Zinc Forward Curve: Two Signals Every Buyer Must Read

The zinc forward curve simultaneously communicates two distinct things: physical supply tension embedded in LME-approved warehouse stock dynamics, and directional bias from speculative positioning roll patterns. Front-month price communicates neither. When sourcing decisions begin and end with the cash price, only one variable from a multi-factor equation enters the analysis. That gap has produced measurable, documented losses for physical buyers at specific moments in zinc market history.

To avoid these losses, buyers must identify both signal layers precisely, apply them to historical zinc curve episodes where they diverged, and establish what reading the zinc forward curve properly requires in practice.

The Zinc Forward Curve Carries Two Simultaneous Signals

Most price analysis treats the zinc forward curve as a single instrument: a continuous line of prices stretching from the cash date into the future.

That framing is incomplete.

The zinc forward curve is the superposition of two independent information layers, each generated by a different set of market participants with different objectives. Reading the curve without separating those layers is like interpreting a double-exposure photograph as a single image. The signals interfere with each other until they are isolated.

Signal Layer One: LME-approved warehouse stock dynamics. The spread between the LME cash price and the 3-month price reflects, among other factors, the physical availability of metal in LME-registered locations. When stocks in approved warehouses fall sharply, nearby spreads move toward backwardation: sellers of prompt contracts command a premium because metal is genuinely harder to source. When stocks build, the market moves toward contango, reflecting the cost of carrying metal over time.

Signal Layer Two: Speculative positioning roll patterns. Financial participants; commodity funds, proprietary desks, commodity trading advisors; take positions across the curve and must roll them forward as expiry approaches. The pattern, timing, and concentration of those rolls shape the spread structure independent of physical inventory. According to LME published positioning data LME open interest and positioning data, managed money participants regularly account for a significant fraction of LME zinc open interest, meaning their roll activity is structurally capable of moving spreads without any change in warehouse availability.

A heavily net-long financial community rolling from front-month into the 3-month will bid up the nearby contract and pressure the deferred, creating spread behavior that looks identical, from the number alone, to a physical tightening event.

Why does front-month zinc price mislead physical buyers?

Front-month price misleads physical buyers because it captures only the current clearing price at a single delivery point in time. It carries no information about whether that price reflects physical scarcity, financial accumulation, or both simultaneously. A cash price of $3,200/t means something categorically different if nearby spreads are in $80/t backwardation driven by depleted warehouses versus if they reflect a large speculative long rolling aggressively into the next prompt date. The sourcing decision that follows should differ accordingly, and front-month price alone provides no basis for making that distinction.

Signal One: LME Warehouse Stock Dynamics and Physical Reality

LME-approved warehouses function as the inventory buffer of last resort for the global zinc market. Their stock levels; published daily by the LME LME daily warehouse report; are among the most reliable leading indicators of physical tightness available to any market participant without access to proprietary producer data.

The mechanism is direct: when physical consumers cannot source zinc through producer contracts or spot purchases, they draw from LME warehouses. Warrant cancellations (the administrative step that precedes physical delivery out of a registered location) spike. Reported stocks fall. The cash-to-3-month spread tightens, then inverts into backwardation.

That backwardation carries specific meaning for a sourcing decision. It tells you the market is paying a premium for metal now, which implies that forward delivery may become structurally cheaper as supply normalizes. A buyer who understands this signal can make a calibrated decision: cover immediate needs at the elevated nearby price while locking in lower-cost forward volume. This strategy is invisible to anyone reading only the front-month number.

How do LME zinc warehouse stocks signal a tightening market?

LME zinc warehouse stocks signal tightening through three sequential mechanics: rising cancellation rates as warrants are pulled from deliverable inventory, accelerating week-over-week stock drawdowns across registered locations, and spread inversion from contango into persistent backwardation. According to LME warehouse reports from mid-2006, LME zinc stocks had declined from over 1 million tonnes in 2002 to below 100,000 tonnes by the summer of 2006, a multi-year drawdown driven by structural supply shortfalls that the curve was communicating clearly well before the price spike became impossible to ignore.

The inventory signal in the curve preceded and confirmed the price move. A sourcing decision informed only by the spot price at any point during that drawdown would have missed the structural urgency the inventory data and spread structure were broadcasting across the full curve.

Signal Two: Speculative Positioning and Roll Patterns

Financial participants operate on a logic entirely separate from physical buyers. A commodity fund does not need zinc delivered to a warehouse in Rotterdam; it needs a return on a price position held for days or weeks. Its interaction with the curve is real and measurable, but its footprint is structurally different from a physical flow.

The LME publishes weekly positioning data on managed money participation LME managed money positioning zinc. Even without parsing those reports in detail, the pattern of how and when funds roll their positions is detectable in spread behavior across prompt date windows.

