Single Book of Record: Real-Time Position Visibility

When a metals trader enters a new physical position, three teams need the same number at the same moment. A single book of record delivers exactly that: one reconciled exposure figure that updates simultaneously for trading, risk, and finance the instant a position is entered, with zero reconciliation lag.

While that is the definition, existing infrastructure rarely delivers it. The operational gap between the two represents measurable, quantifiable risk exposure for most mid-market metals trading operations.

We outline the mechanics below: what the single book of record looks like in live conditions, what it demands architecturally, and why the metals market specifically makes simultaneity non-negotiable.

What "Single Book of Record" Actually Means in Metals Trading

The term appears frequently in vendor documentation and platform discussions. Its operational meaning varies considerably depending on the context in which it is used.

In practice, a single book of record for a metals trading operation means one authoritative source for every open position, committed tonnage, and associated price exposure. It replaces disconnected systems that sync overnight and master spreadsheets updated after end-of-day. Instead, teams consult one live ledger, updated exclusively through the act of entering a position.

According to a 2023 report by Commodity Technology Advisory (ComTech), approximately 68% of commodity trading firms still operate with two or more position-keeping systems that require manual reconciliation at some point in the workflow. That figure is higher among mid-market physical metals traders, where legacy CTRM deployments routinely coexist with Excel-based workarounds built to compensate for their gaps.

Despite significant technology investment, most existing platforms lack the simultaneity requirement: the architectural standard that every team must access the same exposure figure at the same moment, derived from the same event.

Defining the single book of record

A single book of record is the infrastructure standard where one reconciled ledger holds every position, exposure, and transaction, updated in real time, and serves as the authoritative source for all downstream functions including trading decisions, risk limit monitoring, and financial reporting. It eliminates the condition where trading sees one exposure number and risk sees another.

The distinction from a "primary system" or a "consolidated view" is critical. A consolidated view aggregates from multiple sources. A single book of record has only one source. Aggregation introduces reconciliation risk at the aggregation step. A single source eliminates that step entirely.

The Mechanics of Simultaneous Update

This is where the concept holds operationally, or fails.

When a trader enters a new physical copper position (say, 250 metric tonnes of Grade A copper against an LME three-month forward), several facts become immediately true:

- The firm's net long or short on copper changes

- The mark-to-market exposure against that forward changes

- The P&L attribution for the position begins accruing

- The risk team's exposure report must reflect the new position

- The finance team's hedge designation register must log the trade

According to research by Accenture commodities operations benchmarking, firms operating fragmented position-keeping infrastructure spend an average of 4.2 hours per day on cross-system reconciliation tasks that serve no analytical purpose. They exist purely to compensate for architecture that cannot update simultaneously.

The mechanics of simultaneous updates

Simultaneous update works by treating the position ledger as a shared, event-driven data layer rather than a database owned by one department. When a position is entered, the ledger fires an event. Trading, risk, and finance each subscribe to that event and receive the updated exposure figure in real time, requiring no polling, no batch jobs, and no hand-off between systems.

The architectural requirement is that the entry point and the ledger are the same system. If a trade is entered into a trading system and must be exported to a separate risk system, simultaneity is already broken. A propagation delay has been introduced. It may be short. It is never zero.

The True Cost of Fragmented Books

The operational cost of fragmented books appears in specific, measurable workflows.

Scenario one: The morning risk call.

A risk manager opens her 7:00 AM exposure report. It reflects positions as of end-of-day yesterday. During the two hours it takes to update the numbers (pulling from the trading system and reconciling against the finance team's hedge register), the market has moved. The copper curve has shifted. The aluminum spread she was monitoring has widened. The exposure she is presenting is already stale before the call starts.

According to LME annual report, LME base metals markets see an average of $12 to 18 billion in notional value traded daily across copper, aluminum, zinc, nickel, lead, and tin. In a market of that size, a two-hour exposure lag constitutes a material risk management failure with a specific dollar cost.

