Cross-Exchange Basis Management for Metals Traders

Cross-exchange basis management in physical metals trading means tracking the price differential between correlated contracts on different exchanges (LME, COMEX, SHFE, MCX) while accounting for contract size mismatches, currency exposures, and delivery specification differences simultaneously. Get the basis wrong and the hedge is wrong, regardless of notional coverage.

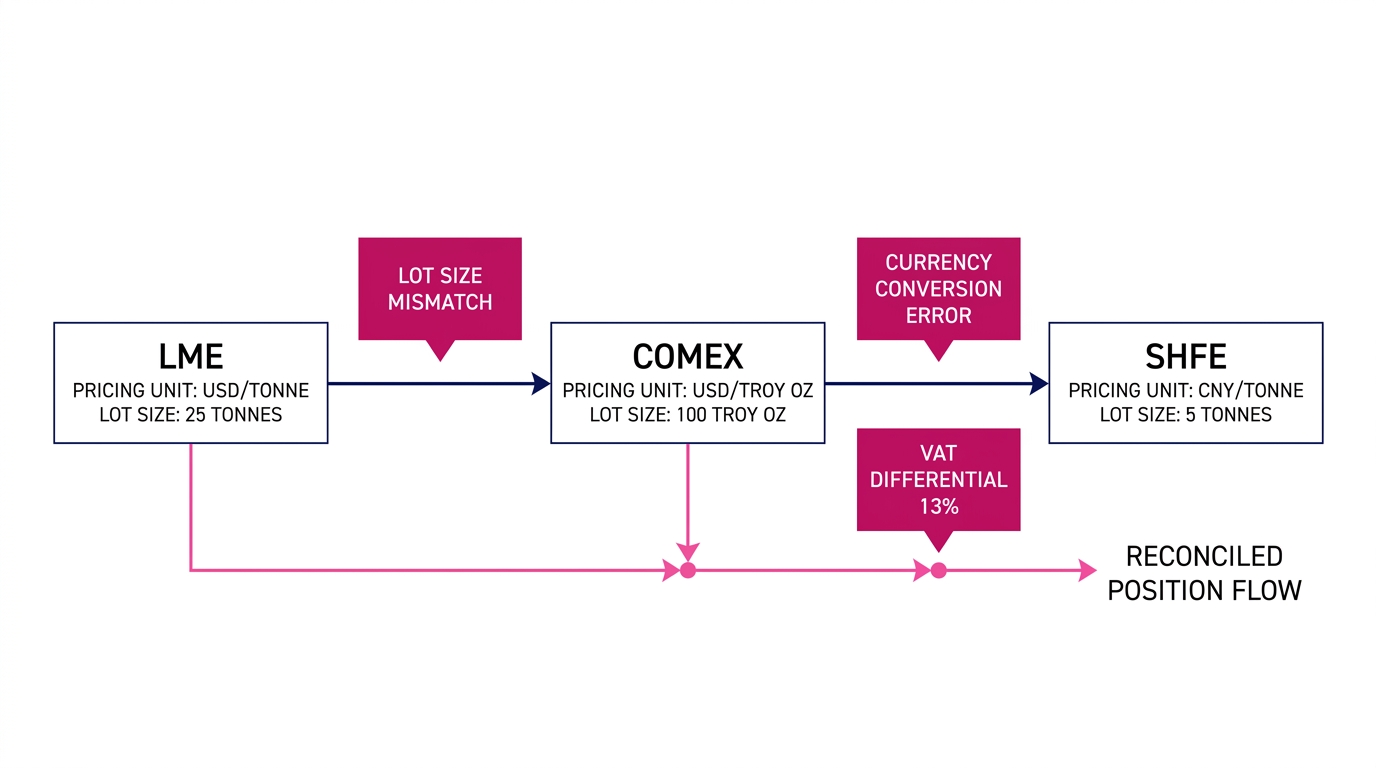

Physical metals traders face a compounding structural problem. The LME quotes copper in USD per metric tonne across 25MT lots on prompt dates. COMEX quotes the same metal in cents per pound across 25,000-lb lots on calendar months. SHFE quotes it in yuan per metric tonne across 5MT lots with a bonded-versus-domestic warehouse distinction that changes the effective price by the full Chinese VAT rate; currently 13%. Managing a basis book across all three exchanges without a unified position view produces reconciliation errors that compound into delivery disputes exactly when market volatility leaves the least time to resolve them.

