Intraday Position Limits Only Work With Real-Time MTM

#Intraday Position Limits Only Work With Real-Time MTM

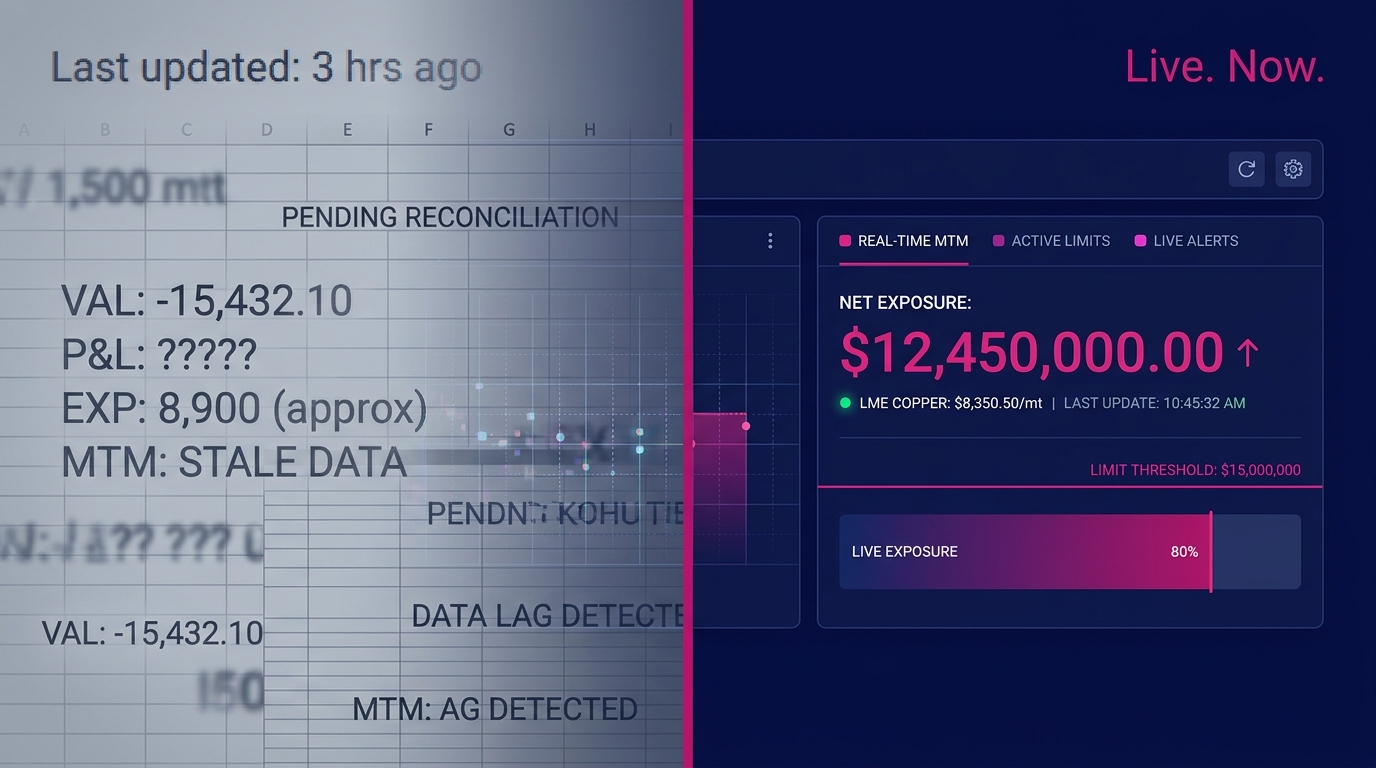

TL;DR: Limits enforced against stale mark-to-market data function as historical records of risk already taken rather than live controls. Real-time MTM serves as the operational precondition turning a position limit from a lagging indicator into a live control mechanism.

In a fast-moving metals market, the gap between a live number and a stale one determines whether a limit prevents exposure or merely documents it after the fact.

For a risk manager setting and enforcing intraday position limits, this distinction determines whether the control framework actually functions or merely appears to. Every hour that passes between valuation and decision is an hour during which actual exposure is unknown and unmeasurable without a live mark.

Why Intraday Position Limits Break Down Without Real-Time MTM

A position limit is only as useful as the number it is being enforced against. If that number reflects market prices from three hours ago, the risk manager is managing a snapshot of exposure that the market has already moved past.

A risk manager sets a position limit of $5 million notional exposure for a base metals desk. That limit was calibrated against an understood price environment. But by the time the morning batch valuation reaches the risk manager's screen, the market has moved. [LINK: LME copper intraday volatility] LME copper can move 1.5-2% in a single morning session. On a $5 million notional position, that translates to $75,000-$100,000 of untracked P&L movement before the first risk decision of the day is made.

According to the London Metal Exchange's published market data, three-month copper futures regularly experience intraday ranges exceeding 1% of contract value during periods of macroeconomic volatility, which in the current environment describes nearly every session.

