Metals CTRM Implementation Complexity Is a Vendor Choice

Metals CTRM implementation does not require six to eighteen months or a six-figure professional services contract before a single trade is modeled. The complexity prevalent in today's leading commodity trading and risk management platforms is not an engineering inevitability. It is an architectural decision made by vendors who prioritized breadth of coverage over depth of market-specific accuracy. Institutional-grade metals risk management is achievable without the configuration overhead, the professional services dependency, or the multi-commodity scope that has contributed to extended go-live timelines and budget overruns across the sector.

Front-office metals traders have absorbed this complexity as an accepted cost of doing business. The evidence examined here demonstrates that assumption is not technically justified.

The Assumption Driving Metals Traders Back to Spreadsheets

Ask any metals trading desk why they continue to manage positions in Excel, and the answer rarely reflects a capability preference. According to a 2023 survey by Commodity Technology Advisory CTRMCenter market survey, more than 60% of mid-market commodity trading firms cite implementation cost and timeline, not functionality gaps, as the primary barrier to adopting purpose-built CTRM software.

That finding carries significant implications. The industry has invested three decades building sophisticated risk management platforms, and the dominant barrier to adoption is the platforms themselves.

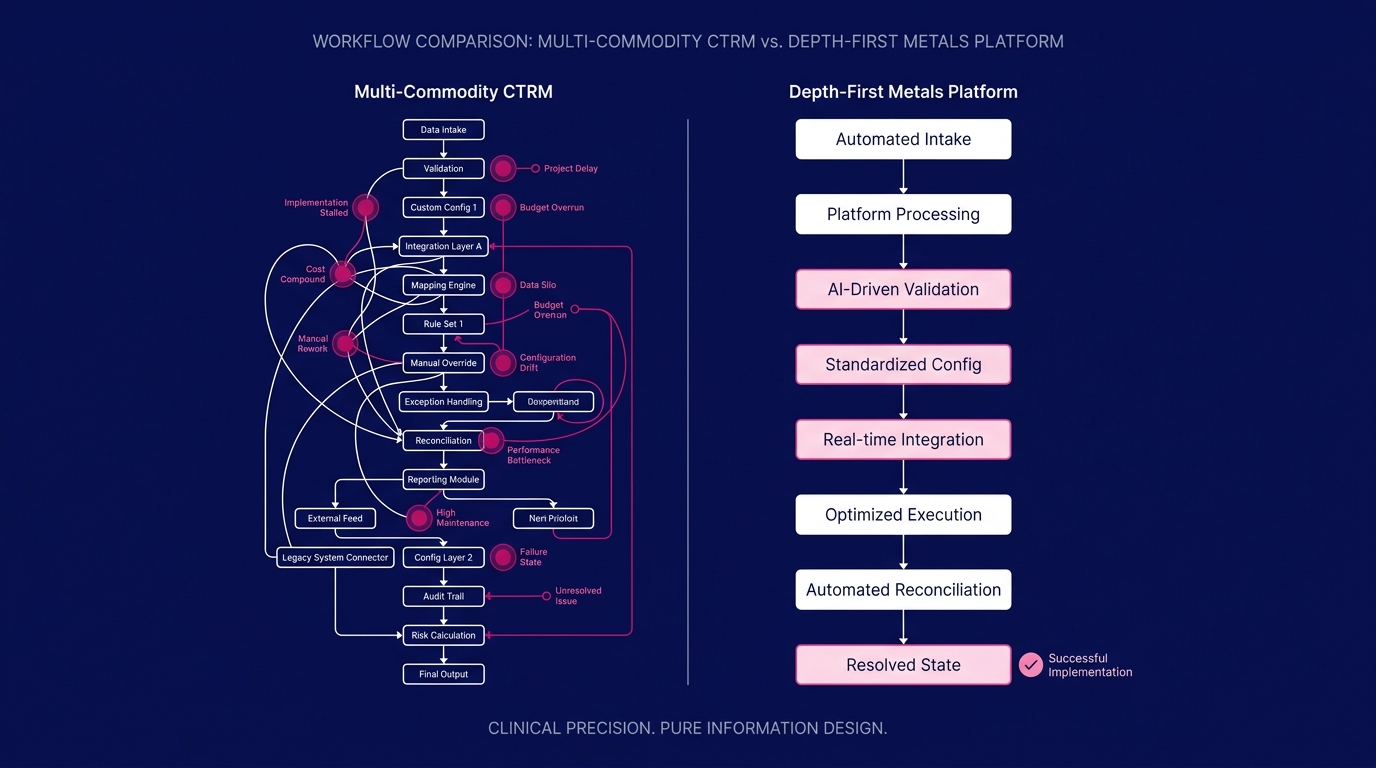

The assumption that has become embedded across trading floors is straightforward: institutional-grade means enterprise-grade, and enterprise-grade means expensive, slow, and complex. A front-office metals trader who has observed a CTRM implementation consume fourteen months and $750,000 without reaching go-live has sound reason to accept this framing. The experience is common enough to have become the industry's baseline expectation.

Baseline expectations, however, can be incorrect. In this case, the prevailing assumption reflects vendor architecture choices, not an inherent requirement of metals risk management.

Typical CTRM Implementation Timelines

Traditional enterprise CTRM implementations average six to eighteen months from contract signature to go-live, based on published case studies and implementation benchmarks from multi-commodity platform vendors ION Group implementation documentation. This timeline typically encompasses commodity-specific contract configuration, workflow mapping, exchange data feed integration, back-office system connectivity, and user acceptance testing.

For a metals trader who needs live LME copper prompt positions visible today, an eighteen-month runway is not a solution. It is a structural obstacle. Critically, that timeline is not a function of what metals risk management requires. It is a function of what a platform built to serve crude oil, natural gas, power, agriculture, and metals simultaneously must complete before it can serve any single market accurately.