What Cross-Exchange Basis Management Actually Requires

The LME-COMEX copper arb is the most actively traded cross-exchange basis in industrial metals. The spread, quoted in USD per metric tonne after converting COMEX's cents-per-pound price, moves on macro sentiment, US warehouse stock draws, and LME ring dynamics simultaneously. According to LME inventory data, copper warrant cancellations exceeded 150,000 tonnes in a single week during the Q4 2023 inventory cycle, compressing the LME cash-three-month spread into sharp backwardation while COMEX spot remained relatively stable. That divergence created basis exposure for any trader running a nominally flat cross-exchange book.

Defining Cross-Exchange Basis Risk

Cross-exchange basis risk is the risk that the price differential between equivalent contracts on two exchanges moves adversely after a trader has established offsetting positions. In copper, a long LME Grade A position hedged with a short COMEX contract carries spread risk. The LME-COMEX spread itself fluctuates continuously and can move 30-50 USD/MT in a single week during inventory stress events.

The basis is also structurally asymmetric. LME copper settles against the London cash price on specific prompt dates, whereas COMEX copper settles against a monthly average or a specific futures close depending on the contract month. A trader rolling an LME position through tom-next carries an entirely different cost structure than a trader rolling COMEX through first notice day; and the two roll costs diverge further when the LME forward curve shifts between contango and backwardation.

Managing this means tracking not just the flat-price spread but the forward curve basis; how the spread behaves across the LME's three-month, 15-month, and 27-month tenors versus COMEX's quarterly back months. According to CME Group contract specifications, COMEX copper open interest in deferred months routinely exceeds 40% of total open interest, meaning the forward basis market is liquid enough to hedge. But only if the position system distinguishes prompt-date exposure from calendar-month exposure in real time. This is a distinction many legacy CTRM systems treat as optional.

The LME-COMEX Copper Spread: Mechanics and Mismatches

The conversion from COMEX cents per pound to LME USD per metric tonne requires multiplying by 22.0462. That is arithmetically trivial until the position system is running 40 lots on each side and the USD/EUR currency cross is moving. A 0.5% USD/EUR move changes the effective LME price without touching the COMEX price, and the reverse applies when sterling moves on UK macro data during London ring hours, shifting the LME official price while New York has not yet opened.

LME and COMEX Contract Interaction

LME copper and COMEX copper represent the same underlying metal but in different delivery locations, lot sizes, and settlement structures. The LME's standard lot is 25MT of Grade A copper in specific shapes (cathodes, wire rod, or billets depending on the registered brand) deliverable to LME-approved warehouses in Rotterdam, Hamburg, Johor, Singapore, New Orleans, or Baltimore. COMEX requires US Grade 1 copper in cathode form, deliverable only to COMEX-licensed US warehouses. The physical delivery geography creates a structural basis component that does not disappear even when flat prices converge.

EFP (Exchange for Physical) transactions connect the two markets more directly. A merchant holding physical copper in a US warehouse can execute an EFP against a COMEX short to deliver into the exchange, then simultaneously establish the LME leg at a negotiated EFP differential. According to CME Group, EFP volumes in copper averaged over 8,000 lots per month in 2023, representing a material portion of physical settlement activity. Traders who do not track EFP differentials separately from exchange-to-exchange basis are combining two distinct risk sources into a single unmanaged number.

Lot size mismatch is a systematic source of residual exposure that compounds across a large book. A 10-lot LME position is 250MT. The nearest equivalent COMEX hedge is 22 lots (249.48MT), with a residual 0.52MT basis mismatch that accumulates at scale. Position systems that round to the nearest lot without flagging the residual produce phantom balance: the books appear flat when they are not, and the discrepancy appears at mark-to-market time rather than at trade capture where it can be managed.

LME copper contract specifications

COMEX copper contract specifications CME Group

SHFE Premiums and the Renminbi Complication

SHFE copper introduces a currency dimension that the LME-COMEX arb does not carry. The effective USD equivalent of the SHFE price depends on the USD/CNY fix, the bonded warehouse VAT status of the underlying warrants, and whether the position is in domestic-registered or bonded-warehouse inventory. According to Shanghai Futures Exchange market data, the SHFE-LME arb window has historically opened during periods when Chinese smelter production outpaces domestic consumption, allowing import-parity pricing to diverge from LME parity by $150-200/MT during extended cycle lows.

Managing Tri-Exchange Basis Positions

Traders managing three-exchange basis books typically assign a functional currency to each leg, then mark the combined basis in a single reporting currency; usually USD. The SHFE leg requires a daily USD/CNY conversion at either the PBOC fix or the offshore CNH rate, depending on the trader's hedging instrument. The two rates diverge by up to 0.5% during periods of capital flow stress. On a 1,000MT copper position, that represents a meaningful P&L variance that belongs in the currency hedge book, not in the metal basis calculation.