The position limit has not changed. The market has. No one at the desk is working with a number that reflects both facts simultaneously.

The Impact of Delayed MTM Data on Position Limits

When MTM data is hours old, position limits lose their enforcement function because the exposure they are designed to cap cannot be measured against the limit in real time. The limit exists on paper; live exposure exists in the market. The two numbers are no longer in conversation with each other.

A trader approaching the edge of a limit may appear well inside it by the stale valuation, while live market movement has already pushed actual exposure through the threshold. This is a structural characteristic of any risk framework that does not feed live prices into its MTM engine.

This structural characteristic creates a false sense of control that is operationally more dangerous than acknowledged uncertainty.

The Real Cost of Stale MTM Data in Moving Markets

Stale MTM data systematically biases decision-making toward underestimating exposure at precisely the moments when exposure is highest.

Price discovery accelerates during periods of high information flow: macroeconomic releases, LME ring sessions, warehouse inventory announcements, and geopolitical events. These are the exact periods when intraday position management is most critical, and the exact periods when the spread between a live mark and a batch-processed mark is widest.

According to a 2022 study by the International Organization of Securities Commissions (IOSCO), firms with intraday risk reporting intervals exceeding two hours experienced materially higher instances of unplanned limit exceedances compared to firms with sub-30-minute refresh cycles. IOSCO intraday risk reporting standards The correlation was strongest during high-volatility sessions, precisely when tight limits matter most.

That gap degrades overall decision quality. Poor desk decisions often stem directly from inaccurate inputs rather than trader error.

The Relationship Between Stale Data and Trading Risk

Stale MTM data increases trading risk by creating a measurement lag between actual market exposure and reported exposure, requiring risk managers to act on information that no longer represents current conditions. In base metals, where price relationships across LME, COMEX, and SHFE can reprice materially within minutes during cross-exchange arbitrage windows, a two-hour lag can misstate multi-leg position values by significant amounts.

A desk running simultaneous long and short legs across physical and paper positions accumulates MTM errors across each position. Those errors do not cancel; depending on market direction, they aggregate into systematic under- or over-statement of net exposure.

A risk manager relying on that aggregated number for limit enforcement is working with structurally compromised data, not temporarily imprecise data.

How Real-Time MTM Changes Intraday Risk Decision Quality

Moving from batch to real-time MTM fundamentally changes the character of intraday risk decisions.

With batch valuation, a risk manager operates in a mode of periodic check-ins. The operative question is: "Where were we a few hours ago, and does that suggest we need to act?" This is retrospective risk management, appropriate for end-of-day reporting but structurally insufficient for intraday control.

With real-time MTM, the question changes to: "Where are we now, and does that require action?" This prospective risk management guarantees that a position limit can prevent an exceedance rather than document one.

Real-Time MTM and Risk Decision Quality

Real-time MTM improves risk decision quality by ensuring that every decision (whether to add to a position, reduce it, or hold) is made against an accurate current measure of exposure. While decisions can still result in losses, those outcomes stem from market conditions rather than delayed data.

This distinction carries direct operational consequence. When a limit breach occurs despite real-time data, the post-mortem is a trading decision review. When a limit breach occurs because of stale data, the post-mortem is a controls failure review, a categorically different and more damaging outcome.

According to a 2021 risk management survey by the Global Association of Risk Professionals (GARP), 61% of commodity trading firms cited data latency as a top-three contributor to intraday risk control failures. GARP commodity trading risk survey Real-time MTM guarantees that any materialized risk was known and accepted.

Real-Time MTM as a Control Mechanism

Real-time MTM serves as the operational precondition for the intraday position limit system to function as a control mechanism rather than a monitoring mechanism.

A monitoring mechanism observes and reports. A control mechanism intervenes. The operational difference between them is the latency of the feedback loop.

If the feedback loop runs on two-hour-old data, the control is merely monitoring. A position may breach a limit, be flagged in the next batch cycle, reviewed the following morning, and discussed in a risk meeting two days later. By then, the market has moved again. The breach is a historical event, not a live risk situation requiring response.

With real-time MTM as the foundation of the intraday position limit system, the feedback loop tightens to the point where limit enforcement becomes genuinely prospective. The system flags an approaching exceedance before it occurs, not after.

According to CME Group's risk management guidelines for futures clearing members, intraday margin calls are calculated using real-time position valuations, reflecting the exchange's baseline requirement that limit enforcement at the trade level demands continuous valuation. [LINK: CME Group intraday margin methodology] The exchange applies this standard to every participant trading on the exchange. The relevant question is whether the internal risk framework is built to match it.

The Hidden Costs of Delayed Valuations

The cost of delayed mark-to-market in metals trading runs through two channels: the direct cost of undetected limit breaches that result in forced position reductions at unfavorable prices, and the indirect cost of degraded decision quality when traders recognize that the risk function is operating on stale data. The second cost creates an information asymmetry between the desk and the risk function that progressively erodes the credibility of the limit framework.

