Physical Copper Basis Trading: Is Your Data Fast Enough?

TL;DR: Physical copper basis trading requires tick-level data resolution. Most generic pricing tools deliver 15-minute or end-of-day pricing updates. This specification gap converts directly into measurable P&L erosion every time the LME basis moves faster than your platform refreshes.

Physical copper is priced against the LME. While this sentence appears simple, the underlying calculation is complex.

A physical copper transaction references a specific LME prompt date, a cash-to-forward spread, a location premium or discount, and (when crossing exchanges) a currency-adjusted futures conversion. Every variable in that chain moves continuously during trading hours. If your pricing tool captures only a snapshot of that chain, you are not measuring basis. You are measuring basis as it existed at some point in the recent past.

Four technical specifications determine whether a pricing tool is fit for physical copper basis trading: data refresh interval, LME normalization depth, spread calculation method, and physical/futures cross-feed fidelity. Each is evaluated against the operational requirements of active basis management, not theoretical benchmarks or a vendor feature sheet.

Why Physical Copper Basis Trading Demands Tick-Level Resolution

The LME copper prompt structure spans cash, Tom/Next, three-month, and monthly forward dates extending up to 123 months. LME copper prompt date structure Per LME contract specifications, the standard lot size is 25 metric tonnes with a minimum price movement of $0.50 per tonne, yielding a tick value of $12.50 per lot.

During active trading sessions, LME three-month copper routinely moves $50 to $100 per tonne or more within a single session. That is not extreme volatility. That is the normal operating range for an actively traded industrial metal responding to macro data releases, SHFE overnight positioning, or Shanghai import arbitrage flows.

Defining Basis in Physical Copper Trading

Basis in physical copper trading is the difference between a physical transaction price and the relevant LME futures price for the same delivery period. It incorporates location premiums, quality differentials, exchange timing, and carry costs, repricing continuously as the underlying futures market moves.

For a front-office trader managing a physical copper book, basis tracking is a real-time workflow, not an end-of-day reconciliation task. The LME operates two ring sessions for copper each trading day at 12:00, 12:05 and 12:55, 13:00 London time, which generate the official settlement prices. LME ring session schedule The market trades continuously on LMEselect outside those windows. A pricing tool that updates only on official fixings captures roughly four price points across a six-hour active trading window.

Intraday copper basis can shift by $5 to $20 per tonne within a single 15-minute interval during active market periods. This range is consistent with observable LME behavior around macro event risk.

On a 1,000-tonne physical position (a modest transaction size for an industrial buyer or merchant), a $10 per tonne unobserved basis move represents $10,000 of unreported P&L movement. At 5,000 tonnes, the same $10 move is $50,000. Your tool will eventually capture that move on its next refresh cycle. The real risk lies in the trading decisions made in the interval between the market moving and your platform registering it.

