Why Metals Trading Reconciliation Breaks Happen

TL;DR: Metals trading reconciliation breaks are not random. They cluster at three predictable workflow junctions: end-of-day position aggregation, premium netting, and multi-exchange roll coordination. Each has a distinct mechanical cause rooted in architecture rather than individual performance.

If you have opened a morning P&L report and found your books out of sync with the exchange, you have experienced this pattern directly. The instinct is to locate the incorrectly entered trade. The data points elsewhere.

According to a 2023 survey by the International Swaps and Derivatives Association (ISDA), over 61% of operational breaks in commodity trading occur at repeatable workflow transition points rather than as isolated incidents distributed across the trading day. In metals specifically, the problem compounds: multiple exchanges with non-identical settlement conventions, physically deliverable contracts carrying premium components, and rolling strategies requiring coordinated position management across prompt dates.

The following analysis maps the three junctions where metals trading reconciliation breaks are most likely to occur, explains the mechanical failure at each one, and establishes why these are architectural problems rather than performance problems.

The Predictable Anatomy of Metals Trading Reconciliation Breaks

Most reconciliation workflows are built on a flawed assumption: that data flows cleanly from execution to book, from book to risk engine, from risk engine to P&L. In practice, every handoff point is a potential break.

The metals market adds structural complexity because it operates across the LME, COMEX, MCX, and SHFE, each with different settlement calendars, lot sizes, currency denominations, and prompt date conventions. LME vs COMEX settlement conventions compared

According to Oliver Wyman's 2022 Commodities Operations Report, the average commodity trading operation reconciles positions manually at least once per day, and in metals specifically, over 40% of those reconciliation cycles require at least one manual override or correction. That figure is significant not because manual overrides exist, but because they concentrate at predictable moments.

The Predictability of Metals Trading Reconciliation Breaks

A predictable reconciliation break occurs when workflow design creates a structural gap: a moment where two systems or two data streams are expected to agree but have no mechanism to guarantee agreement. These are not events that might happen. They are events that will happen under specific conditions.

The distinction matters operationally. A random error demands vigilance across all points in the workflow. A predictable failure demands targeted intervention at specific junctions. That shift from perimeter defense to junction-specific controls is what separates reactive operations teams from resilient ones.

Base metals compound this problem. LME prompt date structures create daily position changes even without new trades. LME prompt date mechanics and carry valuation A copper position entered today may carry a different value tomorrow due to carry movement and date rolling before a single new trade is executed. Reconciliation in metals is not simply about matching trade records. It is about matching a moving set of valuations across multiple dimensions simultaneously.

