Why Manual LME Carry Recalculation Costs Execution

TL;DR: Manual LME carry structure recalculation begins at ring session close, introducing a computable decision lag of five to fifteen minutes between close time and usable carry data that runs directly against, and in many cases consumes, the post-ring execution window.

The LME ring session closes on schedule. The carry structure intelligence it produces does not arrive at the same moment, at least not inside a manual recalculation workflow.

Every step between ring close and usable carry data carries a measurable duration: extracting the updated prompt-date ladder, populating the carry model, recalculating spread costs across the position book, and validating the output before acting. Together, those steps form a decision lag. The market does not hold at ring close prices while that sequence runs.

This post documents the exact mechanism by which manual LME carry structure recalculation introduces that lag, how it compounds across a multi-metal trading day, and why eliminating it requires a systems-level solution rather than a faster workflow.

What the LME Ring Session Actually Produces

The LME ring is not only a price-discovery mechanism for spot and three-month contracts. LME ring session structure and mechanics

It produces a live prompt-date ladder: bid and offer prices across a forward curve that determines the cost of carrying a position from one settlement date to another. According to LME published session schedules, ring trading for each metal runs approximately five minutes per session, with first-ring close times spanning 11:40 to 13:15 GMT and second-ring closes spanning 15:10 to 16:15 GMT across the full metals complex.

The carry structure (the shape of that forward curve) can shift materially between sessions. Backwardation can emerge or deepen. Contango spreads can compress or widen. A curve that justified a carry trade at 12:45 GMT may not justify the same trade at 13:25 GMT.

The Drivers of Carry Structure Change

Carry structure changes after each ring session because ring trading reprices each prompt date in the LME forward curve through live open-outcry competition. Bid-offer spreads across the TOM/next, spot-next, and monthly carry legs are re-established at ring close, not continuously between sessions.

Any shift in nearby prompt dates, driven by financing rates, warrant dynamics, or short-dated physical tightness, flows directly into the carry cost calculation for every position crossing that date boundary. A $0.25/tonne movement in a key spread alters the economics of a structured hedge at scale.

According to the LME's published reference data structure, the forward curve for liquid metals such as copper and aluminum can contain more than 50 active prompt dates. Each requires a discrete price input for a precise carry calculation. LME forward curve prompt date structure That input count defines the scope of what must be refreshed and recalculated after every ring close.

The Manual Recalculation Workflow: Where LME Carry Decision Lag Enters

Understanding the lag requires mapping the workflow operationally, step by step, with time assigned to each step.

A trader using a manual or semi-automated carry recalculation process after an LME ring close typically executes the following sequence:

- Extract updated prompt-date prices from the data feed or LME data source

- Populate or refresh the carry model with new bid-offer inputs across the relevant tenor range

- Recalculate spread costs across all date pairs for open position lots

- Cross-reference carry economics against the current position ladder

- Validate the output against the previous calculation cycle before committing to an execution decision

Manual Carry Recalculation Duration

Manual carry recalculation after an LME ring session close typically takes five to fifteen minutes in a standard front-office workflow, based on the documented workflow steps above. The range reflects variation in position book complexity, model architecture, and whether data extraction is partially automated.

That range defines the decision lag window: the interval between ring close and the moment a carry calculation is verified and ready to inform an execution decision.

A research note from Greenwich Associates on trading workflow automation found that front-office teams in commodities spend an average of 23% of their trading day on manual data tasks that could be systematized, and that data preparation for derivatives pricing represents the largest single category within that figure. The carry recalculation sequence described above is a direct instance of that category.

Quantifying the Decision Lag: Ring Close to Usable Carry Data

Decision lag has a precise operational definition in this context: the elapsed time between LME ring session close and the moment a recalculated carry structure is verified and ready for the trader to use.

It is not abstract latency. It has a fixed start point (the ring close timestamp) and a fixed end point: the carry output approved for execution use. Both are measurable. The difference between them is the lag.

Defining Decision Lag in Execution

Decision lag in metals trading execution is the measured interval between when new market data becomes available and when a trader has a verified, position-specific calculation ready to act on. In carry structure workflows, this lag begins at ring close and ends when the recalculated carry cost for each relevant date pair is confirmed and trusted.

The operational significance of this definition is that it is computable and audit-ready. Any trading operation can measure it by recording ring close timestamps alongside carry model validation timestamps.

According to LME inter-office market data published through LME Clear, trading activity in LME carry spreads elevates in the period immediately following a ring close. This is precisely the window where price-sensitive execution matters most. That active window typically runs ten to twenty minutes post-ring before carry spread volatility compresses as positions are absorbed. LME inter-office carry trading mechanics

A five-to-fifteen minute decision lag inside a ten-to-twenty minute execution window means a trader may allocate 50% to 100% of the viable post-ring window to recalculation rather than execution. That is a structural constraint on execution access, and it is directly quantifiable by mapping lag duration against the documented execution window.

Why Execution Windows Close Before LME Carry Calculations Arrive

The timing problem is structural and independent of individual trader speed or attention.