The bonded-versus-domestic distinction on SHFE affects basis calculations at the full VAT rate. Bonded warehouse copper has cleared customs but VAT has not been paid. It prices at approximately LME parity plus a small China location premium. Domestic warehouse copper is VAT-paid and typically prices 13% above bonded copper on the SHFE curve. Traders mixing warrant types in the same SHFE position without tagging the VAT status will mismark their basis exposure by the full VAT differential until physical delivery forces reconciliation.

MCX copper in India adds a fourth dimension for traders active in South Asian physical markets. MCX's 1MT lots and INR denomination mean that a position large enough to affect a physical book (500 lots for 500MT) requires tracking the USD/INR rate alongside the MCX-LME differential, which incorporates Indian import duties currently at 2.5% plus GST of 18% on the assessable value. The MCX-LME spread trades as a proxy for Indian import demand, and its divergence from the COMEX-LME spread during monsoon season construction slowdowns is a recognized seasonal pattern that physical traders in the Indian subcontinent use for timing.

SHFE copper contract specifications

MCX copper contract specifications

Physical Delivery Reconciliation: Where Basis Becomes Real

Physical delivery reconciliation is the process of matching warrant-level copper inventory to contractual delivery obligations, verifying brand and shape specifications against the counterparty's contractual requirements, and confirming warehouse location against the delivery terms of the underlying physical trade. It is where basis errors that were accounting problems become operational problems with real financial consequences.

Sources of Physical Delivery Reconciliation Disputes

Delivery reconciliation disputes in copper typically arise from three sources: brand mismatches, location mismatches, and weight discrepancies. The LME maintains a registered brands list LME registered brands copper that specifies acceptable shapes and minimum purity levels. A buyer expecting cathodes under a specific producer brand (Aurubis, Codelco, Freeport-McMoRan) can reject delivery of an off-brand that technically meets Grade A specification but falls outside the agreed contract terms. The dispute does not appear until delivery notice is filed, at which point redelivery timelines create additional cost.

Location disputes are more operationally damaging than brand disputes. A delivery obligation specifying Rotterdam warrants cannot be fulfilled with Baltimore warrants without a freight adjustment negotiated in advance. Traders who manage physical commitments in the same system as their financial hedge positions can identify location mismatches before first delivery notice. Traders managing them in separate systems (physical in one spreadsheet, financial in the CTRM) typically discover mismatches the morning of delivery, after the market has moved.

Weight discrepancy reconciliation requires comparing warrant weights against original trade quantities, accounting for the LME's permissible tolerance band. Each LME copper lot can vary between 23.5MT and 26.5MT from the standard 25MT lot. On a 100-lot delivery, the weight tolerance across the full parcel can span 50MT; enough to create significant mark-to-market variance against a fixed-quantity physical sale contract that priced at a specific metric tonne total.

Why Real-Time Position Visibility Defines Cross-Exchange Basis Management

According to a 2023 survey by the International Swaps and Derivatives Association ISDA operational risk survey commodity, 67% of commodity trading firms reported that position data latency (the gap between trade execution and position reflection in the risk system) was their primary source of intraday risk management failure. In cross-exchange basis trading, that latency creates the precise window in which an unmonitored basis move turns a hedged position into an open one.

The Physical Delivery Reconciliation Process

Physical delivery reconciliation in copper trading is the process of matching exchange-registered warrants to physical trade obligations, verifying metal specifications against contract terms, and clearing any discrepancies before the delivery date. A complete reconciliation cycle for a 100-lot LME delivery covers warrant cancellation timing, brand and shape verification against counterparty requirements, and warehouse release coordination, typically a 48-72 hour operational window from cancellation to physical pickup.

LME warrant cancellation data functions as a leading indicator of delivery pressure in specific warehouse locations. When cancellations in Johor spike, a pattern seen repeatedly during periods of Asian end-user restocking, traders with real-time warrant visibility can reposition before the resulting premium impact reaches their physical book. Johor cancellation cycles have moved Asian copper premiums by $80-120/MT within two-week windows in recent inventory cycles. Traders relying on morning reports published 12 hours after the warrant data generates are responding to completed moves, not managing live exposure.