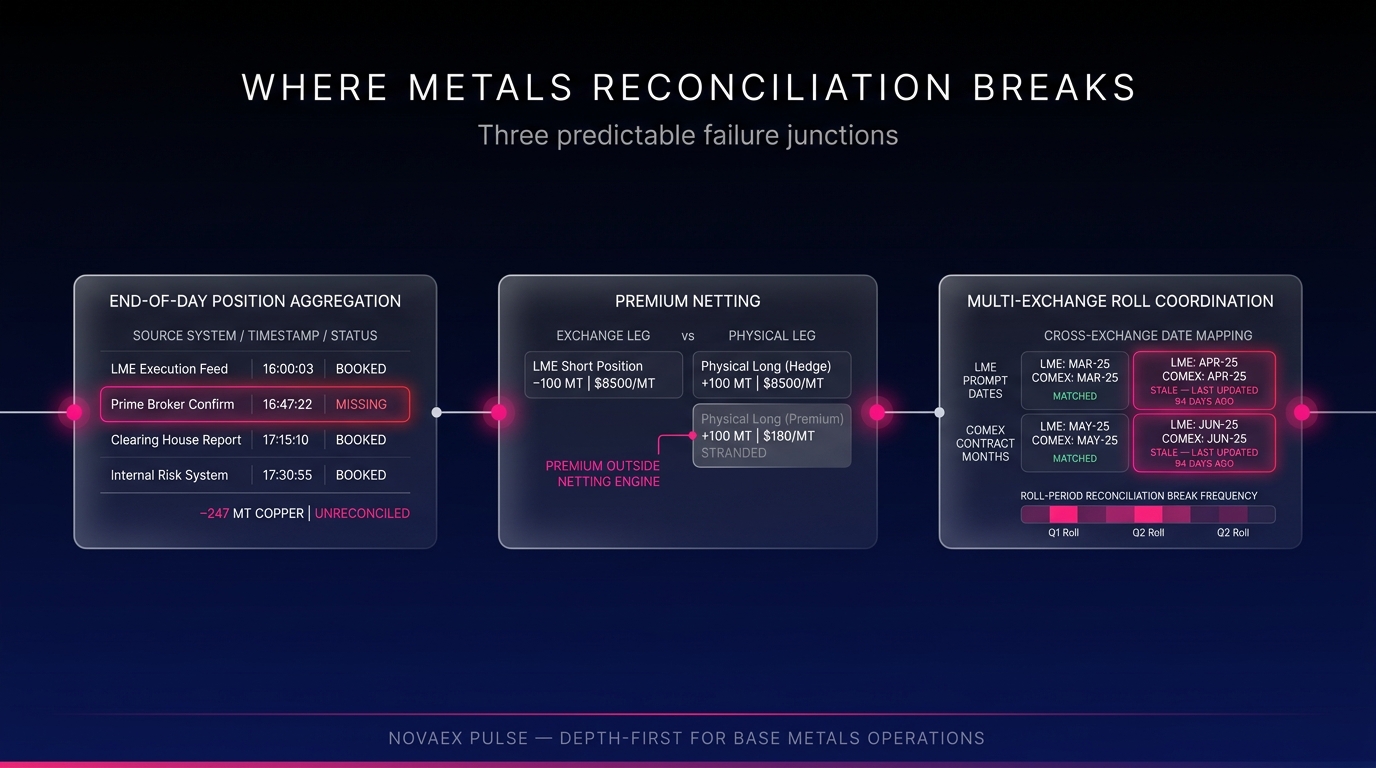

Failure Junction One: End-of-Day Position Aggregation

End-of-day position aggregation is the most common source of metals trading reconciliation breaks. The failure mechanism is precise: positions flow into an aggregation engine from multiple upstream sources (execution platforms, manual trade capture, prime broker feeds, and OTC confirmations) on different latency schedules.

According to Accenture's 2023 Capital Markets Technology Report, the average commodity trading desk integrates data from 4.7 distinct upstream systems during end-of-day processing. Each system carries its own timestamp convention, lot size normalization, and trade status definition.

The aggregation engine operates on what it has received. If a trade confirmation from a prime broker arrives after the aggregation timestamp, that position is absent from the end-of-day book regardless of when it was executed.

Causes of End-of-Day Position Reconciliation Breaks

End-of-day position reconciliation breaks occur because aggregation windows and data delivery schedules are not synchronized. When an execution system closes its position feed at 16:00 but a prime broker confirmation arrives at 16:47, the aggregation engine has already run, and that trade is absent from the day's book.

In a single-exchange equity environment, this gap is manageable. In metals, where one copper position may exist simultaneously across the LME, COMEX, and a physical OTC contract, the aggregation gap multiplies with each additional data source. The failure is not that the data is wrong. The failure is that the aggregation architecture assumes synchronous data delivery in an asynchronous trading environment.

Operational signature of this failure:

- Morning position totals do not match exchange-reported positions

- The reconciliation break resolves when a late confirmation is located

- The break recurs at approximately the same time on high-volume close days

The recurrence pattern is the diagnostic signal. When a reconciliation team regularly resolves the same type of break at the same time of day, the aggregation window (rather than the trade) is the architecture under examination.

Failure Junction Two: Premium Netting in Physical Metals Contracts

Premium netting is where metals trading reconciliation diverges sharply from financial commodity reconciliation. Physical metals contracts (copper cathode, aluminum P1020, zinc SHG) carry a physical premium component that sits outside the exchange price but within the total position value.

According to the London Metal Exchange's 2023 Annual Report, physical premiums on copper cathode ranged from $95 to $240 per metric ton across the year. LME physical premium benchmarks That variance is sufficient to materially affect P&L when netting is applied incorrectly, and most netting engines apply it incorrectly by design.

