SHFE Pricing in Your Intraday Workflow: No Analyst Needed

SHFE pricing context belongs in every base metals trader's intraday decision cycle. The mechanism is direct: SHFE's daytime session closes at 15:00 Beijing time, 07:00 GMT in winter, before LME electronic trading reaches peak liquidity. That close delivers a confirmed Chinese price signal, a calculable basis reading, and a directional input before your first hedge of the day. No overnight subscription required. No dedicated analyst required.

The reason most trading desks still treat SHFE data as a specialist function is infrastructure, not complexity. Legacy platforms bundle Asian market data into separate modules or parallel analyst workflows that eliminate the timing advantage SHFE's session structure actually provides. According to the World Federation of Exchanges, SHFE copper futures volume regularly exceeds LME copper on a tonnes-traded basis. Treating that price discovery mechanism as optional is a significant oversight WFE annual statistics.

This post maps the specific workflow mechanics that make SHFE context available within the intraday decision cycle without adding headcount or subscription layers.

Why SHFE Pricing Context Belongs in Every Intraday Workflow

The default assumption on many Western trading desks is that SHFE matters only when a position carries direct mainland Chinese price exposure. That framing undersells the signal by a significant margin.

SHFE copper, aluminum, zinc, lead, nickel, and tin prices are independent price discovery mechanisms. They reflect domestic Chinese supply, demand, and inventory conditions that frequently diverge from LME pricing before that divergence becomes visible in London. When SHFE and LME prices move in opposite directions, or when one market moves and the other doesn't, the basis spread itself is the signal.

The LME-SHFE Basis and Its Impact on Base Metals

The LME-SHFE basis is the spread between SHFE prompt prices (converted to USD/tonne via spot CNY/USD FX) and LME cash or three-month prices for the equivalent metal. A widening SHFE premium signals stronger Chinese demand or tighter mainland supply than LME pricing currently reflects. A narrowing basis or outright SHFE discount can indicate demand deceleration or elevated bonded warehouse inventory building in Shanghai.

For physical pricing decisions, particularly for material moving into or out of Asian markets, basis direction is a direct input to premium and discount negotiations.

According to the Shanghai Metals Market (SMM), bonded copper warehouse stocks in Shanghai can swing by tens of thousands of tonnes within a single week SMM bonded warehouse data. That kind of inventory movement generates basis moves of $50 to $150/tonne that are entirely invisible if you are only monitoring LME. By the time LME cash prices reflect those dynamics, the physical pricing window has already shifted.

