Zinc Rollover Costs: What Front-Month Price Hides

The single zinc price your platform displays is not your cost basis. It is the cost of owning zinc at one specific prompt date, under one specific market condition, for one specific lot. The moment you add a second prompt date, or a third, fourth, or fifth, you are no longer trading a price. You are trading a compounding cost structure that requires explicit forward curve modeling to accurately represent.

This analysis traces exactly how zinc rollover costs accumulate across a multi-month physical position, quantifying each prompt date's contribution to the total cost basis.

The Front-Month Illusion in Zinc Trading

Open almost any trading platform or commodity data feed and one zinc price is prominently displayed: the LME three-month or nearby prompt.

On a representative day in mid-2025, that number might read $2,850 per metric tonne. While clean and real-time, it is materially incomplete for any trader managing a position that extends beyond a single prompt date.

According to the London Metal Exchange, zinc is consistently among the top three most actively traded base metals on the exchange, with daily traded volumes regularly exceeding 200,000 lots LME market data. That liquidity is real, but it is concentrated at the front of the curve. The further out you go, the thinner the market, the wider the carry, and the larger the implicit cost of maintaining or rolling a position.

The front-month price captures none of that. It is a snapshot of value at one moment in time, not a statement about what it actually costs to hold or hedge zinc across multiple months.

Components of a zinc rollover cost on the LME

A zinc rollover cost on the LME comprises three distinct components: the bid-offer spread paid at each roll date, the carry cost between the near and far leg (contango or backwardation), and the financing cost on the notional position value across the holding period. Each component is real, each is quantifiable, and none of them appears in the front-month quote your platform displays.

Together, these three costs form the true cost structure of a multi-month zinc position, and their interaction is precisely what full-curve position management must model.

Zinc Rollover Costs Begin Before the First Roll

Before a single prompt date moves, a trader pricing a multi-month zinc book has already accepted a structural disadvantage: the market they will need to access at each future roll date is not the market they are pricing against today.

LME zinc quotes at the three-month date reflect the cost of borrowing and carrying metal for 91 days. Beyond that, the curve prices in additional carry (storage costs, financing, and risk premium) at each successive monthly prompt. According to Metal Bulletin Metal Bulletin zinc market reports, zinc has spent the majority of the past five years in contango, meaning forward prices consistently exceed spot prices.

That contango is not a fixed number. It steepens and flattens with LME zinc inventory levels, prevailing interest rates, and warehouse queue dynamics. At mid-2025 curve levels, the zinc forward curve shows approximately $5.50 per metric tonne of monthly carry in the near portion, widening to approximately $8.10 per metric tonne in the six-to-eight month range, where the curve compensates for progressively lower liquidity and higher financing duration.

For a physical trader pricing a 12-month supply agreement, or a smelter hedging forward production, that widening carry is a compounding liability. It is a cash cost at every roll date rather than a theoretical variable.

The impact of contango on zinc hedging costs

In a contango market, forward prices are higher than spot prices. When a hedger rolls a short zinc position forward (selling the nearby date and buying the next prompt), they pay the spread between those two prices. That spread is the contango carry, and it represents a real cash outflow at every roll date. In a persistently contango zinc market, these carry costs accumulate with each successive roll, building a total cost basis that consistently exceeds the front-month price used to value the original position.

The longer the holding period and the wider the contango, the larger the cumulative drag on the hedge's realized price.

How Each Zinc Rollover Cost Builds Across Prompt Dates

Consider a 1,000 metric tonne zinc short hedge held across five consecutive monthly prompt dates, with a starting three-month reference price of $2,850 per metric tonne.

A platform displaying only the front-month reference shows one number: $2,850/mt.

The full curve shows something structurally different. At each roll, the position incurs three measurable, documented costs:

- Bid-offer spread: On LME zinc, a conservative market estimate for spread cost at each roll is $1.50/mt, or $1,500 on a 1,000 mt position LME zinc bid-offer spread data.