Causes of Premium Netting Discrepancies

Premium netting discrepancies occur when the system netting financial positions against physical positions treats the premium component as a separate P&L line rather than as part of the hedged position. The hedging relationship breaks at the accounting layer even when the commercial logic is intact.

A trading operation holding a short LME copper position against a long physical copper position with a $180/mt premium expects those positions to net as a hedge. If the system records the LME leg at exchange price and logs the premium separately, the netting calculation does not reflect the actual hedge relationship, and the position appears un-hedged in risk reports. This creates two failures: the reconciliation breaks and the risk report misrepresents the position simultaneously.

The specific failure mechanism:

Most CTRM systems were architected with financial contract logic as the primary framework. Physical premium components were added later, typically as secondary fields or supplementary contract types. CTRM physical contract architecture history

The netting engine was never designed to treat premium as integral to position value. It was designed to record premium. When a trader nets a physical delivery against an exchange hedge, the premium either strands in a separate P&L bucket or disappears from the position report entirely. Neither outcome reflects commercial reality.

Operational signature of this failure:

- Hedged positions show residual exposure in risk reports

- Physical delivery P&L does not reconcile with expected hedge performance

- Premium-related breaks appear consistently on delivery month positions

According to a 2022 report by Commodity Technology Advisory (ComTech Advisory), over 55% of physical commodity trading operations identify premium handling as a primary source of reconciliation complexity. ComTech Advisory CTRM benchmarking report That figure has remained stable across three consecutive annual surveys, confirming that this is a structural condition rather than a transitional one.

Failure Junction Three: Multi-Exchange Roll Coordination

Multi-exchange roll coordination is the most technically complex of the three failure junctions and the most underdiagnosed. A metals roll (moving a position from one prompt date to another) is operationally straightforward on a single exchange. Across multiple exchanges, it becomes a synchronization problem.

Consider a copper position held simultaneously on the LME and COMEX as part of a spread or basis trade. When the LME position rolls from the third Wednesday prompt to the next, the roll trade appears in the LME book. If the corresponding COMEX adjustment is not recorded at the same moment, the cross-exchange position is temporarily incorrect, and every risk report generated during that window is inaccurate.

According to the CME Group's 2023 Metals Market Overview, open interest in copper futures is distributed approximately 65% LME, 30% COMEX, and 5% across other venues. CME Group copper open interest data For operations managing cross-exchange copper positions, roll coordination is a constant operational requirement rather than an occasional one.

Roll Coordination Reconciliation Errors

Multi-exchange roll coordination creates reconciliation errors when a roll on one exchange is processed before the corresponding adjustment on another exchange has been confirmed and booked. The time gap (even measured in hours) creates a window where cross-exchange positions do not net correctly.

This is particularly acute on the LME, where prompt dates are daily and rolls may be executed multiple times per week on active positions. COMEX does not carry the same prompt date granularity, which means the mapping between LME prompt dates and COMEX contract months must be managed through a date mapping configuration, typically a static table within the CTRM system.

The failure occurs when that mapping table is not updated to account for irregular prompt dates, exchange-specific holidays, or non-standard roll windows. A static configuration applied to a shifting market structure will produce periodic misalignment without exception.

Operational signature of this failure:

- Cross-exchange position net does not balance after roll execution

- Risk reports show temporary spikes in gross exposure during roll periods

- Reconciliation team performs manual post-roll position verification as standard procedure

The institutionalization of manual post-roll verification is particularly telling. When a verification step has become standard operating procedure, the workflow is acknowledging what the architecture has already demonstrated: it cannot guarantee cross-exchange consistency independently.

Why These Reconciliation Failures Are Architectural, Not Accidental

The three failure junctions share a common origin. They were designed into the workflow rather than introduced by it.

End-of-day aggregation breaks emerge from architectures that assume synchronous data delivery in an asynchronous trading environment. Premium netting breaks emerge from systems that treat physical premium as supplementary rather than integral. Roll coordination breaks emerge from static date mapping applied to a market with shifting prompt date structures.

None of these are edge cases. They are inherent properties of the environments in which metals trading operates, and they have always been inherent properties of those environments.