The key observable: when a concentrated net-long financial community approaches front-month expiry and begins rolling into the 3-month contract, the cash contract is bid up relative to the deferred, compressing or inverting the spread. This generates backwardation that is structurally indistinguishable from a physical tightening event if you look only at the spread number.

The critical difference: if the backwardation is speculative roll-driven, it will typically reverse sharply once the roll window closes. Physical stock levels will remain unchanged or may actually be building. A buyer who responds to that spread signal by accelerating purchases or paying a spot premium is reacting to a financial artifact, not a physical reality. According to commodity market research published by Macquarie's base metals team Macquarie base metals research, divergence between spread behavior and LME inventory trends has been a consistent, repeating feature of LME zinc markets during periods of elevated managed money positioning.

How can you distinguish speculative roll pressure from physical tightness?

The most reliable method is cross-referencing the spread move against LME stock levels and warrant cancellation rates simultaneously. If spreads invert while warehouse stocks remain stable or are growing and cancellations are low, the backwardation is more likely roll-driven. A second method is examining the term structure beyond the front prompt: physical tightness tends to create backwardation concentrated in the near term that fades progressively over longer tenors as the market prices in eventual supply normalization. Speculative positioning effects, by contrast, create spread anomalies at specific roll dates that are not matched by corresponding structural shifts further out the curve.

When Signals Align: The 2006, 2007 Zinc Super-Spike

The 2006 zinc cycle is the clearest historical example of both signal layers pointing in the same direction simultaneously, and why that alignment produces an extreme, sustained market move.

The physical signal was unambiguous. As documented by ILZSG [LINK: ILZSG zinc market statistics], the global refined zinc market ran in consecutive annual deficits through the mid-2000s, driven by rising infrastructure demand from China and a production pipeline that had not kept pace. LME stocks had fallen from over 1 million tonnes to below 100,000 tonnes, a 90-plus percent drawdown that represented genuine, structural scarcity, not seasonal noise. Warrant cancellations remained elevated. The cash-to-3-month spread moved into persistent backwardation, confirming that the market could not satisfy prompt demand from exchange inventory.

The speculative signal amplified the physical one. Zinc's fundamental tightness attracted commodity fund positioning within the broader supercycle narrative of the mid-2000s. Large net-long financial positions accumulated across the curve. Their roll activity during prompt date windows amplified the backwardation already generated by physical drivers. According to price data from the LME, zinc rose from approximately $1,000/t in early 2005 to above $4,500/t by late 2006. This move reflected the compounding of two aligned signals rather than either alone.

A physical buyer reading only the front-month price during 2006 would have observed a rising market. Two operationally critical pieces of information would have remained out of view: first, that the full backwardation structure made forward purchases materially cheaper than prompt, creating a strategic opportunity to lock in deferred volume at a discount; second, that speculative amplification was inflating spot premiums beyond fundamental justification, informing how aggressively to cover near-term needs versus waiting for financial rollover to create a brief retracement window.

Both pieces of information were in the curve. Neither was in the front-month price.

When Signals Diverge: The 2022, 2023 Zinc Curve

The 2022, 2023 zinc episode is the more instructive case for sourcing professionals because the two signal layers pulled in opposite directions, and reading only one produced a categorically wrong market view.

The physical signal was tight. European zinc smelter capacity was curtailed sharply following Russia's invasion of Ukraine and the resulting energy price crisis. According to the International Zinc Association International Zinc Association production data, curtailments at facilities including Nyrstar's Budel plant in the Netherlands and Glencore's Portovesme smelter in Sardinia removed an estimated 500,000 tonnes of annual refined zinc capacity from the European market. LME zinc stocks, already at multi-year lows entering 2022, fell further. The cash-to-3-month spread moved into significant backwardation at multiple points through late 2022 and into early 2023, confirming that prompt availability was genuinely constrained.

The speculative signal was bearish. Simultaneously, rising global interest rates, deteriorating demand expectations in key end-use sectors, and broad risk-off positioning across commodities drove fund managers to reduce zinc exposure. Managed money net longs were declining. The roll pattern during this period reflected not bullish extension but position unwinding; longs rolling out while deferred contracts softened under the weight of emerging short positioning.

The result was a curve in structural conflict: near-term backwardation signaling physical tightness, deferred term structure softening as financial participants priced in demand destruction. According to LME price data, zinc peaked above $4,500/t in April 2022 before declining sharply through the second half of the year, ending 2022 near $3,000/t. This trajectory coexisted with ongoing smelter curtailments.

What happened to zinc prices when European smelters curtailed in 2022?

