LME Tom-Next Carry Modeling: No Manual Adjustment Required

LME Tom-Next carry is the daily cost of rolling an LME forward position one prompt date forward. Most CTRM platforms approximate it. Novaex models it natively, pulling actual LME forward curve spreads across each daily prompt date and embedding the result directly in your position view and P&L attribution, with no manual adjustment required.

If your platform is approximating carry, your hedge P&L is wrong before a single trade executes.

Most front-office metals teams rely on a workaround for this: a spreadsheet updated each morning, a configuration adequate for normal market conditions, or a tolerance for small carry discrepancies that eventually accumulates into a material error when the front curve inverts.

This post walks through exactly how Novaex handles LME Tom-Next carry: the specific data inputs, the named UI panels where the result appears, and the output your book reflects.

What LME Tom-Next Carry Actually Measures

The LME is structurally unlike any other major futures exchange. Where CME copper offers monthly expirations, the LME trades daily prompt dates from cash (T+2) through three months forward, then monthly to 27 months, and quarterly to 123 months for select metals. According to the LME's published contract specifications, copper alone carries over 240 tradeable daily dates in the front of the curve.

This structure is not a curiosity. It is operationally critical. Physical delivery on the LME occurs on a specific prompt date. When you hedge a physical position, you hedge to the exact date that metal moves. The spread between adjacent prompt dates is not an approximation of a monthly roll cost; it is the actual market price for one day of carry.

The Role of LME Tom-Next Carry

LME Tom-Next carry is the bid/offer spread between the "tomorrow" prompt date (T+1) and the "next" business day (T+2, the LME cash date). It represents one day of metal lending and borrowing cost and is the building block of the LME's daily forward curve. For metals traders, it matters because every prompt-date hedge uses this mechanism when rolled forward. Getting the rate wrong means mispricing the cost of carry and misreporting P&L.

The rate is not stable or predictable from first principles. During the LME nickel crisis of March 2022, Tom-Next spreads exceeded $1,000/MT per day, compared to typical copper levels of $0.10, $2.00/MT in normal market conditions. According to Bloomberg Commodities data, the LME suspended nickel trading for eight consecutive days as a direct consequence of extreme front-curve backwardation. A platform that models carry as a linear interpolation would have been catastrophically wrong across every open nickel position during that window.

LME Prompt Dates vs. Standard Futures Expiry

Standard futures (CME, NYMEX) expire on a fixed calendar convention: a third Wednesday, a last Friday, or a defined month-end. The LME has no equivalent. Every business day from cash to three months forward is a valid, liquid, independently quoted prompt date. A position booked to a Tuesday prompt date three weeks out is not rounded to a monthly expiry. It stays on that Tuesday, and the carry between that date and cash is the exact spread quoted in the LME ring or on LMEselect for that specific tenor.

This distinction collapses the monthly-expiry model that underpins most multi-commodity platforms. Any system that treats LME positions as monthly contracts is not modeling the LME.

Why Legacy Platforms Get LME Tom-Next Carry Wrong

Most CTRM platforms were built to handle energy and agricultural commodities, which are markets with monthly or seasonal contract structures. Base metals were added later, and the LME's daily prompt structure was mapped onto an existing monthly framework rather than rebuilt from scratch.

According to a 2023 Accenture Commodity Management survey, 68% of commodity trading firms reported that their CTRM system required manual intervention for at least one daily workflow. For LME base metals specifically, carry calculation is the most consistently cited manual step among front-office teams.

Common Carry Calculation Failures in Legacy CTRMs

Legacy platforms typically fail by interpolating the LME forward curve linearly between the cash date and 3M, dividing the total spread by the number of business days. This ignores the actual market-quoted spread for each individual daily date. They also require users to manually enter Tom-Next rates each morning, creating a data input risk and a workflow dependency that breaks under pressure. Additionally, they often round LME prompt dates to the nearest monthly period, which fundamentally misrepresents the position.