According to Gartner's 2023 Technology Trends in Capital Markets report, operational data integration failures account for an estimated $2.1 billion in annual operational losses across commodity trading globally. Gartner commodity operations risk research The concentration of those losses at workflow transitions (precisely the junctions described here) is a structural finding, not a statistical anomaly.

The correct diagnostic question asks what in the architecture permitted this to happen predictably.

The Operational Cost of Treating Predictable Failures as Random Events

When a reconciliation break is treated as a random event, the operational response is investigation. When it is treated as a predictable failure, the operational response is intervention. The cost difference between those two postures is substantial.

The 2023 ISDA Operations Survey found that reconciliation investigation consumed an average of 2.3 hours per break across commodity trading operations, with metals-specific breaks averaging 3.1 hours due to cross-venue complexity. At a standard operations cost structure, a metals desk experiencing three to five reconciliation breaks per week is spending between 9.3 and 15.5 hours weekly on investigation alone before remediation begins.

Random vs. Systematic Reconciliation Failures

Random reconciliation failures distribute statistically across the trading day and workflow without clustering at specific points. Systematic failures like those at the three junctions described here cluster predictably at the same workflow transitions, on the same position types, under the same market conditions.

The diagnostic test is pattern analysis: if your reconciliation break log shows temporal or positional clustering, you are observing architectural failures, not random events. The clustering is the signal.

Systematic failures also escalate in proportion to position complexity and volume, not in proportion to execution errors. A correctly captured trade will still produce a reconciliation break if the aggregation architecture is misaligned. That is the clearest evidence that the failure is structural.

According to PwC's 2022 Commodities Operations Benchmarking Study, operations teams that categorize reconciliation breaks by structural type (rather than by trade type or counterparty) reduce average break investigation time by 34% and reduce total break volume by 22% within six months of implementing structured break analysis. PwC commodity operations benchmarking The reduction in break volume derives from targeted architecture review, not increased vigilance. That distinction is the operational payoff of structural awareness.

What Structural Awareness Changes in Metals Operations

Understanding these three failure junctions changes the nature of the reconciliation conversation from "what did someone miss" to "where does the architecture need to be rebuilt."

For operations teams, this means designing reconciliation workflows around specific failure points rather than around the end-of-day P&L cycle. It means building break investigation protocols that begin at the junction, not the trade.

For risk managers, it means reading position reports with the understanding that aggregation timing, premium handling, and roll coordination each introduce systematic gaps, and that those gaps carry a predictable signature.

Operations and risk teams can take four immediate diagnostic actions:

- Audit your end-of-day aggregation window against your latest upstream data arrival timestamps to quantify the gap between when your slowest feed arrives and when your aggregation engine runs

- Map your premium recording fields against your netting engine logic to confirm that premium is treated as integral to position value, not as a supplementary line item

- Review your cross-exchange date mapping table against current LME prompt date calendars and COMEX contract month specifications to identify any static mappings that have not been updated in the last 90 days

- Classify your last 30 reconciliation breaks by failure junction to identify clustering patterns and confirm whether your breaks are structural or genuinely random

Metals trading reconciliation breaks follow a predictable map. End-of-day position aggregation fails when data arrival is asynchronous but aggregation is timed. Premium netting fails when physical premium components are recorded outside the netting engine. Multi-exchange roll coordination fails when prompt date mapping is static in a shifting market structure.

Each failure has a mechanical cause. Each mechanical cause has a structural origin. Each structural origin can be precisely identified once the right questions are directed at the right workflow junctions.

The front-office metals trader encountering morning reconciliation breaks is not dealing with bad luck. They are operating within an architecture built before the full complexity of multi-exchange, physically deliverable base metals trading was structurally understood. base metals CTRM architecture evolution

Recognition of that fact is the starting point. The path from recognition to resolution runs through each of these three junctions when examined with clinical specificity.

Novaex is built depth-first for base metals operations. To map these failure junctions against your current workflow architecture, begin with our structured reconciliation diagnostic framework engineered specifically for LME, COMEX, MCX, and SHFE position workflows. Novaex metals reconciliation diagnostic