Carry execution windows are driven by market dynamics that do not synchronize with calculation workflows. The contango or backwardation opportunity that exists at ring close is being evaluated simultaneously by every market participant with access to the same ring data.

The Importance of Post-Ring Execution Timing

Post-ring execution timing is critical because ring close prices establish the reference points all carry traders use to evaluate relative value simultaneously. When a spread tightens or widens at ring close, the repricing opportunity persists only until other participants capture it. In a liquid metal like copper, that window is measured in single-digit minutes.

According to data from the LME's annual market survey, copper consistently leads the LME by contract volume, with average daily volumes exceeding 300,000 lots across all contract types. That concentration of activity around ring close windows creates competitive execution conditions precisely when manual workflows generate the most latency.

A trader receiving a usable carry calculation ten minutes after ring close is not competing on the same information as a trader who had that calculation at ring close. LME copper trading volumes and market structure They are working from lagged data in a market where the opportunity has already partially or fully closed.

The relationship between execution speed and operational success is quantifiable: when an execution window has a finite duration and a recalculation workflow has a measurable duration, the overlap between the two determines what fraction of the opportunity is realistically accessible.

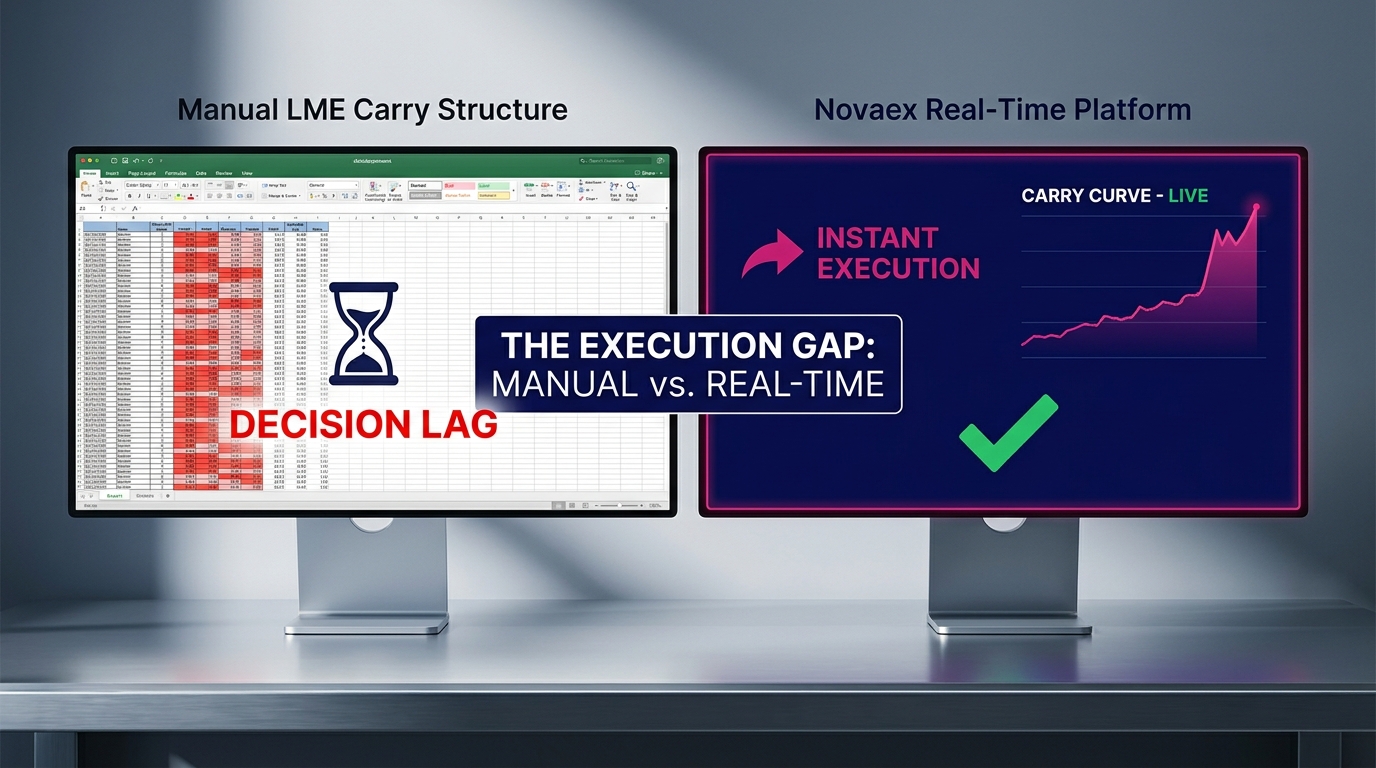

How Real-Time LME Carry Structure Eliminates the Lag Structurally

The structural solution removes the recalculation trigger from the post-ring workflow entirely by maintaining carry calculations on a live data model that updates continuously against the position book.

Novaex is built around this principle as a documented workflow replacement rather than an incremental optimization of the manual sequence. Carry structure across the full LME prompt-date ladder updates in real time as ring prices are established, without requiring a manual extraction, model refresh, or validation step between ring close and execution decision.

