Pulse vs. Ledger: Diagnosing and Resolving Your Metals Trading Workflow Failure

If your firm has a metals trading workflow problem, it belongs to one of two documented categories: degraded market intelligence or unreconciled positions. Novaex Pulse is built to resolve the first. Novaex Ledger is built to resolve the second. Determining which failure is generating the most operational cost at your desk right now is the only evaluation framework that produces a defensible product decision at this stage.

Both products are built on the same depth-first methodology and cover the same base metals universe across LME, COMEX, MCX, and SHFE. They enter the workflow at entirely different failure points. This means starting with the wrong product addresses a secondary problem while the primary one continues to compound losses, reconciliation hours, and execution lag.

This comparison uses operational vocabulary. The objective is a specific, committed product decision supported by a repeatable diagnostic framework.

Two Documented Failure Modes in Metals Trading

Every trader who has operated a legacy CTRM platform during a fast-moving LME session can identify precisely when the system fails operationally. Either the desk is receiving price updates with a 90-second lag while the market moves in 15-second increments, or the book shows a copper long that middle office cannot reconcile against the broker confirmation received that morning.

These are distinct problems. They produce different downstream costs and require different solutions.

A 2023 Coalition Greenwich study Coalition Greenwich commodity trading data latency research found that 62% of commodity trading desks identifies data latency as their primary operational obstacle during high-volatility sessions. A separate Accenture analysis of mid-market trading firms found that position reconciliation discrepancies consume an average of 4.2 hours per week per risk manager. This is time spent manually resolving what automated governance architecture should catch before the trading day opens.

Both failure modes generate measurable cost. They compound through different mechanisms, and conflating them explains why evaluation processes achieve feature-level comparison without producing a product commitment.

Differences between market intelligence and position management software

Market intelligence software delivers real-time pricing, spread analysis, basis risk modeling, and cross-exchange arbitrage visibility: the information set that informs trade decisions before execution. Position management software tracks, reconciles, and governs what the firm already owns, ensuring the book is accurate and auditable before the next position is added.

One defines what the market is doing. The other defines what the firm has already done. Both are operationally necessary. Only one is the current bottleneck. That bottleneck is where the product evaluation should begin.