Scenario two: The intraday hedge decision.

A trader needs to know her current net position before executing a hedge. In a fragmented-book environment, she either calls risk for a number (which may itself be outdated), queries the trading system (which does not reflect positions that came through procurement), or consults her own spreadsheet (which reflects what she entered, not what the desk entered collectively). None of those constitutes a single book of record. All are workarounds with documented failure modes.

The impact of disparate data sources

When teams use different data sources, they operate from different versions of the same underlying reality. Traders optimize against one exposure number, risk managers govern against another, and finance reports a third. According to KPMG financial controls and risk data integrity report, firms with fragmented risk data infrastructures are 3.1x more likely to experience material P&L restatements than firms operating unified position-keeping architectures. The root cause is almost always the same: a reconciliation failure between systems that were never designed to share a single truth.

The downstream effects compound. A risk limit breach that should be visible in real time goes undetected until the next reconciliation cycle. A hedge that should qualify for documentation under IAS 39 or ASC 815 fails effectiveness testing because the hedge register and the trading book were not synchronized at the time of designation. These are predictable outcomes of fragmented book architecture.

The Single Book in Live Conditions: A Concrete Illustration

Architecture claims are straightforward to make. The following illustration establishes precisely what the single book of record looks like in the moments following a physical position entry.

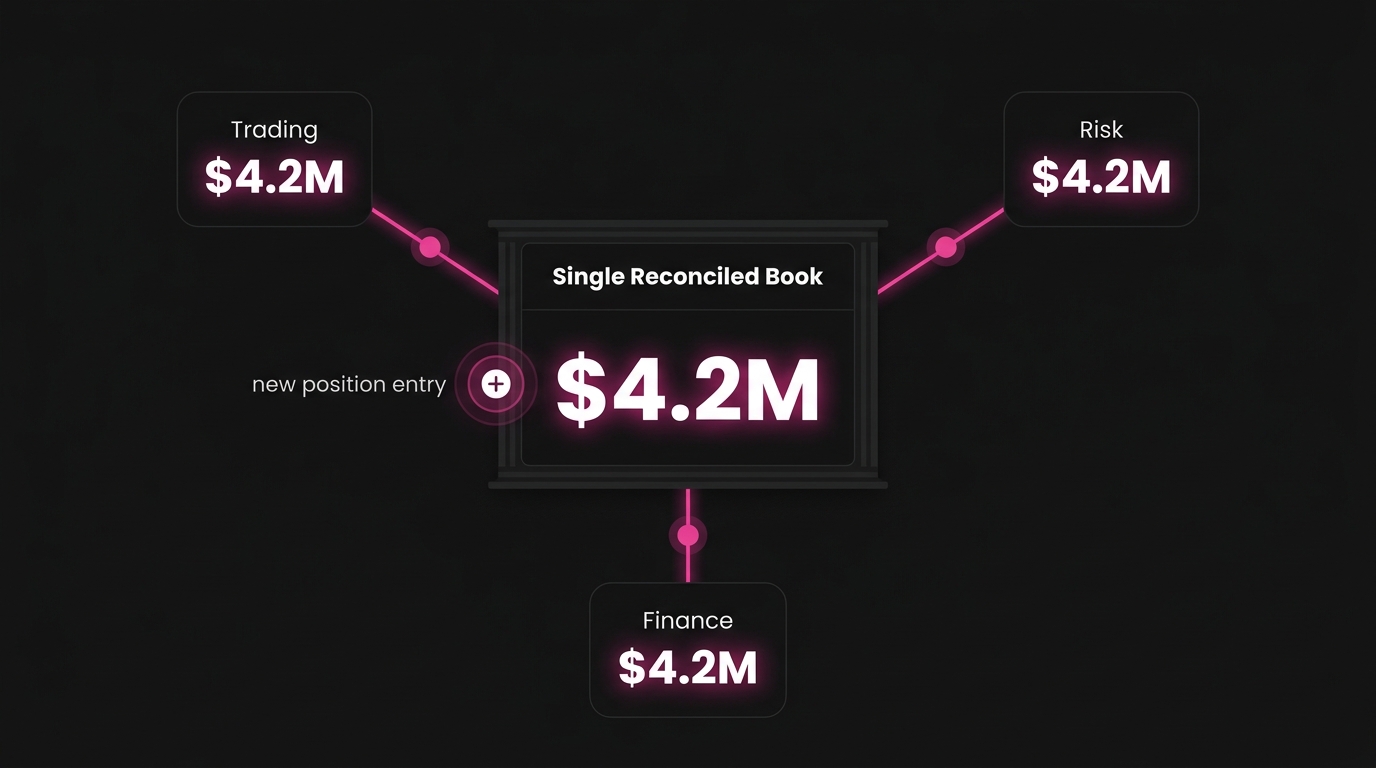

T=0:00: A physical aluminum position is entered.

A trader on the metals desk enters a purchase of 500 metric tonnes of primary aluminum, delivery in three months. The entry goes into the position ledger. The trade ticket captures: commodity, quantity, delivery date, counterparty, agreed price, and associated price risk basis.

T=0:00: Simultaneously, across three functions:

- Trading sees the desk's net long increase by 500 MT. The delta against the desk's current short hedge updates automatically. The trader can immediately assess whether the position is under- or over-hedged and can act on that information now.

- Risk sees the new position in the firm's total aluminum exposure. The mark-to-market runs against the updated position immediately. If the position pushes the desk above a pre-set exposure limit, the alert fires exactly at T=0:00.

- Finance sees the new position in the hedge designation register. The commitment is logged. Potential hedge documentation starts from the moment of trade entry, avoiding delays from manual file transfers.