When traders understand that position limits are enforced against a number that is hours old, they calibrate their behavior accordingly. The limit becomes a soft constraint, managed by timing trades around the batch cycle, rather than a hard boundary.

A real-time MTM system closes this behavioral gap by making limits unambiguous at any point during the trading session.

Setting Meaningful Intraday Position Limits Against a Live Number

Setting an intraday position limit against a real-time MTM requires a different calibration process than setting one against a batch-processed end-of-day figure.

End-of-day limits are typically structured around overnight exposure tolerances and daily VaR thresholds. Intraday position limits require a distinct framework because the operative question is: what is the maximum live exposure the desk should carry at any given moment during the session?

This requires inputs that batch systems cannot provide: live unrealized P&L by position, real-time aggregation of physical and paper positions into net exposure, and live cross-market spread valuations for multi-leg trades spanning LME, COMEX, and SHFE simultaneously. [LINK: multi-exchange base metals position management]

According to the Basel Committee on Banking Supervision's guidelines on intraday liquidity risk management, intraday exposure limits should be monitored against real-time data and subject to automated alert thresholds rather than reviewed at periodic intervals. While these guidelines formally apply to banking institutions, they define the operational standard that sophisticated commodity trading organizations apply to their own intraday risk frameworks.

Setting Intraday Position Limits

Intraday position limits in commodity trading are typically set as a percentage of daily VaR tolerance, adjusted for intraday volatility patterns specific to the markets being traded. For base metals, this requires accounting for the concentration of volatility around LME ring openings and SHFE morning sessions, when price moves are statistically larger than inter-session periods.

Effective intraday limits also distinguish between gross and net exposure. A desk with large offsetting positions may show modest net exposure while carrying significant gross exposure. This distinction matters when liquidity tightens and the ability to exit both legs simultaneously cannot be assumed.

Real-time MTM is the prerequisite for making this distinction operational rather than theoretical, because it enables gross and net exposures to be monitored simultaneously against separate thresholds throughout the session.

Implementing a Real-Time MTM Control Framework

Risk managers can immediately evaluate their process through a structured audit of the current intraday risk decision workflow.

The structured audit centers on one question: at the moment a risk-relevant intraday decision is made (whether by the trader, desk head, or risk manager) what is the age of the MTM data informing that decision?

If the answer is "up to the last batch cycle," the follow-on question is: what is the realistic price movement over that interval in the markets being traded, and what does that movement represent in dollar terms against current position sizes?

LME aluminum trades at approximately $2,200 per metric ton. A base metals desk running 1,000 metric tons of gross aluminum exposure experiences roughly $22,000 of MTM change per $1/MT price move. [LINK: LME aluminum volatility and position sizing] During a session where aluminum moves $20/MT ($20/MT is not unusual during inventory announcement windows), a two-hour batch interval creates a $440,000 window of unmeasured exposure before a single limit check occurs.

According to S&P Global Commodity Insights, base metals price volatility has increased materially since 2020, with annualized volatility for LME copper exceeding 25% in multiple quarters. In this environment, intraday measurement intervals that were operationally adequate five years ago are structurally insufficient today.

The process change has three components:

- Establish a measurement standard. Define the maximum acceptable MTM latency for intraday position limit enforcement. This risk governance decision creates the requirement that drives downstream technology needs.

- Audit current latency against the standard. Map the actual data flow from market price to position valuation to risk manager screen. Identify where batch processes, manual steps, or system handoffs introduce latency that exceeds the defined standard.

- Quantify the control gap in dollar terms. Convert the measured latency into dollar-equivalent unmeasured exposure using current position sizes and realized intraday volatility for the markets being traded. This turns an abstract data-quality problem into a concrete risk-dollar figure that supports a clear case for remediation.

From Lagging Indicator to Live Control Mechanism

Intraday position limits are among the foundational tools of commodity trading risk management. They function as controls only when the MTM data supporting them is current enough to reflect actual market conditions at the moment of enforcement.

Hours-old data creates a false sense of coverage by allowing a risk manager to operate as though limits are being enforced when they are actually being monitored against a number the market has already moved past.

Real-time MTM resolves this by ensuring that the limit and the exposure exist in the same time frame: the present.

Three concrete steps to take now:

- Run the latency audit. Map your current MTM data flow from price source to risk manager screen and calculate the dollar-equivalent exposure window your current batch interval creates against actual position sizes and recent intraday volatility.

- Reframe the internal conversation around control integrity rather than reporting features. The operative question is whether the intraday position limit system is functioning as a control mechanism or as a monitoring mechanism.

- Evaluate any CTRM/ETRM platform against this standard explicitly. Require any solution under consideration to demonstrate how it sources, processes, and delivers real-time MTM to the risk decision workflow, not just to a reporting view. CTRM platform evaluation for intraday risk