Commodity Data vs. Trading Intelligence: The Gap

Your data vendor and your trading intelligence platform are not the same system. This is true even when trading infrastructure treats them as equivalent. A data vendor delivers prices, settlement values, and exchange feeds. A trading intelligence platform synthesizes that data into decision-context: position-adjusted exposure, hedge effectiveness signals, and executable risk output specific to your book. The gap between these two functions is structural. It is also measurable in the daily manual work your desk absorbs to bridge it.

The base metals trading industry has a name for the infrastructure that performs this bridging. Most desks have not yet built it.

What Commodity Data Vendors Are Actually Built to Do

Data vendors are infrastructure businesses. Their core engineering problem is reliability and coverage: delivering accurate, low-latency price feeds from LME, COMEX, MCX, and SHFE to as many subscribers as possible with maximum uptime and minimum distortion.

According to a 2023 Coalition Greenwich institutional data study, the average commodity trading desk subscribes to between four and seven market data services simultaneously. Each is optimized for a different exchange, asset class, or data type. That fragmentation is not a product failure. It reflects how data vendor businesses are designed: around feed delivery, not decision support.

A data vendor's output is designed to be consumed downstream by a spreadsheet, a risk system, a CTRM, or a trader's screen. The vendor's function ends at delivery. What happens next is architecturally outside its scope.

Data Vendors Do Not Provide Trading Signals

Data vendors do not provide trading signals because their product depends on neutrality. A vendor serving hundreds of firms cannot embed directional logic or firm-specific position context without compromising the product's universality and its standing as an independent price reference. Signal generation requires context that only exists inside one firm's operational data: your specific position, your open hedges, your board-approved risk limits.

This represents an architectural boundary. The vendor is performing exactly as designed.

Understanding that boundary is the first step in correctly classifying what your desk is and is not receiving when the feed updates.