- Monthly carry (contango): Based on mid-2025 zinc curve structure, carry costs escalate progressively along the forward curve.

- Financing cost: At approximately 5.25% annualized (reflecting prevailing short-term secured lending rates) on a notional position value of $2,850,000, monthly financing adds $1,248 per roll period.

Building the cost stack prompt by prompt:

Roll 1: 3-Month to 4-Month Prompt

- Bid-offer spread: $1.50/mt -> $1,500

- Monthly carry: $5.50/mt -> $5,500

- Financing cost: $1,248

- Roll 1 cost: $8,248 | Cumulative total: $8,248 | Per metric tonne: $8.25

Roll 2: 4-Month to 5-Month Prompt

- Bid-offer spread: $1.50/mt -> $1,500

- Monthly carry: $6.20/mt -> $6,200

- Financing cost: $1,248

- Roll 2 cost: $8,948 | Cumulative total: $17,196 | Per metric tonne: $17.20

Roll 3: 5-Month to 6-Month Prompt

- Bid-offer spread: $1.50/mt -> $1,500

- Monthly carry: $6.80/mt -> $6,800

- Financing cost: $1,248

- Roll 3 cost: $9,548 | Cumulative total: $26,744 | Per metric tonne: $26.74

Roll 4: 6-Month to 7-Month Prompt

- Bid-offer spread: $1.50/mt -> $1,500

- Monthly carry: $7.40/mt -> $7,400

- Financing cost: $1,248

- Roll 4 cost: $10,148 | Cumulative total: $36,892 | Per metric tonne: $36.89

Roll 5: 7-Month to 8-Month Prompt

- Bid-offer spread: $1.50/mt -> $1,500

- Monthly carry: $8.10/mt -> $8,100

- Financing cost: $1,248

- Roll 5 cost: $10,848 | Cumulative total: $47,740 | Per metric tonne: $47.74

Accumulation of prompt date spread costs

Across five monthly rolls on a 1,000 mt LME zinc position at mid-2025 curve levels, the combined cost of bid-offer spreads, carry, and financing totals $47,740, or $47.74 per metric tonne. Each roll is progressively more expensive. Roll 1 costs $8,248 while Roll 5 costs $10,848, marking a 31.5% increase between the first and final roll. This compounding accelerates as the carry structure widens further out the curve.

A trader relying solely on the front-month price sees none of this cost accumulation.

