Metals Hedge Execution Data: Where Two Standards Diverge

The quality of your hedge execution is determined before you place the trade. Metals hedge execution data that reflects actual broker-quoted spreads across LME, COMEX, MCX, and SHFE gives traders a significantly different starting position than indicative pricing sourced from aggregated multi-commodity feeds. That difference, repeated across every hedge in a quarter, compounds into a measurable performance gap.

The distinction separates traders who structure their daily workflow around broker-accurate spread data from those who accept approximations as an operational standard.

This workflow decision, the data architecture that makes it sustainable, and the resulting execution outcomes define modern base metals practice.

The Execution Gap That Data Quality Creates

Execution quality in metals hedging is not a function of trading skill alone. According to Bank for International Settlements derivatives research from the Bank for International Settlements, transaction costs in OTC commodity derivatives markets (including metals forwards and swaps) vary by as much as 30, 50 basis points depending on the information asymmetry between counterparties at the point of execution.

That asymmetry is almost entirely a data problem.

When a trader executes a hedge without broker-accurate spread visibility, they are negotiating from an approximation. The counterparty, typically a clearing broker or bank, is not. That structural information gap has a cost, and it appears in slippage, in spread capture rates, and in the cumulative effect of repeatedly accepting execution terms that were mispriced relative to actual market conditions.

According to transaction cost analysis commodity derivatives industry analysis of commodity derivatives transaction costs, front-office traders who conduct pre-trade spread benchmarking before hedge execution reduce their average execution cost by 15, 25% compared to those relying on post-trade analysis alone.

Knowing the actual cost of execution before committing changes the decision on timing, size, and venue selection. The traders who have built this into their standard workflow are operating on a different informational foundation for every hedge, not a different market.

Why Exchange-Specific Metals Hedge Execution Data Matters

Base metals do not trade uniformly across exchanges. The LME, COMEX, MCX, and SHFE each carry structurally different spread behavior for the same underlying metal, driven by different prompt date structures, settlement mechanics, liquidity windows, and margin requirements.

According to LME market data and statistics, copper trades across cash, three-month, and 15-month contracts with spread structures that shift significantly intraday based on warrant cancellations, warehouse inventory movements, and ring session dynamics. COMEX copper carries different margin and settlement characteristics that produce different spread behavior, even when both markets price the same metal at similar absolute levels.

Using cross-exchange or blended spread data introduces basis risk at the data level, before a position is opened. For organizations running physical copper, aluminum, or zinc positions against exchange-hedged books, that basis error is systematic and accumulates without appearing in any single transaction.

Defining Broker-Accurate Spread Data

Broker-accurate spread data reflects the actual bid-ask spreads quoted by clearing brokers on a specific exchange at a specific moment, not a calculated mid-market estimate or a delayed aggregation from a data vendor. It represents the price at which execution will actually occur, not the price at which a model suggests it should occur.

As a result, indicative copper spreads on the LME at the moment of hedge execution may differ from a broker's live quote by $2, $8 per tonne depending on market conditions. For an organization running $20M, $50M in annual copper hedging volume, that spread variance is not a rounding error. It is a material execution cost difference that accumulates across every hedge in the book.

Multi-commodity platforms are built to provide the indicative layer efficiently across many markets. Depth-first metals intelligence is built to provide the broker-accurate layer specifically because base metals execution requires that precision to be practical.

The Daily Workflow Decision That Defines Execution Quality

The specific practice that separates measurably better metals hedge execution outcomes from adequate ones is checking broker-accurate spreads before hedge execution. This must happen every time as a non-negotiable step in the pre-trade process.

This straightforward procedural requirement takes under three minutes with the right data infrastructure. However, it is the step most frequently eliminated when traders operate on data environments that require navigation across multiple systems to complete it.

According to Journal of Financial Markets pre-trade TCA research published in the Journal of Financial Markets, pre-trade transaction cost analysis adoption among institutional derivatives traders correlates with a 15, 25% reduction in execution cost versus traders who do not conduct pre-trade benchmarking. The traders who show the highest adoption rate share one structural characteristic: their platform makes the check the path of least resistance.

The Frequency of Spread Data Checks

Metals traders should check broker-accurate spread data immediately before every hedge execution, not once at the start of the trading session. Spread conditions in base metals markets shift significantly throughout the day: around LME ring sessions, CME settlement windows, and Shanghai market open and close.

A spread snapshot from 9:00 AM London time does not reflect conditions at 11:30 AM during the LME second ring. Treating a morning reading as valid for afternoon execution is a systematic source of slippage that accumulates and appears in post-trade attribution as unexplained variance.

Traders who build this check into their pre-execution workflow do not treat it as a precaution. They treat it as the starting point for every hedge decision. It is the first data point that determines whether execution proceeds, waits, or adjusts in size.