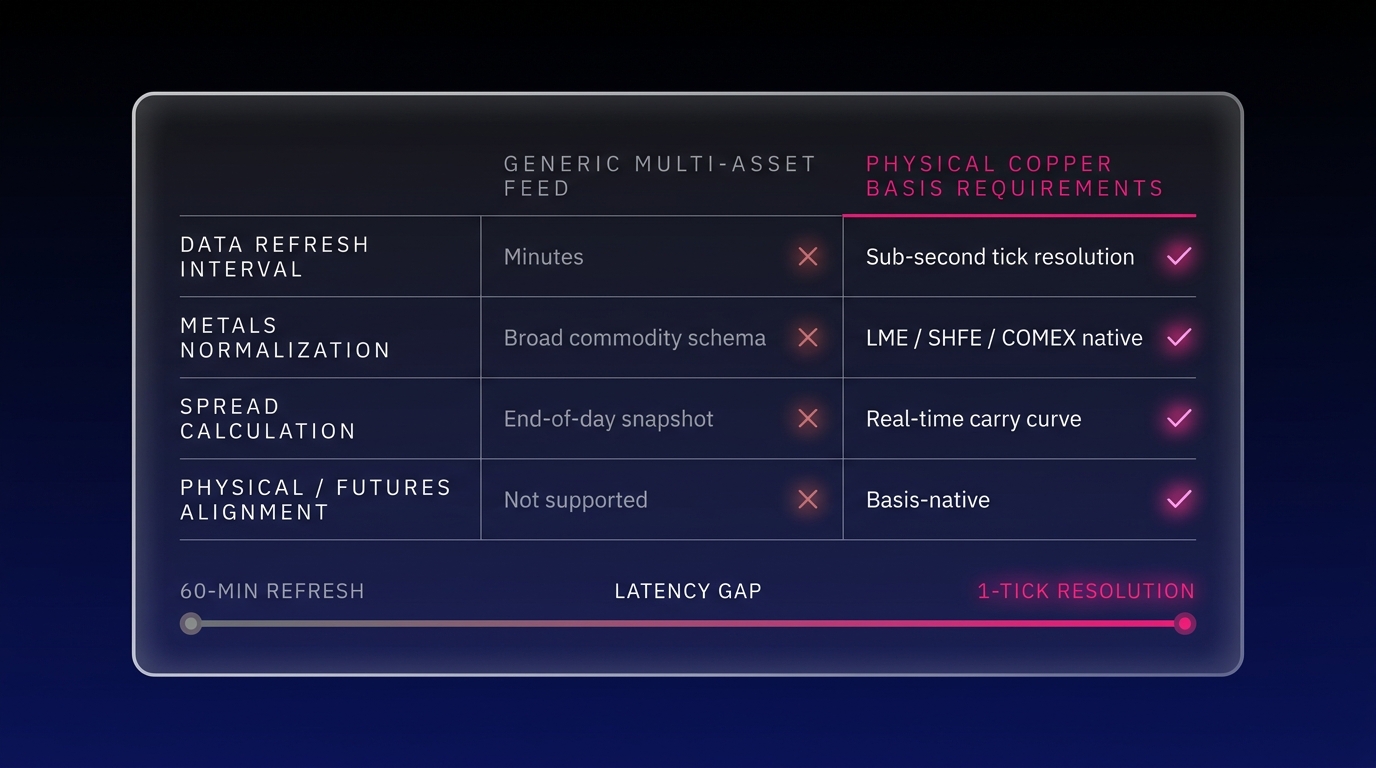

The Four Specifications That Define Adequate Coverage

Generic multi-commodity platforms are engineered for coverage breadth, not depth. Their pricing architectures are built to handle dozens of commodities with reasonable accuracy rather than a single commodity with complete fidelity. That design philosophy produces predictable specification trade-offs.

The table below maps the requirements of active physical copper basis management against the default configuration of a general-purpose CTRM pricing module.

| Specification | Generic CTRM Default | Physical Basis Requirement |

|---|---|---|

| Data refresh interval | EOD or 15-min batch | Sub-second / tick-level |

| LME normalization depth | Cash price only | Full prompt curve: cash, Tom, 3M, forward dates |

| Spread calculation method | Static official settlement | Live bid/ask mid with carry |

| Physical/futures cross-feed | Manual import, separate modules | Synchronized sub-second feed |

Each row represents a documented architecture decision made by the platform vendor. These defaults are acceptable trade-offs when copper is one commodity among fifty. They become structural liabilities when physical copper basis management is a primary function of the trading desk.

Data Refresh Interval in Physical Copper Basis Trading

Refresh Rate Requirements for LME Copper Basis Trading

For active physical copper basis management, effective data resolution requires a minimum of one update per second, and ideally tick-by-tick. Any platform refreshing at intervals longer than 60 seconds introduces structural latency into basis calculations during fast-market conditions.

This is a mandatory specification. The LME electronic platform LMEselect operates continuously from 01:00 to 19:00 London time, generating price updates throughout the day. LMEselect trading hours A platform that polls that market every 15 minutes samples approximately 25 data points across the full trading session. Tick-by-tick data from the same session may contain thousands of price revisions.

The arithmetic is direct. A 15-minute refresh interval means that at any given moment, your pricing system is running on data between 0 and 15 minutes stale, with an average staleness of 7.5 minutes across the session. In stable markets, that lag is operationally tolerable. In active markets, 7.5 minutes is the difference between the price you intended to trade and the price you actually traded.

The Cost of a 15-Minute Refresh Interval in Fast Markets

Physical copper basis decisions happen precisely when conditions are volatile: during the approach to LME ring sessions, during SHFE open and close windows, during macro data releases, and during supply disruption events.

These are the exact moments when the refresh interval gap carries its greatest consequences and when traders must act with the most urgency. A pricing tool that only performs adequately during calm periods functions as a reconciliation tool, not a basis management tool.

Reconciliation tells you what happened. Basis management tells you what is happening while there is still time to act.

LME Normalization Depth and Spread Calculation in Physical Copper Basis Trading

LME Normalization Depth in Copper Trading

LME normalization depth refers to how many points on the LME forward curve a pricing tool ingests and normalizes when calculating a copper basis position. Shallow normalization uses the LME cash price as a single proxy for all forward pricing. Deep normalization maps each physical delivery obligation to its specific prompt date on the actual forward curve.

The LME copper forward curve is not flat. The cash-to-three-month spread (trading in contango or backwardation depending on inventory conditions and financing rates) regularly ranges between $20 and $80 per tonne. LME forward curve mechanics During periods of physical tightness or squeeze conditions, that spread can widen considerably further.

Using cash as a proxy for a three-month delivery obligation introduces the full cash/3M spread as a systematic pricing error. For a portfolio carrying mixed prompt dates (the standard state of any active physical copper book), normalization depth determines whether basis calculations are accurate or structurally biased toward an incorrect reference point.

A tool that reports a single LME cash reference price is providing one number when your book requires a curve.

The Impact of Spread Calculation Methods on Basis Accuracy

Spread calculation method determines whether a tool derives basis from official settlement prices or from live bid/ask data during the continuous electronic session.

Official settlement prices are generated twice daily during LME ring sessions. Live spread calculations use the continuous bid/ask midpoint from the electronic market throughout the trading day. The difference is material for any transaction executed between fixings.