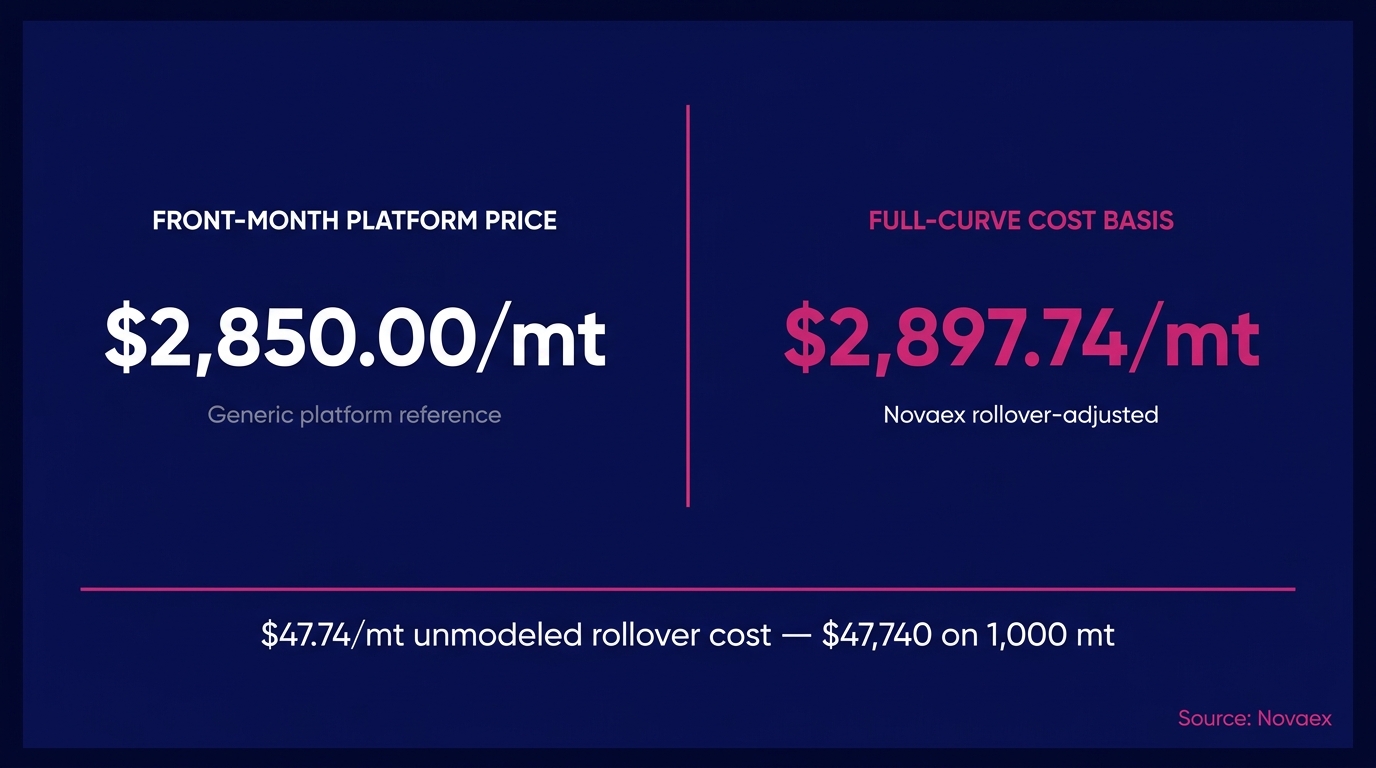

The Full-Curve Zinc Price: What the Number Actually Is

The front-month price of $2,850/mt simply describes what zinc costs to buy at the three-month prompt today.

Meanwhile, the full-curve cost basis reveals what it costs to maintain, roll, and settle a zinc position across the duration of a physical book. After five prompt date rolls on the position analyzed above, the effective cost basis is:

$2,850.00 + $47.74 = $2,897.74 per metric tonne

That is a 1.68% gap between what a single-price platform tells you and what it actually costs to run this position. On 1,000 mt, the cumulative cost differential totals $47,740, and that figure is before any adverse directional market move.

[LINK: commodity cost basis calculation methodology]

The limitations of the three-month LME zinc price

The three-month LME zinc price is a reference price, not a cost basis. It reflects the market's assessment of zinc value at a specific forward date, but it does not account for the cumulative cost of rolling, carrying, and financing a position across multiple prompt dates. Using it as the foundation for a multi-month hedge or supply contract systematically undercounts true exposure. This produces pricing variances that remain unquantified until settlement, at which point they are fully realized in cash P&L.

According to a 2023 survey by the International Commodity Management Network ICMN survey data, approximately 61% of mid-market commodity traders reported that their primary valuation tool did not adequately capture forward cost structures in base metals, leading to systematic pricing gaps in physical contract agreements.

The Zinc Rollover Cost Gap Becomes a Business Consequence

A $47,740 cost differential on a 1,000 mt zinc position is a direct business consequence, traceable to specific outcomes in two common physical zinc market scenarios.

Scenario 1: Physical Sourcing Agreement

A procurement team prices a 1,000 mt zinc supply contract for a downstream manufacturer using the front-month price of $2,850/mt as its cost reference. The offer price is set with a 3.0% margin. The true rollover-adjusted cost basis is $2,897.74/mt. Before a single tonne ships, the margin contracts from 3.0% to approximately 1.3%, assuming no adverse directional price move during the contract period.