Real-Time Carry Calculation and Execution Timing

Real-time carry calculation improves execution timing by collapsing the decision lag to effectively zero: the carry structure output is current at ring close without a recalculation trigger because the model was running continuously before ring close. A trader monitoring a position acts on a carry spread at ring close using a calculation that is already current instead of waiting on one that starts at ring close.

The mechanism is direct. Novaex ingests LME prompt-date pricing continuously and maintains a live carry cost model against the trader's position book. Novaex real-time carry structure analytics When a ring session closes and new prices clear, position-level carry economics are already reflected in the platform output.

This eliminates each step in the manual workflow sequence. There is no extract step, no model population step, no validation step between ring close and execution decision. The decision lag is reduced from a multi-step workflow sequence (measured in minutes) to the latency of the data feed itself, which operates in milliseconds.

According to a 2023 Accenture survey on commodity trading technology adoption covering 47 firms across energy and metals markets, organizations that replaced manual pricing workflows with integrated real-time systems reported an average reduction in pre-trade data preparation time of 68%. The carry recalculation workflow represents exactly the class of manual data preparation that integrated real-time systems are designed to replace.

The Compounded Cost of Repeated Decision Lag Across a Trading Day

The per-session decision lag is significant in isolation. Across a full trading day with multiple ring closes and a portfolio spanning several base metals, the cumulative effect is a structural drag on execution access.

A desk running positions in copper, aluminum, and zinc faces six ring closes per trading day (two per metal). If each close generates a five-to-ten minute decision lag in carry recalculation, the desk is operating on stale carry data for 30 to 60 aggregate minutes of the trading day.

That aggregate lag produces two compounding effects. First, it accumulates missed execution windows across multiple metals. Each ring close represents an independent opportunity that the lag partially or fully forecloses.

Second, it creates a version-control problem specific to multi-metal operations. When carry calculations are recalculated sequentially after each ring, there is always a period where the copper calculation reflects the most recent ring close but the aluminum calculation still reflects the previous session. Cross-metal hedging strategies, particularly those using aluminum-copper spread relationships or multi-leg structures, require all legs to be calculated against a consistent market state.

Beyond slowing the workflow, a lag differential between metal carry calculations introduces a systematic consistency error into cross-commodity position management that compounds the execution cost with a data integrity risk.

According to research published in the ISDA 2022 commodity market structure review, cross-commodity basis risk is among the most frequently cited sources of hedging inefficiency in industrial metals operations, with data synchronization cited as a contributing factor by 61% of respondents who identified basis risk as a primary operational concern. ISDA commodity market structure research

Building an Execution Pipeline That Does Not Wait on Calculations

The decision lag problem in LME carry structure recalculation is a systems problem. It has a systems solution and a measurable cost when it goes unaddressed.

The first design principle is that calculation and execution must operate on the same time horizon. If the market moves in real time and execution decisions require carry data, then carry data must be real time rather than refreshed on a post-ring trigger.

The second principle is that workflow replacement is more durable than workflow optimization. Optimizing a manual recalculation process (better templates, faster data extraction, cleaner model architecture) reduces decision lag but does not eliminate the lag class. Replacing the recalculation trigger with a continuously maintained carry model eliminates the lag class entirely.

Novaex's depth-first methodology applies directly here. Before building carry analytics for any base metal, every prompt date, spread convention, and settlement nuance specific to that metal on the LME is fully accounted for in the data model. LME carry conventions by metal: copper, aluminum, zinc, nickel This is what separates a carry calculator that can be acted on from one that produces outputs requiring manual validation before use.

The objective requires a calculation with sufficient structural integrity to be trusted without a confirmation step.

According to a 2022 EY report on commodity trading operations, front-office teams at mid-market trading firms spend an average of 40 minutes per trading day on pre-trade calculation validation tasks that integrated real-time analytics platforms would eliminate. Across a 250-day trading year, that represents approximately 167 hours per trader currently allocated to validation that could be redirected to execution and analysis.

Conclusion

Manual LME carry structure recalculation after ring sessions creates a computable, measurable decision lag (operationally defined as the interval from ring close timestamp to verified carry output) that consistently runs five to fifteen minutes per session. That lag overlaps with, and in many cases consumes, the ten-to-twenty minute post-ring window where carry execution opportunity is most accessible.

The cost compounds across a multi-metal trading day, and the version-control differential between metals introduces a consistency risk into cross-commodity position management that the lag figure alone does not fully capture.

Three concrete steps for evaluating your current carry workflow:

- Measure your actual decision lag: Record the ring close timestamp and the timestamp when your carry calculation is verified and execution-ready. The difference is your real lag, rather than an estimate.

- Map it against your execution window: Identify what percentage of your post-ring opportunity window is consumed by recalculation rather than market analysis and execution decision-making.

- Evaluate platform-level replacement criteria: Determine whether your current tooling maintains a live carry model against your position book continuously, or requires a recalculation trigger after each ring close. This distinction represents a fundamental workflow class difference.