This is the operational reality a single book of record delivers. The entry and the update are the same event. There is no window between them, and therefore no untracked risk exposure contained within that window.

According to a study by Oliver Wyman energy and commodities practice, real-time position visibility reduces intraday hedge slippage by an estimated 15 to 23% in active physical commodity operations. This is primarily because traders execute against current exposure rather than stale snapshots.

Why Metals Trading Specifically Demands Single-Book Architecture

Not all commodity markets make the simultaneity requirement equally urgent. Metals trading has structural characteristics that amplify the cost of every reconciliation window.

Multi-exchange exposure is the structural default.

A copper trader active on LME, COMEX, and SHFE simultaneously holds positions across three venues with different settlement conventions, margin requirements, and price references. The exposure aggregation problem is harder than in single-venue markets. A fragmented book that accommodates one exchange adequately encounters meaningful structural failures when three are in play.

According to CME Group base metals market data, copper futures open interest across LME, COMEX, and SHFE combined has averaged over 2 million contracts in recent periods, reflecting the genuinely global nature of base metals price discovery. A trader active across these venues cannot afford a book that reconciles by exchange rather than aggregating to a single net position in real time.

Physical and financial positions must net against each other.

A metals trader's true exposure represents the net of her physical commitments and financial hedges. Calculating that net correctly requires physical purchases, sales, warehouse receipts, forward contracts, and futures positions to all live in the same ledger, avoiding separate systems that approximate a consolidated view downstream.

Eliminating position reconciliation delays

A single reconciled book eliminates reconciliation delays by making reconciliation unnecessary. When there is only one ledger and all positions flow into it at the moment of entry, there is nothing to reconcile after the fact. The reconciliation work that currently consumes analyst hours daily is eliminated entirely, because the condition that creates the need for it no longer exists.

LME prompt date management adds another layer of complexity.

LME forward curves involve prompts for every business day up to three months, weekly dates to six months, and monthly dates to 63 months. Position management on LME requires accurate date-specific exposure tracking. When a physical delivery date shifts, the financial hedge must be rolled. That roll must update across trading, risk, and finance simultaneously, or the firm is managing a position that no team sees accurately for whatever window the propagation takes.