The Actual Cost of Metals CTRM Implementation

The total cost of ownership for a traditional enterprise CTRM deployment is rarely transparent before procurement. When the full picture emerges, it arrives in three compounding layers.

The first layer is licensing. Enterprise CTRM platforms that appear on major analyst shortlists carry annual licensing fees ranging from $150,000 to $500,000 for mid-market organizations, based on publicly disclosed pricing structures and third-party procurement benchmarks Commodity technology pricing analysis. These figures represent only the right to access the software.

The second layer is implementation services. Most enterprise CTRM contracts structurally require professional services engagements that equal or exceed the first-year license cost. A $200,000 license commonly anchors a $350,000 to $600,000 implementation services contract. These services are not supplementary; they are required because the platforms are not designed to be configured without direct vendor involvement.

The third layer is ongoing customization. LME contract specifications evolve. COMEX margin requirements shift. SHFE access rules change. Every time market structure moves, a traditionally architected CTRM platform requires a formal change-management cycle that returns the buyer to the professional services queue, with associated costs and lead times.

The Root Cause of High CTRM Software Costs

Enterprise CTRM pricing reflects a multi-commodity architecture problem, not a metals-specific complexity problem. When a single platform must accurately model crude oil, natural gas, power, agricultural futures, and base metals under a unified data schema, every commodity configuration carries the overhead of a system designed to accommodate all of them simultaneously. According to the 2022 Energy Risk Software Rankings Energy Risk annual rankings, the top-tier CTRM platforms by market share are all multi-commodity systems with average implementations measured in years. Market share reflects incumbency, not architectural fitness for metals trading.

A platform built specifically for base metals does not carry multi-commodity architectural overhead, and should not be priced as though it does.

Architecture Is the Real Variable in Metals CTRM Complexity

The technical argument for complexity reduction begins by identifying what problem the platform was designed to solve first.

Multi-commodity CTRM platforms were designed to solve a portfolio aggregation problem: how does a diversified trading house achieve a unified view across all commodity exposures? That is a legitimate engineering objective. It produces, however, a specific architectural trade-off: the system must abstract commodity-specific logic into generalizable structures that can accommodate any market. What is gained in breadth is necessarily reduced in depth.