LME zinc prices rose sharply into the curtailment period and then declined substantially despite supply constraints remaining in place, because the speculative layer of the curve was simultaneously pricing deteriorating demand. According to ILZSG data published for the period, refined zinc production fell while consumption projections were revised downward, meaning both supply and demand were contracting. A sourcing professional relying on the spot price alone had no framework for reconciling these competing dynamics. The curve structure; read across both layers; provided exactly that framework: cover near-term needs because physical supply was genuinely tight, but avoid extending forward hedges aggressively because financial participants were pricing a weaker demand environment into longer tenors.

The buyer who misread the backwardation as purely physical and built forward cover at elevated deferred prices during mid-2022 paid for that misread in the months that followed.

What the Zinc Forward Curve Tells You That Front-Month Price Cannot

A front-month zinc price tells you one thing: the current clearing price between buyers and sellers for prompt delivery.

The full zinc forward curve tells you a categorically larger set of things:

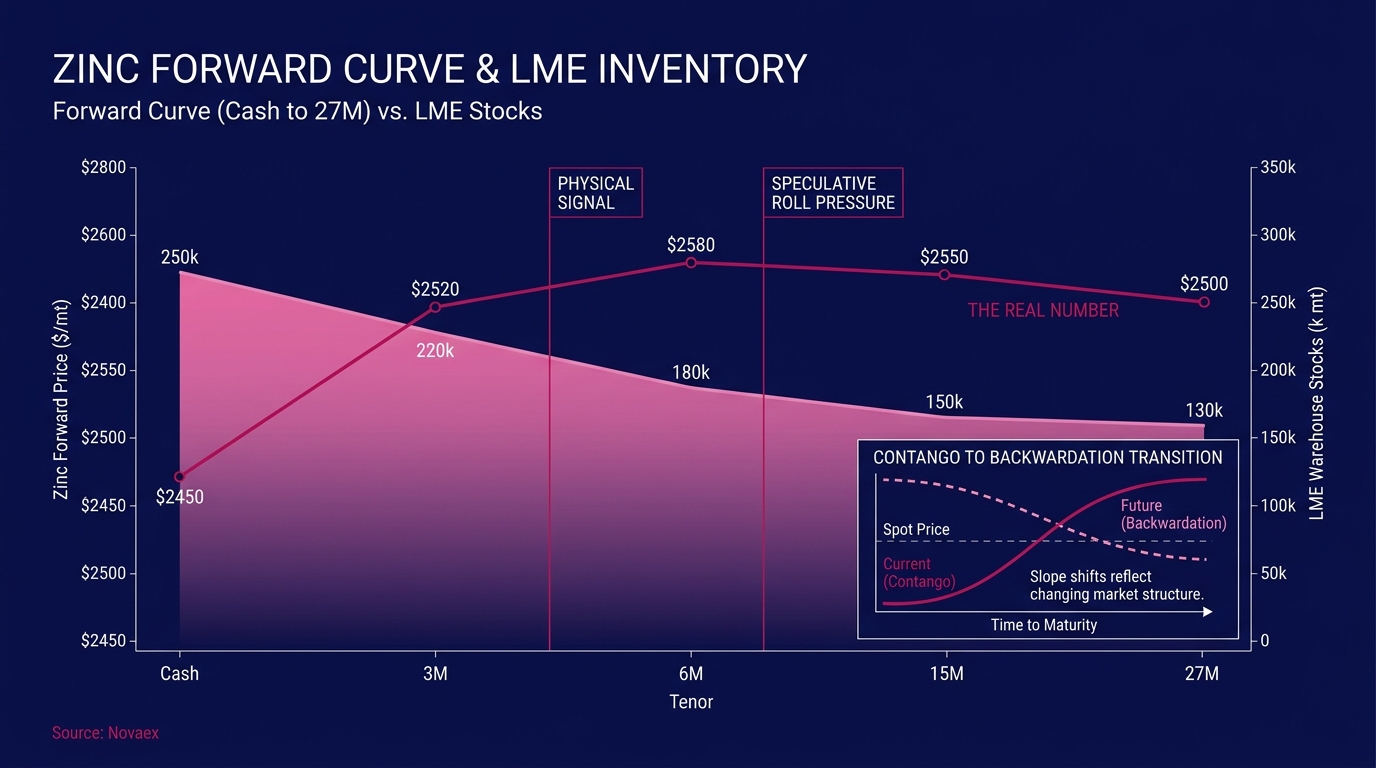

- The spread structure shape across cash, 3-month, 15-month, and 27-month dates, encoding the market's collective assessment of physical balance at each point in time

- The character of any backwardation or contango, which can be decomposed into inventory-driven and positioning-driven components when read against LME stock data and cancellation rates

- The implied cost of carry versus the actual spread, which identifies whether the market is pricing physical scarcity or financial crowding

- The term structure drift over successive sessions, which signals whether tightness is structural and self-reinforcing or transient and roll-window-specific

According to research from Wood Mackenzie's base metals practice Wood Mackenzie zinc market research, sourcing decisions informed by full curve structure carry demonstrably different risk profiles than those made on spot price reference alone, particularly in zinc, where the combination of a relatively concentrated physical market and active financial participation creates recurring episodes of spread dislocation that are large enough to affect procurement economics materially.