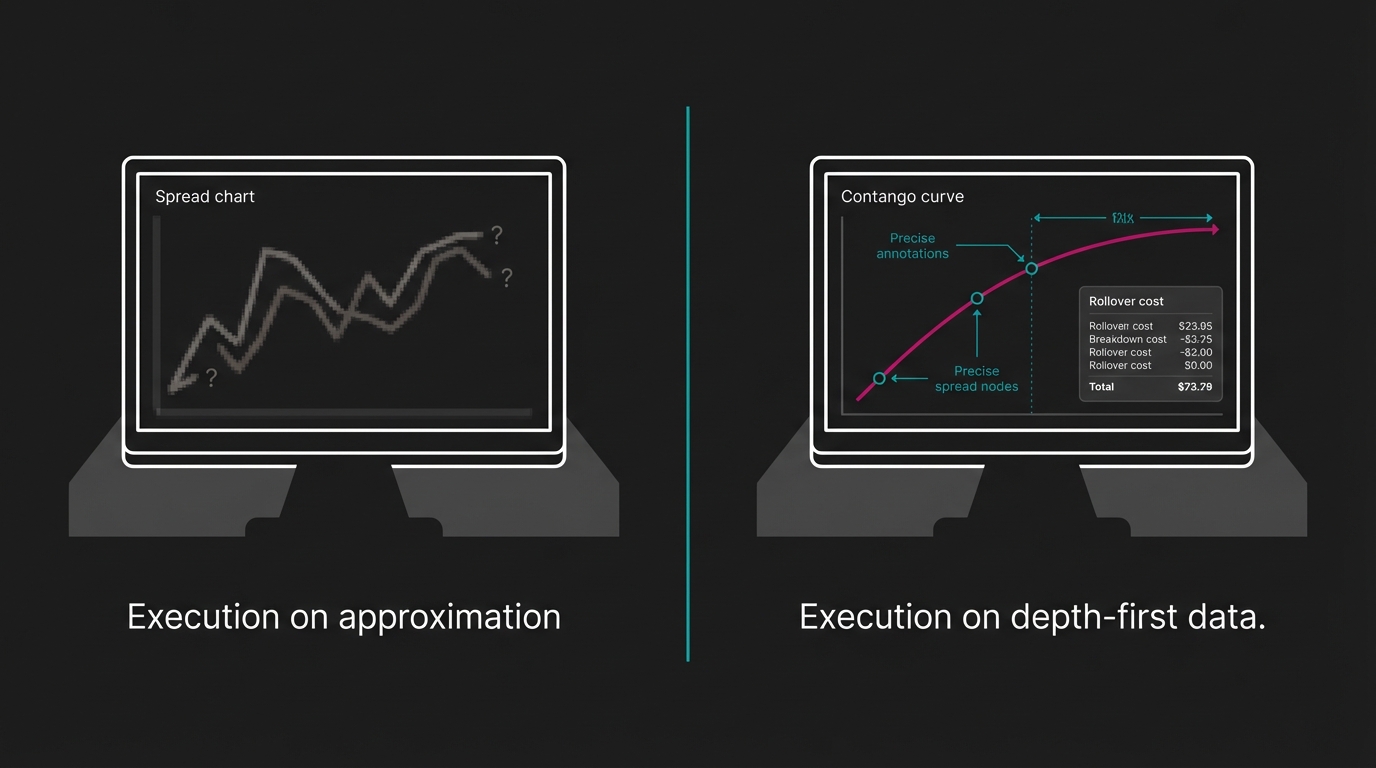

Depth-First Metals Data vs. Multi-Commodity Approximations

The platform architecture that determines whether this workflow is operationally sustainable comes down to a foundational design question: is the platform built to understand base metals specifically, or to provide adequate coverage across many commodity markets?

Multi-commodity platforms are built for breadth. According to Gartner CTRM ETRM market analysis Gartner's commodity trading and risk management platform research, the majority of commercially deployed CTRM/ETRM systems today serve 10 or more commodity classes simultaneously. That architecture requires data normalization trade-offs that reduce exchange-specific nuance to enable cross-commodity comparison.

For a trader with diversified commodity exposure, those trade-offs may be acceptable. For a front-office base metals trader running physical positions against hedged books across four exchanges, they are not. The cost of that trade-off appears in execution quality, not in a platform evaluation scorecard.

Indicative vs. Broker-Accurate Spread Data

The difference between indicative and broker-accurate spread data is the difference between a modeled estimate and a live market quote. Indicative spreads are derived from exchange feed data (typically mid-market) and represent where execution might theoretically occur. Broker-accurate spreads reflect the actual bid and offer a clearing broker would provide at that moment.

Executing a hedge using indicative spread assumptions when actual broker spreads are wider means the hedge cost exceeds what was modeled. That discrepancy, repeated across an active hedging book, represents a systematic and quantifiable drag on execution performance.

According to commodity data accuracy benchmarks analysis of multi-commodity platform spread data for base metals, indicative data deviates from broker-quoted execution prices by 8, 15% on a given trading day. This variance range scales directly with hedge size and frequency.