Scenario 2: Smelter Production Hedge

A zinc smelter hedges five months of forward production at $2,850/mt, using the front-month price as its hedge reference. Over the five-month period, the actual rollover costs consume $47.74/mt in carry, spread, and financing. The effective realized price drops to approximately $2,802/mt, which is 1.7% below the intended hedge level and potentially below breakeven depending on the smelter's production cost structure.

zinc smelter hedging strategy frameworks

Both scenarios share a root cause: the cost basis used to make the decision was incomplete. The trader pricing a contract at $2,850/mt made an error in data rather than an error in judgment.

Consequences of pricing off the wrong prompt

When a zinc hedge uses the wrong prompt date as its reference, the hedger accepts basis risk they have not quantified or priced into their position. At settlement, if the physical delivery price is determined by a prompt date different from the hedge date, the mismatch in the rollover cost structure creates a cash P&L variance. Over a multi-month book, these variances accumulate. This typically happens in one direction because contango systematically disadvantages the rolled short hedger across every successive prompt.

LME risk management guidance LME hedging guide identifies basis risk (including prompt date mismatch) as the most commonly underestimated risk factor in physical base metals hedging programs.

Full-Curve Zinc Visibility Changes the Hedge Decision

The difference between a platform displaying $2,850/mt and one showing a full-curve cost basis of $2,897.74/mt fundamentally alters the decision-making process.

A trader with full-curve zinc visibility operates differently across four critical workflows:

- Supply contract pricing: Incorporates actual rollover costs into the bid structure, preserving the intended margin rather than surrendering it to unmodeled carry.

- Hedge tenor selection: Compares the all-in cost of a five-month rolled hedge against a single long-date position, choosing the structure that minimizes total cost rather than minimizing upfront complexity.

- Prompt date optimization: Identifies which roll dates carry the widest spread and adjusts the roll schedule forward or backward to reduce carry exposure.

- P&L attribution: Accurately separates market directional moves from structural roll costs in position P&L, enabling precise evaluation of hedge performance.

None of these decisions are possible when position management relies on a single front-month reference price as the basis for a multi-month zinc position.

Novaex zinc full-curve pricing and position management

According to a 2024 analysis by a leading commodity analytics research group commodity analytics benchmarking report, firms with full forward curve visibility in base metals reduced unplanned hedge cost variances by an average of 38% compared to firms relying on spot or near-prompt pricing alone. This reduction stems from applying better information at the exact moment the decision is made.

Comprehensive forward curve coverage means the carry structure at every prompt date is modeled, the financing cost at every roll is calculated, and the spread cost at every transition is visible before the trade is executed rather than discovered afterward during settlement.

The $47,740 Is the Starting Point, Not the Ceiling

The metric built across this analysis ($47,740 in cumulative zinc rollover costs on 1,000 mt over five prompt dates) is based on mid-2025 contango levels and conservative spread estimates. In periods of steeper contango or wider bid-offer spreads, the number is larger. In a multi-year supply contract or a larger physical book, it scales proportionally.

That $47,740 is the precise figure separating a platform that shows one zinc price from a platform that models the full zinc cost structure. It is the difference between the contract you think you priced and the contract you actually signed.

Three actions for traders managing multi-month zinc positions today:

- Map your prompt date structure now: For every open zinc position, identify the roll dates and calculate the contango cost at each transition. Do not accept the three-month price as a proxy for a multi-month cost basis.

- Recalculate your forward pricing commitments: Apply the full-curve cost basis to any zinc supply contract currently in negotiation or recently executed. If the number changes materially, the pricing assumption needs to be corrected before the position is committed.

- Require full-curve visibility from your platform: If your current system cannot display per-roll cost contributions across your zinc book (carry, spread, and financing itemized at each prompt date), you are managing a multi-month position on single-date information.

Novaex platform demonstration request

Relying on the front-month price carries a significant hidden cost. On a 1,000 mt zinc book across five prompt dates, that cost is $47,740. Now you know exactly where every dollar of it originates.