Each failure mode produces a different error signature in your book. Linear interpolation underprices carry in backwardated regimes and overprices it in steep contango. Manual entry introduces fat-finger risk and stale-data exposure between entry windows. Monthly rounding generates a phantom hedge basis that surfaces as unexplained P&L variance with no clean attribution trail.

The common thread: none of these are LME carry models. They are adaptations of models built for other markets, applied to a structure they were not designed to handle.

The operational cost is measurable. A front-office team running a 500-lot copper book across 15 prompt dates may spend 45, 90 minutes daily reconciling carry discrepancies that a correctly modeled platform resolves automatically. Across a 250-day trading year, that represents a material allocation of analyst capacity to a problem that correct modeling eliminates.

CTRM base metals implementation challenges

How Novaex Models LME Tom-Next Carry Natively

Novaex treats LME Tom-Next carry as a first-class data type. It functions as an independent variable rather than a derived field or a user-configured approximation retrofitted to a generic forward curve module.

The platform ingests LME forward curve data at the daily prompt-date level. Each date from cash to three months forward is stored as a discrete data point with its own bid, offer, and mid. The spread between adjacent dates is computed directly from this data, rather than being interpolated or estimated from a monthly anchor.

Here is the specific workflow:

Step 1: Forward Curve Ingestion

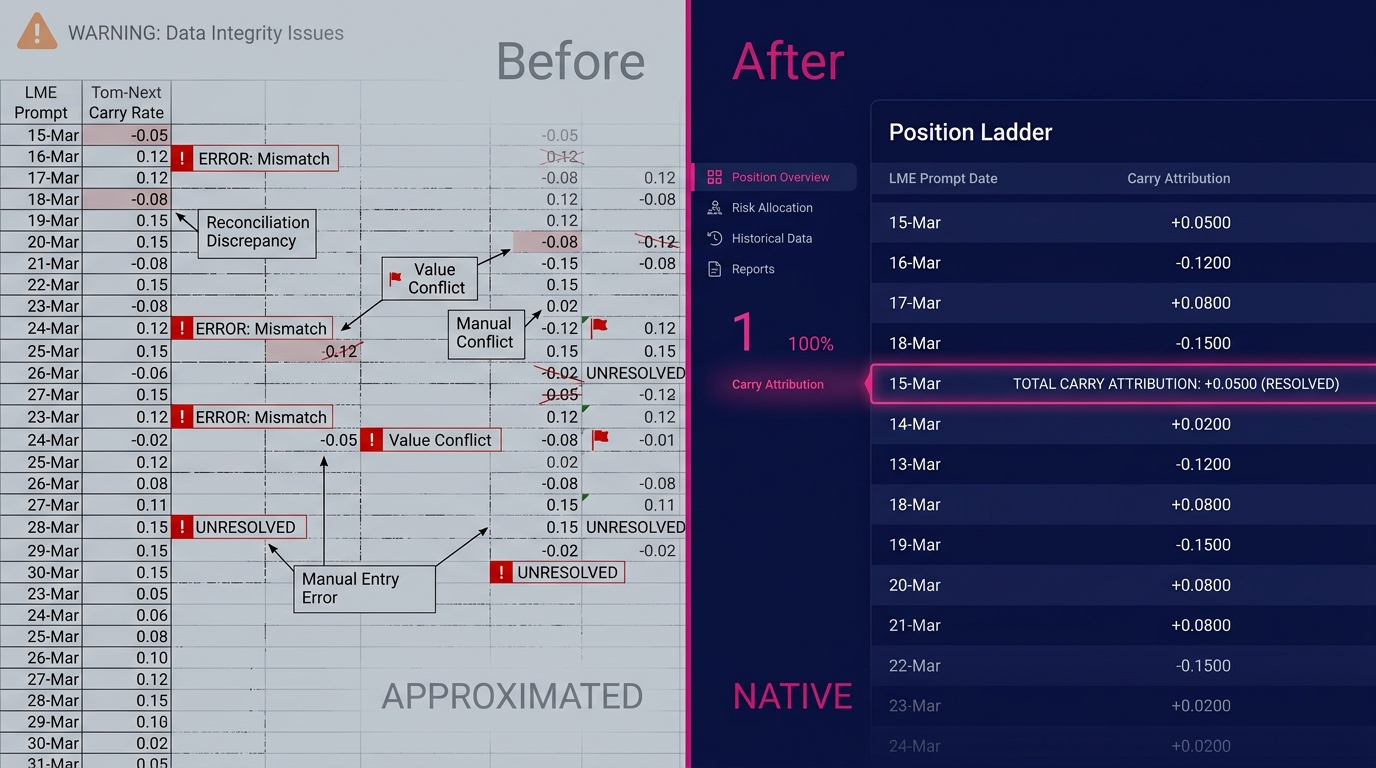

Navigate to Pricing > LME Forward Curve. The grid displays each business day from T+0 through 3M as a separate row. Columns show bid, offer, mid, and the date-to-date spread versus the prior prompt. Data refreshes on the configured feed interval, typically every 60 seconds during LME trading hours. There is no "LME monthly approximation" toggle. The daily structure is the default and only structure for LME contracts.

Step 2: Position Tag to Prompt Date

When you book a trade in Trading > New Position, the prompt date field accepts any valid LME business date. The platform validates the entry against the LME prompt calendar and flags non-prompt dates before confirmation. There is no silent rounding to a monthly expiry.

Step 3: Carry Attribution in MTM

Open Positions > Mark-to-Market. For each open LME position, the P&L decomposition shows a Carry Attribution line item. This reflects the actual spread between the position's prompt date and today's cash date, drawn live from the forward curve grid. The number updates dynamically intraday as the LME curve moves.