A physical copper trader executing at 14:30 London time is working with market conditions that have evolved for 90 minutes since the 13:00 official fixing. A tool pricing that transaction against the 13:00 settlement applies a reference price that is 90 minutes stale to a market that may have repriced by $20 to $30 per tonne in the interim. The counterparty operating with live market data has a complete picture of current conditions. The trader relying on a batch-priced tool does not.

Physical/Futures Cross-Feed Fidelity: The Hidden Specification

Physical/Futures Cross-Feed Fidelity

Physical/futures cross-feed fidelity is the synchronized, continuous maintenance of price relationships between a physical commodity and its derivatives hedges across multiple exchanges and currencies. For books that hedge LME copper physical with COMEX futures, or vice versa, this specification determines whether your hedge ratio reflects current market conditions or the market as it existed at the last batch update.

LME and COMEX copper contracts are not interchangeable references. The COMEX contract size is 25,000 pounds (approximately 11.34 metric tonnes) versus the LME standard lot of 25 metric tonnes. LME vs COMEX copper contract comparison They trade in the same currency but reference different delivery specifications and respond to different regional liquidity profiles.

The LME/COMEX arb relationship (the spread between these two references after size normalization) fluctuates throughout the day as relative open interest, geographic demand signals, and macro positioning shift. A tool that does not maintain continuous, synchronized conversion between these two references introduces structural basis risk into any cross-exchange hedge.

Most generic platforms handle cross-feed through manual imports or scheduled batch conversions. The feed is a periodic update that preserves the appearance of synchronized pricing while the actual spread drifts unobserved between refresh cycles.

How Cross-Feed Latency Creates Invisible Hedge Exposure

Cross-feed latency creates a gap between the hedge position your system reports and the hedge exposure you actually carry.

If the LME/COMEX arb has moved $8 per tonne since your last cross-feed update, every line item in your hedge book is marked against a stale conversion factor. On a 10,000-tonne portfolio, an $8 per tonne conversion error applied to the entire book is $80,000 of unrecognized exposure. The position appears hedged. The actual hedge efficiency is degraded by an amount proportional to the latency.

This exposure only becomes visible during reconciliation, which is too late for corrective action.

Translating the Specification Gap into a Real Trading Cost

The Real Cost of Data Latency in Basis Trading

Data latency in physical copper basis trading generates cost through three distinct mechanisms: execution mispricing, hedge drift, and delayed risk identification. Each operates independently, and all three compound during the same market condition: when copper is moving fastest.

Execution mispricing occurs when a trader prices a physical transaction against stale basis data. If the actual LME basis has moved $5 per tonne during the platform's refresh cycle and a 2,000-tonne transaction is priced against the stale figure, the result is $10,000 of systematic mispricing on a single transaction in favor of whichever counterparty had more current data.

Hedge drift accumulates when cross-feed latency allows the physical/futures spread to diverge unobserved. A position marked as 90% hedged against stale cross-feed data may carry actual coverage of 84% or 96% depending on which direction the arb has moved. This difference becomes visible only at end-of-day reconciliation, after the window to correct it has closed.

Delayed risk identification compounds both. Commodity risk management practitioners broadly recognize that the cost of late risk identification in active trading books scales non-linearly with market volatility, meaning the specification gap carries proportionally greater cost during the exact sessions where copper is most active. commodity basis risk management

The specification gap documented in the comparison table becomes material whenever copper behaves as the historical record consistently shows it does: repricing faster than batch-priced systems were designed to follow. That condition is present on most active trading days.

Conducting Your Own Specification Audit

The comparison table in this article is a starting framework, not a complete audit. If you are evaluating whether your current pricing tool meets the requirements of physical copper basis management, four questions will surface the critical gaps without requiring specialized tools or external consultants.

- What is the documented refresh interval for your LME copper price feed? If the answer is "daily," "end of day," or "official settlement," you are operating on batch pricing.

- How many prompt dates does your system normalize for copper forward curve exposure? If the answer is "we use the cash price as a reference," you have a normalization depth problem on any position that does not settle on the cash date.

- Does your spread calculation use live bid/ask data or official settlement prices? If settlement, measure the average time gap between your typical execution window and the last official fixing. That gap is your systematic spread error.

- How is your physical/futures cross-feed updated? If the answer involves manual imports, scheduled batch jobs, or anything other than a live synchronized feed, your cross-exchange hedge efficiency is not what your system currently reports.

For copper books where basis accuracy directly affects transaction pricing, hedge efficiency, and intraday risk visibility, that distinction is worth $10,000 to $80,000 per significant market move; using only the position sizes and spread ranges documented in this post. At the frequency with which copper reprices during macro event windows, "per significant market move" is not an occasional occurrence.

It is a recurring specification problem with a recurring cost attached to it.

Novaex is a depth-first commodity intelligence platform built specifically for base metals trading workflows. The specifications examined in this post (LME normalization methodology, data refresh architecture, and physical position analytics) reflect the technical standards Novaex applies across its base metals data infrastructure. These are covered in detail in our technical documentation series(Novaex base metals data architecture).