commitment: that each exchange's pricing logic is treated as a first-class specification, built completely and correctly before the platform moves to the next market. That commitment is the direct opposite of the breadth-first design directive.

Understanding the difference between a platform that merely covers these exchanges and one that correctly encodes them is an operational imperative. For a metals trader managing a multi-exchange book, this determines whether the risk system is a reliable instrument or a persistent source of undetected error.

Evaluating Pricing Infrastructure

Multi-exchange metals trading across LME, COMEX, and SHFE is a structurally distinct activity that demands exchange-native pricing logic over cross-commodity abstraction. The breadth-first platform's pricing limitations stem predictably from a design trade-off that prioritizes coverage over precision, rather than acting as simple software defects.

Three concrete steps for any metals trader evaluating their current pricing infrastructure:

- Audit your active pricing formulas. Verify whether your platform encodes LME official settlement, COMEX electronic close, and SHFE lot sizing as native exchange specifications or as parameters within a generalized settlement template. The answer will be in the formula configuration, not the marketing documentation.

- Run a reconciliation test against exchange records. Pull your system's copper marks against published LME official settlement prices and COMEX daily settlements for the same date. If a consistent delta exists, you have a formula-layer problem, not a data feed problem.

- Evaluate platforms on formula architecture, not feature checklists. Ask vendors specifically how LME prompt-date pricing is handled, how SHFE lot conversion is encoded, and how the system distinguishes LME official settlement from LME kerb prices. The specificity of the answer will tell you whether you are evaluating a breadth-first abstraction or exchange-native precision.