Automated Carry Calculation in Novaex

Novaex calculates Tom-Next carry automatically by sourcing the bid/offer spread for each daily LME prompt date directly from its market data layer. The carry attribution in the P&L view is a live computation. The spread between your position's prompt date and cash is pulled from the same forward curve grid that prices the position. No morning data entry, no spreadsheet reconciliation, no configuration file to update. The mechanism is the model.

This ensures the carry number in your book matches the exact number the LME market is quoting.

The Tom-Next Carry Walkthrough: What Your Book Shows

The practical difference between approximated and native carry modeling is most visible in three scenarios: normal contango, acute backwardation, and multi-date books.

Normal Contango (Copper, Typical Market)

In a typical contango market, the LME 3M copper spread over cash trades in the $15, $30/MT range. Linear interpolation across 65 business days implies roughly $0.23, $0.46/MT per day. The actual daily Tom-Next spread is not uniform. Front dates typically trade tighter than back dates as the curve steepens away from cash.

In Novaex, the carry attribution for a position three weeks out reflects the exact spread quoted for that specific date. The difference may be $0.05, $0.15/MT per day. On a 500-lot position (12,500 MT), that is $625, $1,875 per day in carry P&L. Over the life of a 60-day hedge, the cumulative discrepancy versus a linearly interpolated model is material and directionally biased by the shape of the curve.

Acute Backwardation

During periods of acute backwardation (supply tightness, dominant warehouse positions, or delivery squeezes), the LME front curve inverts sharply. The Tom-Next spread widens from cents to dollars and, in extreme cases, to hundreds of dollars per MT per day.

A platform that linearly interpolates carry from the 3M spread will not capture this inversion at the front dates where it actually occurs. The error is largest precisely when it is most consequential.

LME backwardation and dominant position mechanics

The Impact of Tom-Next Carry on Hedging P&L

Tom-Next carry is a direct component of hedge P&L for any physical metals position held through a prompt date. When you own physical metal and have sold an LME forward hedge, the carry on your hedge is either a cost (contango) or income (backwardation) that must be attributed separately from your price exposure. Mismodeling this carry produces a hedge effectiveness error that distorts both P&L reporting and risk metrics. Under IFRS 9 hedge accounting guidance, carry attribution is required for fair value assessment of hedging instruments; an approximated figure is not a compliant figure.