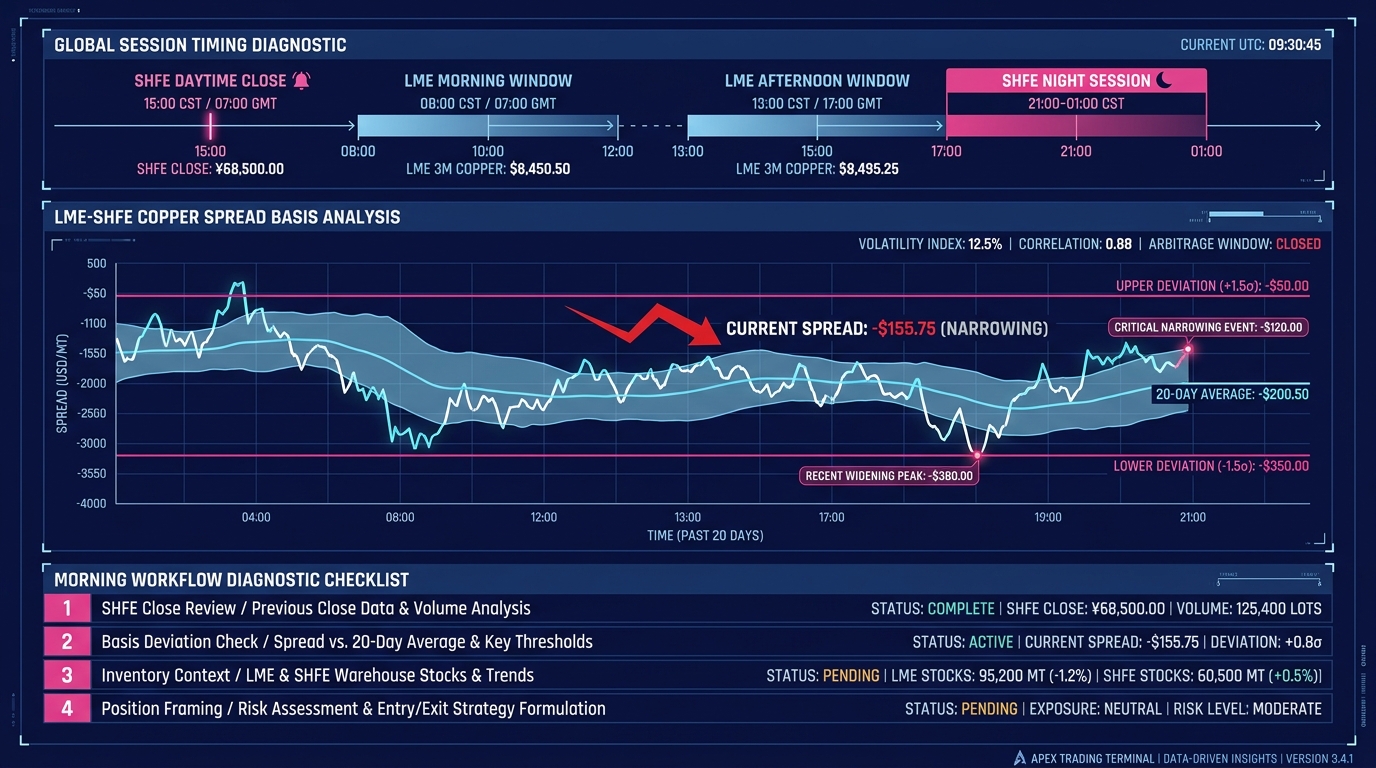

Understanding LME and SHFE Session Timing Differences

Session timing is the operational foundation of SHFE integration, and the part most traders have accepted as a barrier without actually testing the sequencing.

SHFE operates two daytime sessions: 09:00 to 11:30 and 13:30 to 15:00 Beijing time (CST, UTC+8). The daytime close at 15:00 CST translates to 07:00 GMT in winter and 08:00 BST in summer. Most London-based front-office traders are at their desks by 07:30. SHFE has already closed.

SHFE also runs a night session for base metals from 21:00 to 01:00 CST. In London winter hours (GMT), that session runs 13:00 to 17:00, directly concurrent with LME afternoon trading and the London close window.

SHFE Session Timing Effects on LME Pricing Decisions

SHFE's daytime close is the primary actionable session for London-based traders because it captures overnight Chinese market sentiment and settles before LME electronic trading reaches maximum volume. The night session, running concurrent with LME afternoon trading, creates a live cross-market basis reading during the most directionally significant part of the London session.

That dual-session structure creates two distinct integration points: a morning review of daytime close data to anchor the day's basis view, and a live monitoring function during afternoon LME trading where SHFE night session movement can confirm or contradict a directional thesis in real time.

Neither integration point requires an analyst. Both require a platform that surfaces the data at the correct moment in your workflow rather than in a separate research environment.

The LME-SHFE Basis Relationship in Physical Pricing

For traders dealing in physical refined cathode, ingot, or concentrate, the LME-SHFE basis functions as position arithmetic with direct margin implications.

Converting an SHFE price to a USD/tonne equivalent requires three inputs: the SHFE settlement price in CNY/tonne, the spot CNY/USD exchange rate, and an import parity adjustment covering Chinese VAT (currently 13% for most base metals), applicable import duties, and freight. According to CRU Group, import parity calculations can shift by $80 to $120/tonne in a high-volatility month based on FX movement alone CRU base metals analysis. That range is large enough to invert a marginal physical trade.