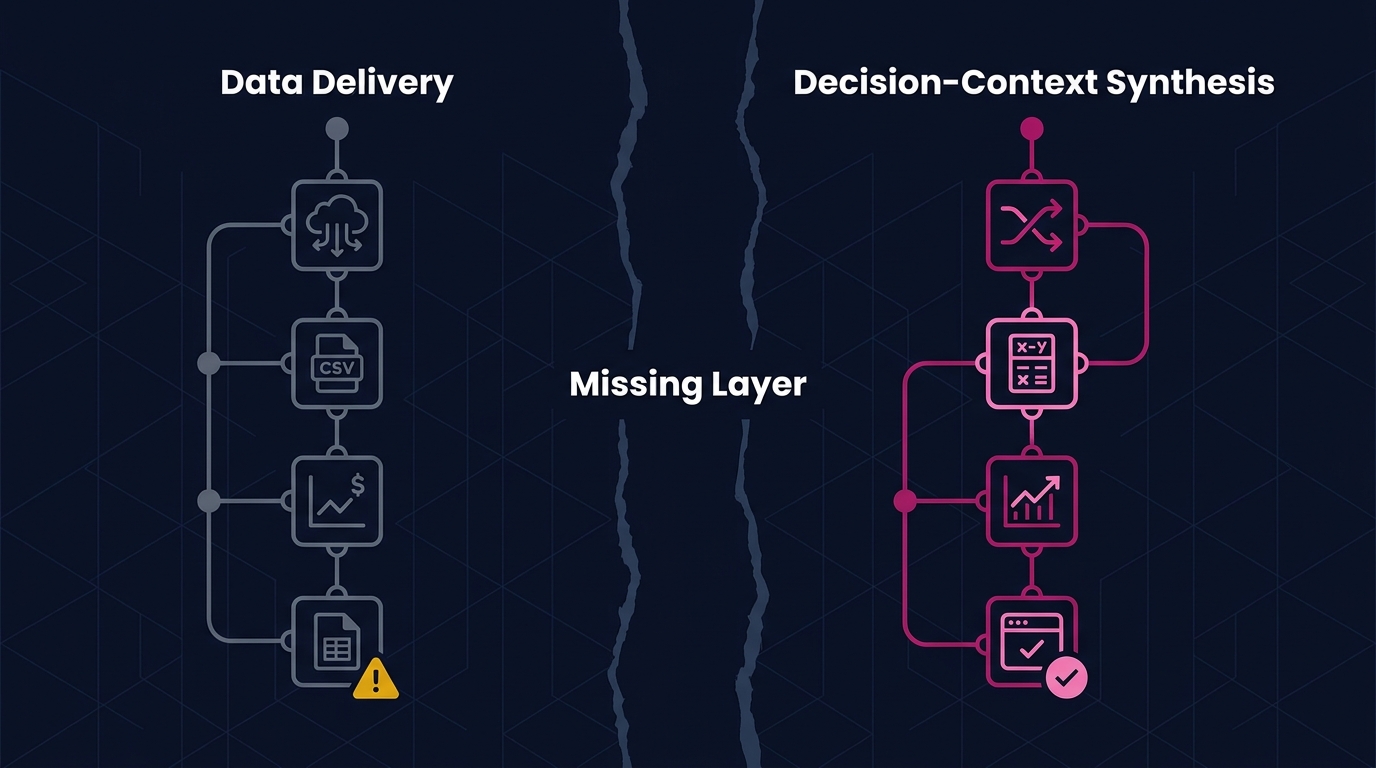

The Missing Layer in Commodity Trading Intelligence

Between raw data delivery and a trader's executable decision sits a layer that most desks have never formally named. This is the synthesis layer: the operational process that takes incoming market data and maps it against a desk's live position, open hedges, physical book, and risk thresholds to produce position-specific output.

According to a 2022 Accenture commodity trading operations study, traders at mid-market metals desks spend an estimated 25-35% of their active working time on manual data assembly. This includes pulling feeds from multiple sources, reconciling settlement prices against internal records, and translating raw market moves into position-adjusted P&L views.

This represents manual synthesis layer construction, performed daily by professionals whose expertise belongs elsewhere.

The synthesis layer, when formalized, produces four specific operational outputs:

- Position-adjusted exposure: What a given price move means for your book, not the market in aggregate

- Hedge effectiveness signals: Whether existing hedges are performing as modeled or diverging on basis

- Threshold breach alerts: When a market move crosses a pre-defined risk parameter tied to actual position size

- Executable decision context: The minimum information required to take or modify a position with confidence

The Process of Decision-Context Synthesis in Commodity Trading

Decision-context synthesis is the process of transforming raw market data into position-specific intelligence a trader can act on without additional manual steps. It maps current LME or COMEX price movements to an open physical position, runs those movements through pre-set hedge ratios, and surfaces the outputs as direct answers to a single operational objective: determining what a market move means for the book immediately.

Synthesis requires the structural integration of market data, position state, and risk parameters into a single calculation engine that updates continuously as inputs change.

A desk that receives data but not synthesis receives half the infrastructure required to trade with precision. The other half is being assembled manually.

Why the Commodity Data Intelligence Gap Has Measurable Cost

The gap between data delivery and decision-context synthesis produces recurring financial exposure in the daily operational reality of metals desks running physical and financial positions simultaneously.

According to a 2021 Oliver Wyman risk operations report, manual reconciliation processes in commodity trading introduce an average four-to-six-hour lag between a significant market event and a fully-reconciled risk position. During that window, the desk is managing live exposure against an inaccurate view of its own book.

On the LME, copper moves 2-3% within a single session on macro catalyst events, generating a $150-200 per metric ton swing that translates directly to P&L for any unhedged or partially hedged position. A desk that requires four hours to synthesize that move into a position-adjusted view is making hedge decisions against stale data during the period when precision matters most.

The Impact of Data Fragmentation on Metals Hedging

Data fragmentation affects metals hedging by forcing traders to maintain multiple price references that may not resolve to the same value at the same time. LME official settlement, COMEX front-month, and SHFE prices operate on different time zones and different contract specifications. Without an integrated synthesis layer mapping these references to a single position framework, basis risk accumulates silently inside the gap between data sources.

A copper desk running physical and financial books across two exchanges faces this problem structurally every day. The vendor delivers the price. The desk manually constructs the bridge from price to position under time pressure, using systems that were never designed to communicate with each other.

According to LME 2023 market statistics, the three-month copper contract averages over 400,000 lots per month in traded volume. Each lot represents 25 metric tons. At that scale, even a one-day reconciliation lag on a modestly sized physical book represents material untracked basis exposure.

LME copper contract specifications and hedging mechanics

The Architecture of Integrated Commodity Trading Intelligence

A platform built for commodity trading intelligence operates on a different architectural premise. It acts as a calculation layer that holds live position state.

Integrated trading intelligence requires three structural components operating simultaneously:

- Live market data ingestion: Real-time pricing from relevant exchanges, settlement curves, and forward structures

- Position state management: A continuously updated record of physical book, financial hedges, and net exposure by metal, contract date, and geography

- Synthesis engine: The calculation layer that maps component one against component two in real time, producing position-adjusted intelligence outputs

Outputs of a Trading Intelligence Synthesis Layer

A synthesis layer produces outputs that answer specific operational questions a trader faces in real time. These include the effect of today's LME cash-to-three-month spread on a carry position, the current delta on a hedge given the front-month move, and current standing relative to board-approved risk limits.