In Novaex, the P&L Decomposition panel under Positions > Risk Analytics shows four separate attribution lines: Price Delta, Gamma (for options), Carry, and Basis. The Carry line is always derived directly from the live forward curve spread.

Multi-Date Books

A typical physical metals trader runs positions across multiple prompt dates simultaneously. This involves material purchased for delivery on different days, hedged to matching or near-matching LME dates. A platform that approximates carry applies a version of the same error to each date, and those errors may compound or partially offset depending on the curve shape.

Novaex handles multi-date books through the Position Ladder view, accessible from Positions > Ladder. Each prompt date appears as a discrete row with its own carry attribution, MTM value, and risk exposure. The ladder aggregates to a net position that correctly reflects the full carry profile of the book based on precise daily rates.

What Correct Carry Modeling Changes in Your Operations

The immediate operational impact of native Tom-Next modeling is the elimination of the morning carry reconciliation workflow. Teams that previously extracted LME spreads from a data terminal, entered them into a spreadsheet, and reconciled the output against their CTRM no longer perform that step.

The downstream impact is more significant: hedge P&L accuracy that does not require a caveat. When carry is correctly attributed in real time, the P&L your desk reports to risk management reflects actual market exposure. According to a 2022 EY commodity risk management study, 42% of commodity trading firms identified manual data processes as a primary contributor to P&L reporting errors. Carry mismodeling is a documented component of that category.

This accuracy matters specifically for three workflows:

- Hedge effectiveness testing under IFRS 9 / ASC 815, where carry attribution is a required component of fair value measurement

- Intraday risk limit monitoring, where MTM accuracy determines whether a position is within limits or has breached them

- Roll decision-making, where the actual cost of carrying a position forward against the bid/offer spread determines whether rolling or closing is the correct action

IFRS 9 hedge accounting base metals

Why Depth-First Design Produces the Correct Model

Most platforms mismodel LME Tom-Next carry due to architectural constraints. A platform built to cover 30 commodity markets simultaneously models each market to a level of generality sufficient for it to function across all of them. The LME's daily prompt structure creates a decision point: build a native LME date engine, or map LME dates onto the existing monthly-expiry framework.

Multi-commodity platforms consistently choose the latter. The engineering cost of a native LME date engine benefits only base metals users, so it is deferred in favor of features that serve the broader installed base. Base metals traders absorb that architectural choice as a daily operational cost.

CTRM platform selection criteria base metals

Novaex was built on the opposite premise. From the beginning, the forward curve module was designed around the LME's actual prompt date calendar, including the holiday schedule, the daily date rolling logic, and the treatment of carry across the cash-to-3M window. The platform was built entirely around the Tom-Next mechanism.

According to the LME's own market data documentation, the LME publishes official cash-to-3M carries for base metals on a daily basis as part of its closing price data set. Novaex ingests this feed directly, with no transformation layer that introduces interpolation or approximation between the source and the position view.

The result is a platform where the model matches the market exactly, eliminating the need for analyst reconciliation before the desk can trust the number.

The Standard for LME Tom-Next Carry

LME Tom-Next carry is not an edge case. It is the daily operational reality of every front-office metals desk running physical hedges against LME forwards. Getting it right is the baseline requirement for a platform that claims to support base metals trading.

A platform that models it correctly does not require configuration workarounds, morning data entry routines, or spreadsheet reconciliation. It connects to the LME forward curve at the daily prompt-date level and computes carry attribution automatically for every position, in real time, from the same data the market is using.

That is the standard Novaex is built to.

How to evaluate your carry modeling:

- See the forward curve grid and carry attribution live: Request a platform walkthrough to step through the Tom-Next workflow in a live Novaex environment with current LME data, viewing the specific panels described above with real numbers.

- Benchmark your current carry accuracy: Pull the LME's official daily carries for the last 30 trading days and compare them to what your current system attributed to open positions in that window. The discrepancy quantifies what your current platform is costing you.

- Audit your P&L decomposition: If your CTRM does not show a separate carry attribution line for each LME position (distinct from price delta and basis), you are not seeing the full picture of your hedge performance.