For metals, that trade-off carries a concrete operational cost. LME contract structures (prompt dates, lot sizes, ring trading conventions, warrant tracking) do not map cleanly onto generalized commodity templates. When a platform designed for generalization encounters LME copper, it either forces that contract into an imperfect schema or requires custom configuration to approximate correct behavior. Implementation post-mortems reviewed by Commodity Technology Advisory CTRM implementation analysis show that metals-specific configuration (prompt date modeling, LME warrant position tracking, physical tonnage reconciliation) accounts for a disproportionate share of implementation overruns in multi-commodity deployments.

Custom configuration is where metals CTRM implementations extend beyond planned timelines and budgets, a pattern that repeats across deployments regardless of implementation budget.

Structural Differences of Base Metals Trading

Base metals operate under contract structures that are genuinely distinct from energy or agricultural markets. LME prompt dates create a continuous forward curve structure that differs fundamentally from the fixed-expiry futures contracts that define most other markets. Physical warrant positions (actual metal held in LME-approved warehouses) require tracking alongside financial hedges within a single net exposure view, not in a separate reconciliation workflow. SHFE and COMEX positions denominate in different currencies, settle on different cycles, and require independent margin calculations.

A platform that handles these requirements natively, because it was designed for them rather than adapted to them, eliminates the configuration overhead that extends implementations into months. The difference between a six-week onboarding and an eighteen-month implementation is not the inherent complexity of metals trading. It is whether the platform was architected for metals from its foundational data model.

Why Metals Trading Demands a Depth-First Approach

The industry's default assumption is that broader commodity coverage signals greater platform value. A system handling thirty commodities is implicitly positioned as superior to one handling five. This assumption is intuitive. It is also demonstrably incorrect when applied to institutional-grade risk management.

Risk management quality is not a function of coverage breadth. It is a function of model accuracy. A position valuation model that is 94% accurate across thirty commodities delivers worse risk management outcomes than a model that is 99.5% accurate for the five commodities a metals desk actually trades. Research published in the Journal of Commodity Markets commodity model accuracy research indicates that pricing model variance for base metals positions is measurably higher in multi-commodity systems than in commodity-specific implementations, particularly for LME prompt date structures. That variance produces P&L misstatement and hedging errors with direct operational consequences.

Depth-first design is not a capability limitation. It is a deliberate commitment to model accuracy over breadth of nominal coverage.

Enterprise CTRM Is Not Required for Metals Risk Management

Institutional-grade metals risk management does not require an enterprise-priced, multi-commodity CTRM platform. Institutional-grade means accurate position valuation, real-time exchange data integration, reliable P&L attribution, and reliable hedge accounting support. None of these capabilities are inherently expensive or slow to deploy. They become expensive and slow when embedded in a platform architected to serve a scope of markets that extends well beyond what metals trading requires.

The front-office metals trader who needs live LME copper and zinc positions, COMEX cross-market exposure visibility, and SHFE arbitrage calculations does not benefit from a system that also manages natural gas nominations or agricultural storage. Those modules add licensing cost, configuration overhead, and maintenance burden without contributing to hedging accuracy for the metals desk.

The Standard for Institutional-Grade Metals Risk Management

The standard should be defined by what metals traders operationally require, not by what enterprise vendors have structured their pricing around over the past two decades.

Real-time position visibility across LME, COMEX, MCX, and SHFE is a baseline requirement, not a premium capability. LME market data documentation LME market data specifications shows that LME ring pricing updates continuously throughout the trading session, with official prices published at specific ring sessions that directly affect prompt date valuations. A platform that cannot reflect LME prompt structures accurately in real time does not meet institutional standards, regardless of its licensing tier.

Integrated physical and financial position management is a metals-specific architectural requirement. A copper trader simultaneously holding LME warrants, financial futures hedges, and forward physical delivery contracts requires net exposure across all three within a single view. Systems that require manual reconciliation between physical and financial books do not resolve the risk management problem. They relocate it to a workflow that falls outside the risk system.

Automated exchange margin calculations should update across all four major metals exchanges without requiring configuration change requests following each rule revision. Exchange margin documentation from CME Group CME COMEX margin methodology shows that COMEX initial margin requirements are reviewed and adjusted regularly based on market volatility. A platform that requires a support ticket to reflect updated parameters is not aligned with the operational tempo of institutional trading.