These are not reports. They are live state answers. They require all three architectural components to be simultaneously active and integrated. A desk that has components one and two but not three receives data and maintains records. It does not receive intelligence.

Legacy CTRM Platform Limitations in Real-Time Intelligence

Legacy CTRM platforms struggle with real-time intelligence because they were designed as record-keeping systems, not calculation engines. Their core function is transaction capture, contract management, and settlement workflow. These batch processes are built around end-of-day data states.

Real-time synthesis requires continuous position recalculation against live market feeds, an architectural demand legacy CTRMs were not built to fulfill.

The result is a desk with accurate position records but stale position intelligence. These are structurally different operational conditions that look identical until the market moves fast.

According to a McKinsey commodity analytics survey, firms using three or more disconnected data and risk systems report 40% higher rates of hedge accounting exceptions and manual override incidents compared to firms using integrated platforms. The exceptions do not occur because any single system failed. They occur because no system owned the synthesis.

CTRM platform evaluation criteria for metals desks

How the Synthesis Gap Persists in Practice

The synthesis gap persists because the component pieces typically exist in separate systems that were never designed to communicate. A data vendor, a CTRM platform, and a risk reporting tool each perform their defined function correctly. The gap lives in the handoffs between them, or more precisely, in the architectural absence of those handoffs.

This is the classification error at the center of the assumption this article addresses. The desk has data infrastructure. It has position infrastructure. It has assumed those two categories together constitute trading intelligence. They do not. Trading intelligence requires a third category: synthesis infrastructure.

According to a 2022 Gartner analysis of commodity technology stacks, organizations that identified and addressed synthesis gaps in their trading infrastructure reported a 30% improvement in hedge execution timing, specifically in the critical window between market signal and position-adjusted response.

That window is where hedging decisions are made. It is also where the synthesis gap is most expensive.

Commodity Trading Intelligence Built Depth-First

The depth-first methodology applied to base metals changes what a synthesis layer can do. Rather than building generalizable analytics across multiple asset classes, it models the specific pricing behaviors, forward curve structures, and basis relationships of LME copper, aluminum, zinc, lead, nickel, and tin with sufficient resolution that the synthesis engine produces accurate, exchange-specific output rather than approximations.

This precision matters because base metals have structural pricing relationships that generic commodity analytics do not model correctly. The LME's prompt-date system, COMEX futures mechanics, MCX rupee-denominated pricing, and SHFE warehouse-delivery structure interact differently for each metal. A synthesis layer that treats them identically produces position-adjusted intelligence that is approximately right. This creates a different operational condition than being precisely right when a position is large and a market is moving.

According to a 2023 Deloitte metals trading technology review, base metals desks that implemented integrated pricing and position analytics reported a median 60% reduction in time spent on manual reconciliation within the first six months of deployment. The synthesis layer, built into the platform as infrastructure rather than manual process, eliminates the daily reconstruction cost entirely.

The desk receives decision-context. The trader trades.

depth-first approach to base metals trading intelligence

The Structural Finding: A Classification Correction

The architectural finding this analysis documents is precise:

Your data vendor is performing correctly. Your CTRM is performing correctly. The structural gap exists in the synthesis layer that neither system was designed to own.

This is not a critique of any vendor relationship. It is a classification correction. Data delivery and decision-context synthesis are two different engineering problems requiring two different architectures. Treating one as a substitute for the other is the misclassification. It manifests as manual workarounds, reconciliation lag, and hedging decisions made against an incomplete view of the book.

Recognizing the gap does not require immediate vendor replacement; it requires naming the missing layer, measuring its cost, and evaluating whether your current stack contains synthesis infrastructure or data infrastructure with the gap filled by human effort.

Closing the Synthesis Gap: Three Steps for Metals Desks

The reframe this article presents is structural. It does not prescribe a vendor change. It names the missing layer so you can evaluate whether your current stack contains one, and what it is costing your desk to operate without it.

Three immediate diagnostic actions:

- Map your synthesis workflow: Document every manual step between receiving a market data update and arriving at a position-adjusted risk view. That document is a precise picture of your current synthesis gap, including the professionals absorbing it daily and the cumulative time cost.

- Measure your reconciliation lag: Time the interval between a significant LME price move and your desk's fully-reconciled position P&L. That lag, expressed in minutes or hours, is the cost of the missing synthesis layer stated as operational risk.

- Ask the distinguishing question when evaluating platforms: Ask whether the platform holds live position state and synthesizes it against real-time market feeds continuously, or if it delivers data for manual synthesis. That answer separates data infrastructure from trading intelligence infrastructure.

Novaex base metals trading intelligence platform overview

base metals hedging workflow evaluation guide