Accessing SHFE Copper Pricing Without an Overnight Subscription

SHFE settlement prices are published after each session and available through market data vendors carrying Asian exchange feeds, including Bloomberg, Reuters Eikon, and purpose-built commodities platforms. You need a platform that pre-builds the conversion calculation and surfaces the basis reading without requiring you to pull three separate data sources and run the arithmetic manually.

When that calculation is pre-built into the workflow, reviewing the morning basis is reading a number. Without it, reviewing the morning basis is building a spreadsheet, a process that delays, rather than informs, the first trading decision of the day.

The distinction depends on whether the platform is doing the assembly work or offloading it to the trader at the worst possible time.

How SHFE Pricing Integration Works Without a Dedicated Analyst

The headcount argument against SHFE integration rests on a specific assumption: processing Asian market data requires specialist knowledge that a front-office trader cannot absorb during an active trading session. That assumption is only valid when the platform forces raw data consumption instead of delivering structured outputs.

Structured SHFE integration delivers three outputs:

- Basis reading: SHFE price converted to USD/tonne using live FX, compared to LME cash or three-month, displayed with a directional indicator versus the prior session and a deviation flag against the 20-session rolling average.

- Session quality indicator: SHFE settlement volume and open interest changes flagged when they deviate significantly from the 20-session average, distinguishing conviction moves from thin-session drift that can produce misleading price prints.

- Inventory context: Shanghai bonded and on-warrant warehouse inventory changes mapped directly against the basis reading, so price signals are cross-referenced against their physical market explanation without a separate research step.

Using SHFE Context During LME Trading Hours

During the LME morning session, traders use the SHFE daytime close as a directional anchor. If SHFE copper settled sharply higher on above-average volume, that serves as a confirmed bid signal entering the LME open.

During LME afternoon trading, the live SHFE night session provides concurrent validation: an LME rally that fails to see SHFE night session confirmation is a divergence worth sizing against before the London close.

In both cases, the operational value is the same: the trader is working from pre-processed, contextualized signals rather than running a multi-source data assembly exercise while the market is moving.

Building Your Morning Workflow Around SHFE Pricing Context

A morning workflow that properly integrates SHFE pricing context should take three to eight minutes. The sequence is as follows:

Step 1: SHFE daytime close review (60 to 90 seconds)

Check SHFE settlement prices for each metal in your active position. Note the direction and magnitude versus the prior daytime close. Flag any metal where the SHFE overnight move materially exceeds the LME close-to-close move from the prior London session. Those divergences identify the basis candidates worth examining before the Ring.

Step 2: Basis deviation check (60 to 90 seconds)

Review the pre-calculated LME-SHFE basis for your active metals. Note whether the current basis is wider or tighter versus the 5-day and 20-day averages. A move greater than one standard deviation from the 20-day average is a physical market signal with enough magnitude to affect hedge ratio decisions.

Step 3: Inventory context (60 to 90 seconds)

Cross-reference Shanghai bonded inventory updates against the basis reading. SMM publishes bonded copper data weekly; SHFE on-warrant data is available daily. If basis compression is accompanied by rising bonded inventory, the signal has physical confirmation. If they diverge, the basis move warrants additional scrutiny before you act on it.

Step 4: Position framing (2 to 3 minutes)

Map the basis reading against your open positions. If you hold LME copper longs and SHFE is showing basis compression on rising bonded inventory, your risk profile has changed from the prior close, even if LME hasn't moved yet. This is where the three prior steps convert into a trading decision.

According to Fastmarkets, LME-SHFE copper basis movements have preceded LME price direction changes by one to three sessions during periods of significant Chinese demand shifts, suggesting the basis functions as a leading rather than coincident indicator in those environments Fastmarkets copper basis analysis. A morning workflow built around this sequence captures that lead time systematically rather than retroactively.