How Novaex Pulse Closes the Market Intelligence Gap

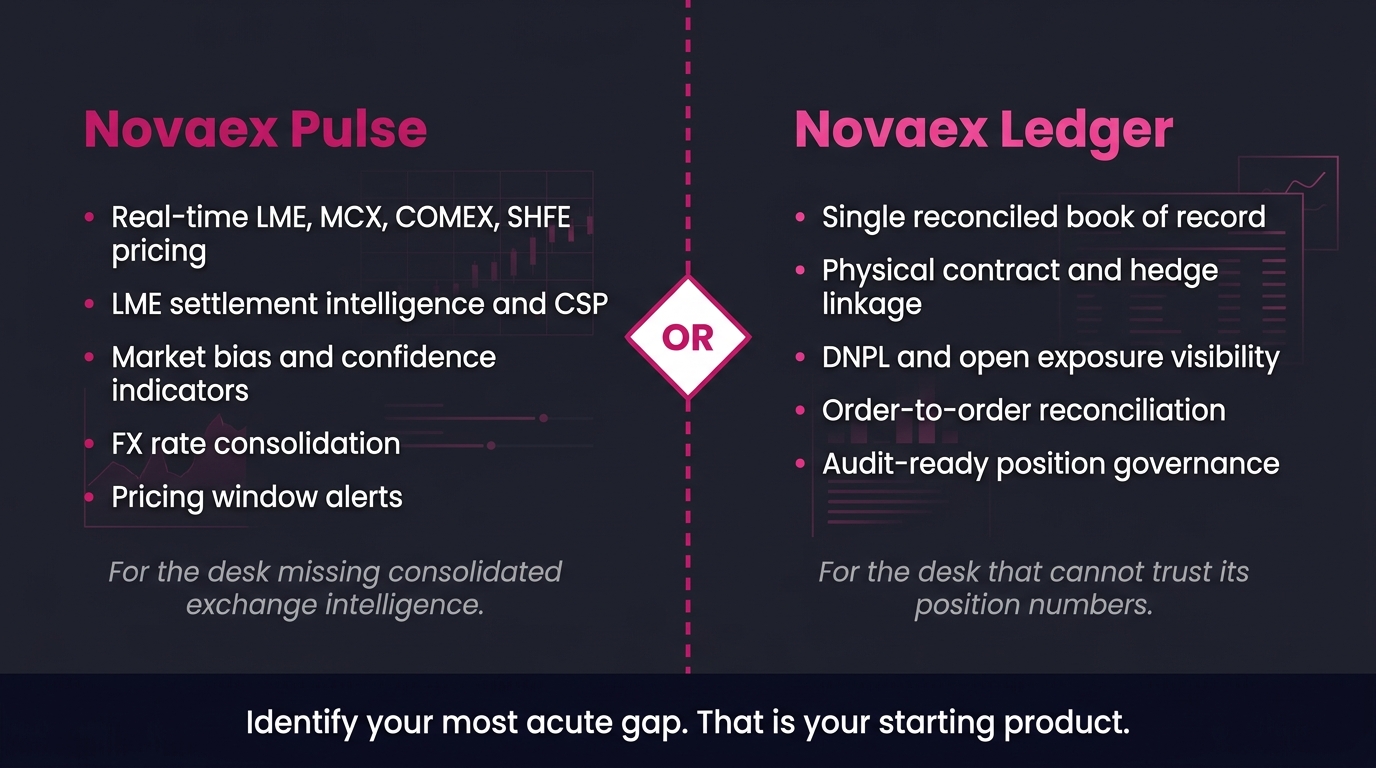

Novaex Pulse was built to resolve a specific, documented failure mode: the inability to generate accurate, exchange-calibrated intelligence across LME, COMEX, MCX, and SHFE from a single interface without manual aggregation.

Legacy platforms (and multi-commodity platforms that cover base metals as one asset class among twenty) consistently deliver headline data: LME three-month copper, aluminum settlement, and zinc cash. What they consistently fail to deliver is inter-exchange spread behavior, warehouse warrant dynamics, currency-adjusted basis across SHFE contracts, and the premium and discount structure against physical delivery points that drives hedging decisions in base metals.

According to the LME's 2023 Annual Market Report LME 2023 Annual Market Report, base metals futures across LME, COMEX, and SHFE represent over $11 trillion in annual notional traded volume. A trading desk operating on partial data across those venues is making hedging decisions with a structurally incomplete picture of its own market.

Workflow failures resolved by market intelligence software

Pulse addresses four specific, recurring failure points: (1) cross-exchange basis miscalculation when hedging physicals against futures across venues; (2) latency-induced execution lag during LME Ring sessions and electronic trading hours; (3) inability to model spread relationships between SHFE copper and LME copper without manual data assembly; and (4) the absence of real-time premium analysis for physical delivery contracts against published exchange prices.

These are workflow deficiencies that, when unresolved, produce mispriced hedges and missed execution windows in markets where price windows close in seconds. Pulse's depth-first architecture means copper is not a data feed. It is a complete information model covering every exchange where copper trades, every forward curve segment, and every premium structure relevant to both physical and paper positions. The same applies to aluminum, zinc, nickel, lead, and tin across all relevant venues.

When to prioritize market intelligence over reconciliation

Prioritize Pulse when the dominant issue is decision quality before execution: when traders need the real cross-exchange basis and the answer requires more than 30 seconds to produce, or when hedging models rely on end-of-day data for decisions made intraday.

The diagnostic is measurable: track how many times per week a trader cannot answer a real-time pricing question from a live system and defaults to a phone call, a Bloomberg terminal workaround, or a manually maintained spreadsheet. According to a 2022 Oliver Wyman trading operations study [LINK: Oliver Wyman trading operations efficiency research], traders at firms with fragmented market data infrastructure spend an average of 23 minutes per session on manual data aggregation tasks that should be fully automated. That represents 23 minutes of reduced market engagement during the periods when market engagement has the highest operational impact.

How Novaex Ledger Closes the Position Governance Gap

Novaex Ledger was built to resolve a different failure mode: the inability to maintain a continuously reconciled, auditable position record across physical trades, futures hedges, and broker confirmations in real time.

Position governance failures operate differently from market intelligence failures. They do not surface during a fast LME session. They emerge during end-of-day reconciliation, during margin calls, during regulatory reporting cycles, or when a trader attempts to add to a position that middle office flags as inconsistent with the system of record.

According to a 2023 EY Commodity Trading Risk Survey EY commodity trading risk management survey, 41% of mid-market commodity trading firms reported at least one significant position reconciliation discrepancy in the prior 12 months, defined as a difference exceeding 100 MT between the trading desk's live position and the risk management system's recorded position. The downstream cost, measured in margin exposure, audit remediation time, and regulatory risk, is a governance architecture problem, not a data quality problem.

Indicators of a position governance problem

A trading firm has a position governance problem when any of the following conditions hold: end-of-day book reconciliation requires manual intervention more than twice per week; the risk manager and trading desk consistently open the morning with different position figures; or the audit trail for a single physical trade, from confirmation through hedging instrument through final settlement, requires records from more than two disconnected systems.

Ledger resolves this by functioning as the single position record that updates continuously as trades are executed, confirmed, and settled. The system ingests broker confirmations, matches them against trade records, flags discrepancies with rule-based governance logic, and maintains an immutable audit log that satisfies both internal risk oversight and external regulatory requirements. According to research from Commodity Technology Advisory ComTech CTRM reconciliation best practices research, firms using automated position reconciliation reduce end-of-day close time by an average of 67% compared to firms running manual or semi-manual reconciliation processes. This marks a structural change in how back and middle office operations function every trading day.