The necessity of simultaneous exposure updates

Metals traders need simultaneous exposure updates because physical and financial positions interact in real time, and the correct action for each team depends on the same current number. When a physical long increases, the hedge ratio changes immediately. The trader may need to add a hedge. Risk may need to flag a limit. Finance may need to log a designation. If any one of them is working from a delayed figure, their action is miscalibrated by exactly the magnitude of the delay.

What Single-Book Architecture Requires to Deliver

Describing "single book of record" as a design principle requires no effort. Building infrastructure that actually honors simultaneity requires specific, clearly defined architectural choices.

Entry and record must be the same act.

If entering a trade in the trading interface requires a separate step to push it to the position ledger, simultaneity fails at the first opportunity. The entry interface must write directly to the single ledger. There can be no export, no sync, and no batch transfer between the entry point and the book.

All position types must share one data model.

Physical purchases and sales, exchange-traded futures, OTC forwards, options, and warehouse receipts must all resolve to the same position representation in the ledger. If physical and financial positions live in separate data models that are aggregated downstream, the aggregation step reintroduces exactly the reconciliation risk the single-book architecture was designed to eliminate.

According to Gartner data management and analytics research, organizations operating unified data models for operational and financial data reduce data quality incidents by an average of 47% compared to organizations managing parallel data stores. In metals trading, data quality incidents manifest as position miscalculations with direct P&L consequences.

Risk calculations must run against live position data.

The risk engine (whether it calculates mark-to-market, value-at-risk, or hedge effectiveness) must query the live ledger, rather than a snapshot taken at a fixed interval. Snapshot-based risk calculation is the precise technical reason why risk reports lag reality, even in organizations that believe they have achieved real-time visibility. The snapshot interval, however short, is a reconciliation window.

The Standard: Depth Before Breadth

The industry has described single book of record as a goal for more than a decade. The reason it has remained a goal for most mid-market metals traders is that platforms serving this segment were built to cover multiple commodities broadly, rather than any single commodity with sufficient depth to honor the simultaneity requirement.

A platform built to handle metals, energy, agriculture, and softs simultaneously makes architectural compromises. The data models must be generic enough to accommodate the structural differences between these markets. Generic data models produce approximate position representations. Approximate representations require reconciliation. Reconciliation introduces windows. Windows carry risk.

A depth-first architecture makes a different trade-off.

Rather than compromising the data model to achieve breadth, a depth-first platform builds the data model that accurately represents one commodity (in this case, base metals) and refuses to generalize until that model is proven complete. For metals, that means:

- LME prompt date granularity built into the core position model, rather than bolted on.

- Physical and financial positions netting in the same ledger by design, avoiding post-trade aggregation.

- Multi-exchange aggregation across LME, COMEX, MCX, and SHFE without approximation.

- Exposure figures that update at entry, because entry and update are the same event.

The single book of record serves as the minimum viable infrastructure for a trading operation making decisions in real time.

Conclusion: The Moment of Entry Is the Moment of Update

A single book of record in metals trading means one thing operationally: the moment a physical position is entered is the moment exposure updates for every team. Trading sees it. Risk sees it. Finance sees it. All at once. All from the same ledger. No reconciliation window. No version drift between desks.

Every architectural deviation from that standard (every export step, every sync job, every aggregation layer) is a reconciliation window. And reconciliation windows are exactly when markets move.

Three concrete steps for evaluating your current infrastructure:

- Measure your reconciliation window. Time the gap between a physical position entry and the moment that position is visible in your risk manager's exposure report. That gap is the direct cost of lacking a single book.

- Map every entry point. Identify every system through which a position can enter your book. Each system that is not the book itself represents a reconciliation risk with a propagation delay attached to it.

- Evaluate your risk engine queries. Identify whether your risk engine queries live data or snapshots. If the answer is snapshots, your real-time visibility claim has a structural asterisk, and that asterisk carries a financial cost.