How do you read zinc backwardation vs. contango for sourcing decisions?

Backwardation in zinc (cash price above forward prices) signals that prompt metal is scarcer or more valuable than deferred supply. For physical buyers, backwardation in an inventory-depleted environment is a directive to secure near-term supply and consider locking forward volumes at the lower deferred prices visible in the curve structure. Contango (cash price below forward prices) signals ample nearby availability and rewards storage; for buyers it implies no urgency in prompt procurement and may favor spot purchases over forward commitment. The critical qualification is that neither reading is reliable without first determining which signal layer is driving the spread. Physical tightness and speculative positioning can produce identical spread shapes with opposite implications for sourcing strategy.

Building Zinc Forward Curve Awareness Into Physical Sourcing Workflows

Translating dual-signal curve awareness into operational practice requires three workflow changes that most physical sourcing desks have not yet formalized.

1. Replace the spot check with a curve snapshot.

Every sourcing decision should begin with a five-point curve snapshot: cash, 3-month, 6-month, 15-month, and 27-month prices. This takes approximately the same time as pulling a single spot price and produces incomparably more decision-relevant context. The cash-to-3-month spread alone, and its direction of travel over recent sessions, tells you whether the physical environment is tightening or relaxing and at what rate.

2. Cross-reference the spread against LME inventory data.

The LME publishes daily warehouse stock reports and warrant cancellation data LME daily warrant and stock report. Before any significant sourcing commitment, the spread reading should be cross-referenced with the current stock level and the week-over-week cancellation trend. If spread tightness is accompanied by rising cancellations and falling stocks, the physical signal is confirmed. If the spread is tight but stocks are stable or building, the pressure is more likely speculative and should be weighted accordingly.

3. Track the speculative positioning calendar.

LME positioning data and the exchange's published prompt date calendar allow you to identify roll windows, periods when financial participants are most likely managing position expiry. Understanding when these windows fall helps separate roll-driven spread moves from fundamental ones. According to workflow analysis among physical metals trading desks conducted by a major commodity risk consultancy commodity trading workflow benchmarking, teams that integrated full-curve monitoring into their daily workflow identified procurement cost reduction opportunities that were structurally invisible to spot-price-only monitoring.

Why is curve structure more reliable than spot price for hedging decisions?

Spot price reflects only the current moment of equilibrium between buyers and sellers. Curve structure reflects the collective forward expectations of both physical and financial participants, weighted by their actual capital commitments across multiple time horizons. For hedging decisions specifically, curve structure determines the real cost of establishing a forward position: not just the reference price, but the roll cost, the carry differential, and the implied supply trajectory that will govern whether the hedge performs as intended. Establishing a hedge against a misread curve is not risk management; it substitutes one exposure for another, less transparent one.

The Minimum Standard for Zinc Sourcing Intelligence

The zinc market has produced multiple documented episodes (2006, 2017, 2022) where the forward curve communicated categorically different information than the front-month price. In each case, the spread structure and inventory dynamics told a story that no spot price ever could. In some episodes the signals aligned and amplified each other. In others they diverged and demanded simultaneous interpretation. In every case, the front-month price alone was insufficient to support the decision in front of a sourcing professional.

Reading the zinc forward curve for its two simultaneous signal layers (LME-approved warehouse stock dynamics and speculative positioning roll patterns) is not advanced practice reserved for specialist desks. It is the minimum standard for informed physical sourcing decisions.

Professionals who hold themselves to that standard need tools that deliver the full curve, the inventory overlay, and the positioning context in a single workflow, not assembled manually across three separate data sources in the minutes before a decision has to be made. The analytical framework described in this post is not theoretically complex. The barrier is operational: most platforms do not build it into the daily workflow because they were not designed with zinc's specific market mechanics in mind.

Novaex was. A depth-first methodology means that before Novaex covers any commodity, it builds complete understanding of that market's unique signal structure, including the dual-layer dynamics documented here. That is the foundation on which base metals intelligence should be built, and the standard it should consistently deliver.

If your current workflow starts and ends with front-month price, the immediate next step is clear: pull the full zinc forward curve alongside the LME daily inventory report and make them a standing pairing. The signals are already there. The only question is whether your workflow is built to read both of them.

Novaex zinc market intelligence platform | LME zinc daily data and reports | ILZSG zinc market statistics archive