The COMEX equivalent requires monitoring two separate data feeds: the CME Group daily warrant report and the COMEX daily delivery notice. A trader who is short COMEX copper and holds registered warehouse receipts needs to match delivery intent against specific warehouse locations before the exchange assigns them automatically. The assignment process follows exchange rules that are not optimized for short-side traders who are passive, which means passive short traders absorb the least favorable available location assignments.

CME Group COMEX copper daily delivery notices

Cross-Exchange Basis Management Workflow: From Trade Capture to Close

A cross-exchange basis management workflow starts at trade capture. Each leg of a basis trade (LME-COMEX arb, LME-SHFE spread, or physical-versus-financial EFP) must be captured with the correct exchange, prompt date or contract month, lot size, and currency. A trade captured as a generic copper purchase without the exchange designation cannot be marked against the correct benchmark curve, and the basis calculation that follows will be incorrect from inception.

Daily workflow for a three-exchange basis book follows a time-zone sequence:

- LME ring close (13:00 London): Lock official prices for LME cash and three-month. Run prompt-date P&L against the LME Official and LME Closing Price. Identify any prompt dates requiring tom-next rolls.

- COMEX close (17:00 New York): Capture COMEX settlement. Convert to USD/MT at the 22.0462 multiplier. Calculate LME-COMEX basis delta versus opening marks. Flag any first notice day obligations filed during the session.

- SHFE close (15:00 Shanghai, captured following London morning): Capture SHFE settlement. Convert via USD/CNY close; CNH for offshore-hedged legs. Reconcile bonded and domestic warrant P&L as separate line items.

- Physical position reconciliation: Match any warrant cancellations or delivery intentions filed that day against open physical commitments. Update the delivery calendar for the forward 72-hour window.

Building a Basis Book That Performs Under Market Stress

The March 2022 LME nickel suspension LME nickel suspension March 2022 demonstrated that exchange-level risk (a venue simply halting trade) can strand basis positions in a way no VaR model anticipates. Traders holding LME short positions against COMEX longs had no mechanism to close the LME leg during the suspension. The LME-COMEX nickel basis reached levels that were operationally unmanageable, and the lesson transferred directly to how copper basis books are stress-tested today.

Copper's equivalent stress scenario is a simultaneous inventory squeeze across multiple warehouse locations. During the Q1 2024 period when LME copper stocks fell below 80,000 tonnes; their lowest level since 2005, according to LME inventory data; the cash-three-month spread moved into backwardation exceeding $100/MT. Traders who had modeled their basis book assuming a contango carry structure discovered that their rolling cost had inverted from a credit to a debit, compressing the effective hedge return on physical positions that were priced months earlier.

A basis book built for stress conditions requires three structural elements:

- Location-specific inventory tracking: Know which LME warehouse locations hold your cancelled warrants before a cancellation spike creates queue premiums in that location. Rotterdam and Johor have historically moved at different premium rates during the same cancellation event; holding position at the aggregate warrant level misses this.

- Currency hedge coverage at each exchange leg independently: SHFE and MCX legs carry currency exposure that the metal hedge does not cover. The USD/CNY basis can widen independently of the copper metal basis, and both move simultaneously during Chinese macro stress events.

- Delivery calendar integration with financial prompt dates: A basis position expiring on the March LME prompt date with physical delivery obligations three weeks later represents two separate risk events with different market exposures in the interim period.

The Standard This Work Demands

Cross-exchange basis management in physical metals trading rewards operational precision and punishes approximation at the worst possible moments; when basis moves fastest, when delivery deadlines are imminent, and when the market provides the least time for reconciliation. The LME-COMEX spread mechanics, the SHFE bonded-versus-domestic distinction, and physical delivery reconciliation requirements are not complexities to be managed later. They are the structural core of the position from the moment the first leg is executed.

Traders who manage this well share three consistent practices: they capture trade-level detail at the point of execution without deferring exchange and currency tagging to end-of-day, they mark basis positions separately from flat-price positions so each risk type is visible independently, and they maintain a live delivery calendar that connects financial prompt dates to physical logistics with a 72-hour forward horizon.

Immediate operational steps:

- Audit your current position system's handling of LME prompt dates versus COMEX monthly expiries. If the system does not distinguish between them at the position level, your basis marks are approximations, and the error compounds as the delivery date approaches.

- Map your SHFE warrant inventory by bonded versus domestic status as a standing daily procedure. The VAT differential is a real and recurring P&L line, not a footnote to be resolved at settlement.

- Build a delivery reconciliation checklist that initiates 72 hours before first notice day rather than 24 hours. The LME warrant cancellation window requires it, and the time between cancellation and warehouse release is not recoverable once a location mismatch is discovered inside it.