What Changes When You Operate on Broker-Accurate Spreads

Traders who transition from multi-commodity indicative data to depth-first broker-accurate metals hedge execution data report three consistent operational changes. None of these are behavioral in origin. All three are structural consequences of the data environment they operate on.

Pre-trade conviction improves. When spread data reflects actual execution conditions on the specific exchange and contract, the decision to execute, or to wait for better conditions, is grounded in a real benchmark. Execution decisions made on approximations carry a hidden uncertainty that only becomes visible post-trade.

Post-trade attribution becomes cleaner. According to CFA Institute post-trade analytics research on execution quality measurement, traders who maintain documented pre-trade benchmarks attribute execution variance to specific decisions at significantly higher rates than those without pre-trade records. This matters for both performance review and institutional risk reporting standards.

The workflow enforces consistent standards. A data environment that makes broker-accurate spread checks simple establishes a default operational standard. The check occurs because the infrastructure makes it automatic, not because individual discipline must sustain it under pressure every day.

The Impact of Data Quality on Execution Outcomes

Data quality affects metals hedge execution outcomes by determining the accuracy of the pre-trade cost model against which execution decisions are made. A trader sizing a hedge based on spread assumptions that are 10% wider than actual market conditions will either over-hedge relative to cost targets or accept higher-than-modeled execution costs. Neither of these outcomes is visible in the decision logic; they only appear in post-trade results.

According to Journal of Portfolio Management microstructure research on commodity market microstructure, bid-ask spreads in metals derivatives widen by an average of 35, 60% during elevated volatility periods versus normal market conditions. The cost of executing on a stale indicative spread assumption during a volatility event is proportionally higher, precisely when execution decisions carry the most weight in a trading book.

Building the Metals Hedge Execution Workflow That Holds Under Pressure

Execution workflow standards break down under predictable conditions: fast-moving markets, simultaneous position management demands, and time pressure. These are the conditions under which checking broker-accurate spreads before hedge execution is most easily bypassed. These are also the conditions under which bypassing it carries the highest cost.

According to Basel Committee operational risk commodity the Basel Committee's operational risk framework for commodity trading firms, inadequate pre-trade information is classified as a systematic operational risk factor, not a trader behavior issue. Platforms that eliminate the information gap at the workflow level address this risk structurally.

The Need for Exchange-Specific Spread Data

Metals traders need exchange-specific spread data because the LME, COMEX, MCX, and SHFE create structurally different execution environments for the same underlying metal. Each exchange has unique liquidity concentration periods, margin structures, and spread behavior that produce significantly different execution costs for identical hedge sizes.

A base metals trader applying COMEX spread assumptions to an LME copper execution will encounter a different market than their model anticipated. A trader with SHFE aluminum exposure who uses LME spread data as a proxy is not benchmarking against the venue where execution occurs. These are not edge cases. They are the normal operating conditions for any organization carrying multi-exchange base metals exposure.

The practical pre-trade workflow standard:

- Check broker-accurate spread data for the specific exchange and contract immediately before hedge initiation

- Compare live spread conditions against position-level execution cost models

- Make the timing decision to execute, wait, or adjust size based on real spread data rather than session-open assumptions

- Record the pre-trade benchmark for post-trade attribution and risk reporting

The Standard That Separates Two Measurably Different Outcomes

The professional distinction in base metals trading is not created by platform access as a credential. It is created by the daily operational decision to check broker-accurate spread data before executing hedges, and by operating on infrastructure that makes that decision automatic rather than effortful.

According to commodity trading execution performance research analysis of execution performance across commodity trading operations, firms that implement systematic pre-trade TCA workflows in metals hedging capture an estimated 10, 20 basis points of execution improvement per hedge compared to those relying on post-trade analysis alone. Across a substantial hedging book, that improvement represents a real annual P&L contribution, not from better market calls, but from better data at the moment decisions are made.

Novaex was built specifically for this workflow requirement. The depth-first methodology (mastering LME, MCX, COMEX, and SHFE across copper, aluminum, zinc, lead, nickel, and tin before expanding to additional commodity classes) exists because base metals execution data requires that level of market specificity to be practical. Integrated pricing intelligence, position management, and risk analytics in a single platform means the spread check, the position view, and the hedge decision do not require navigation between systems. That integration is the operational architecture that makes broker-accurate spread checking the default behavior, not an additional step requiring deliberate effort.

Three immediate actions for front-office metals traders:

- Audit your current pre-trade data source: Determine whether your spread data reflects broker-accurate quotes or indicative aggregations. Identify the deviation between your pre-trade assumptions and your post-trade execution records from the past quarter.

- Quantify the variance in your current book: Pull execution records and compare pre-trade spread assumptions against actual execution costs. The gap between those two numbers is the measurable operational cost of working on multi-commodity approximations.

- Evaluate whether your platform makes the check automatic: If accessing broker-accurate spreads for LME, COMEX, MCX, and SHFE requires navigating multiple systems before each hedge, the friction is a structural workflow risk that compounds every time markets move.

The standard is established. Your execution data must reflect it.