Steps one through three require no analytical judgment; they require a platform that delivers pre-calculated outputs. Step four is where the trader's judgment is applied. That division of labor is what makes SHFE integration headcount-neutral.

What SHFE Integration Actually Looks Like in Practice

The practical test of SHFE integration is whether a front-office trader can answer four questions before the LME Ring opens:

- Where did SHFE settle relative to the LME equivalent, and in which direction?

- Is the current basis wider or tighter than recent averages, and by how much?

- Did SHFE volume confirm the directional move, or was it a thin-session print?

- What is Shanghai bonded inventory doing versus the trend?

Differences Between SHFE and LME Copper Pricing

LME copper reflects global price discovery anchored by warrant trading across LME-approved warehouses worldwide, futures spread trading, and physical delivery obligations. SHFE copper reflects Chinese domestic market conditions: on-warrant and bonded Shanghai inventory levels, domestic smelter output, PBOC monetary policy effects on trader financing, and Chinese fabrication demand cycles. The two markets are linked by arbitrage but frequently diverge: the SHFE-LME copper spread has historically ranged from a $200/tonne premium to a $150/tonne discount depending on domestic Chinese supply-demand dynamics.

According to the International Copper Study Group (ICSG), China accounts for approximately 55% of global refined copper consumption ICSG copper balance data. A pricing mechanism that reflects 55% of global demand serves as a core market signal, and omitting it from the intraday workflow is a structural gap in market coverage.

SHFE Pricing Intelligence as a Base Metals Platform Standard

Positioning SHFE data access as a premium feature (something unlocked at higher subscription tiers or requiring specialist onboarding) reflects an incomplete understanding of base metals market structure. It is not a credible product position for any platform that claims to provide genuine base metals intelligence.

The LME, MCX, COMEX, and SHFE together constitute the global pricing architecture for copper, aluminum, zinc, nickel, lead, and tin. A platform integrating only three of the four exchanges delivers a partial dataset with a gap precisely where Chinese price discovery occurs.

According to the World Federation of Exchanges 2023 annual statistics, SHFE ranks among the top five commodity exchanges globally by contracts traded, with SHFE copper alone regularly generating daily volume exceeding 200,000 lots WFE 2023 statistics. These represent the dominant volume center for the world's most-consumed industrial metal.

A depth-first approach to base metals intelligence means every exchange that contributes meaningfully to price discovery for a covered metal must be integrated at the workflow level.

SHFE is a mandatory inclusion for copper, aluminum, and zinc. It forms part of the complete picture that a serious base metals platform is obligated to provide as a baseline.

Front-office traders should not be building spreadsheet bridges between SHFE settlement data and their LME position views. That workflow friction represents a platform design gap.

Making SHFE Pricing Context Operational Today

SHFE pricing context is no longer a barrier to integrate into the intraday decision cycle. The session timing structure creates a natural workflow anchor: SHFE daytime close data is available before LME morning liquidity peaks, and SHFE night session data runs concurrent with LME afternoon trading. Both windows are actionable with pre-processed signals rather than raw data assembly, provided the platform is doing the conversion and contextualization work it should be doing.

Three concrete steps to make this operational without adding headcount:

- Audit your current morning brief. If answering the four SHFE questions above takes more than five minutes or requires more than one platform, you have identified a workflow gap.

- Require pre-calculated basis outputs. The LME-SHFE basis calculation involves arithmetic that a purpose-built platform should deliver as a standard workflow element. If your current platform requires you to perform that calculation manually, the platform is not built for base metals depth.

- Use volume alongside price. SHFE settlement price without session volume context is incomplete. A sharp SHFE move on thin volume is categorically different information from the same move on elevated volume. Both data points belong in the same view.

Novaex base metals platform overview to see how SHFE, LME, MCX, and COMEX pricing are integrated into a single workflow view built for depth-first base metals intelligence.