Diagnosing Your Most Acute Workflow Failure Mode

The diagnostic framework is operational. It identifies which current failure is actively degrading trading or risk outcomes, not which capabilities a firm might eventually want.

Market intelligence gap indicators:

- Real-time cross-exchange basis is unavailable without manual data assembly

- Traders routinely use external terminals or spreadsheets to supplement system pricing

- Hedging models rely on T+1 or T+2 data for decisions made intraday

- LME, COMEX, and SHFE spread relationships require manual calculation

- Physical delivery premiums are estimated rather than live-priced

Position governance gap indicators:

- End-of-day reconciliation requires manual intervention more than twice per week

- Trading desk and risk management hold different live position figures before the morning mark

- Broker confirmation matching is a manual or partially manual process

- The audit trail for any single trade requires accessing more than two disconnected systems

- Margin exposure calculations are delayed because position accuracy is unresolved

According to a 2022 McKinsey Global Commodity Markets report McKinsey global commodity markets operational risk research, trading firms operating with fragmented position records face 2.3 times higher operational risk exposure during high-volatility periods compared to firms running integrated governance architecture. The compounding effect of position uncertainty during fast markets produces delayed execution decisions and margin exposure that integrated governance eliminates.

The operational cost of delaying a platform decision

Every week of continued operation on a fragmented system generates measurable cost: mispriced hedges, reconciliation labor, execution lag, and audit exposure that accumulates incrementally until it surfaces in a material operational event. According to analysis from TriplePoint Commodity Management TriplePoint CTRM modernization cost-of-delay analysis, commodity trading firms that delay CTRM modernization for 12 months past their identified evaluation point incur average incremental operational costs equivalent to 1.8 times the annual license cost of the platform deferred.

The evaluation phase carries a documented cost. A committed product decision eliminates it.

The Metals Trading Workflow Each Product Enters

Understanding where each product enters the workflow establishes that this is a sequencing decision, not a capability ranking.

Novaex Pulse enters pre-execution: before a trader decides whether to hedge, at what price, on which exchange, and against which forward curve segment. It is the intelligence layer that makes hedging decisions operationally defensible.

Novaex Ledger enters post-execution: after a trade is placed, governing what now exists in the book, ensuring accurate recording, reconciliation against counterparty confirmations, and correct reflection in risk exposure calculations before the next trade is added.

Neither product is superior to the other. They resolve different problems at different points in the same workflow. Rather than asking which is better, the evaluation must identify which workflow failure currently generates the highest operational cost at this desk. That question has a specific, answerable answer for every trading operation.

A physical copper merchandiser who consistently prices physicals against an incomplete view of LME and COMEX basis has a Pulse problem. A hedging desk that spends Tuesday mornings correcting position discrepancies before it can trade has a Ledger problem. Both scenarios are well-documented in the operational literature on mid-market commodity trading. Only one applies to your desk.

According to the World Bureau of Metal Statistics WBMS global refined copper consumption data, global refined copper consumption exceeded 26 million metric tons in 2023, with hedging activity across LME, COMEX, and SHFE accounting for the dominant share of price risk management volume. Firms operating with degraded intelligence or unreconciled positions in that market do not have the same operational foundation as firms that have resolved those failure modes.

From Evaluation to a Committed Product Decision

At this stage of a structured evaluation, continued ambiguity often stems from relying on capability-based evaluation criteria instead of failure-mode diagnostics.

Return to the diagnostic framework in Section 4. Identify the failure mode your desk encounters most frequently and at the highest operational cost this week. That failure mode determines the starting product, not the eventual full-stack configuration, but the first implementation that resolves the most acute problem.

If your most acute failure is degraded market intelligence (incomplete cross-exchange pricing, intraday basis gaps, reliance on manual data aggregation for live decisions), the starting product is Novaex Pulse.

If your most acute failure is position governance breakdown (reconciliation discrepancies, audit trail fragmentation, mismatched position records between trading and risk), the starting product is Novaex Ledger.

The full implementation path leads to both products operating as an integrated stack, with Ledger governing the position record and Pulse supplying the market intelligence layer against which that position is evaluated in real time. The decision point is which failure mode to resolve first.

Three immediate next steps:

- Run the failure-mode diagnostic: Map the last five trading days of workflow issues against the two indicator lists in Section 4. The category with more matches identifies the starting product with a precision no feature comparison can replicate.

- Request a workflow-scoped demonstration: When contacting Novaex, specify which failure mode is being addressed. The demonstration should be scoped to that specific workflow failure, not a general product tour that reintroduces evaluation ambiguity. Novaex product demonstration request

- Define your go-live success metric before the first implementation meeting: Establish the single operational metric that will confirm the primary failure mode has been resolved: basis accuracy within a defined threshold, reconciliation discrepancies below a defined frequency, or end-of-day close time under a defined ceiling. Agreeing on that metric before implementation removes ambiguity about whether the problem has been solved.