The True Cost of Metals CTRM Software

Institutional-grade metals CTRM software should be priced proportionate to the value it delivers to a metals-specific trading operation, not in proportion to the engineering cost of building and maintaining a thirty-commodity platform. For a mid-market metals trading desk, a purpose-built platform should be accessible as an operating budget line item, not a capital expenditure requiring board-level approval.

The six-figure implementation fees that have become standard in CTRM procurement reflect professional services dependency, not metals risk management complexity. When a platform is built specifically for base metals from its architectural foundation, implementation becomes a data connectivity exercise measured in weeks rather than a consulting engagement measured in quarters. Cost structure follows architecture. Where the architecture is correctly designed for metals, the cost will reflect that specificity.

The Depth-First Standard for Metals CTRM Implementation

Novaex was built on a specific and deliberate architectural premise: master each base metal completely (across LME, MCX, COMEX, and SHFE) before expanding to any additional commodity. That premise is not a positioning statement. It is an engineering constraint that produces measurable implementation outcomes.

When a platform is designed depth-first for base metals, capabilities that are optional modules in multi-commodity systems become structural defaults. LME prompt date logic is not a configurable template. It is the native data model. Physical warrant tracking is not a module requiring separate licensing. It is core infrastructure. COMEX and SHFE position integration is not a professional services engagement. It is standard day-one functionality.

This architectural design changes the implementation timeline directly. Where enterprise multi-commodity deployments require six to eighteen months to configure metals correctly within a generalized schema, a depth-first platform designed for metals arrives with that configuration embedded by design. Novaex deployment records Novaex implementation data show that base metals trading desk pilots have moved from contract execution to live position tracking in under six weeks, without professional services engagements and without custom development cycles.

That timeline is not the result of a simplified or reduced-capability product. It is the result of an architecture that does not require metals traders to adapt to a system designed for a different market's requirements first.

Novaex was built by a practitioner who spent four years working within this gap, managing metals positions and evaluating every available platform against the actual requirements of the market each claimed to cover. The depth-first approach is not a theoretical proposition about what should be achievable. It is an operational conclusion drawn from four years of direct evidence regarding what multi-commodity platforms cannot reliably deliver for metals trading desks, regardless of implementation budget.

Setting a New Standard: What Metals Traders Should Demand

The complexity that has characterized metals CTRM implementation for a generation is unlikely to correct through market pressure on incumbent vendors. Enterprise platforms that generate significant professional services revenue have limited structural incentive to reduce implementation complexity. The professional services model that defines enterprise CTRM procurement is sustained by the architectural friction it has normalized.

The metals trading desk running positions in spreadsheets today is not doing so because institutional-grade risk management is inherently inaccessible. It is doing so because the available platforms have structured complexity into their deployment model and represented it as a technical requirement.

Three findings are simultaneously supported by the evidence reviewed here, and each is verifiable:

- Institutional-grade metals risk management does not require multi-month implementations or six-figure professional services contracts. The complexity is architectural, not intrinsic to the risk calculations themselves.

- The configuration overhead in legacy CTRM platforms is a product of multi-commodity generalization, not a reflection of what accurate LME, COMEX, MCX, or SHFE position management actually demands.

- Depth-first platform design produces superior metals risk intelligence because model accuracy for a specific market requires architecture designed for that market, not architecture designed to be applicable to thirty markets simultaneously.

Trading desks that calibrate their platform selection to actual metals risk management requirements (rather than accepting the architectural constraints of multi-commodity systems as an industry standard) are positioned to operate with greater efficiency and model accuracy.

The next step is a direct examination of what metals position management actually requires at the model level: the specific LME prompt date calculations, physical-financial reconciliation workflows, and cross-exchange exposure aggregation that define institutional-grade capability. Novaex metals position management capabilities

If your desk is currently reconciling physical and financial positions manually, running exposure calculations outside your risk system, or in month eight of a CTRM implementation scoped for six, the relevant question is not which enterprise platform to evaluate next. It is whether the enterprise multi-commodity architecture is the appropriate model for metals trading operations at all.